RSS Feed

RSS Feed by Calculated Risk on 4/26/2014 01:11:00 PM

Saturday, April 26, 2014

Schedule for Week of April 27th

This will be a busy week for economic data with several key reports including the April employment report on Friday and the advance Q1 GDP report on Wednesday.

Other key reports include the ISM manufacturing index on Thursday, April vehicle sales, also on Thursday, and the February Case-Shiller house price index on Tuesday.

There will a two-day FOMC meeting on Tuesday and Wednesday, and the Fed is expected to announce on Wednesday a decrease in asset purchases from $55 billion per month to $45 billion per month.

10:00 AM ET: Pending Home Sales Index for March. The consensus is for a 0.6% increase in the index.

10:30 AM: Dallas Fed Manufacturing Survey for April. This is the last of the regional Fed manufacturing surveys for April.

9:00 AM: S&P/Case-Shiller House Price Index for February. Although this is the February report, it is really a 3 month average of December, January and February.

9:00 AM: S&P/Case-Shiller House Price Index for February. Although this is the February report, it is really a 3 month average of December, January and February. This graph shows the nominal seasonally adjusted Composite 10 and Composite 20 indexes through January 2014 (the Composite 20 was started in January 2000).

The consensus is for a 13.0% year-over-year increase in the Composite 20 index (NSA) for February. The Zillow forecast is for the Composite 20 to increase 12.8% year-over-year, and for prices to increase 0.6% month-to-month seasonally adjusted.

10:00 AM: Conference Board's consumer confidence index for April. The consensus is for the index to increase to 83.0 from 82.3.

10:00 AM: Q1 Housing Vacancies and Homeownership report from the Census Bureau. This report is frequently mentioned by analysts and the media to report on the homeownership rate, and the homeowner and rental vacancy rates. However, this report doesn't track with other measures (like the decennial Census and the ACS).

7:00 AM: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for April. This report is for private payrolls only (no government). The consensus is for 210,000 payroll jobs added in April, up from 191,000 in March.

8:30 AM: Q1 GDP (advance estimate). This is the advance estimate of Q1 GDP from the BEA. The consensus is that real GDP increased 1.1% annualized in Q1.

9:45 AM: Chicago Purchasing Managers Index for April. The consensus is for an increase to 56.9, up from 55.9 in March.

2:00 PM: FOMC Meeting Announcement. No change in interest rates is expected (for a long time). However the FOMC is expected to reduce QE3 asset purchases by $10 billion per month at this meeting.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for claims to decrease to 320 thousand from 329 thousand.

All day: Light vehicle sales for April. The consensus is for light vehicle sales to decrease to 16.2 million SAAR in April (Seasonally Adjusted Annual Rate) from 16.3 million SAAR in March.

All day: Light vehicle sales for April. The consensus is for light vehicle sales to decrease to 16.2 million SAAR in April (Seasonally Adjusted Annual Rate) from 16.3 million SAAR in March.This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the March sales rate.

8:30 AM: Personal Income and Outlays for March. The consensus is for a 0.4% increase in personal income, and for a 0.6% increase in personal spending. And for the Core PCE price index to increase 0.2%.

8:30 AM: Speech by Fed Chair Janet Yellen, Community Bank Supervision, At the Independent Community Bankers of America 2014 Washington Policy Summit, Washington, D.C.

9:00 AM ET: The Markit US PMI Manufacturing Index for April.

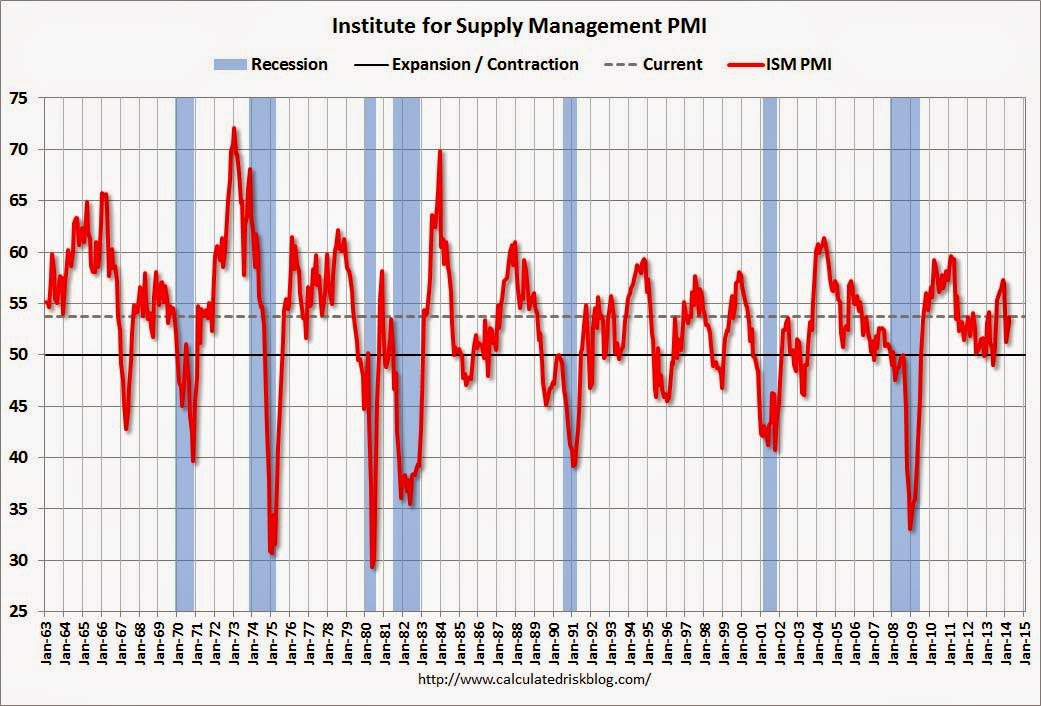

10:00 AM ET: ISM Manufacturing Index for April. The consensus is for an increase to 54.2 from 53.7 in March.

10:00 AM ET: ISM Manufacturing Index for April. The consensus is for an increase to 54.2 from 53.7 in March.Here is a long term graph of the ISM manufacturing index.

The ISM manufacturing index indicated expansion in March at 53.7%. The employment index was at 51.1%, and the new orders index was at 55.1%.

10:00 AM: Construction Spending for March. The consensus is for a 0.6% increase in construction spending.

8:30 AM: Employment Report for April. The consensus is for an increase of 215,000 non-farm payroll jobs in April, up from the 192,000 non-farm payroll jobs added in March.

The consensus is for the unemployment rate to decline to 6.6% in April.

This graph shows the percentage of payroll jobs lost during post WWII recessions through March.

This graph shows the percentage of payroll jobs lost during post WWII recessions through March.The economy has added 8.9 million private sector jobs since employment bottomed in February 2010 (8.3 million total jobs added including all the public sector layoffs).

There are 110 thousand more private sector jobs now than when the recession started in 2007, but total employment is still 437 thousand below the pre-recession peak.

10:00 AM: Manufacturers' Shipments, Inventories and Orders (Factory Orders) for March. The consensus is for a 1.3% increase in March orders.