RSS Feed

RSS Feed by Calculated Risk on 8/30/2010 11:29:00 PM

Monday, August 30, 2010

Europe Bond Yields

Usually I just post the bond spreads in Europe, but I think this excellent tool from Bloomberg shows visually what is happening with bond yields in Europe. Click on graph for larger image in new window.

Click on graph for larger image in new window.

You can click here for the graph for the Greece 10 year bond yields. Then you can add other bonds for comparison.

This is a 3 year graph from Bloomberg.

Where it says "Add a comparison" you can enter the symbols for Germany (GDBR10:IND) and then Ireland (GIGB10YR:IND) to create this graph.

Here are the symbols for Portugal (GSPT10YR:IND) and Spain (GSPG10YR:IND) too (not graphed). Nemo has links for more countries on the sidebar of his site.

Starting in 2008 the bond yields started to separate - with Greece and Ireland paying more. Then in May of this year, the situation reached crisis levels. And now the spreads are steadily widening again - as the German bond yields have fallen recently (like the U.S. yields) and the Irish and Greek bond yields have been increasing.

Gibbs: Housing Tax Credit not high on list of options

by Calculated Risk on 8/30/2010 08:33:00 PM

From the Press Briefing by Press Secretary Robert Gibbs

Q: A lot of folks have been talking about the first-time homebuyers tax credit sort of propping up the housing market. Is that one of these new measures that he might be considering?And a "hoocoodanode" moment too:

MR. GIBBS: Look, obviously, there was -- that was something that was done originally. I don't -- while I have not see, obviously, a final list, that is -- I think bringing that back is not on -- is not as high on the list as many other things are.

Q: In retrospect, was the stimulus too small?How about Christina Romer (

MR. GIBBS: Look, we always -- I think it makes sense to step back just for a second. If you look at -- and I don't think anybody had -- and I think we’d be the first to admit that nobody had, in January of 2009, a sufficient grasp at the sheer depth of what we were facing. I think that's, quite frankly, true for virtually every economist that made predictions.

the chair of the Council of Economic Advisers)? From Ryan Lizza at the New Yorker:

At the December [2008] meeting, it was Romer’s job to explain just how bad the economy was likely to get. “David Axelrod said we have to have a ‘holy-shit moment,’ ” she began. “Well, Mr. President, this is your ‘holy-shit moment.’ It’s worse than we thought.” She gave a short tutorial about what happens to an economy during a depression, what happened during previous severe recessions, and what could happen if the Administration didn’t act. She showed PowerPoint slides emphasizing that the situation would require a bold government response.So Romer thought the right size was probably about double what was actually enacted (excluding the Alternative Minimum Tax relief).

...

The most important question facing Obama that day was how large the stimulus should be. Since the election, as the economy continued to worsen, the consensus among economists kept rising. ... Romer had run simulations of the effects of stimulus packages of varying sizes: six hundred billion dollars, eight hundred billion dollars, and $1.2 trillion. The best estimate for the output gap was some two trillion dollars over 2009 and 2010. Because of the multiplier effect, filling that gap didn’t require two trillion dollars of government spending, but Romer’s analysis, deeply informed by her work on the Depression, suggested that the package should probably be more than $1.2 trillion.

Lawler: HUD Secretary May Have Just Made Near-Term Home Sales Worse

by Calculated Risk on 8/30/2010 04:53:00 PM

CR Note: Here are economist Tom Lawler's thoughts on HUD Secretary Shaun Donovan comments this weekend ...

In an interview with CNN over the weekend, HUD Secretary Donovan noted that the July plunge in home sales following the end of the federal home buyer tax credit was much sharper than the administration expected; that the administration was “very concerned,” and would “do everything we can” to stabilize the shaky housing market. While he said that “it's too early to say after one month of numbers whether the tax credit will be revived or not,” he also said that "we're going to be focused like a laser on where the housing market is moving going forward, and we are going to go everywhere we can to make sure this market stabilizes and recovers."

Many folks appear to have interpreted Donovan’s remarks as meaning that the administration has not “ruled out” reviving the home buyer tax credit if home sale continue to be weaker than expected, thus confirming some potential home buyers’ views that it’s better to wait to buy a home until the government “does it again.” While follow-ups by CNBC got a comment from a HUD spokesperson that there was “(n)o news here … there are no discussions underway to revive the credit,” in fact to some potential home buyers there was in fact news: the administration’s housing spokesperson said that if housing remains weak, the administration may revive the federal home buyer tax credit!!! CNBC even speculated that the next one might include a credit not just for “first time/move-up (sic) buyers, but a credit for buyers purchasing foreclosed properties or short sales” as well (though CNBC gave no supporting evidence for such a move, and I’m guessing they “made this up.”).

As best as I can tell Secretary Donovan was in New Orleans giving interviews on the “Katrina” anniversary, but CNN’s reporter focused first on housing and the possibility of a “double dip.” and Donovan appeared to be “winging it.”

Nevertheless, Donovan’s comments, and the press reports that followed, could well lead many a prospective home buyer to hold off on buying a home because another tax credit might be coming – which, of course, would lead to weaker than otherwise home sales, which Donovan implied might lead the administration to consider reviving the home buyer tax credit!!!!!! A few realtors and home builders have noted that a few potential buyers have already been citing the possibility of a “revival” of the tax credit as a reason for them “holding off” buying now.

The home buyer tax credit, of course, was an enormously costly and inefficient program where many home buyers who would have purchased a home anyway got a tax credit for doing so. Estimates vary, but the 2009-2010 tax credits probably will “cost” the government in terms of lost revenue somewhere in the neighbor of $26-28 billion. While to some that might not seem like “a lot,” it’s about equal to the combined SF REO carrying value of Fannie, Freddie, and FHA (the latter of which I am estimating)!!! Imagine if the government, rather than enacting yet another costly and ineffective tax credit, instead spent a fraction of the probable cost on more effective REO management, including perhaps a program to rehab and rent out such properties instead of “dumping ‘em” on the market!

Already there are news headlines along the lines of “Homebuyer Tax Credit Back in Play?,” “Another Home Buyer Tax Credit?, and “A Revival of the Homebuyer Tax Credit?,” and right after Donovan’s interview two (whacky) Florida Senate candidates both said they would heartily support a home buyer tax credit “revival.”

If in fact there is “no news here” – and good God I hope administration officials realize that giving potential home buyers the notion that a home buyer tax credit MIGHT be revived will absolutely and unequivocally depress home sales over the next several months – the administration should have Donovan or another HUD spokesperson explicitly state that there is no plan to revive the home buyer tax credit in the foreseeable future – and they should do this SOON!!!!

CR Note: This was from economist Tom Lawler.

Report: No discussions underway to revive housing tax credit

by Calculated Risk on 8/30/2010 02:33:00 PM

Last night I posted some comments from HUD Secretary Shaun Donovan. From CNN's "State of the Union" transcript:

[CNN's Ed] HENRY: Is that housing credit now dead? Or does the administration think you should try to revive it to try to prop this industry up?Diana Olick at CNBC contacted HUD today: Another Home Buyer Tax Credit?

DONOVAN: Look, Ed, I think it's too early to say after one month of numbers whether the tax credit will be revived or not. All I can tell you is that we are watching very carefully.

[A] HUD spokesperson ... responded: "No news here...there are no discussions underway to revive the credit."Hopefully the tax credit is done.

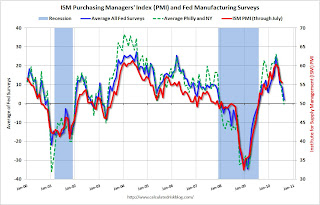

Regional Fed Manufacturing Surveys and the ISM PMI

by Calculated Risk on 8/30/2010 11:39:00 AM

Now that all the regional Fed manufacturing surveys for August have been released, here is an update to the graph I posted last week: Click on graph for larger image in new window.

Click on graph for larger image in new window.

For this graph I averaged the New York and Philly Fed surveys (dashed green), and averaged five surveys including New York, Philly, Richmond, Dallas and Kansas City (blue).

The Institute for Supply Management (ISM) PMI (red) is through July (right axis).

ISM PMI for August will be released on Wednesday at 10 AM ET. The consensus is for a decline to 53.0 from 55.5 in July.

Based on the regional surveys, it appears that the PMI will decline in August - but will probably still be above 50 (indicating expansion in August).

Dallas Fed: Texas Manufacturing Activity Still Weak in August

by Calculated Risk on 8/30/2010 10:33:00 AM

From the Dallas Fed: Texas Manufacturing Activity Still Weak

Texas factory activity was unchanged in August, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, came in at zero, posting a third consecutive month of little to no growth.This is the last of the regional Fed surveys for August, and they all showed manufacturing slowing or even contracting.

Most other indexes for current activity remained negative in August. The new orders index stayed at –9, implying incoming orders continue to fall. The capacity utilization and shipments indexes pushed deeper into negative territory, suggesting further contraction of business.

...

The employment index turned negative for the first time in six months, largely due to the share of firms reporting layoffs rising from 15 percent in July to 23 percent in August, and hours worked contracted again.

The national ISM manufacturing survey will be released on Wednesday.

Personal Income, Spending increase in July

by Calculated Risk on 8/30/2010 08:30:00 AM

From the BEA: Personal Income and Outlays, July 2010

Personal income increased $30.0 billion, or 0.2 percent ... Personal consumption expenditures (PCE) increased $44.1 billion, or 0.4 percent

...

Real PCE -- PCE adjusted to remove price changes -- increased 0.2 percent in July, compared with an increase of 0.1 percent in June.

...

Personal saving as a percentage of disposable personal income was 5.9 percent in July, compared with 6.2 percent in June.

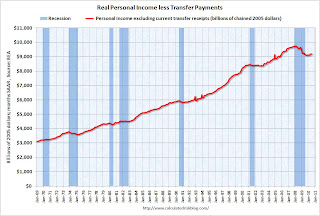

Click on graph for large image.

Click on graph for large image.This graph shows real personal income less transfer payments since 1969.

This measure of economic activity is moving sideways - similar to what happened following the 2001 recession.

This month the saving rate decreased slightly ...

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the July Personal Income report. The saving rate decreased to 5.9% in July from 6.2% in June (flat at 6.1% using a three month average).

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the July Personal Income report. The saving rate decreased to 5.9% in July from 6.2% in June (flat at 6.1% using a three month average). I expect the saving rate to rise further - perhaps to 8% or more.

The increase in income was good news, but personal income less transfer payments are still only 1.2% above the low of last year - and still 5.5% below the pre-recession peak.

Sunday, August 29, 2010

Another Housing Tax Credit?

by Calculated Risk on 8/29/2010 09:17:00 PM

From Reuters: No Decision on Reviving Homebuyer Credit: Donovan

"It's too early to say whether the tax credit will be revived," Donovan said in an interview on CNN's "State of the Union" program. He said the administration would "do everything we can" to stabilize the shaky U.S. housing market.The problem in housing is there is too much supply (at the current price). Incentivizing people to buy existing homes just shuffles households around - it does NOT reduce the overall supply unless the buyer is moving out of their parent's basement. I doubt that happened very often. Note: It is important to remember that rental units are part of the overall supply, so moving people from a rental unit to homeownership doesn't help.

And if the tax credit leads to more new home sales - that ADDS to the excess supply. And that makes the situation WORSE.

It would be far better for housing and the economy to announce "There will be no further housing tax credits."

Earlier today:

Foreclosures: Movin' on up!

by Calculated Risk on 8/29/2010 06:19:00 PM

This is a something we've been watching for some time ...

From Lauren Beale at the Los Angeles Times: Foreclosures of million-dollar-plus homes on the rise

Although the pace of foreclosures has slowed in the general housing market in Southern California and much of the nation, it's still rising for upper-tier homes.Earlier today:

The number of homes in the $1-million-and-up slice of the market that have become bank owned has tripled in the second quarter compared with the same period three years earlier in Los Angeles County, which has the majority of Southern California's high-priced REO houses. And the trend has shown little sign of slowing, according to data from ForeclosureRadar.

...

"We believe the high end is ready to fall apart," [Bryan Ochse of Media West Realty in Burbank, which works with 11 lending institutions and specializes in REO sales] said.

Schedule for Week of August 29th

by Calculated Risk on 8/29/2010 12:55:00 PM

This will be another busy week - the August employment report on Friday is the key economic release this week.

The previous post is the summary of last week.

8:30 AM ET: Personal Income and Outlays for July 2010. The consensus is for a 0.3% increase in both income and spending (compared to June). The core PCE Price Index is expected to increase 0.1%.

10:30 AM Dallas Fed Manufacturing Survey for August. The consensus is for a decrease in the index to flat (neither expanding or contracting) from 5 last month. These regional surveys are important now since it appears manufacturing is slowing (or contracting like the Philly Fed survey showed).

9:00 AM: S&P/Case Shiller Home Price Index for June (3 month average). The consensus is for prices to be mostly flat in the June report.

9:45 AM Chicago Purchasing Managers Index (PMI) for August. The consensus is for a decline to 56.0 from 62.3 in July.

10:00 AM Consumer confidence index from the Conference Board for August. The consensus is for a slight increase to 51.0 from 50.4.

2:00 PM: FOMC Minutes, Meeting of August 10, 2010

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index has been fairly flat over the last couple of months - suggesting reported existing home sales in August will not be much stronger than in July.

8:15 AM: ADP Employment Report for August. This report is for private payrolls only (no government). The consensus is for +20,000 payroll jobs in August, down from +42,000 in July.

10:00 AM: ISM Manufacturing Index for August. The regional Fed reports suggest a decline in the ISM manufacturing index. The consensus is for a decline to 53.0 from 55.5 in July.

10:00 AM: Construction Spending for July. The consensus is for a 0.6% decline in spending.

4:00 PM (approx): Light Vehicle Sales for August. The various manufacturers will report August sales in the morning. Usually around 4 PM I post an estimate of SAAR for the month. The consensus is for sales of 11.6 million, about the same as in July.

NOTE: There is a conference on Wednesday and Thursday in Washington, D.C. at the Federal Reserve: Federal Reserve REO and Vacant Properties Summit

8:30 AM: The initial weekly unemployment claims report will be released. Consensus is for a slight decrease to 470K from 473K last week. The increase in weekly claims is very concerning and the 4-week average is at the highest level since last November.

8:30 AM: Nonfarm Productivity for Q2 (Final)

10:00 AM: Manufacturers' Shipments, Inventories and Orders for July.

10:00 AM: Pending Home Sales Index for July. The consensus is for a slight increase (about 1.5%) in contracts signed. This index declined 2.6% in June (after collapsing in May). It usually takes 45 to 60 days to close, so this will provide an early indication of closings in September.

8:30 AM: Employment Report for August. The consensus is for about a loss of 90,000 payroll jobs, with 116,000 fewer Census jobs, or about +26,000 ex-Census increase in payrolls. The consensus is for the unemployment rate to increase slightly to 9.6% from 9.5% in July. For a preview, see: Will the unemployment rate spike higher?

10:00 AM: ISM Non-manufacturing Index for August. The consensus is for a decrease in the service index to 53.0 from 54.3 in July.

After 4:00 PM: The FDIC will probably have another busy Friday afternoon ...

Expected early in the week: Q2 Quarterly Banking Profile from the FDIC.

Expected on Thursday: August Personal Bankruptcy Filings