RSS Feed

RSS Feed by Calculated Risk on 9/29/2005 02:55:00 PM

Thursday, September 29, 2005

CNN Poll on Gas Prices

CNN had an online poll today on the cause of rising gas prices. Without getting into the flaws of online polls (a self selecting sample), this poll shows several other problems. First the results:

Q: What do you think is the main cause of rising gas prices?

| Cause | percent | votes |

| Hurricanes | 4% | 6738 votes |

| Lack of refining capacity | 21% | 33619 votes |

| Price gouging | 65% | 104096 votes |

| Other market forces | 10% | 16527 votes |

However gas prices have been rising for some time. This wasn't due to hurricanes or the lack of refining capacity. Instead this was due primarily to market forces.

Regardless of the time frame used, "price gouging" (the most popular answer) is incorrect.

The 'R' Word

by Calculated Risk on 9/29/2005 01:17:00 PM

Knight Ridder reports: Economists mention the ‘R’ word

Economic forecasters and Wall Street analysts are quietly hedging their bets after months of rosy reports about a vibrant U.S. economic outlook. They’re now mentioning the growing possibility of recession.The article quotes Ed Yardeni of Oak Associates:

Why? Soaring gas prices, nightmarish home-heating costs this winter, plunging consumer confidence, rising interest rates and falling new-home sales.

"The U.S. economy has been remarkably resilient in recent years, but consumers may start to postpone discretionary spending to build some cushion to pay their higher heating bills on top of paying more to fill up their gasoline tanks," he wrote to investors. "In other words, I am not sure that the economy is resilient enough to withstand the one-two punches from the Katrina-Rita tag team."Also the Conference Board reported that the help wanted market weakened in August, BEFORE the storms hit: U.S. Help-Wanted Advertising Index Declines Four Points

Yardeni said it was "increasingly likely" the U.S. economy soon could face a six-month bout of stagflation — in which prices rise but wages and hiring stagnate — the economic curse of the 1970s.

The Conference Board Help-Wanted Advertising Index - a key measure of job offerings in major newspapers across America - declined four points in August. The Index now stands at 35, down from 39 in July. It was 37 one year ago.However, online help wanted "ad volume continued to edge higher".

In the last three months, help-wanted advertising declined in seven of the nine U.S. regions. Steepest declines occurred in the West South Central (-19.4%) and West North Central (-10.8%) regions.

Says Ken Goldstein, Labor Economist at The Conference Board: "Key market indicators gave ground just before the storms and flooding. While print want-ad volume rose a bit in June and July, it sagged to May levels in August. Consumers' concerns about finding a new job were also essentially the same in August as in May, but declined noticeably in September, after the hurricanes and flooding. Latest readings show that job growth has been downsized significantly. Before the storms, there was a chance for 150,000 to 175,000 jobs per month over the near term. However, prospects may now be reduced by as much as half of that."

It appears the economy was starting to weaken prior to the devastation of Hurricanes Katrina and Rita. But one thing is certain, all problems will be blamed on the hurricanes.

Wednesday, September 28, 2005

FED: Household Debt Service Sets Record

by Calculated Risk on 9/28/2005 05:22:00 PM

The Federal Reserve released the "Household Debt Service and Financial Obligations Ratios" for Q2 2005 today.

DEFINITIONS: The household debt service ratio (DSR) is an estimate of the ratio of debt payments to disposable personal income. Debt payments consist of the estimated required payments on outstanding mortgage and consumer debt.The household DSR (Debt Service ratio) set another record at 13.55%, up from 13.46% in Q1 '05.

The financial obligations ratio (FOR) adds automobile lease payments, rental payments on tenant-occupied property, homeowners' insurance, and property tax payments to the debt service ratio.

The owner FOR (Financial Obligation Ratio) set a new record of 16.37%, up from 16.25% in Q1 '05.

The mortgage portion of the FOR set a new record at 10.55%, up from 10.41% in Q1 2005.

With low interest rates, one would expect the mortgage portion of the FOR to be lower - not higher! The third quarter will be even higher, and the increase in the minimum credit card payments will impact the 4th quarter DSR.

Mortgage Applications Down, Credit Card Late Payments Up

by Calculated Risk on 9/28/2005 11:28:00 AM

UPDATE: on credit cards, the Post has an explanation of how payments will increase (its not a hard and fast rule): We'll Have to Pay More. Good! (Thanks to Shawn for link)

The Mortgage Bankers Association reports:

The Market Composite Index — a measure of mortgage loan application volume – was 721.2, a decrease of 6.6 percent on a seasonally adjusted basis from 772.2 one week earlier. On an unadjusted basis, the Index decreased 7.1 percent compared with the previous week and was down 0.5 percent compared with the same week one year earlier.And the American Bankers Association reported:

The seasonally-adjusted Purchase Index decreased by 3.4 percent to 483.1 from 500.3 the previous week whereas the Refinance Index decreased by 10.5 percent to 2106.6 from 2353.7 one week earlier.

... the seasonally adjusted percentage of credit card accounts 30 or more days past due rose in the April-to-June quarter to 4.81 percent. That followed a delinquency rate of 4.76 percent in the first quarter and was the highest since the association began collecting this information in 1973.The rise in late payments was blamed on the increase in gas prices:

The rise in gas prices is really stretching budgets to the breaking point for some people," the association's chief economist, Jim Chessen, said in an interview. "Gas prices are taking huge chunks out of wallets, leaving some individuals with little left to meet their financial obligations."And the situation will probably get worse since the minimum credit card payment is set to rise on Oct 1st (hat tip to Paul Williamson at Property Economics):

Next month, people who have held a credit card for some time should get a surprise: each month, they will have to pay 4 percent of the outstanding balance on the card, not 2 percent. This move was dictated by the federal government's comptroller of the currency in 2003. The phase-in for new customers began in the summer, and October is the big month for existing customers. It's not small change. Almost 40 percent of credit-card holders pay only the minimum balance, according to Cardweb.com.A housing slowdown, less equity extraction, rising gasoline bills, rising late payments ... not a good combination.

The average household credit-card balance is around $9000, according to Boston's Babson Capital. Previously, families paid a minimum of $180 a month. Now, they will have to pay $360 each month.

UCLA Forecast: Peak for Housing Said to Be Near

by Calculated Risk on 9/28/2005 02:45:00 AM

Economists at the UCLA Anderson Forecast will present their quarterly outlook today in Los Angeles. The LA Times previews the report: "Peak for Housing Said to Be Near"

California's housing boom appears to be peaking, and the resultant slowdown is expected to produce "weak growth" in the state's economy during the next two years and a possible recession by the end of 2007.UCLA forecasts that prices may just stablize, not fall:

That's the view of economists at the UCLA Anderson Forecast... "There are some signs that the housing party is ending," said Christopher Thornberg, senior economist at the UCLA group and author of its California forecast.

Thornberg said that a peaking housing market doesn't necessarily mean prices will plunge. Prices could continue to rise, but at a much slower rate. That's already started to happen in previously hot markets such as San Diego and the Bay Area, he said.And UCLA projects that the slowing housing market will impact consumer spending, especially in California:

The latest UCLA outlook is slightly more downbeat than its previous report in June "because I think we're at the peak" of housing, Thornberg said. UCLA economists have long warned that a decline was coming and could end badly, but this is their strongest suggestion yet that the top may finally be at hand.

Because the state's job growth and consumer spending have been supported by rising home prices, any flattening of real estate values would cut into overall hiring and prompt consumers to rein in their pocketbooks, the UCLA forecast said. Job creation in other sectors is not strong enough to fully offset declines in housing-related fields such as construction, the state's fastest-growing job sector, the report said.How soon?

"When consumers realize they can no longer expect that appreciation bonus to subsidize their consumption habits, they will very likely pull back on spending," Thornberg said.

Typically, it takes 12 to 18 months before a slowdown in housing dampens the overall economy, UCLA's Thornberg said. The UCLA forecast calls for the state's job growth — the best indicator of expansion — to slow from 1.6% this year to 1.2% in 2006 and 0.8% in 2007.I think the economy will slow significantly about 8 to 10 months after the housing peak - sooner than Dr. Thornberg is projecting. I base this prediction on previous housing slow downs. If New Home Sales peaked in July, then I would expect the economy to slow in early '06. However one month does not make a trend, and it is possible but unlikely that housing will rebound.

Tuesday, September 27, 2005

Jobs: Georgia On My Mind

by Calculated Risk on 9/27/2005 11:08:00 PM

Georgia has an unemployment problem. The Atlantic Journal Constitution reported on a job fair today:

By noon Tuesday, signs of a troubled Georgia job market swollen with storm evacuees were unmistakable inside the massive Georgia World Congress Center.

At a job fair designed to help victims of Hurricane Katrina, organizers had to block the doors to newcomers after the event reached its limit of 15,000 job-seekers. It was still three hours before registration was expected to end.

The crowd was so big at the United Way Job Fair Tuesday that the 180,000 square feet at the Georgia World Congress Center couldn't hold everyone, so some job seekers were turned away. The limit was 15,000, and most of those, say employers and job seekers, were from Georgia.

Yet the majority of those who made it inside the center, and those who were stuck outside, were not storm evacuees. They were Georgia's jobless — a telling indicator of the state's serious problem with unemployment.

"A Category 5 economic storm is brewing in Georgia, and that's not hyperbole," said Michael Thurmond, commissioner of the Georgia Department of Labor. "The job fair today presents additional evidence as to how difficult the job market is in this state."

Click on graph for larger image.

The job picture is concerning in Georgia. The unemployment rate is rising and has reached the highest level since the recession of the early '90s.

Part of the problem is that Georgia's housing market has underperformed during the housing boom. According to the OFHEO House Price Index, Georgia's housing has only appreciated 12.4% since the end of 2002. This compares to the national average of 26.1%.

So Georgia probably hasn't seen the same housing related employment boom as much of the nation. This is a chicken and the egg problem. Housing might be weak because of relatively weak employment; employment might be weak because of relatively weak housing.

Perhaps partly because of the weak labor market, and as buyers stretch to afford a home, Georgia leads the nation in IO mortgages:

Georgia has become the national leader in an increasingly popular but controversial type of mortgage that lets borrowers postpone payments on the loan principal for years.So it isn't surprising that with a relatively weak labor market, a high concentration of creative loans and minimal house price appreciation:

More than half of mortgages last year in Georgia were interest-only, compared with fewer than one-third nationwide ...

"Georgia ranked fourth in the nation in the number of properties in foreclosure".But what comes first? Weak employment or weak housing? And as the housing market slows, will Georgia's problem become a national problem?

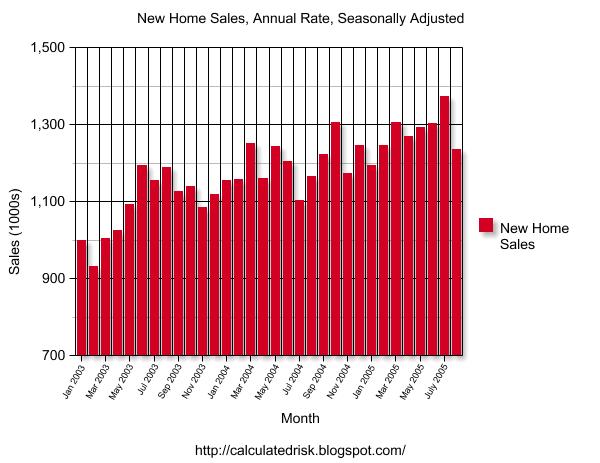

August New Home Sales: 1.237 Million

by Calculated Risk on 9/27/2005 01:49:00 AM

According to a Census Bureau report, New Home Sales in August were at a seasonally adjusted annual rate of 1.237 million vs. market expectations of 1.345 million. July sales were revised down to 1.373 million from 1.41 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in August 2005 were at a seasonally adjusted annual rate of 1,237,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

The Not Seasonally Adjusted monthly rate was 106,000 New Homes sold, down from a revised 118,000 in July.

The median sales price of new houses sold in August 2005 was $220,300; the average sales price was $283,400.

Both the average and median sales price rebounded.

The seasonally adjusted estimate of new houses for sale at the end of August was 479,000. This represents a supply of 4.7 months at the current sales rate.

The seasonally adjusted supply of New Homes was 4.7 months, a significant increase from recent months.

With the usually caveat that one month does not make a trend, this report shows a significant downturn in the New Home Sales market. Sales were off. Inventories were up. Revisions were negative.

This may be the beginning of the end for this housing cycle.

Monday, September 26, 2005

WSJ: Greenspan Warns of Reliance on Housing Loans

by Calculated Risk on 9/26/2005 09:51:00 PM

Greg Ip writes at the WSJ:

]"Federal Reserve Chairman Alan Greenspan, drawing on new research he has personally supervised, said American consumers have become enormously dependent on borrowing against their homes to fuel their spending, and that a rise in mortgage rates could trigger a spending pullback.

Mr. Greenspan's new data show that borrowing against home values added a stunning $600 billion to consumers' spending power last year, equivalent to 7% of personal disposable income -- compared with 3% in 2000 and 1% in 1994.

...

That reversal need not be "disruptive," Mr. Greenspan said. Indeed, he suggested that such a reversal would bring about a needed rise in U.S. saving and a narrower trade deficit. But he also sounded new warnings about speculation in the housing market, focusing on rising sales of second homes, though also playing down the threat of overleveraged homebuyers.

Mr. Greenspan's remarks were among his most extensive to date on the scope and risks of the rise in housing prices and mortgage debt in the past decade, developments to which his own policies have contributed. The remarks suggest that while in the near term higher energy prices may be the greatest threat to consumers, in the longer term Mr. Greenspan sees a cooling housing market as potentially more significant.

Last year's estimate of the value of "home equity extraction," as Mr. Greenspan calls it, was double the value of President Bush's tax cuts, as estimated by Brookings Institution scholar Peter Orszag. It's unclear how much of that home-financed borrowing was spent on goods and services, but Mr. Greenspan suggested it was about half.

...

Mr. Greenspan also repeated his warnings on the increased popularity of some exotic mortgages, which expose the borrower to a greater risk of rising rates or declining home prices.

...

Mr. Greenspan believes this home-equity extraction has been a powerful channel of support to the economy in recent years. Indeed, he believes it's how the Fed's low interest rates propped up the economy after the stock bubble burst in 2001. While the Fed has raised short-term interest rates since last summer, long-term mortgage rates, which are set by bond investors, have stayed surprisingly low. Thus, home-equity extraction has fueled consumer spending longer than Mr. Greenspan thought likely ...

Greenspan on Housing

by Calculated Risk on 9/26/2005 04:26:00 PM

Bloomberg reports: Greenspan Says Speculation Having 'Greater Role' in Home Prices

Sales of vacation houses, or homes that aren't always occupied by owners, are "arguably at historically unprecedented levels," Greenspan said in the text of his remarks to the American Bankers Association annual convention in Palm Desert, California. "This suggests that speculative activity may have had a greater role in generating the recent price increases than it customarily has had in the past."MarketWatch adds: Greenspan weighs in on home prices, Drops may not be fatal, even as housing fuels spending

A new study, co-authored by Greenspan, has found that about four-fifths of the rise in home-mortgage debt has been due to homeowners taking some cash out of the rise in their property's value.Here is the Greenspan study (PDF): Estimates of Home Mortgage Originations, Repayments, and Debt on One-to-Four-Family Residences

"It is difficult to dismiss the conclusion that a significant amount of consumption is driven by capital gains on some combination of both stocks and residences," Greenspan said.

As a result, consumer spending would decline if mortgage rates rise and home turnover and opportunities for mortgage refinancing cash-outs decline, he added.

There also would be some positive developments, as the personal savings rate would likely rise, and the trade deficit would narrow given the likely drop in imports of consumer goods.

"How significant and disruptive such adjustments turn out to be is an open question," Greenspan said.

A few comments: 80% of the increase in mortgage debt "has been due to homeowners taking some cash out". That is a huge amount. If cash refis were cut in half for the last year, GDP would have been flat and if there were no cash out refis, GDP would have declined 3.1%. (Update: assuming cash out goes to consumption) And that is just the direct impact and does not include any secondary effects of layoffs in the housing and retail industries.

I do agree with Greenspan's comment: it is difficult to predict how disruptive the coming adjustment will be, but a recession is likely.

Existing Homes: Sales Strong, Inventories Rise

by Calculated Risk on 9/26/2005 10:44:00 AM

CBS reports: Existing Home Sales Hit 2nd Highest Level

The National Association of Realtors reported Monday that sales of existing homes rose 2 percent in August to a seasonally adjusted annual rate of 7.29 million units, a sales pace that was exceeded only by an all-time high of 7.35 million units in June.Inventories increased from 2,759,000 in July to 2,856,000 in August. This is about what I expected. Existing Home Sales are a trailing indicator and are mostly sales in June and July. Tomorrow's New Home Sales is more interesting and might show the first signs of a slowing housing market.

...

The strong demand pushed prices up to a record level of $220,000 last month, a gain of 15.8 percent from August 2004. That was the biggest 12-month increase since a 17.2 percent increase in July 1979.

...

While the Realtors predicted that Hurricane Katrina, which came ashore in New Orleans in late August, would impact sales in September, they said the impact in August appeared to be minimal.