RSS Feed

RSS Feed by Calculated Risk on 7/24/2006 03:39:00 PM

Monday, July 24, 2006

FDIC: Breaking New Ground in U.S. Mortgage Lending

From the FDIC Summer Outlook 2006:

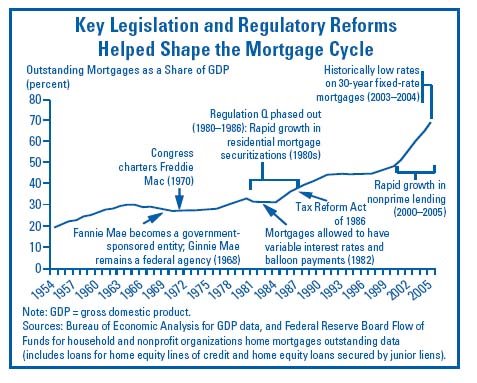

[Mortgage lending] growth has not come without risk. Widespread marketing of nontraditional products could be raising the risk profile of some mortgage lenders and consumers. Growing unease about risk taking by lenders and consumers recently led bank regulators to propose new supervisory guidelines on risks of, and disclosures for, various mortgage products.Looking at the first chart, it appears the boom happened during a period of historically low interest rates and a rapid increase in non-prime lending.

This article examines historical developments in mortgage loan volume and underwriting trends. It also assesses the significance of recent market and institutional innovations in light of historical trends, reviews mortgage loan performance trends, discusses the role of regulation, and considers the near-term outlook for the mortgage lending cycle.

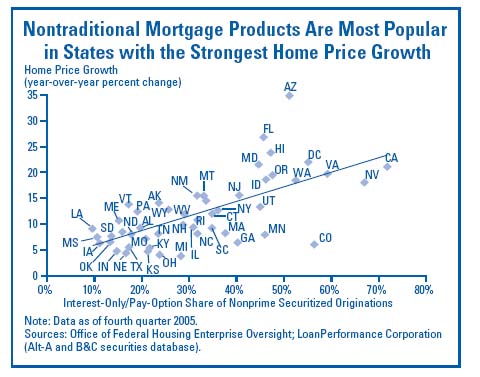

Since 2003, strong home price appreciation and declining affordability have helped drive growing demand for nontraditional mortgage products that can be used to stretch home-buying power. Aided by new computer models and an easing in lending standards, many lenders have accommodated this demand by expanding

the variety of nontraditional mortgage products offered while also extending loans to borrowers with less-than stellar credit histories. As a result, by 2005, nonprime

lending, comprised of subprime and Alt-A (low- or nodocumentation) loans, accounted for about 33 percent of all mortgage loan originations, up from almost 11 percent in 2003.

Rapid growth also has occurred among some of the higher-risk mortgage alternatives within the nonprime arena. As recently as 2002, IOs and pay-option ARMsThere is much more in the FDIC outlook.

represented only 3 percent of total nonprime mortgage originations that were securitized. However, the IO share of credit to nonprime borrowers has soared during the past two years to 30 percent of securitized nonprime mortgages, while the pay-option product jumped to a similar share in less time (see Chart).

Furthermore, the low- or no-documentation share of subprime lending has grown significantly since 2001, from about 25 percent to just over 40 percent.