RSS Feed

RSS Feed by Calculated Risk on 5/05/2025 02:14:00 PM

Monday, May 05, 2025

Recession Watch Metrics

Early in February, I expressed my "increasing concern" about the negative economic impact of "executive / fiscal policy errors", however, I concluded that post by noting that I was not currently on recession watch.

In early April, I went on recession watch, but I'm still not yet predicting a recession for several reasons: the U.S. economy is very resilient and was on solid footing at the beginning of the year, the administration might reverse many of the tariffs (we've seen that before), and Congress might take back complete authority for tariffs. Also, perhaps these tariffs are not enough to topple the economy.

"We should be looking to trade with the rest of the world, and we should do what we do best, and they should do what they do best ... Trade should not be a weapon.”In the short term, it is mostly trade policy that will negatively impact the economy. However, there are several policies that will negatively impact the economy in the long run, and I'll discuss those later.

Here is some of the data I'm watching.

Housing: Housing is the basis of one of my favorite models for business cycle forecasting.

This graph shows the YoY change in New Home Sales from the Census Bureau. Currently new home sales (based on 3-month average of NSA data) are up 2% year-over-year.

This graph shows the YoY change in New Home Sales from the Census Bureau. Currently new home sales (based on 3-month average of NSA data) are up 2% year-over-year.Usually when the YoY change in New Home Sales falls about 20%, a recession will follow. An exception for this data series was the mid '60s when the Vietnam buildup kept the economy out of recession. Another exception was in late 2021 - we saw a significant YoY decline in new home sales related to the pandemic and the surge in new home sales in the second half of 2020. I ignored that downturn as a pandemic distortion. Also note that the sharp decline in 2010 was related to the housing tax credit policy in 2009 - and was just a continuation of the housing bust.

The YoY change in new home sales in late 2022 and early 2023 suggested a possible recession. But as I noted earlier, I was able to look past the pandemic distortion and was able to predict a pickup in new home sales due to the low level of existing home inventory and because homebuilders could offer mortgage incentives that would somewhat offset the sharp increase in mortgage rates.

There are no special circumstances now, and if this measure falls to off 20% a recession seems likely.

Yield Curve: The yield curve is a commonly used leading indicator. I dismissed it when the yield curve inverted in 2019 and again in 2022. Both times dismissing the yield curve was correct (the recession in 2020 was obviously due to the pandemic, so we will never know if the yield curve failed to predict a recession in 2019).

Here is a graph of 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity from FRED since 1976.

The yield curve reverted to normal last year and is currently positive at 0.50. If this inverts, this might suggest a recession is coming.

Heavy Truck (and Vehicle Sales): Another indicator I like to use is heavy truck sales. This graph shows heavy truck sales since 1967 using data from the BEA. he dashed line is the April 2025 seasonally adjusted annual sales rate (SAAR) of 403 thousand. Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight."

Heavy truck sales were at 505 thousand SAAR in April, up from 450 thousand in March, and up 0.8% from 501 thousand SAAR in April 2025 (essentially unchanged YoY).

Usually, heavy truck sales decline sharply prior to a recession and sales were solid in April. It is likely that some April truck buyers rushed to beat the tariffs - and we might see some weakness next month.

And light vehicle sales were strong in April.

And light vehicle sales were strong in April. This graph shows light vehicle sales since the BEA started keeping data in 1967. This is more of a concurrent indicator than heavy trucks.

Light vehicle sales were at 17.27 million SAAR in April, down 3.1% from March, and up 7.8% from April 2024 as some buyers rushed to beat the tariffs.

Unemployment: Two other concurrent indicators are the unemployment rate (using the "Sahm Rule") and weekly unemployment claims.

Here is a graph of the Sahm rule from FRED since 1959.

Here is a graph of the Sahm rule from FRED since 1959.The Sahm Rule was at 0.27 in March (Last data at FRED) and increased to 0.30 in April.

If this increases to 0.5 it will suggest a possible recession.

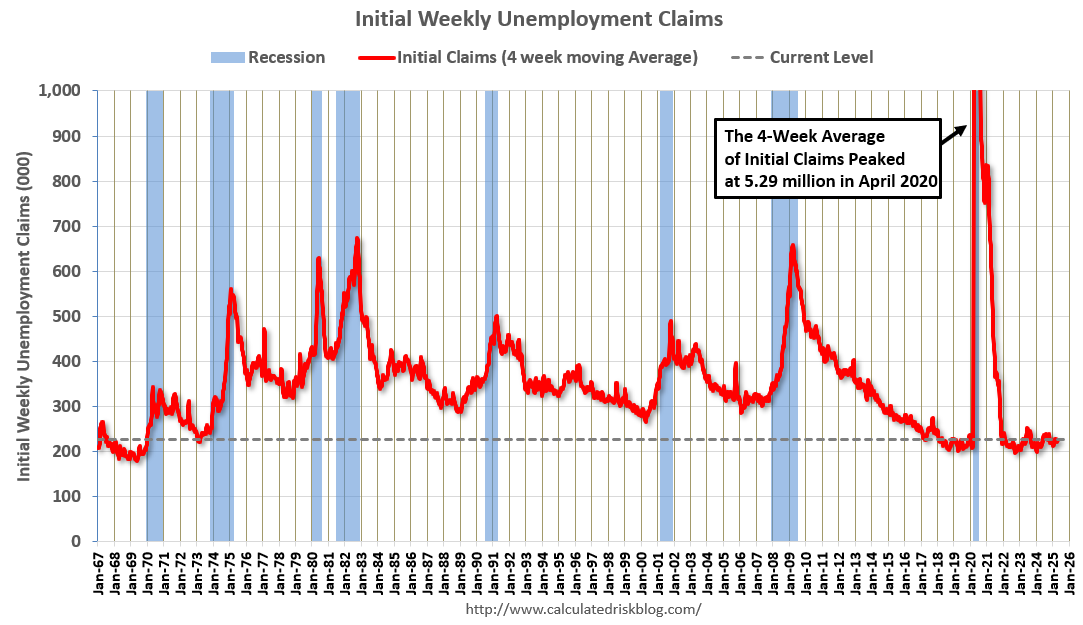

And weekly unemployment claims always rise sharply at the beginning of a recession (other events - like hurricane Katrina - can cause a temporary spike in weekly claims).

And weekly unemployment claims always rise sharply at the beginning of a recession (other events - like hurricane Katrina - can cause a temporary spike in weekly claims).

And weekly unemployment claims always rise sharply at the beginning of a recession (other events - like hurricane Katrina - can cause a temporary spike in weekly claims).

And weekly unemployment claims always rise sharply at the beginning of a recession (other events - like hurricane Katrina - can cause a temporary spike in weekly claims).As I noted earlier, I'm not sure how to estimate the economic damage caused by these tariffs. And they might just go away (no one knows). There are also boycotts of U.S. goods and less international tourism based on both the tariffs and the inflammatory rhetoric of the new administration.

None of the leading are suggesting recession. For now, I'll focus on the leading indicators (especially housing) and I'll update this post monthly while I'm on recession watch.