RSS Feed

RSS Feed by Calculated Risk on 4/22/2024 08:14:00 AM

Monday, April 22, 2024

DOT: Vehicle Miles Driven Increased 1.4% year-over-year in February 2024 SA

This is something I check occasionally.

The Department of Transportation (DOT) reported:

• Travel on all roads and streets changed by +2.0% (+4.8 billion vehicle miles) for February 2024 as compared with February 2023. Travel for the month is estimated to be 240.2 billion vehicle miles.

• The seasonally adjusted vehicle miles traveled for February 2024 is 274.8 billion miles, a +1.4% ( +3.9 billion vehicle miles) change over February 2023. It also represents a 0.6% change (1.7 billion vehicle miles) compared with January 2024.

• Cumulative Travel for 2024 changed by +0.6% (+2.7 billion vehicle miles). The cumulative estimate for the year is 487.4 billion vehicle miles of travel.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the monthly total vehicle miles driven, seasonally adjusted.

Miles driven declined sharply in March 2020, and really collapsed in April 2020. Miles driven are now at pre-pandemic levels.

Sunday, April 21, 2024

Sunday Night Futures

by Calculated Risk on 4/21/2024 07:14:00 PM

Weekend:

• Schedule for Week of April 21, 2024

Monday:

• At 8:30 AM ET, Chicago Fed National Activity Index for March. This is a composite index of other data.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 17 and DOW futures are up 100 (fair value).

Oil prices were up over the last week with WTI futures at $83.26 per barrel and Brent at $86.96 per barrel. A year ago, WTI was at $78, and Brent was at $83 - so WTI oil prices are up year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.64 per gallon. A year ago, prices were at $3.67 per gallon, so gasoline prices are down $0.03 year-over-year.

When Do Market Participants Expect the Fed to Cut Rates?

by Calculated Risk on 4/21/2024 09:40:00 AM

As of December 2023, looking at the "dot plot", most FOMC participants expected between 2 and 4 rate cuts in 2024:

| As of Dec 2023 Meeting | |

|---|---|

| 25 bp Rate Cuts | FOMC Members |

| No Change | 2 |

| One Rate Cut | 1 |

| Two Rate Cuts | 5 |

| Three Rate Cuts | 6 |

| Four Rate Cuts | 4 |

| More than Four | 1 |

As of the March 2024 meeting, FOMC participants were down to 2 to 3 rate cuts in 2024:

| As of Mar 2024 Meeting | |

|---|---|

| 25 bp Rate Cuts | FOMC Members |

| No Change | 2 |

| One Rate Cut | 2 |

| Two Rate Cuts | 5 |

| Three Rate Cuts | 9 |

| Four Rate Cuts | 1 |

Most market participants expect between 1 and 2 rate cuts this year, with the first cut in September. Here are a couple analyst views:

From BofA:

[W]e revised our Fed forecasts in response to the upside surprise in the March inflation data. We now expect the Fed to start cutting in December rather than June, and we still think cuts will proceed at a quarterly cadence. Importantly, we did not simply push our projected cutting cycle out by two quarters. We removed the June and September 2024 cuts entirely from our forecast, raising the terminal rate by 50bp to 3.5-3.75%.From Goldman Sachs:

The FOMC was already narrowly divided on its three-cut baseline for 2024, and we think it will now need to see the string of three firmer inflation prints from January to March balanced by a series of softer prints in subsequent months.

We continue to expect cuts at a quarterly pace after July, which now implies two cuts in 2024 in July and November.

Saturday, April 20, 2024

Real Estate Newsletter Articles this Week: Single Family Starts Up 22% Year-over-year in March; Multi-Family Starts Down Sharply

by Calculated Risk on 4/20/2024 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• Single Family Starts Up 22% Year-over-year in March; Multi-Family Starts Down Sharply

• NAR: Existing-Home Sales Decreased to 4.19 million SAAR in March

• NMHC: "Apartment Market Continues to Loosen"

• 4th Look at Local Housing Markets in March; California Home Sales Down 4.4% YoY in March

• Lawler: Early Read on Existing Home Sales in March

• 3rd Look at Local Housing Markets in March

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of April 21, 2024

by Calculated Risk on 4/20/2024 08:11:00 AM

The key reports scheduled for this week are the advance estimate of Q1 GDP, March New Home sales and March Personal Income and Outlays.

For manufacturing, the April Richmond and Kansas City manufacturing surveys will be released.

8:30 AM ET: Chicago Fed National Activity Index for March. This is a composite index of other data.

10:00 AM: New Home Sales for March from the Census Bureau.

10:00 AM: New Home Sales for March from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 670 thousand SAAR, up from 662 thousand in February.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for April.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Durable Goods Orders for March from the Census Bureau. The consensus is for a 2.0% increase in durable goods orders.

During the day: The AIA's Architecture Billings Index for March (a leading indicator for commercial real estate).

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 210 thousand initial claims, down from 212 thousand last week.

8:30 AM: Gross Domestic Product, 1st quarter 2024 (Advance estimate). The consensus is that real GDP increased 2.1% annualized in Q1, down from 3.4% in Q4.

10:00 AM: Pending Home Sales Index for March. The consensus is for a 2.0% decrease in the index.

11:00 AM: the Kansas City Fed manufacturing survey for April.

8:30 AM ET: Personal Income and Outlays, March 2024. The consensus is for a 0.5% increase in personal income, and for a 0.3% increase in personal spending. And for the Core PCE price index to increase 0.3%. PCE prices are expected to be up 2.6% YoY, and core PCE prices up 2.7% YoY.

10:00 AM: University of Michigan's Consumer sentiment index (Final for April). The consensus is for a reading of 77.9.

Friday, April 19, 2024

April 19th COVID Update: Weekly Deaths Decreased

by Calculated Risk on 4/19/2024 07:11:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

It is likely that we will see pandemic lows for hospitalizations and deaths in the next several weeks. That is welcome news!

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Hospitalizations have declined significantly from the winter high of 30,027 but are still slightly above the low of 5,386 last year.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Hospitalized2 | 5,899 | 6,686 | ≤3,0001 | |

| Deaths per Week2 | 779 | 982 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Hospitalized and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Weekly deaths have declined sharply from the recent peak of 2,558 but are still 50% above the low of 490 last July.

This appears to be a leading indicator for COVID hospitalizations and deaths.

This appears to be a leading indicator for COVID hospitalizations and deaths.Nationally, COVID in wastewater is now off close to 90% from the holiday peak at the end of December, and that suggests weekly hospitalizations and deaths will continue to decline.

Q1 GDP Tracking: Movin' on Up

by Calculated Risk on 4/19/2024 11:31:00 AM

From BofA:

Since our update last week, 1Q GDP tracking is up two-tenths to 2.1% q/q saar. [Apr 19th estimate]From Goldman:

emphasis added

We left our Q1 GDP forecast unchanged at +3.1% (qoq ar) and our domestic final sales forecast also unchanged at +3.1% (qoq ar). [Apr 18th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2024 is 2.9 percent on April 16, up from 2.8 percent on April 15. [April 16th estimate]

NMHC: "Apartment Market Continues to Loosen"

by Calculated Risk on 4/19/2024 08:10:00 AM

Today, in the CalculatedRisk Real Estate Newsletter: NMHC: "Apartment Market Continues to Loosen"

Excerpt:

From the NMHC: Apartment Market Continues to Loosen Amidst Worsening Financing ConditionsThere is much more in the article.Apartment market conditions continued to weaken in the National Multifamily Housing Council’s (NMHC’s) Quarterly Survey of Apartment Market Conditions for April 2024. With the exception of Sales Volume (52), which turned positive this quarter, the Market Tightness (41), Equity Financing (49), and Debt Financing (44) indexes all came in below the breakeven level (50).

...

"[T]he U.S. apartment market continues to absorb historic levels of new supply, resulting in rising vacancy rates and decreasing rent growth.”

...• The Market Tightness Index came in at 41 this quarter – below the breakeven level (50) – indicating looser market conditions for the seventh consecutive quarter. That said, a plurality of respondents (42%) thought market conditions were unchanged compared to three months ago, while 37% thought markets have become looser. Twenty percent of respondents reported tighter markets than three months ago, up from 5% in January.The quarterly index increased to 41 in April from 23 in January. Any reading below 50 indicates looser conditions from the previous quarter.

This index has been an excellent leading indicator for rents and vacancy rates, and this suggests higher vacancy rates and a further weakness in asking rents. This is the seventh consecutive quarter with looser conditions than the previous quarter.

Thursday, April 18, 2024

Hotels: Occupancy Rate Increased 2.8% Year-over-year

by Calculated Risk on 4/18/2024 06:11:00 PM

Helped by the total solar eclipse, U.S. hotel performance increased from the previous week, according to CoStar’s latest data through 13 April. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

7-13 April 2024 (percentage change from comparable week in 2023):

• Occupancy: 65.8% (+2.8%)

• Average daily rate (ADR): US$160.20 (+2.9%)

• Revenue per available room (RevPAR): US$105.48 (+5.8%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2024, black is 2020, blue is the median, and dashed light blue is for 2023. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking last year, and also at the median rate for the period 2000 through 2023 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will move mostly sideways seasonally until the summer travel season.

Realtor.com Reports Active Inventory UP 29.1% YoY; New Listings Up 7.2% YoY

by Calculated Risk on 4/18/2024 02:01:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For March, Realtor.com reported inventory was up 23.5% YoY, but still down almost 38% compared to March 2017 to 2019 levels.

Now - on a weekly basis - inventory is up 29.1% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data Week Ending April 13, 2024 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 23rd consecutive week following 20 consecutive weeks with a YoY decrease in inventory.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data Week Ending April 13, 2024

• Active inventory increased, with for-sale homes 29.1% above year-ago levels.

For the 23rd week in a row, there were more homes listed for sale compared with the previous year, giving homebuyers a wider selection to choose from. However, this week’s increase was not as high as the 30.4% growth seen last week, possibly suggesting a slowdown in inventory growth. This could be due to the continued impact of high mortgage rates, which might be discouraging some sellers from listing their homes.

• New listings–a measure of sellers putting homes up for sale–were up this week, by 7.2% from one year ago.

Following some ups and downs around Easter, sellers kept putting homes on the market at a faster rate compared with last year, with a 7.2% increase in newly listed homes. However, this growth rate is slower than what we’ve seen since early February.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 23rd consecutive week following 20 consecutive weeks with a YoY decrease in inventory.

Inventory is still historically very low.

New listings remain below typical pre-pandemic levels although increasing.

NAR: Existing-Home Sales Decreased to 4.19 million SAAR in March; Median House Prices Increased 4.8% Year-over-Year

by Calculated Risk on 4/18/2024 10:40:00 AM

Today, in the CalculatedRisk Real Estate Newsletter: NAR: Existing-Home Sales Decreased to 4.19 million SAAR in March

Excerpt:

Sales Year-over-Year and Not Seasonally Adjusted (NSA)There is much more in the article.

The fourth graph shows existing home sales by month for 2023 and 2024.

Sales declined 3.7% year-over-year compared to March 2023. This was the thirty-first consecutive month with sales down year-over-year.

NAR: Existing-Home Sales Decreased to 4.19 million SAAR in March

by Calculated Risk on 4/18/2024 10:00:00 AM

From the NAR: Existing-Home Sales Descended 4.3% in March

Existing-home sales slipped in March, according to the National Association of REALTORS®. Among the four major U.S. regions, sales slid in the Midwest, South and West, but rose in the Northeast for the first time since November 2023. Year-over-year, sales decreased in all regions.

Total existing-home sales – completed transactions that include single-family homes, townhomes, condominiums and co-ops – receded 4.3% from February to a seasonally adjusted annual rate of 4.19 million in March. Year-over-year, sales waned 3.7% (down from 4.35 million in March 2023).

...

Total housing inventory registered at the end of March was 1.11 million units, up 4.7% from February and 14.4% from one year ago (970,000). Unsold inventory sits at a 3.2-month supply at the current sales pace, up from 2.9 months in February and 2.7 months in March 2023.

emphasis added

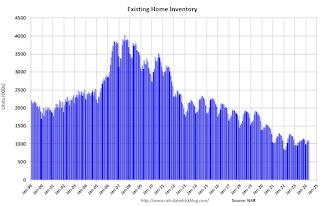

Click on graph for larger image.

Click on graph for larger image.This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1994.

Sales in March (4.19 million SAAR) were down 4.3% from the previous month and were 3.7% below the March 2023 sales rate.

The second graph shows nationwide inventory for existing homes.

According to the NAR, inventory increased to 1.11 million in March from 1.06 million the previous month.

According to the NAR, inventory increased to 1.11 million in March from 1.06 million the previous month.

According to the NAR, inventory increased to 1.11 million in March from 1.06 million the previous month.

According to the NAR, inventory increased to 1.11 million in March from 1.06 million the previous month.Headline inventory is not seasonally adjusted, and inventory usually decreases to the seasonal lows in December and January, and peaks in mid-to-late summer.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was up 14.4% year-over-year (blue) in March compared to March 2023.

Inventory was up 14.4% year-over-year (blue) in March compared to March 2023.

Months of supply (red) increased to 3.2 months in March from 2.9 months the previous month.

This was at the consensus forecast. I'll have more later.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was up 14.4% year-over-year (blue) in March compared to March 2023.

Inventory was up 14.4% year-over-year (blue) in March compared to March 2023. Months of supply (red) increased to 3.2 months in March from 2.9 months the previous month.

This was at the consensus forecast. I'll have more later.

Weekly Initial Unemployment Claims Unchanged at 212,000

by Calculated Risk on 4/18/2024 08:30:00 AM

The DOL reported:

In the week ending April 13, the advance figure for seasonally adjusted initial claims was 212,000, unchanged from the previous week's revised level. The previous week's level was revised up by 1,000 from 211,000 to 212,000. The 4-week moving average was 214,500, unchanged from the previous week's revised average. The previous week's average was revised up by 250 from 214,250 to 214,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 214,500.

The previous week was revised up.

Weekly claims were lower than the consensus forecast.

Wednesday, April 17, 2024

Thursday: Unemployment Claims, Philly Fed Mfg, Existing Home Sales

by Calculated Risk on 4/17/2024 08:23:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 217 thousand initial claims, up from 211 thousand last week.

• Also at 8:30 AM, the Philly Fed manufacturing survey for April. The consensus is for a reading of 0.0, down from 3.2.

• At 10:00 AM, Existing Home Sales for March from the National Association of Realtors (NAR). The consensus is for 4.20 million SAAR, down from 4.38 million.

4th Look at Local Housing Markets in March; California Home Sales Down 4.4% YoY in March

by Calculated Risk on 4/17/2024 04:21:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 4th Look at Local Housing Markets in March; California Home Sales Down 4.4% YoY in March

A brief excerpt:

The NAR is scheduled to release March existing home sales tomorrow, Thursday, April 18th at 10:00AM ET. The consensus is for 4.20 million SAAR, down from 4.38 million in February.There is much more in the article.

Housing economist Tom Lawler expects the NAR to report sales of 4.23 million SAAR for March.

...

And a table of March sales.

In March, sales in these markets were down 9.7% YoY. In February, these same markets were up 1.6% year-over-year Not Seasonally Adjusted (NSA).

Sales in most of these markets are down compared to 2019.

This is a year-over-year decrease NSA for these early reporting markets. However, there were two fewer working days in March 2024 compared to March 2023, so sales Seasonally Adjusted will be higher year-over-year than Not Seasonally Adjusted sales.

...

More local markets will release data after the NAR release tomorrow!

Fed's Beige Book: "Economic activity expanded slightly"

by Calculated Risk on 4/17/2024 02:00:00 PM

Overall economic activity expanded slightly, on balance, since late February. Ten out of twelve Districts experienced either slight or modest economic growth—up from eight in the previous report, while the other two reported no changes in activity. Consumer spending barely increased overall, but reports were quite mixed across Districts and spending categories. Several reports mentioned weakness in discretionary spending, as consumers' price sensitivity remained elevated. Auto spending was buoyed notably in some Districts by improved inventories and dealer incentives, but sales remained sluggish in other Districts. Tourism activity increased modestly, on average, but reports varied widely. Manufacturing activity declined slightly, as only three Districts reported growth in that sector. Contacts reported slight increases in nonfinancial services activity, on average, and bank lending was roughly flat overall. Residential construction increased a little, on average, and home sales strengthened in most Districts. In contrast, nonresidential construction was flat, and commercial real estate leasing fell slightly. The economic outlook among contacts was cautiously optimistic, on balance.

Labor Markets

Employment rose at a slight pace overall, with nine Districts reporting very slow to modest increases, and the remaining three Districts reporting no changes in employment. Most Districts noted increases in labor supply and in the quality of job applicants. Several Districts reported improved retention of employees, and others pointed to staff reductions at some firms. Despite the improvements in labor supply, many Districts described persistent shortages of qualified applicants for certain positions, including machinists, trades workers, and hospitality workers. Wages grew at a moderate pace in eight Districts, with the remaining four noting only slight to modest wage increases. Multiple Districts said that annual wage growth rates had recently returned to their historical averages. On balance, contacts expected that labor demand and supply would remain relatively stable, with modest further job gains and continued moderation of wage growth back to pre-pandemic levels.

Prices

Price increases were modest, on average, running at about the same pace as in the last report. Disruptions in the Red Sea and the collapse of Baltimore's Key Bridge caused some shipping delays but so far did not lead to widespread price increases.

emphasis added

LA Port Traffic Increased Year-over-year in March

by Calculated Risk on 4/17/2024 01:41:00 PM

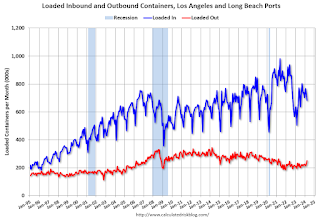

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12-month basis, inbound traffic increased 1.0% in March compared to the rolling 12 months ending in February. Outbound traffic increased 0.7% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year. Imports were up 14% YoY in March, and exports were up 8% YoY.

In general, it appears port traffic is returning to the pre-pandemic patterns.

MBA: Mortgage Applications Increased in Weekly Survey

by Calculated Risk on 4/17/2024 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

“Rates increased for the second consecutive week, driven by incoming data indicating that the economy remains strong and inflation is proving tougher to bring down. Mortgage rates increased across the board, with the 30-year fixed rate at 7.13 percent – reaching its highest level since December 2023,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Despite these higher rates, application activity picked up, possibly as some borrowers decided to act in case rates continue to rise. Purchase applications drove most of the increase, but remain at low levels of around 10 percent behind last year’s pace. Refinance applications increased very slightly, driven by a 3 percent gain in conventional applications.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 7.13 percent from 7.01 percent, with points increasing to 0.65 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is down 10% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is up slightly from the lows in late October 2023, and below the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index declined sharply in 2022, and has mostly flat lined since then.

Tuesday, April 16, 2024

Wednesday: Beige Book

by Calculated Risk on 4/16/2024 09:11:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 2:00 PM, the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

Lawler: Early Read on Existing Home Sales in March

by Calculated Risk on 4/16/2024 03:50:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Lawler: Early Read on Existing Home Sales in March

A brief excerpt:

From housing economist Tom Lawler:Based on publicly-available local realtor/MLS reports released across the country through today, I project that existing home sales as estimated by the National Association of Realtors ran at a seasonally adjusted annual rate of 4.23 million in March, down 3.4% from February’s preliminary pace and down 2.8% from last ’s March’s seasonally adjusted pace. Unadjusted sales should show a larger YOY decline, as there were two fewer business days this March compared to last March.CR Note: The NAR is scheduled to release March existing home sales on Thursday, April 18th. The consensus is for 4.20 million SAAR, down from 4.38 million in February.

Local realtor/MLS reports suggest that the median existing single-family home sales price last month was up by about 6% from last March.