RSS Feed

RSS Feed by Calculated Risk on 5/10/2008 08:09:00 PM

Saturday, May 10, 2008

UK: Home repossessions to double

From The Times: Home repossessions to double this year for mortgage defaulters

The number of people who are losing their homes because they cannot meet rising mortgage bills is set to double this year, experts said yesterday.Hmmm ... 27 thousand foreclosure orders in the first quarter is a 108 thousand annual pace. And the problem seems to be getting worse each quarter. I'm not sure the present level of foreclosure activity is that far below 1991 in the UK.

...

The number of repossession orders granted in England and Wales in the first three months of the year climbed to levels not seen since the early 1990s, reaching 27,530.

...

Experts also urged a sense of perspective, pointing out that the present level of repossessions remains considerably below the peak of 75,540 homes seized during 1991, at the peak of the last recession. About 142,900 repossession orders were made that year.

LA Times: ‘walkaway’ may be suburban myth

by Calculated Risk on 5/10/2008 02:23:00 PM

A follow up to Tanta's post this morning, from Michael Hiltzik at the LA Times: In mortgage meltdown, ‘walkaway’ homeowners may be suburban myth (hat tip Dagny)

Bankers and housing market analysts are warning of a chilling new trend in the mortgage world: Homeowners voluntarily defaulting on their loans even though they can actually afford to make the payments.I nominate Michael Hiltzik honorary UberNerd!

...

At Fannie Mae, the government-chartered company that owns or guarantees billions of dollars in home mortgages, Senior Vice President Marianne Sullivan conceded that there was growing "folklore" about residential walkaways but said that the phenomenon was more likely connected to investors than people who live in their homes, or "owner-occupants."

...

Bruce Marks, CEO of Neighborhood Assistance Corp., a Boston-based nonprofit agency that helps strapped homeowners, says flat out that the notion that legions of borrowers are simply deciding not to pay is an "urban myth" that largely reflects the mortgage industry's desire to blame homeowners, rather than their lenders, for the surge in problem loans.

P.S. and kudos to Tanta: Let's Talk about Walking Away

A Skeptical Look At Walk Aways

by Anonymous on 5/10/2008 10:53:00 AM

In the New York Times, too! I think we're going to have to make Vikas Bajaj an honorary UberNerd.

Millions of Americans are “upside down” on their mortgages — they owe more on their homes than their homes are worth. So far, however, there is little evidence that people who have the means to pay are walking away from their homes as values sink.I think this is my favorite part:

The blogosphere is full of tales of homeowners who supposedly are choosing to mail the house keys to their lenders rather than keep their depreciating homes. And yet “jingle mail,” the term for those tinkling packages of keys, appears to be far rarer than many seem to think.

Jon Madux, a founder of the site YouWalkAway.com, which helps borrowers leave their homes, said a majority of the site’s clients default because of financial hardships. But in the Southwest and Florida, more of its customers are investors who bought multiple condos or houses and are now not able to find renters or sell for more than they owe.Speculators always cave in quickly in a declining market, especially when they weren't required to make a down payment and the rents were never realistic. This, we always knew. It does not constitute a "sea change" in borrower behavior, whatever the hoocoodanode crowd wants you to believe.

The interesting question is why this insistence that walk-aways are widespread is being, apparently, pushed by real estate brokers (they and some mortgage brokers seem to be the sources for most of the claims I've read in this regard).

“These markets are driven by psychology,” Mr. Barry [the real estate agent] said. “If people see that the market will continue to decline and they are already in the hole by 50 to 100 grand” they will leave.Is it just the salesperson's preference for "psychology" as the all-purpose explanation? Classic projection? An attempt to spook the banks into negotiating with borrowers who wouldn't, typically, qualify for a workout? I'd really like to know.

Friday, May 09, 2008

Bank Failure: Some details on ANB Financial

by Calculated Risk on 5/09/2008 08:00:00 PM

The FDIC closed ANB Financial today with an estimated $214 million hit to the FDIC insurance pool (see previous post). Here are some details from an article earlier this week.

From ArkansasBusiness.com: ANB Past Dues Up 58 Percent (hat tip Steve)

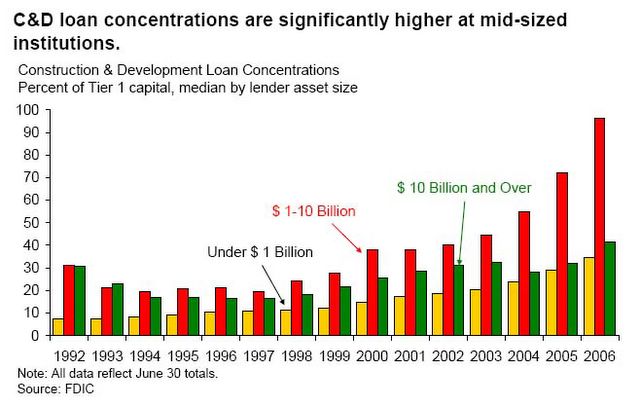

... ANB Financial's loans that are 30 days or more past due were valued at $614.6 million as of March 31, up 58.3 percent from Dec. 31.These small to mid-size institutions mostly missed the residential boom and bust because most residential loans they originated were sold to Wall Street. Instead they focused on construction and development (C&D) and commercial real estate (CRE) loans.

The Bentonville bank's total loan portfolio is about $1.57 billion, so 51 percent of its loans are considered delinquent on one level or another. The majority of those loans - $589.3 million - have been moved all the way into nonaccrual status. A year ago, the bank had $57.9 million in loans that were not accruing interest.

Most of the bank's loans, 77.4 percent, were considered construction and development loans, and 94 percent of the loans are tied to real estate.

C&D loans are especially dangerous. A developer will usually borrow enough to complete the project and make the interest payments, so during development they stay current. However when the developer completes the project - and they can't sell the units - they suddenly stop paying the loan. Notice how the nonaccrual loans increase ten fold over the last year!

Note: for some reason the FDIC hasn't released an "emerging risks" report since late 2006.

So, from 2006: Look at the concentration of C&D loans in late 2006 (from the FDIC Semiannual Report: Economic Conditions and Emerging Risks in Banking):

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loanAnd that was in late 2006; C&D and CRE lending really went crazy in 2007.

concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.

Here come the C&D failures.

Bank Failure: ANB Financial Costs FDIC $214 million

by Calculated Risk on 5/09/2008 06:19:00 PM

Did someone say "bank failure" this morning?

From the FDIC: Bank Closing Information for ANB Financial, NA, Bentonville, AR

ANB Financial, National Association, Bentonville, Arkansas, was closed today by the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation (FDIC) was named receiver. To protect depositors, the FDIC's Board of Directors approved the assumption of the insured deposits of ANB Financial by Pulaski Bank and Trust Company, Little Rock, Arkansas.

The failed bank's nine offices will reopen Monday as branches of Pulaski Bank and Trust Company. Depositors of ANB Financial will automatically become depositors of the assuming bank.

As of January 31, 2008, ANB Financial had approximately $2.1 billion in assets and $1.8 billion in total deposits. Pulaski Bank and Trust Company will assume $212.9 million of the failed bank's insured non-brokered deposits for a premium of 1.011% and will purchase $235.9 million of assets.

At the time of closing, ANB Financial had approximately $39.2 million in 647 deposit accounts that exceeded the federal deposit insurance limit. These customers will have immediate access to their insured deposits, and they will become creditors of the receivership for the amount of their uninsured funds.

ANB Financial also had approximately $1.6 billion in brokered deposits that are not part of today's transaction. The FDIC will pay the brokers directly for the amount of their insured funds.

Over the weekend, all deposit customers can access their insured money by writing checks, or by using their debit or ATM cards. Checks drawn on the bank that did not clear before today will be honored up to the insured limit.

...

In addition to assuming the failed bank's insured deposits, Pulaski Bank and Trust Company will purchase approximately $235.9 million of the failed bank's assets. The assets are comprised mainly of cash, cash equivalents and securities. The FDIC will retain the remaining assets for later disposition.

The transaction is the least costly resolution option, and the FDIC estimates that the cost to its Deposit Insurance Fund is approximately $214 million.

FedEx Lowers Earnings Guidance

by Calculated Risk on 5/09/2008 04:13:00 PM

FedEx Corp. today announced that earnings for the fourth quarter ending May 31, 2008 are expected to be in the range of $1.45 to $1.50 per diluted share, compared to the previous forecast of $1.60 to $1.80.Mostly an oil related warning.

“Since we provided earnings guidance for the fourth quarter in March when the crude oil price was slightly above $100 per barrel, our estimated fuel costs for the quarter have increased more than 7 percent, or $100 million from our previous estimate, and the weak economy has restrained demand for U.S. domestic express package and LTL freight services,” said Alan B. Graf, Jr., FedEx Corp. executive vice president and chief financial officer. “While we have dynamic fuel surcharges in place, they cannot keep pace in the short-term with rapidly rising fuel prices. This revised outlook assumes no additional increases to the current fuel price environment and no further weakening of the economy.”

Economist.com on Rents and House Prices

by Calculated Risk on 5/09/2008 01:53:00 PM

The Economist has a great overview on housing: Map of misery. There is a good discussion on the differences between the OFHEO index (used by Fed Chairman Bernanke) and the Case-Shiller Home Price indices. The story also discusses the huge overhang of inventory (see story for discussion).

At the bottom of the story (hat tip Eyal) is this graph of rents as % of house prices:

[This] chart shows ... the relationship between house prices and rents. This is a sort of price/earnings ratio for the housing market ...Note that the shaded area is the forecast. I think it will take longer for prices to return to the normal ratio.

A recent analysis by Morris Davis of the University of Wisconsin-Madison, and Andreas Lehnert and Robert Martin of the Fed, shows that the rent/price yield in America ranged between 5% and 5.5% from 1960 to 1995, but fell rapidly thereafter to reach a historic low of 3.5% at the height of the boom. Given the typical pace of rental growth, Mr Feroli reckons house prices (as measured by the Case-Shiller index) need to fall by 10-15% over the next year and a half for the rent/price yield to return to its historical average.

Note: I covered this paper in January with some graphs. Here is the paper from Morris A. Davis (Department of Real Estate and Urban Land Economics, University of Wisconsin-Madison), Andreas Lehnert, and Robert F. Martin (both Federal Reserve Board of Governors economists): The Rent-Price Ratio for the Aggregate Stock of Owner-Occupied Housing

March Trade Deficit

by Calculated Risk on 5/09/2008 11:30:00 AM

The Census Bureau reported a goods and services deficit of $58.2 billion for March 2008. Exports, in March, decreased $2.6 billion to $148.5 billion, but are up almost 16% year-over-year. Imports decreased by over $6 billion to $206.7 billion, and excluding petroleum, are up only 4% year-over-year.

So ignoring monthly fluctuations, the story remains the same: exports are surging and imports (ex-petroleum) have slowed. A few years ago the story was how the ports could increase import capacity. Now the problem is finding enough containers for exports - see from the WSJ: Container Shortage Frustrates U.S. Exporters Click on graph for larger image.

Click on graph for larger image.

The red line is the trade deficit excluding petroleum products. (Blue is the total deficit, and black is the petroleum deficit). The current probable recession is marked on the graph.

Unfortunately the dollar amount of petroleum imports is surging, and this increase in petroleum imports (because of price, not quantity) is mostly offsetting the improvement in the non-petroleum trade deficit.

And the petroleum deficit will worsen in April and May. The second graph compares petroleum import prices with the EIA World Spot Price. This shows that import prices in April and May will be significantly higher than for March. Note that the May prices are for last week - and oil prices are setting new records again

The second graph compares petroleum import prices with the EIA World Spot Price. This shows that import prices in April and May will be significantly higher than for March. Note that the May prices are for last week - and oil prices are setting new records again every day every hour!

Fremont General may file BK

by Calculated Risk on 5/09/2008 09:37:00 AM

From Reuters: Fremont General says may file for bankruptcy

Fremont General ... on Friday said it may file for bankruptcy protection.Fremont was the recipient of an ugly Cease and Desist Order issued by the FDIC last year:

The company ... said that absent another "viable transaction" for remaining assets, it expects to file for Chapter 11 protection from creditors.

In taking this action, the FDIC found that the bank was operating without effective risk management policies and procedures in place in relation to its subprime mortgage and commercial real estate lending operations. The FDIC determined, among other things, that the bank had been operating without adequate subprime mortgage loan underwriting criteria, and that it was marketing and extending subprime mortgage loans in a way that substantially increased the likelihood of borrower default or other loss to the bank.So much for Fremont. I'd expect some more bank failures soon.

Sauce For The Goose

by Anonymous on 5/09/2008 07:38:00 AM

Exhibit 1, Floyd Norris, NYT:

Now the mortgage company is warning that it may not be able to pay its bills, and has set out to force those who lent money to it to agree to accept only a fraction of what they are owed. It appears that its lenders have little real choice. If they insist on being paid all that they are owed, they will go to the back of the payment line, with the risk they will get nothing.Exhibit 2, Ruth Simon, Wall Street Journal:

The mortgage industry has bitterly opposed legislative proposals that bankrupt homeowners be able to ask judges to reduce the amount they owe. But that is what this company hopes to accomplish through the threat of a bankruptcy filing. The lender in trouble is known as ResCap, short for Residential Capital. It is a subsidiary of GMAC, which was formerly owned by G.M. . . .

Owners of some notes issued by ResCap are being asked to trade them in for new bonds with face values of as little as 80 cents on the dollar. Other holders are being offered the chance to sell back bonds to the company, for as little as 65 cents on the dollar. GMAC has bought back some ResCap bonds in the public market, paying around 50 cents on the dollar. . . .

As part of the package, GMAC would put another $3.5 billion into ResCap. The company says that any current bondholders who reject the exchange offer would have their debt subordinated to the new loan from the GMAC parent, as well as to the new bonds being issued.

A major provision of the housing-market legislation passed by the House Thursday is getting a lukewarm reception from the mortgage industry. . . .

[T]rade groups that represent mortgage companies and investors say the provision might not help as many borrowers as some expect. They view the write-down provision as one of several options they might use to assist troubled homeowners. "I don't believe this would be a tool that would be used significantly," said Tom Deutsch, deputy executive director of the American Securitization Forum . . .

David Kittle, chairman-elect of the Mortgage Bankers Association, said at a conference earlier this week that he sees no rush by mortgage bankers to write down loans.

Mortgage companies that choose to participate in the proposed plan would be required to write down the value of a delinquent loan by 15% from the home's current appraised value. Borrowers would have to be at least 60 days late on their mortgage payments to qualify for the program. The bill excludes investors and those who lied about their income on their loan applications.

Mr. Deutsch says that in most cases, investors who hold mortgage-backed securities would be better off with other alternatives, such as temporarily reducing the borrower's interest rate or extending the term of the loan, in part because those leave open the chance that investors will get a larger return if the borrower gets back on track and home prices rebound. Mortgage companies are more likely to participate in the write-down program if they expect home prices to continue to decline steeply, he notes, increasing the chances of larger losses.

Thanks for the tip, NYT Junkie!