RSS Feed

RSS Feed by Calculated Risk on 11/01/2018 12:53:00 PM

Thursday, November 01, 2018

October Employment Preview

On Friday at 8:30 AM ET, the BLS will release the employment report for October. The consensus is for an increase of 190,000 non-farm payroll jobs in October (with a range of estimates between 150,000 to 231,000), and for the unemployment rate to be unchanged at 3.7%.

The BLS reported 134,000 jobs added in September.

Here is a summary of recent data:

• The ADP employment report showed an increase of 227,000 private sector payroll jobs in October. This was well above consensus expectations of 180,000 private sector payroll jobs added. The ADP report hasn't been very useful in predicting the BLS report for any one month, but in general, this suggests employment growth above expectations.

• The ISM manufacturing employment index decreased in October to 56.8%. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll increased about 17,000 in October. The ADP report indicated manufacturing jobs increased 17,000 in October.

The ISM non-manufacturing report has not been released yet.

• Initial weekly unemployment claims averaged 214,000 in October, up from 207,000 in September. For the BLS reference week (includes the 12th of the month), initial claims were at 210,000, up from 202,000 during the reference week the previous month.

The increase during the reference week suggests a slightly weaker employment report in October.

• The final October University of Michigan consumer sentiment index decreased to 98.6 from the September reading of 100.1. Sentiment is frequently coincident with changes in the labor market, but there are other factors too like gasoline prices and politics.

• Merrill Lynch has introduced a new payrolls tracker based on private internal BAC data. The tracker suggests private payrolls increased by 200,000 in October, and this suggests employment growth slightly above expectations.

• Looking back at the three previous years:

In October 2017, the consensus was for 325,000 jobs, and the BLS reported 261,000 jobs added (bounce back from Hurricane).

In October 2016, the consensus was for 178,000 jobs, and the BLS reported 161,000 jobs added.

In October 2015, the consensus was for 190,000 jobs, and the BLS reported 271,000 jobs added.

There is no clear pattern comparing consensus to actual for October.

• The hurricanes make the forecast even less certain this month.

• Conclusion: These reports suggest a solid employment report in October. It seems likely there will be some bounce back following Hurricane Florence, but Hurricane Michael might negatively impact the report. My guess is the report will be close to the consensus.

Construction Spending increased slightly in September

by Calculated Risk on 11/01/2018 11:26:00 AM

From the Census Bureau reported that overall construction spending increased slightly in September:

Construction spending during September 2018 was estimated at a seasonally adjusted annual rate of $1,329.5 billion, nearly the same as the revised August estimate of $1,328.8 billion. The September figure is 7.2 percent above the September 2017 estimate of $1,240.4 billion.Private spending increased and public spending decreased:

Spending on private construction was at a seasonally adjusted annual rate of $1,020.4 billion, 0.3 percent above the revised August estimate of $1,016.9 billion. ...

In September, the estimated seasonally adjusted annual rate of public construction spending was $309.1 billion, 0.9 percent below the revised August estimate of $312.0 billion.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Private residential spending had been increasing - although has declined slightly recently - and is still 18% below the bubble peak.

Non-residential spending is 12% above the previous peak in January 2008 (nominal dollars).

Public construction spending is now 5% below the peak in March 2009, and 18% above the austerity low in February 2014.

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is up 5%. Non-residential spending is up 7% year-over-year. Public spending is up 11% year-over-year.

This was below consensus expectations, however spending for July and August were revised up.

ISM Manufacturing index decreased to 57.7 in October

by Calculated Risk on 11/01/2018 10:04:00 AM

The ISM manufacturing index indicated expansion in October. The PMI was at 57.7% in October, down from 59.8% in September. The employment index was at 56.8%, down from 58.8% last month, and the new orders index was at 57.4%, down from 61.8%.

From the Institute for Supply Management: October 2018 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector expanded in October, and the overall economy grew for the 114th consecutive month, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee: “The October PMI® registered 57.7 percent, a decrease of 2.1 percentage points from the September reading of 59.8 percent. The New Orders Index registered 57.4 percent, a decrease of 4.4 percentage points from the September reading of 61.8 percent. The Production Index registered 59.9 percent, a 4 -percentage point decrease compared to the September reading of 63.9 percent. The Employment Index registered 56.8 percent, a decrease of 2 percentage points from the September reading of 58.8 percent. The Supplier Deliveries Index registered 63.8 percent, a 2.7-percentage point increase from the September reading of 61.1 percent. The Inventories Index registered 50.7 percent, a decrease of 2.6 percentage points from the September reading of 53.3 percent. The Prices Index registered 71.6 percent, a 4.7-percentage point increase from the September reading of 66.9 percent, indicating higher raw materials prices for the 32nd consecutive month.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here is a long term graph of the ISM manufacturing index.

This was below expectations of 59.1%, and suggests manufacturing expanded at a slower pace in October than in September.

This was still a solid report.

Weekly Initial Unemployment Claims decreased to 214,000

by Calculated Risk on 11/01/2018 08:34:00 AM

The DOL reported:

In the week ending October 27, the advance figure for seasonally adjusted initial claims was 214,000, a decrease of 2,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 215,000 to 216,000. The 4-week moving average was 213,750, an increase of 1,750 from the previous week's revised average. The previous week's average was revised up by 250 from 211,750 to 212,000.The previous week was revised up.

emphasis added

The following graph shows the 4-week moving average of weekly claims since 1971.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 213,750.

This was slightly higher than the consensus forecast. The low level of claims suggest few layoffs.

Wednesday, October 31, 2018

Thursday: Unemployment Claims, ISM Mfg, Construction Spending

by Calculated Risk on 10/31/2018 07:44:00 PM

Thursday:

• At All day: Light vehicle sales for October. The consensus is for 17.0 million SAAR in October, down from the BEA estimate of 17.36 million SAAR in September 2018 (Seasonally Adjusted Annual Rate).

• At 8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 212 thousand initial claims, down from 215 thousand the previous week.

• At 10:00 AM: ISM Manufacturing Index for October. The consensus is for 59.1%, down from 59.8%. The PMI was at 59.8% in September, the employment index was at 58.8%, and the new orders index was at 61.8%.

• At 10:00 AM: Construction Spending for September. The consensus is for 0.3% increase in spending

Fannie Mae: Mortgage Serious Delinquency rate Unchanged in September

by Calculated Risk on 10/31/2018 04:15:00 PM

Fannie Mae reported that the Single-Family Serious Delinquency rate was unchanged at 0.82% in September, from 0.82% in August. The serious delinquency rate is down from 1.01% in September 2017.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59%.

This ties last month as the lowest serious delinquency for Fannie Mae since September 2007.

Click on graph for larger image

Click on graph for larger image

By vintage, for loans made in 2004 or earlier (3% of portfolio), 2.77% are seriously delinquent. For loans made in 2005 through 2008 (5% of portfolio), 4.90% are seriously delinquent, For recent loans, originated in 2009 through 2018 (92% of portfolio), only 0.34% are seriously delinquent. So Fannie is still working through poor performing loans from the bubble years.

The increase late last year in the delinquency rate was due to the hurricanes - there were no worries about the overall market.

I expect the serious delinquency rate will probably decline to 0.5 to 0.7 percent or so to a cycle bottom.

Note: Freddie Mac reported earlier.

Zillow Case-Shiller Forecast: Slower House Price Gains in September

by Calculated Risk on 10/31/2018 01:08:00 PM

The Case-Shiller house price indexes for August were released yesterday. Zillow forecasts Case-Shiller a month early, and I like to check the Zillow forecasts since they have been pretty close.

From Skylar Olsen at Zillow: August Case-Shiller Results and September Forecast: A Slowdown in Home Prices

The Case-Shiller home price index climbed 5.8 percent in August from a year earlier, marking the first time in 12 months that home price gains have dropped below 6 percent.The Zillow forecast is for the year-over-year change for the Case-Shiller National index to be smaller in September than in August as house price growth slows.

It’s more welcome news for would-be home buyers, who must be breathing a collective sigh of relief that home price growth finally has slowed. Softening appreciation after the rapid growth of just a few months earlier is a sign that fierce competition is dying down. Potential buyers who were intimidated during the heat of the market may find the breathing space now to make a calm, considered decision about whether to lock in a mortgage before rates rise further.

Zillow forecasts an even slower 5.5 percent annual gain for September.

Chicago PMI Decreased in October

by Calculated Risk on 10/31/2018 10:30:00 AM

From the Chicago PMI: Chicago Business Barometer Declines to to 58.4 in October

The MNI Chicago Business Barometer declined to 58.4 in October, the lowest reading since April, down 2.0 points from 60.4 in September.This was below the consensus forecast of 60.0, but still a decent reading.

Business activity continued to expand at a healthy rate this month, despite the pace of activity decelerating for the third month in a row. A decline in order book growth and unfinished orders more than offset a rise in output, delivery times and employment, sending the Barometer to its lowest reading in six months. On the year, the Barometer was down 10.7%, the biggest year-over-year fall since December 2015.

...

Hiring activity intensified this month, with the Employment indicator up for the first time since July. Firms continued to report ongoing difficulties recruiting both skilled and unskilled workers, while others prioritized retention of their existing workforce.

…

“The MNI Chicago Business Barometer continued to revert back towards trend-levels in October, cooling off after a hot and unsustainable run last year,” said Jamie Satchi, Economist at MNI Indicators.

“Production continues to be restrained by issues between firms and their suppliers, reflected by Supplier Deliveries at a 14-year high, while the latest raft of tariffs on Chinese goods appears to be exacerbating uncertainty across firms,” he added.

emphasis added

ADP: Private Employment increased 227,000 in October

by Calculated Risk on 10/31/2018 08:19:00 AM

Private sector employment increased by 227,000 jobs from September to October according to the October ADP National Employment Report®. ... The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.This was above the consensus forecast for 180,000 private sector jobs added in the ADP report.

...

“Despite a significant shortage in skilled talent, the labor market continues to grow,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute.”We saw significant gains across all industries with trade and leisure and hospitality leading the way. We continue to see larger employers benefit in this environment as they are more apt to provide the competitive wages and strong benefits employees desire.”

Mark Zandi, chief economist of Moody’s Analytics, said, “The job market bounced back strongly last month despite being hit by back-to-back hurricanes. Testimonial to the robust employment picture is the broad-based gains in jobs across industries. The only blemish is the struggles small businesses are having filling open job positions.”

The BLS report for October will be released Friday, and the consensus is for 190,000 non-farm payroll jobs added in October.

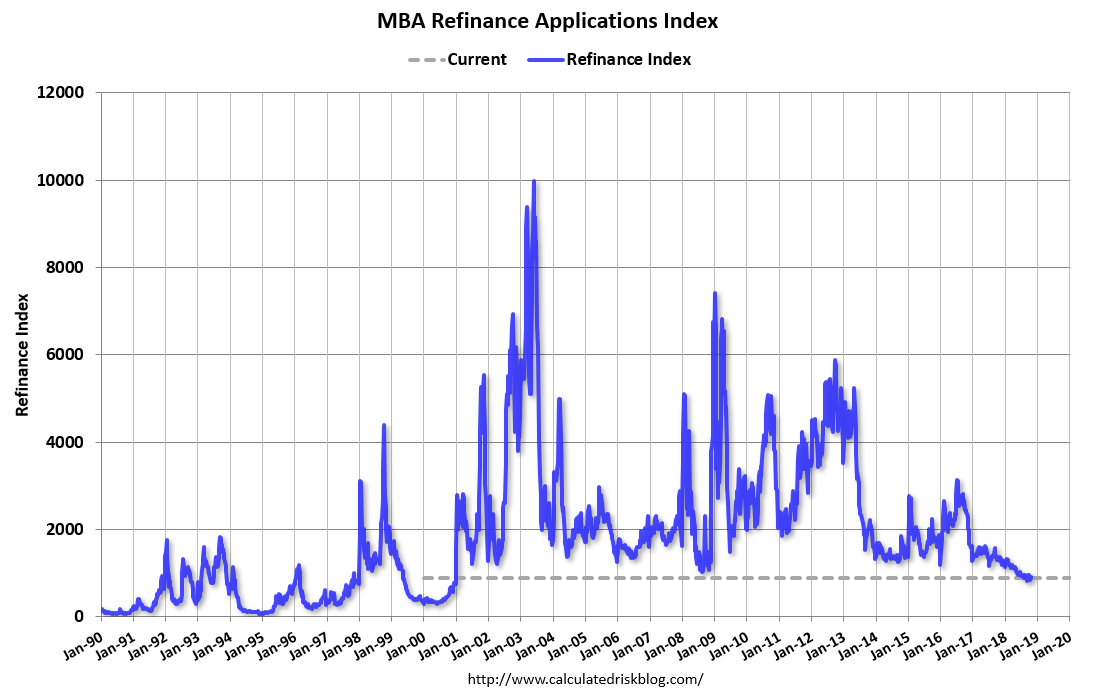

MBA: Mortgage Applications Decreased in Latest Weekly Survey

by Calculated Risk on 10/31/2018 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 2.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 26, 2018.

... The Refinance Index decreased 4 percent from the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 0.4 percent lower than the same week one year ago. ...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) remained unchanged at 5.11 percent, with points decreasing to 0.50 from 0.52 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

Refinance activity will not pick up significantly unless mortgage rates fall 50 bps or more from the recent level.

The second graph shows the MBA mortgage purchase index

The second graph shows the MBA mortgage purchase index According to the MBA, purchase activity is down 0.4% year-over-year.