RSS Feed

RSS Feed by Calculated Risk on 8/15/2005 04:28:00 PM

Monday, August 15, 2005

No more Free Money? OC Home Prices Dip

Back in March I wrote (in jest) that they were giving away free money in The OC (Orange County, CA). At that time the median home price in OC was $555,000.

Over the next few months median home prices rose to $603K. That was a total of $48K in FREE MONEY (not really free of course) since local RE Broker Gary Watts' prediction of $70,000 in gains this year for the median home.

Now the OC Register is reporting a slight dip in home prices to $601,000 for July. Still $46K in 6 months is well on its way to Mr. Watts' $70K annual appreciation prediction.

Fleckenstein: Top in Place for Housing Market

by Calculated Risk on 8/15/2005 12:42:00 PM

Bill Fleckenstein writes the Contrarian Chronicles for MSN Money. This week he touches on housing:

'To get a feeling for the budding inventory problem in many previously hot markets, let's look at a less-hot market (via the following vignette from a reader of this column): A publicly held home-building company (which shall remain nameless) in Columbus, Ohio, has been buying back homes from financially distressed owners and reselling them, at reduced prices, only to folks who are approved for conventional mortgages. As the reader says: "The inventory of homes is growing -- including one cul-de-sac where a staggering 13 of 20 homes, all less than three years old, are already up for sale."'And on subprime mortgages:

'... a contact in the subprime-lending arena (lenders who specialize in making loans to borrowers with less-than-stellar credit records) suggests to me that it's becoming increasingly difficult for originators of subprime mortgages to sell them at a profit. Unless all of these are booked on the originator's own balance sheet, we'll start to see credit being cut off to the more marginal real-estate speculators -- the driving force, at the margin, behind the real-estate market.'Fleck concludes:

'...the macro winds have shifted, I believe, and none of those shifts has occurred in a way that is bullish for U.S. assets. Bottom line: It's my opinion that a top is being formed (or is already in place), both in the housing market and the stock market. That spells trouble for an economy built on the unsustainable strategy of trying to speculate our way to prosperity.'Fleck has been very bearish for a number of years. He was early (but correct) on the NASDAQ. And he has also been early on housing.

The housing market was very strong in the 2nd quarter. However it does appear that inventories are building and, as Fleck suggests, a top may be close.

CNN: Home prices post record gains

by Calculated Risk on 8/15/2005 12:38:00 PM

CNN reports:

Single-home price growth over the 12 months ending June 30 was the strongest in history, according to the National Association of Realtors.See the article for a list of the top 10 markets. Durham, North Carolina is #9?

In its quarterly survey, NAR found that U.S. home prices rose at an annual rate of 13.6 percent, to a median price of $208,300.

Of the 149 metro areas surveyed, 67 showed gains of more than 10 percent.

David Lereah, NAR's chief economist, called the increases unprecedented. "When you look at appreciation of home prices relative to the overall rate of inflation, these are the strongest increases on record," he said.

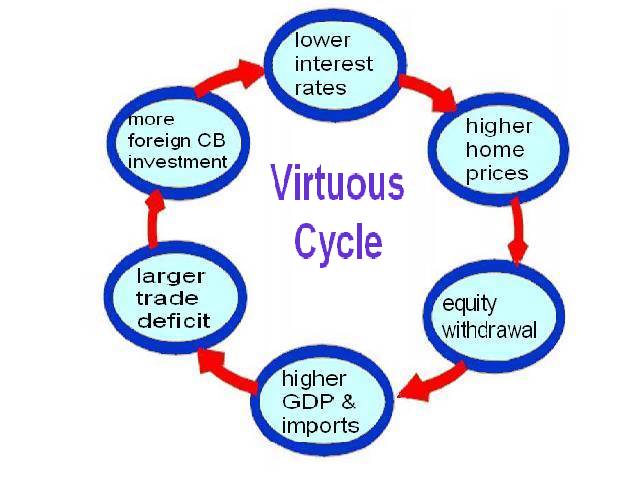

Oil, Trade and Housing

by Calculated Risk on 8/15/2005 12:49:00 AM

My most recent post is up on Angry Bear: Oil Prices Revisited.

It looks like oil imports will add about $1.2 Billion to the July trade deficit.

It is possible that higher oil prices are leading to lower interest rates! As Dr. Setser noted:

"High oil prices = oil windfall = global savings glut = low long-term rates ... and the low-long term rates help even as high oil prices hurt."And finally, back in March, I speculated that there was a relationship between housing and the trade deficit. In fact, it was possible that a virtuous cycle had developed that might become vicious when housing slows down.

UPDATE: Here are the graphics from the Virtuous-Vicious post.

Click on diagram for larger image.

The following diagram depicts the possible unwinding of the current cycle.

Check out the post for a discussion of how this could work (and some numbers).

It all ties together (hopefully). I'm focused mostly on housing because I think housing is the linchpin for the US economy.

Best to all.

Sunday, August 14, 2005

The "Rising tide of abandoned residential properties"

by Calculated Risk on 8/14/2005 12:17:00 AM

Real estate investors are just walking away from residential property and lenders are getting stuck. Some lenders do not want to take title to the worthless property and the city has started a campaign called the "shaming sign" - placing signs on abandoned property with the names of the lenders' executives. This has induced some lenders to take title and either fix up or demolish the abandoned homes.

This is a story from the Great Depression ... except it is happening right now in Dayton, Ohio.

... others have fallen victim to a conspiracy of carelessness and greed by lenders and their clients, many of them investors. When loans go bad, both duck for cover, their abandoned properties becoming a cancer on neighborhoods.With lax lending restrictions it is no surprise that areas with little or no appreciation are seeing rising foreclosures. I wonder if the "investors" were able to borrow against the home before just walking away from the loan.

This reality has led to a new strategy — the "shaming sign." Those who cut out on neighborhoods are held up to richly deserved embarrassment.

A major bank recently took charge of one of its neglected foreclosure properties; a bank official didn't like seeing his name on a sign.

Another big bank has been bobbing and weaving to avoid responsibility. Unable to sell a foreclosed property, it won't take title itself. Instead, it filed suit against its customer, leaving the property to languish and the city holding the bag.

Another property, though, on Helena Street could have a happy ending. A representative for the owner says the owner will tear the building down and deed the property to an adjacent community garden.

That action hasn't happened yet, but should it comes to pass, it will demonstrate the power and potential of the city's attack on abandoned properties.

Saturday, August 13, 2005

Trade Deficit Projection: June Review

by Calculated Risk on 8/13/2005 10:11:00 PM

Three months ago I started to build a simple model to project the trade deficit. I didn't make as much progress as I had hoped, but the first two components (oil and China) performed reasonably well for two months... but I underestimated China for June.

Here are my projections for June. My model projected a deficit of $17.0 Billion Seasonally Adjusted in energy related petroleum product imports. The actual number was $17.77 Billion (see Exhibit 9). This is an error of 4.3%.

For the trade balance with China, my model projected a deficit of $16.3B NSA (SA is not available). The actual number (see Exhibit 14) was $17.6B or an error of 7.3%.

Here are each of the components and how the model performed:

| ITEM | Projection | Actual | Error |

| US Exports to China (NSA) | $3.2B | $3.4 | 6% |

| US Imports from China (NSA) | $19.5B | $20.99B | 7% |

| US Trade Deficit: China (NSA) | $16.3B | $17.6B | 7% |

| Oil: Imports SA | $19.3B | $19.9B | 3% |

| Oil: Exports SA | $2.3B | $2.14B | 7% |

| OIL Balance SA | $17.0B | $17.77B | 4% |

Some internal data:

| ITEM | Projection | Actual | Error |

| Oil: Contract Price BBL | $45.11 | $44.40 | 1.6% |

| Oil: BBLs Crude | 328.0 | 328.3M | 0% |

| Oil: Price Other BBL | $51.88 | $51.58 | <1% |

| Oil: BBLs Other | 90M | 103.7M | 13% |

| Oil: Oil Imports NSA | $19.5B | $19.9B | 2% |

I really missed on China. I wondered about the surge in imports at LA and attributed them to Japan (imports in Japan were up $1.26B). Overall, my guess of $57.7B was on the high end of estimates, and I still underestimated the deficit for June!

Prediction July Trade Deficit: Oil

by Calculated Risk on 8/13/2005 06:32:00 PM

Gen'l Glut pointed out last month that another jump in oil imports would come in July. It looks like he is correct. Here are the forecasted July oil numbers using the same model (described here). The ERPP (Energy Related Petroleum Products) trade numbers for July are forecast to be:

Forecast: Total NSA ERRP Imports: $21.8 Billion

Total SA ERPP FORECAST:

Imports SA: $21.1 Billion (seasonal factor estimated at 0.965 for July)

Exports SA: $2.2 Billion

Balance ERPP: $18.9 Billion

I am forecasting a record average price per barrel of $49.71 compared to June's $44.40 and the previous record of $44.76 in April.

Imports SA and NSA will set records in July. And the projected SA deficit of $18.9 Billion will shatter the previous seasonally adjusted record oil deficit of $17.9 Billion set last November.

This compares to the SA June deficit of $17.76 Billion. It appears oil imports will add approximately $1.2 Billion to the July trade deficit.

Inside Report: Greenspan's Concerns

by Calculated Risk on 8/13/2005 03:08:00 PM

Novak reports (I know, I know - I'm quoting Robert Novak):

WASHINGTON -- Federal Reserve Chairman Alan Greenspan, worried about excesses in real estate investment, has privately called on other federal regulators to take a closer look at imprudent speculation.Thanks to Dr. Thoma.

According to Fed sources, Greenspan has told the regulators that there is a limit to what the central bank's monetary policy can do in tamping down inflationary pressures. He has been in contact with the Comptroller of the Currency and the Office of Thrift Supervision, among other agencies.

A footnote: High officials in the Japanese Ministry of Finance recently commented privately that the vibrant U.S. home mortgage market is supporting an otherwise shaky global economy.

Friday, August 12, 2005

NYTimes: Assess Your Area's Real Estate Bubble

by Calculated Risk on 8/12/2005 10:24:00 PM

The NYTimes suggests waiting for the experts to declare the bubble over in your area might be too late. Do Try This at Home: Assess Your Area's Real Estate Bubble

... the main driver of today's market is consumer psychology. Home prices go up as long as people expect them to go up.The article gives some examples of slowing markets:

When they stop believing, prices fall - and no economist in Washington can get wind of that faster than someone chatting over knockwurst at a neighborhood block party. "Economists looking at the macrodata will be the last to know," said Richard A. Brown, chief economist at the Federal Deposit Insurance Corporation.

"It's taking a lot longer to sell a home," says Karl A. Martone, a Re/Max Properties agent in Providence, where homes now sit on the market an average of 65 days, up from 14 days a year ago. The region has almost six months of inventory, which is up 35 percent from a year ago.And an example of prices disconnected from fundamentals:

Vicki Doran, a real estate agent with Coldwell Banker in Providence, says: "It's switching to a buyer's market. Last year buyers had to snap things up. Now they can shop around."

Take a look at the hot San Diego condo market. In Park Place, one of the many sleek towers of condominiums recently slung up around Petco Park, a one-bedroom condo is offered for $719,000. Someone buying it would expect to make mortgage payments of about $3,775 a month, plus monthly maintenance fees.The article goes on to give several indicators of when a market has topped. Rising inventories is at the top of my list right now. And on loan quality:

But someone really wanting to live in the high-rise, with hardwood floors, granite countertops and city views for a lot less, could rent a nearly identical unit in the same building for $2,400 a month. That is clear evidence prices have to move down.

The popularity of interest-only mortgages could become one of the best indicators of a fragile market, several economists say. Mr. Thornberg of UCLA Anderson says it's a sign that lenders are scraping the bottom of the barrel. "We are close to running out of shills," he says.But in the end it all comes down to sentiment. The entire article is worth reading.

Dr. Leamer: Housing a "fragile and dangerous situation"

by Calculated Risk on 8/12/2005 08:03:00 PM

AP reporter Michael Liedtke writes on housing: Real estate strong despite higher interest. Of course I'm drawn to this quote from Dr. Leamer, UCLA Anderson Forecast Director:

"It's very hard to understand the psychology of any market," said UCLA economics professor Edward Leamer. "But it's fundamentally clear that the housing market is in a fragile and dangerous situation."The article is balanced and touches on the San Diego and Boston housing markets. It concludes:

It's difficult to predict how high mortgage rates will have to rise before home prices are hurt, but industry observers like Karevoll believe the tipping point is somewhere between 7 and 8 percent.How it gets better is prices more aligned with incomes. Also, based on New Home Sales, I believe the "tipping point" is far lower than 7 or 8%.

Meanwhile, current mortgage rates remain enticing, especially to buyers who remember when rates were still above 10 percent in the 1990s, said Denver-area real estate agent Bill Kosena.

"Interest rates are extremely low," he said. "I don't know how it gets any better than it is."