RSS Feed

RSS Feed by Calculated Risk on 2/17/2021 10:04:00 AM

Wednesday, February 17, 2021

NAHB: Builder Confidence Increased to 84 in February

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 84, up from 83 in January. Any number above 50 indicates that more builders view sales conditions as good than poor.

From the NAHB: Builder Confidence: High Demand Offsets Higher Costs – For Now

Strong buyer demand helped offset supply chain challenges and a surge in lumber prices as builder confidence in the market for newly built single-family homes inched up one point to 84 in February, according to the latest NAHB/Wells Fargo Housing Market Index (HMI).

Lumber prices have been steadily rising this year and hit a record high in mid-February, adding thousands of dollars to the cost of a new home and causing some builders to abruptly halt projects at a time when inventories are already at all-time lows.

However, demand conditions remain solid due to demographics, low mortgage rates and the suburban shift to lower cost markets, but we expect to see some cooling in growth rates for residential construction in 2021 due to cost factors, supply chain issues and regulatory risks.

...

The HMI index gauging current sales conditions held steady at 90, while the component measuring sales expectations in the next six months fell three points to 80. The gauge charting traffic of prospective buyers rose four points to 72.

Looking at the three-month moving averages for regional HMI scores, the Northeast rose two points to 78, the Midwest fell one point to 81, the South dropped two points to 84 and the West posted a two-point loss to 93.

Click on graph for larger image.

Click on graph for larger image.This graph show the NAHB index since Jan 1985.

This was slightly above the consensus forecast, and a very strong reading.

Housing and homebuilding have been one of the best performing sectors during the pandemic.

Industrial Production Increased 0.9 Percent in January

by Calculated Risk on 2/17/2021 09:22:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production increased 0.9 percent in January. Manufacturing output rose 1.0 percent, about the same as its average gain over the previous five months. Mining production advanced 2.3 percent, while the output of utilities declined 1.2 percent. At 107.2 percent of its 2012 average, total industrial production in January was 1.8 percent lower than its year-earlier level. Capacity utilization for the industrial sector increased 0.7 percentage point in January to 75.6 percent, a rate that is 4.0 percent below its long-run (1972–2020) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April, but still below the level in February 2020.

Capacity utilization at 75.6% is 4.0% below the average from 1972 to 2019.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased in January to 107.2. This is 1.9% below the February 2020 level.

The change in industrial production was above consensus expectations.

Retail Sales increased 5.3% in January

by Calculated Risk on 2/17/2021 08:37:00 AM

On a monthly basis, retail sales increased 5.3 percent from December to January (seasonally adjusted), and sales were up 7.4 percent from January 2020.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for January 2021, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $568.2 billion, an increase of 5.3 percent from the previous month, and 7.4 percent above January 2020.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were up 5.4% in January.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 8.6% on a YoY basis.

Retail and Food service sales, ex-gasoline, increased by 8.6% on a YoY basis.The increase in January was well above expectations, however sales in November and December were revised down, combined.

MBA: Mortgage Applications Decrease in Latest Weekly Survey

by Calculated Risk on 2/17/2021 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 5.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 12, 2021.

... The Refinance Index decreased 5 percent from the previous week and was 51 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 15 percent higher than the same week one year ago.

“Expectations of faster economic growth and inflation continue to push Treasury yields and mortgage rates higher. Since hitting a survey low in December, the 30-year fixed rate has slowly risen, and last week climbed to its highest level since November 2020,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “The uptick in rates has slightly dampened refinance activity, with MBA’s index falling for the second week in a row, and the overall share dipping below 70 percent for the first time since last October.”

Added Kan, “The housing market in early 2021 continues to be constrained by low inventory and higher prices. Conventional and government applications to buy a home declined last week, but purchase activity overall is still strong – up 15 percent from last year. The average purchase loan size hit another survey high at $412,200, partly due to a larger drop in FHA applications, which tend to have smaller-than average loan sizes.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($548,250 or less) increased to 2.98 percent from 2.96 percent, with points increasing to 0.43 from 0.36 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

The refinance index has been volatile recently depending on rates.

With near record low rates, the index remains up significantly from last year (but will be down year-over-year in early March - since rates fell sharply at the beginning of the pandemic).

The second graph shows the MBA mortgage purchase index

The second graph shows the MBA mortgage purchase indexAccording to the MBA, purchase activity is up 15% year-over-year unadjusted.

Note: Red is a four-week average (blue is weekly).

Tuesday, February 16, 2021

Wednesday: Retail Sales, PPI, Industrial Production, Homebuilder Survey, Q4 Report on Household Debt

by Calculated Risk on 2/16/2021 09:06:00 PM

From Matthew Graham at Mortgage News Daily: Rates Surge; Time To Adjust Your Mortgage Game Plan

Recovery prospects, renewed focus on stimulus, inflation concerns, a brighter covid outlook, etc... All of these are reasons for an ongoing, gradual trend toward higher rates in 2021 (i.e. general bond market weakness) but none of them really explain why the bond market had its worst day in months today specifically.Wednesday:

...

In outright terms, the average 30yr fixed rate is still under 3%, so the world (of low rates) is far from over. [30 year fixed 2.96%]

emphasis added

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, Retail sales for January is scheduled to be released. The consensus is for a 1.0% increase in retail sales.

• Also at 8:30 AM, The Producer Price Index for December from the BLS. The consensus is for a 0.4% increase in PPI, and a 0.3% increase in core PPI.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for January. The consensus is for a 0.4% increase in Industrial Production, and for Capacity Utilization to increase to 74.8%.

• At 10:00 AM, The February NAHB homebuilder survey. The consensus is for a reading of 83, unchanged from 83. Any number above 50 indicates that more builders view sales conditions as good than poor.

• At 11:00 AM, NY Fed: Q4 Quarterly Report on Household Debt and Credit

February 16 COVID-19 Test Results and Vaccinations

by Calculated Risk on 2/16/2021 07:20:00 PM

SPECIAL NOTE: The Covid Tracking Project will end daily updates on March 7th. Heroes that filled a critical void! Quality government data will likely be available soon.

From Bloomberg on vaccinations as of Feb 16th.

"In the U.S., more Americans have now received at least one dose than have tested positive for the virus since the pandemic began. So far, 56.1 million doses have been given, according to a state-by-state tally. In the last week, an average of 1.67 million doses per day were administered."Here is the CDC COVID Data Tracker. This site has data on vaccinations, cases and more.

The US is averaged 1.5 million tests per day over the last week. Based on the experience of other countries, for adequate test-and-trace (and isolation) to reduce infections, the percent positive needs to be well under 5% (probably close to 1%), so the US has far too many daily cases - and percent positive - to do effective test-and-trace.

There were 1,060,442 test results reported over the last 24 hours.

There were 56,312 positive tests.

Over 46,000 US deaths have been reported in February. See the graph on US Daily Deaths here.

This data is from the COVID Tracking Project.

And check out COVID Act Now to see how each state is doing. (updated link to new site)

Click on graph for larger image.

Click on graph for larger image.This graph shows the 7 day average of positive tests reported and daily hospitalizations.

The dashed line is the previous peak for hospitalizations (almost back to the summer peak level).

The percent positive over the last 24 hours was 5.3%. The percent positive is calculated by dividing positive results by total tests (including pending).

Both cases and hospitalizations have peaked, but are still above the previous peaks.

The percent positive over the last 24 hours was 5.3%. The percent positive is calculated by dividing positive results by total tests (including pending).

Both cases and hospitalizations have peaked, but are still above the previous peaks.

Portland Real Estate in January: Sales Up 11% YoY, Inventory Down 48% YoY

by Calculated Risk on 2/16/2021 04:57:00 PM

Note: I'm posting data for many local markets around the U.S. The story is the same everywhere ... inventory is at record lows.

For Portland, OR:

Closed sales in January 2021 were 1,847, up 11.1% from 1,663 in January 2020.

Active Listings in January 2021 were 1,922, down 48.3% from 3,715 in January 2020.

Months of Supply was 1.0 Months in January 2021, compared to 2.2 Months in January 2020.

MBA Survey: "Share of Mortgage Loans in Forbearance Declines to 5.29%"

by Calculated Risk on 2/16/2021 04:00:00 PM

Note: This is as of February 7th.

From the MBA: Share of Mortgage Loans in Forbearance Declines to 5.29%

The Mortgage Bankers Association’s (MBA) latest Forbearance and Call Volume Survey revealed that the total number of loans now in forbearance decreased by 6 basis points from 5.35% of servicers’ portfolio volume in the prior week to 5.29% as of February 7, 2021. According to MBA’s estimate, 2.6 million homeowners are in forbearance plans.

...

“The share of loans in forbearance declined to the lowest level since April 5th of last year, due to decreases in both the GSE and Ginnie Mae portfolios,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “Similar to the trend in recent months, the first week of February showed a faster pace of exits from forbearance compared to recent weeks, while new forbearance requests were unchanged.”

Fratantoni added, “2.6 million homeowners remain in forbearance plans. MBA expects the rollout of the vaccines to boost economic growth through the course of the year, leading to a stronger job market and a greater ability for more struggling homeowners to get back on their feet. We do believe that additional support is needed until they have regained their jobs and incomes.”

...

• Total loans in forbearance decreased by 6 basis points relative to the prior week: from 5.35% to 5.29%.• By investor type, the share of Ginnie Mae loans in forbearance decreased relative to the prior week: from 7.46% to 7.34%.emphasis added

• The share of Fannie Mae and Freddie Mac loans in forbearance decreased relative to the prior week: from 3.07% to 3.01%.

• The share of other loans (e.g., portfolio and PLS loans) in forbearance remained unchanged relative to the prior week at 9.14%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time. Most of the increase was in late March and early April, then trended down - and has mostly moved slowly down recently.

The MBA notes: "Total weekly forbearance requests as a percent of servicing portfolio volume (#) remained unchanged relative to the prior week at 0.07%"

Maryland Real Estate in January: Sales Up 14% YoY, Inventory Down 63% YoY

by Calculated Risk on 2/16/2021 02:23:00 PM

Note: I'm posting data for many local markets around the U.S. The story is the same everywhere ... inventory is at record lows.

From the Maryland Realtors for the entire state:

Closed sales in January 2021 were 6,198, up 14.2% from 5,426 in January 2020.

Active Listings in January 2021 were 6,763, down 63.2% from 18,367 in January 2020.

Months of Supply was 0.8 Months in January 2021, compared to 2.5 Months in January 2020.

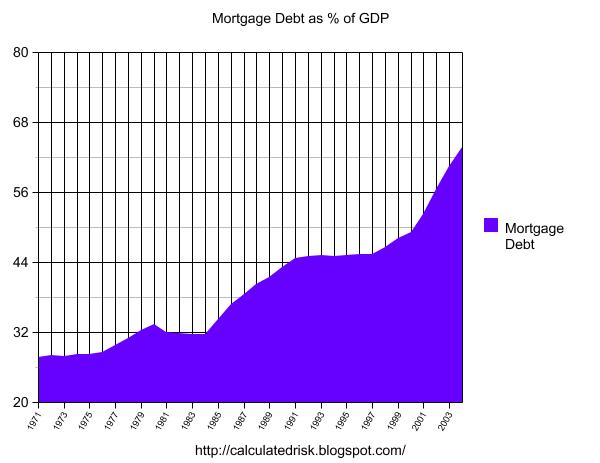

The Housing Bubble and Mortgage Debt as Percent of GDP

by Calculated Risk on 2/16/2021 12:29:00 PM

In a 2005 post, I included a graph of household mortgage debt as a percent of GDP. Several readers asked if I could update the graph.

First, from February 2005 (16 years ago!):

The following chart shows household mortgage debt as a % of GDP. Although mortgage debt has been increasing for years, the last four years have seen a tremendous increase in debt. Last year alone mortgage debt increased close to $800 Billion - almost 7% of GDP. ...CR Note: And a serious problem is what happened!

Many homeowners have refinanced their homes, in essence using their homes as an ATM.

It wouldn't take a RE bust to impact the general economy. Just a slowdown in both volume (to impact employment) and in prices (to slow down borrowing) might push the general economy into recession. An actual bust, especially with all of the extensive sub-prime lending, might cause a serious problem.

The second graph shows household mortgage debt as a percent of GDP through Q3 2020.

The second graph shows household mortgage debt as a percent of GDP through Q3 2020. The "bubble" is pretty obvious on this graph, and the sharp increase in mortgage debt was one of the warning signs.

The blip up in Q2 2020 was related to the collapse in GDP more than an increase in mortgage debt. With the recent house price increases, some people are worried about a new housing bubble - but mortgage debt isn't a concern (and lending standards are much better now then during the bubble).