RSS Feed

RSS Feed by Calculated Risk on 11/03/2006 02:02:00 PM

Friday, November 03, 2006

FDIC: Economic Conditions and Emerging Risks in Banking

The FDIC Semiannual Report: Economic Conditions and Emerging Risks in Banking has been released. The report identifies several risks: declining Net Interest Margins because of the inverted yield curve, the housing market in general and sub-prime lending specifically, looser lending standards and concentration risk - especially for mid-sized institutions - in commercial real estate (CRE) and construction & development (C&D).

Before noting the negative comments, the FDIC outlook is the same as the consensus: a soft landing. Click on graph for larger image.

Click on graph for larger image.

GDP is expected to grow at a rate below its long-run average over the next year due to the combination of a slowing housing market, continued high energy prices, slowing production in the auto industry, and lagged effects of previous interest rate increases. However, the corporate sector continues to perform well. Corporate profits currently make up more than 12 percent of GDP—the highest proportion since the 1960s—and grew more than 20 percent in the twelve months to June 30, 2006. Corporate balance sheets are also strong and reflect a debt-to-net-worth ratio for the second quarter of just over 40 percent, the lowest point since the mid-1980s.The FDIC expressed concern about households:

Household liabilities, on the other hand, reached an all-time high of more than 19 percent of assets by the end of the second quarter 2006, as the personal saving rate has fallen into negative territory for five consecutive quarters. Housing-related debt service costs are at all-time highs, and use of home equity loans has slowed sharply as the effects of recent interest rate increases set in.The second graph shows declining Net Interest Margins (NIMs) due to the inverted yield curve:

... the Treasury yield curve, which exhibited a small positive slope at the time of our last report, is currently more inverted than at any point since 2001. The inverted yield curve is pressuring lending institutions, which tend to have liabilities priced according to short-term interest rates and assets priced according to long-term interest rates. As a result, NIMs have fallen, particularly at large institutions, whose liabilities are more elastic than smaller banks’ due to their smaller percentage of core deposits. Four of six Regional Risk Committees cited interest rate risk as a potential concern due to the flat-to-inverted yield curve and narrowing margins.After reviewing the "softening housing market", the FDIC expressed concern about nontraditional mortages:

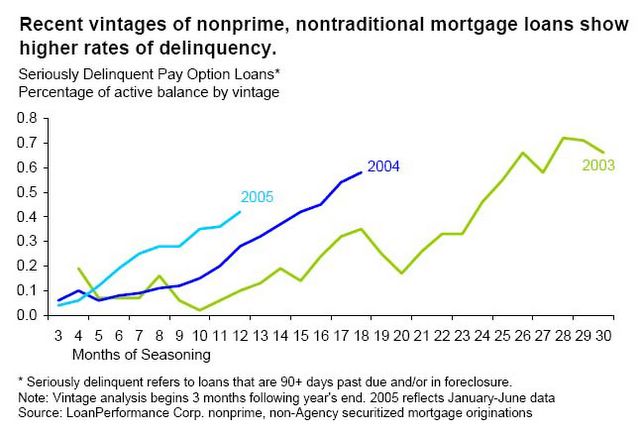

It is very likely that both delinquency and foreclosure rates will rise if the housing slowdown deepens. The first fault lines likely to appear in mortgage credit performance would be among highly leveraged, variable rate borrowers who have stretched their financial resources to purchase a home during the recent housing boom. Five of six Regional Risk Committees reported some level of concern about future performance of prime residential loans due to slowing home price appreciation.

There are emerging signs of potential credit distress among holders of subprime adjustable-rate mortgages (ARMs). Nationwide, foreclosures started on subprime ARMs made up 2.0 percent of loans in the second quarter, up from 1.3 percent in mid-2004. Subprime ARMs are experiencing stress in states as diverse as California, which has had rapid home price gains and solid economic performance, and Michigan, where house prices have been stagnant and the economy is weaker. This suggests that national factors, like interest rate increases, are important factors behind subprime mortgage credit stress, in addition to local economic or housing market conditions.

Certain household-sector developments that have emerged during the recent housing boom could potentially amplify the adverse effects of a housing slowdown. These developments include: (1) a negative personal saving rate and unprecedented levels of home equity liquidation, (2) a greater degree of homeowner leverage, and (3) much broader use of so-called alternative mortgage products, including interest-only and payment option mortgages. With household finances already under pressure from high financial obligation ratios, these developments may place homeowners in a more tenuous position than has been the case prior to previous periods of housing weakness.And another area of concern is the concentration of loans for CRE and C&D:

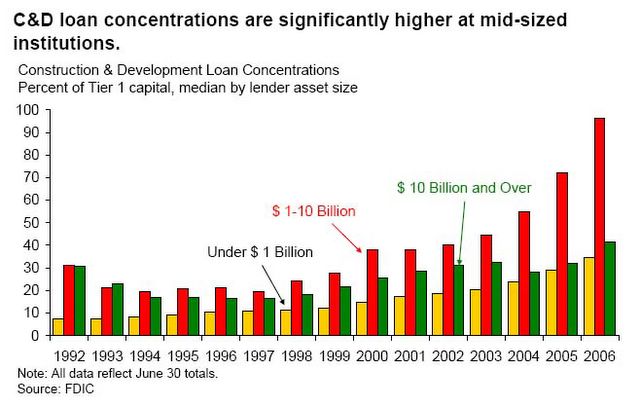

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loan

concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.