RSS Feed

RSS Feed by Calculated Risk on 2/12/2019 10:05:00 AM

Tuesday, February 12, 2019

BLS: Job Openings Increased to Series High 7.3 Million in December

Notes: In December there were 7.335 million job openings, and, according to the December Employment report, there were 6.294 million unemployed. So, for the ninth consecutive month, there were more job openings than people unemployed. Also note that the number of job openings has exceeded the number of hires since January 2015 (almost 4 years).

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings reached a series high of 7.3 million on the last business day of December, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were little changed at 5.9 million and 5.5 million, respectively. Within separations, the quits rate was unchanged at 2.3 percent and the layoffs and discharges rate was little changed at 1.1 percent. ...The following graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

The number of quits was little changed in December at 3.5 million. The quits rate was 2.3 percent. The quits level was little changed for total private but decreased for government (-18,000).

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for December, the most recent employment report was for January.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

Jobs openings increased in December to 7.335 million from 7.166 million in November.

The number of job openings (yellow) are up 29% year-over-year.

Quits are up 4% year-over-year. These are voluntary separations. (see light blue columns at bottom of graph for trend for "quits").

Job openings remain at a high level, and quits are still increasing year-over-year. This was a solid report.

Small Business Optimism Index decreased in January

by Calculated Risk on 2/12/2019 09:17:00 AM

CR Note: Most of this survey is noise, but there is some information, especially on the labor market and the "Single Most Important Problem".

From the National Federation of Independent Business (NFIB): January 2019 Report: Small Business Optimism Index

The NFIB Small Business Optimism Index slipped 3.2 points in January, as owners continued hiring and investing, but expressed rising concern about future economic growth. The 101.2 reading, the lowest since the weeks leading up to the 2016 elections, remains well above the historical average of 98, but indicates uncertainty among small business owners due to the 35-day government shutdown and financial market instability. The NFIB Uncertainty Index rose seven points to 86, the fifth highest reading in the survey’s 45-year history.

..

As reported in January’s NFIB Jobs Report, reports of higher worker compensation rose to the second highest level in the survey’s history to a net 36 percent of all firms. In 2018, nationwide wages increased 3.2 percent. Small business owners continue to hire at record levels, with 56 percent of owners reported hiring or trying to hire. However, 88 percent of those owners reported few or no qualified applicants for the positions.

Twenty-three percent of small business owners reported the availability of qualified labor as their top business problem

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the small business optimism index since 1986.

The index decreased to 101.2 in January.

Note: Usually small business owners complain about taxes and regulations (currently 2nd and 3rd on the "Single Most Important Problem" list). However, during the recession, "poor sales" was the top problem. Now the difficulty of finding qualified workers is the top problem.

Monday, February 11, 2019

Tuesday: Job Openings, Q4 Quarterly Report on Household Debt and Credit

by Calculated Risk on 2/11/2019 04:49:00 PM

From Matthew Graham at Mortgage News Daily: Low Rates Unfazed by a Bit of Market Weakness

Mortgage rates held their ground fairly well today, despite the fact that underlying bond markets were weaker.Tuesday:

...

All of the nuts and bolts above notwithstanding, the average lender remains in line with the lowest rates in a year. Only January 31st saw anything better, and it wasn't much better! [30YR FIXED 4.375 - 4.5%]

emphasis added

• At 6:00 AM ET, NFIB Small Business Optimism Index for January.

• At 10:00 AM, Job Openings and Labor Turnover Survey for December from the BLS. Jobs openings decreased in November to 6.888 million from 7.131 million in October.

• At 11:00 AM, NY Fed: Q4 Quarterly Report on Household Debt and Credit

• At 12:45 PM, Speech by Fed Chair Jerome Powell, Economic Development in High Poverty Rural Communities, At the Hope Enterprise Corporation Rural Policy Forum, Itta Bena, Miss.

"As more older Americans 'age in place,' millennials struggle to find homes"

by Calculated Risk on 2/11/2019 02:55:00 PM

Diana Olick at CNBC has an interesting article: As more older Americans 'age in place,' millennials struggle to find homes

With more seniors than ever aging in place and choosing not to sell the family home, an estimated 1.6 million fewer properties are now available in a market already experiencing a critical shortage, according to Freddie Mac.CR Note: If the Boomer's follow the behavior of the previous generations, many will stay in their homes ("age in place") until they are in their '80s (some until they pass away). Since the leading edge of the Boomer generation is only about 75 right now, it will still be a number of years before a large number of older people will move to retirement communities.

…

"We believe the additional demand for homeownership from seniors aging in place will increase the relative price of owning versus renting, making renting more attractive to younger generations," said Sam Khater, chief economist at Freddie Mac, who estimates that the current market needs about 2.5 million more homes to meet demand.

And, even when people move to retirement communities, many will not sell their homes. They will rent them instead - especially in the higher priced areas with significant capital gains - since they have to pay capital gains if they sell (above $250K exclusion for single, $500K for married), but the property steps up in value when they pass away. So they can leave the property to their kids with no taxes.

This could be fixed with policy changes. Either eliminate "step up" basis (take away the incentive to hold), or give older homeowners a one time unlimited exclusion (so they can sell while they are alive).

Aging in place is great for the senior, but what frequently happens, is a four bedroom house is occupied by just one person (inefficient). This is another area where zoning changes could help - let the senior sell her larger family home without tax consequences, and move to a smaller home in the same community (so they can keep their local ties).

Goldman: When Will Inflation Rise Above 2%?

by Calculated Risk on 2/11/2019 12:27:00 PM

A few excerpts from a research note by Goldman Sachs economists David Choi and David Mericle: US Daily: When Will Inflation Rise Above 2%? A View from Our Bottom-Up Model

In its January statement, the FOMC highlighted “muted inflation pressures” as a key reason to be patient in making future adjustments to interest rates. This new language further raises the burden on the inflation data to justify any potential rate hikes later this year.

Our bottom-up core PCE inflation model now projects a rise to 2.1% by end-2019. ... But the bounce above 2% is unlikely to come until the August report, not available until the FOMC’s October meeting. This adds a bit to the case for Q4 as the most likely timing of the next hike.

Oil: Rig Counts Rebounded

by Calculated Risk on 2/11/2019 10:13:00 AM

A few comments from Steven Kopits of Princeton Energy Advisors LLC on February 8, 2019:

• Oil rig counts rebounded, +7 to 854. Not surprising given last week’s big fall.

• Horizontal oil rig counts fell, -1 to 758

• The Permian lost 3, other plays were largely flat

• Breakeven to add rigs rose to $58.50 WTI compared to $52.70 WTI on the screen as of the writing of this report.

• On paper, we should see a big roll-off in rigs next week.

Click on graph for larger image.

Click on graph for larger image.CR note: This graph shows the US horizontal rig count by basin.

Graph and comments Courtesy of Steven Kopits of Princeton Energy Advisors LLC.

Sunday, February 10, 2019

Sunday Night Futures

by Calculated Risk on 2/10/2019 07:24:00 PM

Weekend:

• Schedule for Week of February 10, 2019

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures: S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were down over the last week with WTI futures at $52.44 per barrel and Brent at $61.89 per barrel. A year ago, WTI was at $59, and Brent was at $62 - so oil prices are down year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.29 per gallon. A year ago prices were at $2.58 per gallon, so gasoline prices are down 29 cents per gallon year-over-year.

Hotels: Occupancy Rate Increased Slightly Year-over-year

by Calculated Risk on 2/10/2019 10:32:00 AM

From HotelNewsNow.com: STR: US hotel results for week ending 2 February

The U.S. hotel industry reported positive year-over-year results in the three key performance metrics during the week of 27 January through 2 February 2019, according to data from STR.The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

In comparison with the week of 28 January through 3 February 2018, the industry recorded the following:

• Occupancy: +0.1% to 56.7%

• Average daily rate (ADR): +2.3% to US$124.95

• Revenue per available room (RevPAR): +2.4% to US$70.83

STR analysts note that results were more stabilized than in recent weeks as the government shutdown ended.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2019, dash light blue is 2018, blue is the median, and black is for 2009 (the worst year probably since the Great Depression for hotels).

A solid start for 2019.

Seasonally, the occupancy rate will increase over the next couple of months.

Data Source: STR, Courtesy of HotelNewsNow.com

Saturday, February 09, 2019

Schedule for Week of February 10, 2019

by Calculated Risk on 2/09/2019 08:11:00 AM

The key reports this week are January CPI and December retail sales.

For manufacturing, the January Industrial Production report and the February NY Fed manufacturing survey will be released.

No major economic releases scheduled.

6:00 AM ET: NFIB Small Business Optimism Index for January.

10:00 AM ET: Job Openings and Labor Turnover Survey for December from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for December from the BLS. This graph shows job openings (yellow line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings decreased in November to 6.888 million from 7.131 million in October.

The number of job openings (yellow) were up 16% year-over-year, and Quits were up 7% year-over-year.

11:00 AM: NY Fed: Q4 Quarterly Report on Household Debt and Credit

12:45 PM: Speech by Fed Chair Jerome Powell, Economic Development in High Poverty Rural Communities, At the Hope Enterprise Corporation Rural Policy Forum, Itta Bena, Miss.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The Consumer Price Index for January from the BLS. The consensus is for 0.1% increase in CPI, and a 0.2% increase in core CPI.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 225 thousand initial claims, down from 234 thousand the previous week.

8:30 AM: The Producer Price Index for January from the BLS. The consensus is for a 0.2% increase in PPI, and a 0.2% increase in core PPI.

8:30 AM: Retail sales for December is scheduled to be released. The consensus is for a 0.1% increase in retail sales.

8:30 AM: Retail sales for December is scheduled to be released. The consensus is for a 0.1% increase in retail sales.This graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993. Retail and Food service sales, ex-gasoline, increased by 3.6% on a YoY basis.

8:30 AM: The New York Fed Empire State manufacturing survey for February. The consensus is for a reading of 7.0, up from 3.9.

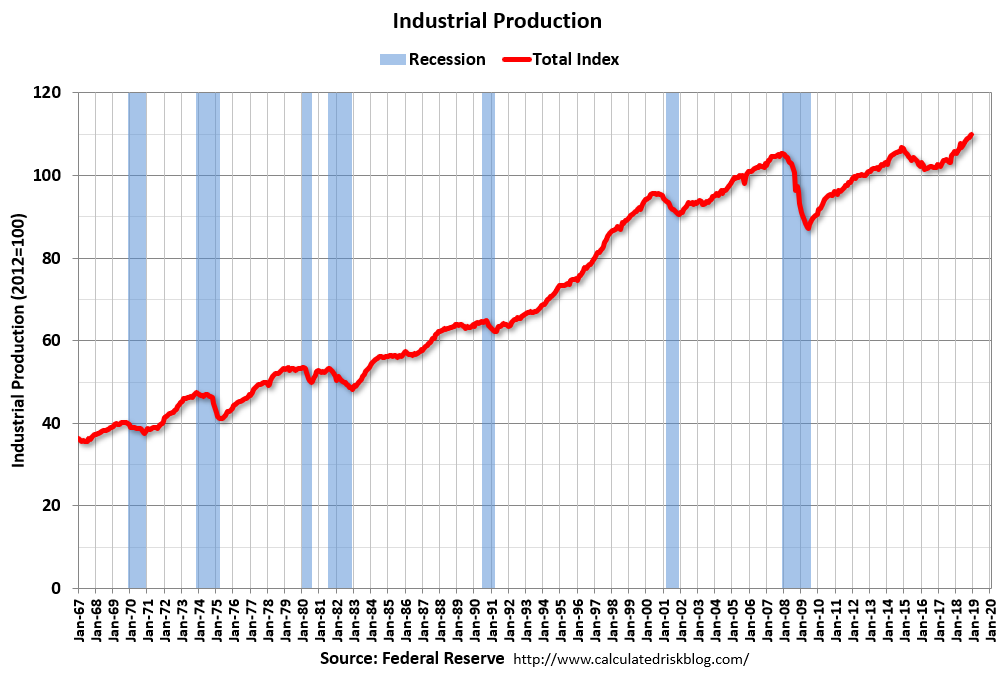

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January.This graph shows industrial production since 1967.

The consensus is for a 0.2% increase in Industrial Production, and for Capacity Utilization to increase to 78.8%.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for February). The consensus is for a reading of 92.5.

Friday, February 08, 2019

Q4 GDP Forecasts: Mid-2s

by Calculated Risk on 2/08/2019 04:09:00 PM

The BEA has announced that the Q4 advanced GDP report will be combined with the 2nd estimate of GDP, and will be released on Feb 28th.

From Merrill Lynch:

Better than expected trade data were offset by soft manufacturing inventories data, leaving our 4Q tracking estimate unchanged at 2.3%. [Feb 8 estimate]From the NY Fed Nowcasting Report

emphasis added

The New York Fed Staff Nowcast stands at 2.4% for 2018:Q4 and 2.2% for 2019:Q1. [Feb 8 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2018 is 2.7 percent on February 6, up from 2.5 percent on February 1. [Feb 6 estimate]CR Note: These estimates suggest GDP in the mid 2s for Q4.