RSS Feed

RSS Feed by Calculated Risk on 8/13/2005 06:32:00 PM

Saturday, August 13, 2005

Prediction July Trade Deficit: Oil

Gen'l Glut pointed out last month that another jump in oil imports would come in July. It looks like he is correct. Here are the forecasted July oil numbers using the same model (described here). The ERPP (Energy Related Petroleum Products) trade numbers for July are forecast to be:

Forecast: Total NSA ERRP Imports: $21.8 Billion

Total SA ERPP FORECAST:

Imports SA: $21.1 Billion (seasonal factor estimated at 0.965 for July)

Exports SA: $2.2 Billion

Balance ERPP: $18.9 Billion

I am forecasting a record average price per barrel of $49.71 compared to June's $44.40 and the previous record of $44.76 in April.

Imports SA and NSA will set records in July. And the projected SA deficit of $18.9 Billion will shatter the previous seasonally adjusted record oil deficit of $17.9 Billion set last November.

This compares to the SA June deficit of $17.76 Billion. It appears oil imports will add approximately $1.2 Billion to the July trade deficit.

Inside Report: Greenspan's Concerns

by Calculated Risk on 8/13/2005 03:08:00 PM

Novak reports (I know, I know - I'm quoting Robert Novak):

WASHINGTON -- Federal Reserve Chairman Alan Greenspan, worried about excesses in real estate investment, has privately called on other federal regulators to take a closer look at imprudent speculation.Thanks to Dr. Thoma.

According to Fed sources, Greenspan has told the regulators that there is a limit to what the central bank's monetary policy can do in tamping down inflationary pressures. He has been in contact with the Comptroller of the Currency and the Office of Thrift Supervision, among other agencies.

A footnote: High officials in the Japanese Ministry of Finance recently commented privately that the vibrant U.S. home mortgage market is supporting an otherwise shaky global economy.

Friday, August 12, 2005

NYTimes: Assess Your Area's Real Estate Bubble

by Calculated Risk on 8/12/2005 10:24:00 PM

The NYTimes suggests waiting for the experts to declare the bubble over in your area might be too late. Do Try This at Home: Assess Your Area's Real Estate Bubble

... the main driver of today's market is consumer psychology. Home prices go up as long as people expect them to go up.The article gives some examples of slowing markets:

When they stop believing, prices fall - and no economist in Washington can get wind of that faster than someone chatting over knockwurst at a neighborhood block party. "Economists looking at the macrodata will be the last to know," said Richard A. Brown, chief economist at the Federal Deposit Insurance Corporation.

"It's taking a lot longer to sell a home," says Karl A. Martone, a Re/Max Properties agent in Providence, where homes now sit on the market an average of 65 days, up from 14 days a year ago. The region has almost six months of inventory, which is up 35 percent from a year ago.And an example of prices disconnected from fundamentals:

Vicki Doran, a real estate agent with Coldwell Banker in Providence, says: "It's switching to a buyer's market. Last year buyers had to snap things up. Now they can shop around."

Take a look at the hot San Diego condo market. In Park Place, one of the many sleek towers of condominiums recently slung up around Petco Park, a one-bedroom condo is offered for $719,000. Someone buying it would expect to make mortgage payments of about $3,775 a month, plus monthly maintenance fees.The article goes on to give several indicators of when a market has topped. Rising inventories is at the top of my list right now. And on loan quality:

But someone really wanting to live in the high-rise, with hardwood floors, granite countertops and city views for a lot less, could rent a nearly identical unit in the same building for $2,400 a month. That is clear evidence prices have to move down.

The popularity of interest-only mortgages could become one of the best indicators of a fragile market, several economists say. Mr. Thornberg of UCLA Anderson says it's a sign that lenders are scraping the bottom of the barrel. "We are close to running out of shills," he says.But in the end it all comes down to sentiment. The entire article is worth reading.

Dr. Leamer: Housing a "fragile and dangerous situation"

by Calculated Risk on 8/12/2005 08:03:00 PM

AP reporter Michael Liedtke writes on housing: Real estate strong despite higher interest. Of course I'm drawn to this quote from Dr. Leamer, UCLA Anderson Forecast Director:

"It's very hard to understand the psychology of any market," said UCLA economics professor Edward Leamer. "But it's fundamentally clear that the housing market is in a fragile and dangerous situation."The article is balanced and touches on the San Diego and Boston housing markets. It concludes:

It's difficult to predict how high mortgage rates will have to rise before home prices are hurt, but industry observers like Karevoll believe the tipping point is somewhere between 7 and 8 percent.How it gets better is prices more aligned with incomes. Also, based on New Home Sales, I believe the "tipping point" is far lower than 7 or 8%.

Meanwhile, current mortgage rates remain enticing, especially to buyers who remember when rates were still above 10 percent in the 1990s, said Denver-area real estate agent Bill Kosena.

"Interest rates are extremely low," he said. "I don't know how it gets any better than it is."

WSJ: Rise in Supply Suggests Housing Market Cooling

by Calculated Risk on 8/12/2005 02:32:00 PM

The WSJ reports:

Rise in Supply of Homes for SaleExcerpt:

Suggests Market Could Be Cooling

By JAMES R. HAGERTY and KEMBA DUNHAM

Staff Reporters of THE WALL STREET JOURNAL

August 12, 2005; Page A1

"The number of homes available for sale has increased sharply in some of the nation's hottest real-estate markets -- one of several recent signs suggesting that air may be seeping out of the frenzied U.S. housing market.

Home prices have surged an average of about 50% in the U.S. in the last five years, largely thanks to the lowest mortgage interest rates in more than four decades and what has been a shortage of available homes in many markets. But some economists and housing-industry analysts believe supply is catching up with demand -- a trend that could cause home-price appreciation to slow down in the months ahead.

In San Diego County, for instance, where the median home price has more than doubled in the last five years, the number of homes listed for sale totaled 12,149 on July 8, more than twice the 5,995 available a year earlier, according to the San Diego Association of Realtors.

In northern Virginia, an area dominated by the fast-growing suburbs of Washington, inventories are up 26% from a year earlier. "Sales have slowed down for sure," says Tip Powers, president of Realty Direct Inc., Sterling, Va. He says home prices have flattened out and speculators are starting to shy away from the market because they no longer can count on quickly unloading properties at a profit.

A similar rise is being seen in Massachusetts, where home inventories are up 31%, according to officials of real-estate organizations there. Real-estate brokers say inventories also are up in such markets as Chicago, Las Vegas and Orlando."

.

.

.

Several factors point to a possible cooling of the market. Mortgage interest rates have been edging higher in recent weeks, raising the cost of purchasing a new home and knocking some potential buyers out of the market. The average rate for a 30-year fixed mortgage is 5.89%, said Freddie Mac, a mortgage-finance company, this week. That's up from 5.53% in late June.

In some markets, such as California and Florida, prices have surged past the ability of many people to afford a home. Additionally, banking regulators have begun to raise questions about whether mortgage lenders are being prudent enough -- which eventually could prompt some lenders to tighten credit standards.

Virginia Housing: "It’s Changing"

by Calculated Risk on 8/12/2005 11:39:00 AM

UPDATE: More inventory data - GREATER NORTHERN VIRGINIA AREA

| Active Listings | 2005 | 2004 | Pct.Chg |

| Single Family Homes | 8,800 | 6,588 | 33.6% |

| Condos & Coops | 1,544 | 1,010 | 52.9% |

| TOTAL | 10,344 | 7,598 | 36.1% |

Leesburg Today reports the Virginia housing market is "changing". The story has many positive comments, but:

... there are definite signs of a slowdown and that the market is undergoing a correction ... reported an across-the-board slowing, a build up of inventories and a shift in power from the seller-dominated market of the past few years back to the buyer.The housing market is still strong, but the story is rising inventories:

Fischer noted that inventories have quadrupled in the resale market over the past two-and-a-half months. Although that trend has not extended yet to new home sales, Fischer predicted "it’s reasonable to expect that as those inventories build, that will have an impact on the new home frenzy."

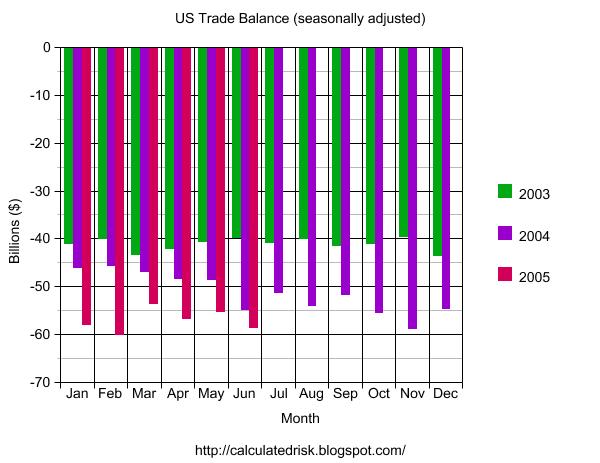

U.S. Trade Deficit: $58.8 Billion for June

by Calculated Risk on 8/12/2005 08:47:00 AM

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis released the monthly trade balance report today for June:

"... total June exports of $106.8 billion and imports of $165.6 billion resulted in a goods and services deficit of $58.8 billion, $3.4 billionNote: all numbers are seasonally adjusted.

more than the $55.4 billion in May, revised.

June exports were virtually unchanged from May, and June imports were $3.4 billion more than May imports of $162.2 billion."

Click on graph for larger image.

June 2005 was only 7% worse than June 2004. For the first six months of 2005, the trade deficits is up 18% over the same period in 2004.

Imports from China were a record $20.988 Billion. And Imports from Japan rebounded to $11.989 Billion.

The average contract price for oil of $44.40 was just below the record of $44.76 in April.

Based on initial data, the trade deficit for July will be close to the seasonally adjusted record of $60.1 Billion set in February.

Krugman: Safe as Houses

by Calculated Risk on 8/12/2005 12:59:00 AM

Dr. Krugman writes in the NYTimes: Safe as Houses about the housing centric US economy:

Since December 2000 employment in U.S. manufacturing has fallen 17 percent, but membership in the National Association of Realtors has risen 58 percent.And Krugman is concerned about the impact on the economy when housing slows:

The housing boom has created jobs in two ways. Many jobs have been created, directly and indirectly, by a surge in housing construction. And rising home values have fueled a simultaneous surge in consumer spending.

Let's start with home building. Between 1980 and 2000, which was before the housing boom, spending on the construction of new homes averaged 4.25 percent of G.D.P. In the most recent quarter, however, the figure was 5.98 percent. That difference is equivalent to about $200 billion a year in additional spending, generating roughly two million extra jobs.

... the economy is expanding. But because that expansion depends so much on real estate - without the housing boom, the economic picture would look dismal indeed - you have to wonder how much to trust it.Krugman concludes:

I've written before about the reasons to believe that current house prices in much of the country represent a bubble. When that bubble begins to deflate, so will housing-related employment.

How solid, then, is America's economic recovery? The British have a phrase that applies: "safe as houses." Our economy is as safe as houses. Unfortunately, given current prices and our dependence on foreign lenders, houses aren't safe at all.

Thursday, August 11, 2005

California's Housing Affordability Index

by Calculated Risk on 8/11/2005 08:33:00 PM

The California Association of Realtors reports: California's Housing Affordability Index fell two points to 16 percent in June

The percentage of households in California able to afford a median-priced home stood at 16 percent in June, a 2 percentage-point decrease compared with the same period a year ago when the Index was at 18 percent, according to a report released today by the California Association of REALTORS® (C.A.R.). The June Housing Affordability Index (HAI) was unchanged from May, when it also stood at 16 percent.See article for table of affordability and prices by region.

...

The minimum household income needed to purchase a median-priced home at $542,720 in California in June was $125,870, based on an average effective mortgage interest rate of 5.71 percent and assuming a 20 percent downpayment. The minimum household income needed to purchase a median-priced home was up from $111,420 in June 2004, when the median price of a home was $468,050 and the prevailing interest rate was 6.01 percent.

FED: Monetary Policy and Asset Price Bubbles

by Calculated Risk on 8/11/2005 11:14:00 AM

The Federal Reserve's Glenn D. Rudebusch, Senior Vice President and Associate Director of Research has released an economic letter: Monetary Policy and Asset Price Bubbles.

In theory at least, an asset price can be separated into a component determined by underlying economic fundamentals and a nonfundamental bubble component that may reflect price speculation or irrational investor euphoria or depression. The expansion of an asset price bubble may lead to a debilitating misallocation of economic resources, and its collapse may cause severe strains on the financial system and destabilize the economy.

Despite these potential problems, the appropriate monetary policy response to an asset price bubble remains unclear and is one of the most contentious issues currently facing central banks. Some have argued that monetary policy should be used to contain or reduce an asset price bubble in order to alleviate its adverse consequences on the economy, while others have argued that such a policy would be both impractical and unproductive given real-world uncertainties about the nature or even existence of bubbles. This Economic Letter examines how policymakers might choose between alternative courses of action when confronted with a possible asset price bubble.

Click on Chart for larger image.

A decision tree for choosing between the Standard and Bubble Policies is shown ... In brief, it poses three questions: (1) Can policymakers identify a bubble? (2) Will fallout from a bubble be significant and hard to rectify after the fact? and (3) Is monetary policy the best tool to deflate the bubble?The problem is each of these hurdles is difficult to negotiate. Rudebusch concludes:

The first hurdle—Can policymakers identify a bubble?—considers whether the particular asset price appears aligned with fundamentals. Some have argued that either bubbles don't exist because asset prices reflect the collective information and wisdom of traders in organized markets or, even if they do exist, they cannot be identified because the requisite estimates of the underlying fundamentals are so imprecise. If policymakers cannot discern a bubble, then the Standard Policy is the only feasible response.

But suppose an asset price bubble is identified. Then the second hurdle is whether bubble fluctuations have significant macroeconomic fallout that monetary policy cannot readily offset after the fact ...

...

The final hurdle before invoking a Bubble Policy involves assessing whether monetary policy is the best way to deflate the asset price bubble. Ideally, for the Bubble Policy, a moderate adjustment of interest rates could constrain the bubble and greatly reduce the risk of severe future macroeconomic dislocations. However, bubbles, even if identified, may not be influenced in a predictable fashion by monetary policy actions. Furthermore, even if changing interest rates could alter the bubble path, such a strategy may involve substantial costs, including near-term deviations from the central bank's macroeconomic goals as well as potential political and moral hazard complications. Finally, even if monetary policy can affect the bubble, alternative strategies to deflate it, such as changes in financial regulation or supervision, may be more targeted and have a lower cost.

The decision tree for choosing a Bubble Policy poses a daunting triple jump. For example, consider the run-up in the stock market in 1999 and 2000, when there was widespread suspicion that an equity price bubble existed and people worried that it could result in capital misallocation and financial instability. Still, those worries did not spur a Bubble Policy, in large part because it appeared unlikely that monetary policy could have deflated the equity price bubble without substantial costs to the economy. After the fact, of course, the macroeconomic consequences from the apparent boom and bust in equity prices arguably have been manageable.My view is regulatory substitutes are the answer, not monetary policy. For the housing bubble, more stringent lending requirements and oversight probably would have prevented much of the speculation.

However, the decision tree does not provide a blanket prohibition on bubble reduction, and as yet, there is no bottom line on the appropriate policy response to asset price bubbles. Those who oppose a Bubble Policy stress the steep informational prerequisites for success, while those who favor it note that policymakers often must act on the basis of incomplete knowledge.