RSS Feed

RSS Feed by Calculated Risk on 3/23/2023 01:41:00 PM

Thursday, March 23, 2023

More Good News for Homebuilders

Today, in the Calculated Risk Real Estate Newsletter: More Good News for Homebuilders

A brief excerpt:

Last October I wrote: Some "Good News" for HomebuildersThere is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

I noted:[T]he good news for the homebuilders is activity usually picks up quickly following an interest rate induced slowdown (as opposed to following the housing bust when the recovery took many years).I included the following graph to illustrate this point. The following graph shows new home sales for three periods: 1978-1982, 2005-2020, and current (red). The prior peak in sales is set to 100 (updated through the February New Home sales release).

...

My sense is this downturn will have some similarities to the 1980 period, see: Housing: Don't Compare the Current Housing Boom to the Bubble and Bust

Black Knight: Mortgage Delinquencies Increased Slightly in February

by Calculated Risk on 3/23/2023 12:33:00 PM

From Black Knight: Black Knight’s First Look at February 2023 Mortgage Data: Prepayments Rebound from All-Time Low; Overall Mortgage Delinquencies Inch Up As 30-Days Late Payments Rise

• The national mortgage delinquency rate increased 7 basis points in February to 3.45%, but remains down 12.6% year over yearAccording to Black Knight's First Look report, the percent of loans delinquent increased 2.0% in February compared to January and decreased 13% year-over-year.

• Prepayment activity (SMM) inched up to 0.35% – breaking a four-month streak of record lows, with relief likely to extend as the spring homebuying season takes hold

• A 36K rise in overall delinquencies was driven by a nearly 65K increase in those just a single payment behind, while 60-day delinquencies fell by nearly 12K (-4.0%) and 90-day delinquencies fell by 17K (-3.0%)

...

• Foreclosure starts decreased by 9% in the month to 29K, breaking a streak of increases, with starts remaining 19% below pre-pandemic levels

...

• Active foreclosure inventory rose marginally (+2K) in the month, and is up 34K (+15%) from February 2022 despite remaining 15% below its pre-pandemic level

• February saw 7.1K foreclosure sales (completions) nationally, up 2.5% from the month prior

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 3.45% in February, up from 3.38% the previous month.

The percent of loans in the foreclosure process increased slightly in February to 0.46%, from 0.45% the previous month.

The number of delinquent properties, but not in foreclosure, is down 235,000 properties year-over-year, and the number of properties in the foreclosure process is up 34,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| Feb 2023 | Jan 2023 | |||

| Delinquent | 3.45% | 3.38% | ||

| In Foreclosure | 0.46% | 0.45% | ||

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,811,000 | 1,775,000 | ||

| Number of properties in foreclosure pre-sale inventory: | 240,000 | 238,000 | ||

| Total Properties | 2,050,000 | 2,012,000 | ||

New Home Sales at 640,000 Annual Rate in February; New Home Average Prices Down 4.5% Year-over-year

by Calculated Risk on 3/23/2023 10:42:00 AM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales at 640,000 Annual Rate in February

Brief excerpt:

And on prices, from the Census Bureau:You can subscribe at https://calculatedrisk.substack.com/.The median sales price of new houses sold in February 2023 was $438,200. The average sales price was $498,700.The following graph shows the median and average new home prices. The average price in February 2023 was $498,700 down 4.5% year-over-year. The median price was $438,200 up 2.5% year-over-year. This suggests a year-over-year decrease in prices, although both the median and the average are impacted by the mix of homes sold.

...

This was for contracts signed in February when mortgage rates were lower - and builders were buying down rates. Mortgage rates increased again at the end of February, and that will likely impact sales in March.

As previously discussed, the Census Bureau overestimates sales, and underestimates inventory when cancellation rates are rising, see: New Home Sales and Cancellations: Net vs Gross Sales. This might be reversing now since cancellation rates have started to decline. When a previously cancelled home is resold, the home builder counts it as a sale, but the Census Bureau does not (since it was already counted).

There are a large number of homes under construction, and this suggests we will see a further increase in completed inventory over the next several months - and that will keep pressure on new home prices.

New Home Sales at 640,000 Annual Rate in February

by Calculated Risk on 3/23/2023 10:06:00 AM

The Census Bureau reports New Home Sales in February were at a seasonally adjusted annual rate (SAAR) of 640 thousand.

The previous three months were revised down.

Sales of new single‐family houses in February 2023 were at a seasonally adjusted annual rate of 640,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 1.1 percent above the revised January rate of 633,000, but is 19.0 percent below the February 2022 estimate of 790,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are close to pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply decreased in February to 8.2 months from 8.3 months in January.

The months of supply decreased in February to 8.2 months from 8.3 months in January. The all-time record high was 12.2 months of supply in January 2009. The all-time record low was 3.3 months in August 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of February was 436,000. This represents a supply of 8.2 months at the current sales rate."Sales were below expectations of 650 thousand SAAR, and sales in the three previous months were revised down. I'll have more later today.

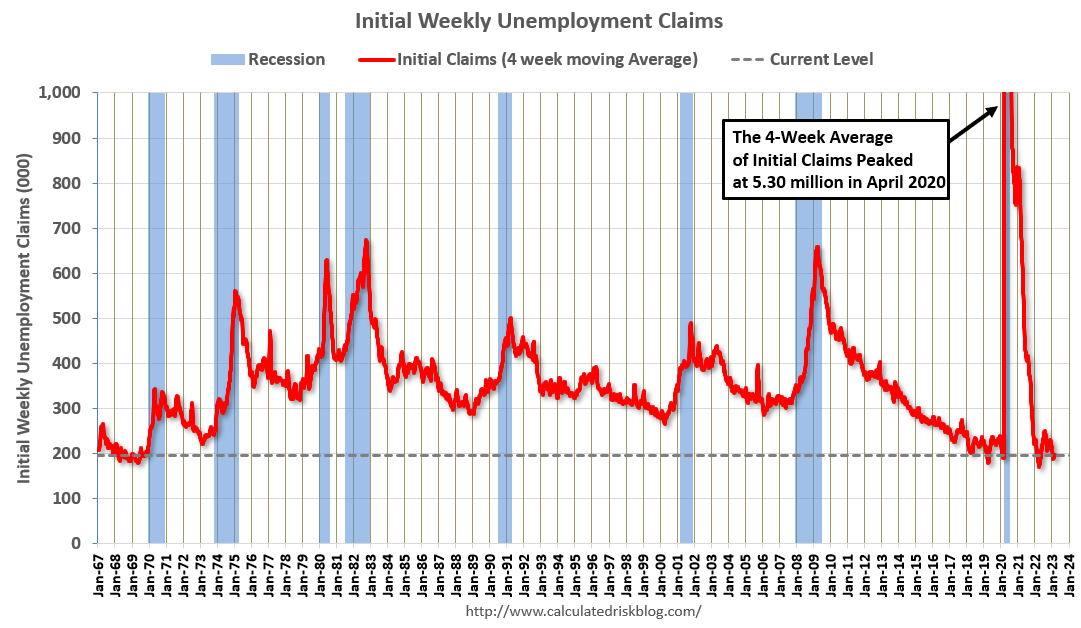

Weekly Initial Unemployment Claims decrease to 191,000

by Calculated Risk on 3/23/2023 08:33:00 AM

The DOL reported:

In the week ending March 18, the advance figure for seasonally adjusted initial claims was 191,000, a decrease of 1,000 from the previous week's unrevised level of 192,000. The 4-week moving average was 196,250, a decrease of 250 from the previous week's unrevised average of 196,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 196,250.

The previous week was unrevised.

Weekly claims were close to the consensus forecast.

Wednesday, March 22, 2023

Thursday: New Home Sales, Unemployment Claims

by Calculated Risk on 3/22/2023 09:05:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 190 thousand initial claims, down from 192 thousand last week.

• At 8:30 AM, Chicago Fed National Activity Index for February. This is a composite index of other data.

• At 10:00 AM, New Home Sales for February from the Census Bureau. The consensus is for 650 thousand SAAR, down from 670 thousand in January.

• At 11:00 AM, the Kansas City Fed manufacturing survey for March.

FOMC Projections and Press Conference

by Calculated Risk on 3/22/2023 02:09:00 PM

Statement here.

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

Here are the projections. In December, the FOMC participants’ midpoint of the target level for the federal funds rate was 5.125%. The FOMC participants’ midpoint of the target range is now somewhat above 5.125%.

Current Wall Street GDP tracking estimates show decent growth in Q1 (although there is a wide range of estimates). GDP projections for 2023 were revised down, contrary to recent data.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2023 | 2024 | 2025 | |

| Mar 2023 | 0.0 to 0.8 | 1.0 to 1.5 | 1.7 to 2.1 | |

| Dec 2022 | 0.4 to 1.0 | 1.3 to 2.0 | 1.6 to 2.0 | |

The unemployment rate was at 3.6% in February, just above the 50-year low. The FOMC revised down slightly their projected unemployment rate for Q4 2023.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2023 | 2024 | 2025 | |

| Mar 2023 | 4.0 to 4.7 | 4.3 to 4.9 | 4.3 to 4.8 | |

| Dec 2022 | 4.4 to 4.7 | 4.3 to 4.8 | 4.0 to 4.7 | |

As of January 2023, PCE inflation was up 5.4% year-over-year from January 2022, and, in general, inflation has been close to expectations. However, after accounting for the unusual dynamics related to the pandemic, inflation is likely lower than expected. The FOMC revised up their PCE inflation projections.

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2023 | 2024 | 2025 | |

| Mar 2023 | 3.0 to 3.8 | 2.2 to 2.8 | 2.0 to 2.2 | |

| Dec 2022 | 2.9 to 3.5 | 2.3 to 2.7 | 2.0 to 2.2 | |

PCE core inflation was up 4.7% in January year-over-year. The FOMC revised up their core PCE projections.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2023 | 2024 | 2025 | |

| Mar 2023 | 3.5 to 3.9 | 2.3 to 2.8 | 2.0 to 2.2 | |

| Dec 2022 | 3.2 to 3.7 | 2.3 to 2.7 | 2.0 to 2.2 | |

FOMC Statement: Raise Rates 25 bp; "some additional policy firming may be appropriate"

by Calculated Risk on 3/22/2023 02:02:00 PM

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

FOMC Statement:

Recent indicators point to modest growth in spending and production. Job gains have picked up in recent months and are running at a robust pace; the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 4-3/4 to 5 percent. The Committee will closely monitor incoming information and assess the implications for monetary policy. The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

emphasis added

AIA: Architecture Billings "Slowdown Continues" in February

by Calculated Risk on 3/22/2023 11:09:00 AM

Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment.

From the AIA: Architecture Billings Index (ABI) Slowdown Continues into February

More architecture firms reported a decline in billings in February, indicating an extension of a recent downturn in design activity according to a new report released today from The American Institute of Architects (AIA).

The combination of an unsettled economy and high interest rates is causing investors and property owners to take a closer look at their plans for construction projects,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “While this is producing delays for some projects under design, architecture firms are reporting that prospects for future project work remain generally positive.”

...

• Regional averages: West (50.4); Midwest (48.8); Northeast (48.4); South (47.3)

• Sector index breakdown: mixed practice (57.0); institutional (46.9); commercial/industrial (45.8); multi-family residential (46.2)

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Architecture Billings Index since 1996. The index was at 48.0 in February, down from 49.3 in January. Anything below 50 indicates contraction in demand for architects' services.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index had been positive for 20 consecutive months but indicated a decline the last five months. This index usually leads CRE investment by 9 to 12 months, so this index suggests a pickup in CRE investment in early 2023, but a slowdown in CRE investment later in 2023.

Note that multi-family billing turned down in August 2022 and has been negative for seven consecutive months. This suggests we will see a downturn in multi-family starts this year.

MBA: Mortgage Purchase Applications Increased in Weekly Survey

by Calculated Risk on 3/22/2023 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

— Mortgage applications increased 3.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 17, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The Refinance Index increased 5 percent from the previous week and was 68 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 3 percent compared with the previous week and was 36 percent lower than the same week one year ago.

"Treasury yields declined last week, driven by uncertainty over the health of the banking sector and worries about the broader impact on the economy. Mortgage rates declined for the second week in a row, with the 30-year fixed rate dropping to 6.48 percent, the lowest level in a month,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “However, mortgage rates have not dropped as much as Treasury rates due to increased MBS market volatility. The spread between the 30-year fixed and 10-year Treasury remained wide at around 300 basis points, compared to a more typical spread of 180 basis points.”

Added Kan, “Both purchase and refinance applications increased for the third week in a row as borrowers took the opportunity to act, even though overall application volume remains at relatively low levels.”

..

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 6.48 percent from 6.71 percent, with points decreasing to 0.66 from 0.79 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index declined sharply in 2022.

The second graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is down 36% year-over-year unadjusted.

According to the MBA, purchase activity is down 36% year-over-year unadjusted. Red is a four-week average (blue is weekly).