RSS Feed

RSS Feed by Calculated Risk on 7/21/2021 07:00:00 AM

Wednesday, July 21, 2021

MBA: Mortgage Applications Decrease in Latest Weekly Survey

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 4.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 16, 2021. The previous week’s results included an adjustment for the Fourth of July holiday.

... The Refinance Index decreased 3 percent from the previous week and was 18 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 18 percent lower than the same week one year ago.

“The 10-year Treasury yield dropped sharply last week, in part due to investors becoming more concerned about the spread of COVID variants and their impact on global economic growth. There were mixed changes in mortgage rates as a result, with the 30-year fixed rate increasing slightly to 3.11 percent after two weeks of declines. Other surveyed rates moved lower, with the 15-year fixed rate loan, used by around 20 percent of refinance borrowers, decreasing to 2.46 percent – the lowest level since January 2021,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting.

“On a seasonally adjusted basis compared to the July 4th holiday week, mortgage applications were lower across the board, with purchase applications back to near their lowest levels since May 2020. Limited inventory and higher prices are keeping some prospective homebuyers out of the market. Refinance activity fell over the week, but because rates have stayed relatively low, the pace of applications was close to its highest level since early May 2021.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($548,250 or less) increased to 3.11 percent from 3.09 percent, with points increasing to 0.43 from 0.37 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With low rates, the index remains elevated, and will likely increase this coming week as rates declined.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 18% year-over-year unadjusted.

According to the MBA, purchase activity is down 18% year-over-year unadjusted.Note: The year ago comparisons for the unadjusted purchase index are now difficult since purchase activity picked up in late May 2020.

Note: Red is a four-week average (blue is weekly).

Tuesday, July 20, 2021

July 20th COVID-19, New Cases, Hospitalizations, Vaccinations

by Calculated Risk on 7/20/2021 08:04:00 PM

The 7-day average cases is the highest since May 11th.

The 7-day average hospitalizations is the highest since June 1st.

This data is from the CDC.

According to the CDC, on Vaccinations.

Total doses administered: 338,491,374, as of a week ago 334,942,236. Average doses last week: 0.51 million per day.

KUDOS to the residents of the 20 states and D.C. that have achieved the 70% goal (percent over 18 with at least one dose): Vermont, Hawaii, Massachusetts and Connecticut are at 80%+, and Maine, New Mexico, New Jersey, Rhode Island, Pennsylvania, California, Maryland, Washington, New Hampshire, New York, Illinois, Virginia, Delaware, Minnesota, Oregon, Colorado and D.C. are all over 70%.

According to the CDC, on Vaccinations.

Total doses administered: 338,491,374, as of a week ago 334,942,236. Average doses last week: 0.51 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent over 18, One Dose | 68.3% | 68.3% | 67.7% | ≥70.0%1,2 |

| Fully Vaccinated✅ (millions) | 161.6 | 161.5 | 159.7 | ≥1601 |

| New Cases per Day3🚩 | 35,547 | 33,541 | 22,222 | ≤5,0002 |

| Hospitalized3🚩 | 19,251 | 18,460 | 14,308 | ≤3,0002 |

| Deaths per Day3🚩 | 245 | 240 | 171 | ≤502 |

| 1 America's Short Term Goals, 2my goals to stop daily posts, 37 day average for Cases, Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met (even if late). | ||||

KUDOS to the residents of the 20 states and D.C. that have achieved the 70% goal (percent over 18 with at least one dose): Vermont, Hawaii, Massachusetts and Connecticut are at 80%+, and Maine, New Mexico, New Jersey, Rhode Island, Pennsylvania, California, Maryland, Washington, New Hampshire, New York, Illinois, Virginia, Delaware, Minnesota, Oregon, Colorado and D.C. are all over 70%.

Next up are Florida at 66.7%, Utah at 66.7%, Wisconsin at 66.4%, Nebraska at 66.3%, South Dakota at 65.2%, and Iowa at 64.8%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

This data is from the CDC.

Indiana Real Estate in June: Sales Up 9% YoY, Inventory Down 36% YoY

by Calculated Risk on 7/20/2021 03:03:00 PM

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

For for the entire state Indiana:

Closed sales in June 2021 were 9,969, up 9.2% from 9,127 in June 2020.

Active Listings in June 2021 were 7,743, down 36.2% from 12,139 in June 2020.

Months of Supply was 0.9 Months in June 2021, compared to 1.6 Months in June 2020.

Inventory in June was up 18.1% from last month, and up 31.3% from 5,898 in March 2021.

Existing Home Sales: Lawler vs. the Consensus

by Calculated Risk on 7/20/2021 12:15:00 PM

Housing economist Tom Lawler has been sending me his predictions of what the NAR will report for over 11 years. And he has graciously allowed me to share his predictions with the readers of this blog.

The table below shows the consensus for each month, Lawler's predictions, and the NAR's initially reported level of sales.

Lawler hasn't always been closer than the consensus, but usually when there has been a fairly large spread between Lawler's estimate and the "consensus", Lawler has been closer.

For example, last month Lawler estimated the NAR would report sales of 5.78 million SAAR, the consensus was 5.74 million SAAR, and the NAR reported 5.80 million SAAR.

The NAR is scheduled to release Existing Home Sales for June at 10:00 AM, Thursday, July 22nd.

The consensus is for 5.90 million SAAR in June, up from 5.80 million in May. Tom Lawler estimates the NAR will report sales of 5.79 million SAAR. Based on Lawler's estimate, I expect existing home sales to be slightly below the consensus in June.

NOTE: There have been times when Lawler "missed", but then he pointed out an apparent error in the NAR data - and the subsequent revision corrected that error. As an example, see: The “Curious Case” of Existing Home Sales in the South in April

Over the last 11+ years, the consensus average miss was 147 thousand, and Lawler's average miss was 73 thousand.

The NAR is scheduled to release Existing Home Sales for June at 10:00 AM, Thursday, July 22nd.

The consensus is for 5.90 million SAAR in June, up from 5.80 million in May. Tom Lawler estimates the NAR will report sales of 5.79 million SAAR. Based on Lawler's estimate, I expect existing home sales to be slightly below the consensus in June.

NOTE: There have been times when Lawler "missed", but then he pointed out an apparent error in the NAR data - and the subsequent revision corrected that error. As an example, see: The “Curious Case” of Existing Home Sales in the South in April

Over the last 11+ years, the consensus average miss was 147 thousand, and Lawler's average miss was 73 thousand.

| Existing Home Sales, Forecasts and NAR Report millions, seasonally adjusted annual rate basis (SAAR) | |||

|---|---|---|---|

| Month | Consensus | Lawler | NAR reported1 |

| May-10 | 6.20 | 5.83 | 5.66 |

| Jun-10 | 5.30 | 5.30 | 5.37 |

| Jul-10 | 4.66 | 3.95 | 3.83 |

| Aug-10 | 4.10 | 4.10 | 4.13 |

| Sep-10 | 4.30 | 4.50 | 4.53 |

| Oct-10 | 4.50 | 4.46 | 4.43 |

| Nov-10 | 4.85 | 4.61 | 4.68 |

| Dec-10 | 4.90 | 5.13 | 5.28 |

| Jan-11 | 5.20 | 5.17 | 5.36 |

| Feb-11 | 5.15 | 5.00 | 4.88 |

| Mar-11 | 5.00 | 5.08 | 5.10 |

| Apr-11 | 5.20 | 5.15 | 5.05 |

| May-11 | 4.75 | 4.80 | 4.81 |

| Jun-11 | 4.90 | 4.71 | 4.77 |

| Jul-11 | 4.92 | 4.69 | 4.67 |

| Aug-11 | 4.75 | 4.92 | 5.03 |

| Sep-11 | 4.93 | 4.83 | 4.91 |

| Oct-11 | 4.80 | 4.86 | 4.97 |

| Nov-11 | 5.08 | 4.40 | 4.42 |

| Dec-11 | 4.60 | 4.64 | 4.61 |

| Jan-12 | 4.69 | 4.66 | 4.57 |

| Feb-12 | 4.61 | 4.63 | 4.59 |

| Mar-12 | 4.62 | 4.59 | 4.48 |

| Apr-12 | 4.66 | 4.53 | 4.62 |

| May-12 | 4.57 | 4.66 | 4.55 |

| Jun-12 | 4.65 | 4.56 | 4.37 |

| Jul-12 | 4.50 | 4.47 | 4.47 |

| Aug-12 | 4.55 | 4.87 | 4.82 |

| Sep-12 | 4.75 | 4.70 | 4.75 |

| Oct-12 | 4.74 | 4.84 | 4.79 |

| Nov-12 | 4.90 | 5.10 | 5.04 |

| Dec-12 | 5.10 | 4.97 | 4.94 |

| Jan-13 | 4.90 | 4.94 | 4.92 |

| Feb-13 | 5.01 | 4.87 | 4.98 |

| Mar-13 | 5.03 | 4.89 | 4.92 |

| Apr-13 | 4.92 | 5.03 | 4.97 |

| May-13 | 5.00 | 5.20 | 5.18 |

| Jun-13 | 5.27 | 4.99 | 5.08 |

| Jul-13 | 5.13 | 5.33 | 5.39 |

| Aug-13 | 5.25 | 5.35 | 5.48 |

| Sep-13 | 5.30 | 5.26 | 5.29 |

| Oct-13 | 5.13 | 5.08 | 5.12 |

| Nov-13 | 5.02 | 4.98 | 4.90 |

| Dec-13 | 4.90 | 4.96 | 4.87 |

| Jan-14 | 4.70 | 4.67 | 4.62 |

| Feb-14 | 4.64 | 4.60 | 4.60 |

| Mar-14 | 4.56 | 4.64 | 4.59 |

| Apr-14 | 4.67 | 4.70 | 4.65 |

| May-14 | 4.75 | 4.81 | 4.89 |

| Jun-14 | 4.99 | 4.96 | 5.04 |

| Jul-14 | 5.00 | 5.09 | 5.15 |

| Aug-14 | 5.18 | 5.12 | 5.05 |

| Sep-14 | 5.09 | 5.14 | 5.17 |

| Oct-14 | 5.15 | 5.28 | 5.26 |

| Nov-14 | 5.20 | 4.90 | 4.93 |

| Dec-14 | 5.05 | 5.15 | 5.04 |

| Jan-15 | 5.00 | 4.90 | 4.82 |

| Feb-15 | 4.94 | 4.87 | 4.88 |

| Mar-15 | 5.04 | 5.18 | 5.19 |

| Apr-15 | 5.22 | 5.20 | 5.04 |

| May-15 | 5.25 | 5.29 | 5.35 |

| Jun-15 | 5.40 | 5.45 | 5.49 |

| Jul-15 | 5.41 | 5.64 | 5.59 |

| Aug-15 | 5.50 | 5.54 | 5.31 |

| Sep-15 | 5.35 | 5.56 | 5.55 |

| Oct-15 | 5.41 | 5.33 | 5.36 |

| Nov-15 | 5.32 | 4.97 | 4.76 |

| Dec-15 | 5.19 | 5.36 | 5.46 |

| Jan-16 | 5.32 | 5.36 | 5.47 |

| Feb-16 | 5.30 | 5.20 | 5.08 |

| Mar-16 | 5.27 | 5.27 | 5.33 |

| Apr-16 | 5.40 | 5.44 | 5.45 |

| May-16 | 5.64 | 5.55 | 5.53 |

| Jun-16 | 5.48 | 5.62 | 5.57 |

| Jul-16 | 5.52 | 5.41 | 5.39 |

| Aug-16 | 5.44 | 5.49 | 5.33 |

| Sep-16 | 5.35 | 5.55 | 5.47 |

| Oct-16 | 5.44 | 5.47 | 5.60 |

| Nov-16 | 5.54 | 5.60 | 5.61 |

| Dec-16 | 5.54 | 5.55 | 5.49 |

| Jan-17 | 5.55 | 5.60 | 5.69 |

| Feb-17 | 5.55 | 5.41 | 5.48 |

| Mar-17 | 5.61 | 5.74 | 5.71 |

| Apr-17 | 5.67 | 5.56 | 5.57 |

| May-17 | 5.55 | 5.65 | 5.62 |

| Jun-17 | 5.58 | 5.59 | 5.52 |

| Jul-17 | 5.57 | 5.38 | 5.44 |

| Aug-17 | 5.48 | 5.39 | 5.35 |

| Sep-17 | 5.30 | 5.38 | 5.39 |

| Oct-17 | 5.30 | 5.60 | 5.48 |

| Nov-17 | 5.52 | 5.77 | 5.81 |

| Dec-17 | 5.75 | 5.66 | 5.57 |

| Jan-18 | 5.65 | 5.48 | 5.38 |

| Feb-18 | 5.42 | 5.44 | 5.54 |

| Mar-18 | 5.28 | 5.51 | 5.60 |

| Apr-18 | 5.60 | 5.48 | 5.46 |

| May-18 | 5.56 | 5.47 | 5.43 |

| Jun-18 | 5.45 | 5.35 | 5.38 |

| Jul-18 | 5.43 | 5.40 | 5.34 |

| Aug-18 | 5.36 | 5.36 | 5.34 |

| Sep-18 | 5.30 | 5.20 | 5.15 |

| Oct-18 | 5.20 | 5.31 | 5.22 |

| Nov-18 | 5.19 | 5.23 | 5.32 |

| Dec-18 | 5.24 | 4.97 | 4.99 |

| Jan-19 | 5.05 | 4.92 | 4.94 |

| Feb-19 | 5.08 | 5.46 | 5.51 |

| Mar-19 | 5.30 | 5.40 | 5.21 |

| Apr-19 | 5.36 | 5.31 | 5.19 |

| May-19 | 5.29 | 5.40 | 5.34 |

| Jun-19 | 5.34 | 5.25 | 5.27 |

| Jul-19 | 5.39 | 5.40 | 5.42 |

| Aug-19 | 5.38 | 5.42 | 5.49 |

| Sep-19 | 5.45 | 5.36 | 5.38 |

| Oct-19 | 5.49 | 5.36 | 5.46 |

| Nov-19 | 5.45 | 5.43 | 5.35 |

| Dec-19 | 5.43 | 5.40 | 5.54 |

| Jan-20 | 5.45 | 5.42 | 5.46 |

| Feb-20 | 5.50 | 5.58 | 5.77 |

| Mar-20 | 5.30 | 5.25 | 5.27 |

| Apr-20 | 4.30 | 4.17 | 4.33 |

| May-20 | 4.38 | 3.80 | 3.91 |

| Jun-20 | 4.86 | 4.65 | 4.72 |

| Jul-20 | 5.39 | 5.85 | 5.86 |

| Aug-20 | 6.00 | 5.92 | 6.00 |

| Sep-20 | 6.25 | 6.38 | 6.54 |

| Oct-20 | 6.45 | 6.63 | 6.85 |

| Nov-20 | 6.70 | 6.50 | 6.69 |

| Dec-20 | 6.55 | 6.62 | 6.76 |

| Jan-21 | 6.60 | 6.48 | 6.69 |

| Feb-21 | 6.51 | 6.29 | 6.22 |

| Mar-21 | 6.17 | 6.02 | 6.01 |

| Apr-21 | 6.09 | 5.96 | 5.85 |

| May-21 | 5.74 | 5.78 | 5.80 |

| Jun-21 | 5.90 | 5.79 | NA |

| 1NAR initially reported before revisions. | |||

Comments on June Housing Starts

by Calculated Risk on 7/20/2021 10:20:00 AM

Earlier: Housing Starts increased to 1.643 Million Annual Rate in June

Total housing starts in June were above expectations, however starts in April and May were revised down.

Single family starts increased in June, and were up 28% year-over-year. Starts declined at the beginning of the pandemic, and then increased due to strong demand.

The volatile multi-family sector is up 31% year-over-year.

The housing starts report showed total starts were up 6.3% in June compared to the previous month, and total starts were up 29.1% year-over-year compared to June 2020.

The housing starts report showed total starts were up 6.3% in June compared to the previous month, and total starts were up 29.1% year-over-year compared to June 2020.

Low mortgage rates, limited existing home inventory, and favorable demographics have given a boost to single family housing starts.

The first graph shows the month to month comparison for total starts between 2020 (blue) and 2021 (red).

Click on graph for larger image.

Click on graph for larger image.

Starts were up 29.1% in June compared to June 2020. The year-over-year comparison will be more difficult starting in July.

In 2020, starts were off to a strong start before the pandemic, and with low interest rates, and little competing existing home inventory, starts finished 2020 strong.

The first graph shows the month to month comparison for total starts between 2020 (blue) and 2021 (red).

Click on graph for larger image.

Click on graph for larger image.Starts were up 29.1% in June compared to June 2020. The year-over-year comparison will be more difficult starting in July.

In 2020, starts were off to a strong start before the pandemic, and with low interest rates, and little competing existing home inventory, starts finished 2020 strong.

Starts were solid in the first half of 2021.

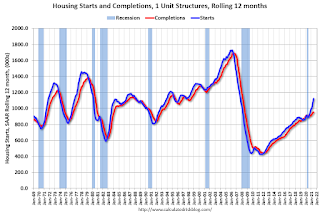

Below is an update to the graph comparing multi-family starts and completions. Since it usually takes over a year on average to complete a multi-family project, there is a lag between multi-family starts and completions. Completions are important because that is new supply added to the market, and starts are important because that is future new supply (units under construction is also important for employment).

These graphs use a 12 month rolling total for NSA starts and completions.

The blue line is for multifamily starts and the red line is for multifamily completions.

The blue line is for multifamily starts and the red line is for multifamily completions.

The rolling 12 month total for starts (blue line) increased steadily for several years following the great recession - then mostly moved sideways.

These graphs use a 12 month rolling total for NSA starts and completions.

The blue line is for multifamily starts and the red line is for multifamily completions.

The blue line is for multifamily starts and the red line is for multifamily completions. The rolling 12 month total for starts (blue line) increased steadily for several years following the great recession - then mostly moved sideways.

Completions (red line) had lagged behind starts, but have caught up again.

The last graph shows single family starts and completions. It usually only takes about 6 months between starting a single family home and completion - so the lines are much closer. The blue line is for single family starts and the red line is for single family completions.

The last graph shows single family starts and completions. It usually only takes about 6 months between starting a single family home and completion - so the lines are much closer. The blue line is for single family starts and the red line is for single family completions.

Single family starts are getting back to more normal levels, but I still expect some further increases in single family starts and completions on a rolling 12 month basis - especially given the low level of existing home inventory.

The last graph shows single family starts and completions. It usually only takes about 6 months between starting a single family home and completion - so the lines are much closer. The blue line is for single family starts and the red line is for single family completions.

The last graph shows single family starts and completions. It usually only takes about 6 months between starting a single family home and completion - so the lines are much closer. The blue line is for single family starts and the red line is for single family completions.Single family starts are getting back to more normal levels, but I still expect some further increases in single family starts and completions on a rolling 12 month basis - especially given the low level of existing home inventory.

Housing Starts increased to 1.643 Million Annual Rate in June

by Calculated Risk on 7/20/2021 08:37:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately‐owned housing starts in June were at a seasonally adjusted annual rate of 1,643,000. This is 6.3 percent above the revised May estimate of 1,546,000 and is 29.1 percent above the June 2020 rate of 1,273,000. Single‐family housing starts in June were at a rate of 1,160,000; this is 6.3 percent above the revised May figure of 1,091,000. The June rate for units in buildings with five units or more was 474,000.

Building Permits:

Privately‐owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 1,598,000. This is 5.1 percent below the revised May rate of 1,683,000, but is 23.3 percent above the June 2020 rate of 1,296,000. Single‐family authorizations in June were at a rate of 1,063,000; this is 6.3 percent below the revised May figure of 1,134,000. Authorizations of units in buildings with five units or more were at a rate of 483,000 in June.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows single and multi-family housing starts for the last several years.

Multi-family starts (red, 2+ units) increased in June compared to May. Multi-family starts were up 31% year-over-year in June.

Single-family starts (blue) increased in June, and were up 28% year-over-year (starts slumped at the beginning of the pandemic).

The second graph shows total and single unit starts since 1968.

The second graph shows total and single unit starts since 1968. The second graph shows the huge collapse following the housing bubble, and then the eventual recovery (but still not historically high).

Total housing starts in June were above expectations, however starts in April and May were revised down.

I'll have more later …

Monday, July 19, 2021

Tuesday: Housing Starts

by Calculated Risk on 7/19/2021 09:00:00 PM

From Matthew Graham at Mortgage News Daily: MBS RECAP: Big Bond Rally Just Got Bigger

U.S. traders fired up the screens this morning to see a substantial bond rally and stock sell-off that happened almost exclusively during European hours. Rather than push back against the move, the domestic session took things a step farther. ... the core is the fact that covid case counts are rising at their fastest pace since January. The pace of the stock sell-off added an additional source of motivation for bonds. [30 year fixed 2.89%]Tuesday:

emphasis added

• At 8:30 AM ET, Housing Starts for June. The consensus is for 1.592 million SAAR, up from 1.572 million SAAR in May.

Phoenix Real Estate in June: Sales Up 2% YoY, Active Inventory Down 33% YoY

by Calculated Risk on 7/19/2021 06:18:00 PM

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

The Arizona Regional Multiple Listing Service (ARMLS) reports ("Stats Report"):

1) Overall sales were at 9,661 in June, up 1.6% from 9,508 in June 2020.

2) Active inventory was at 5,866, down 33.3% from 8,792 in June 2020.

3) Months of supply decreased to 1.05 in June from 1.51 in June 2020. This is very low.

Inventory in June was up 12.4% from last month, and up 42% from the record low in February 2021.

MBA Survey: "Share of Mortgage Loans in Forbearance Decreases to 3.50%"

by Calculated Risk on 7/19/2021 04:00:00 PM

Note: This is as of July 11th.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 3.50%

The Mortgage Bankers Association’s (MBA) latest Forbearance and Call Volume Survey revealed that the total number of loans now in forbearance decreased by 26 basis points from 3.76% of servicers’ portfolio volume in the prior week to 3.50% as of July 11, 2021. According to MBA’s estimate, 1.75 million homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 8 basis points to 1.83%. Ginnie Mae loans in forbearance decreased 42 basis points to 4.36%, while the forbearance share for portfolio loans and private-label securities (PLS) decreased 61 basis points to 7.33%. The percentage of loans in forbearance for independent mortgage bank (IMB) servicers decreased 19 basis points to 3.68%, and the percentage of loans in forbearance for depository servicers decreased 36 basis points to 3.62%.

“Forbearance exits edged up again last week and new forbearance requests dropped to their lowest level since last March, leading to the largest weekly drop in the forbearance share since last October and the 20th consecutive week of declines,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “The forbearance share decreased for every investor and servicer category.”

Added Fratantoni, “The latest economic data regarding the job market and consumer spending continue to show a robust pace of economic recovery, which is supporting further improvements in the forbearance numbers as more homeowners are able to resume their payments.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time. Most of the increase was in late March and early April 2020, and has trended down since then.

The MBA notes: "Total weekly forbearance requests as a percent of servicing portfolio volume (#) decreased relative to the prior week: from 0.04% to 0.03% – the lowest level reported since the week ending March 15, 2020."

July 19th COVID-19, New Cases, Hospitalizations, Vaccinations

by Calculated Risk on 7/19/2021 03:55:00 PM

Note: Cases and deaths reported on Monday are always low - and almost always revised up significantly when additional data is received.

This data is from the CDC.

According to the CDC, on Vaccinations.

Total doses administered: 338,247,434, as of a week ago 334,600,770. Average doses last week: 0.52 million per day.

KUDOS to the residents of the 20 states and D.C. that have already achieved the 70% goal (percent over 18 with at least one dose): Vermont, Hawaii, Massachusetts and Connecticut are at 80%+, and Maine, New Mexico, New Jersey, Rhode Island, Pennsylvania, California, Maryland, Washington, New Hampshire, New York, Illinois, Virginia, Delaware, Minnesota, Oregon, Colorado and D.C. are all over 70%.

According to the CDC, on Vaccinations.

Total doses administered: 338,247,434, as of a week ago 334,600,770. Average doses last week: 0.52 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent over 18, One Dose | 68.3% | 68.2% | 67.7% | ≥70.0%1,2 |

| Fully Vaccinated✅ (millions) | 161.5 | 161.2 | 159.5 | ≥1601 |

| New Cases per Day3🚩 | 26,011 | 27,776 | 20,849 | ≤5,0002 |

| Hospitalized3🚩 | 16,974 | 17,168 | 12,831 | ≤3,0002 |

| Deaths per Day3🚩 | 218 | 226 | 159 | ≤502 |

| 1 America's Short Term Goals, 2my goals to stop daily posts, 37 day average for Cases, Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met (even if late). | ||||

KUDOS to the residents of the 20 states and D.C. that have already achieved the 70% goal (percent over 18 with at least one dose): Vermont, Hawaii, Massachusetts and Connecticut are at 80%+, and Maine, New Mexico, New Jersey, Rhode Island, Pennsylvania, California, Maryland, Washington, New Hampshire, New York, Illinois, Virginia, Delaware, Minnesota, Oregon, Colorado and D.C. are all over 70%.

Next up are Florida at 66.6%, Utah at 66.5%, Wisconsin at 66.4%, Nebraska at 66.3%, South Dakota at 65.1%, and Iowa at 64.7%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

This data is from the CDC.