RSS Feed

RSS Feed by Calculated Risk on 6/25/2009 02:07:00 PM

Thursday, June 25, 2009

Hotel RevPAR off 20.5 Percent

From HotelNewsNow.com: STR posts US results for 14-20 June 2009

In year-over-year measurements, the industry’s occupancy fell 11.5 percent to end the week at 63.0 percent. Average daily rate dropped 10.1 percent to finish the week at US$96.78. Revenue per available room [RevPAR] for the week decreased 20.5 percent to finish at US$61.01.The report also includes some hightlights on the performance for the top 25 markets. As an example, occupancy is off almost 20% in Dallas and Phoenix, and the Average daily rate (ADR) is off 30% and RevPAR off 35% in New York. Ouch.

No wonder more and more hotels are defaulting ...

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the YoY change in the occupancy rate (3 week trailing average).

The three week average is off 12.1% from the same period in 2008.

The average daily rate is down 10.1%, so RevPAR is off 20.5% from the same week last year.

Note: some readers might notice the occupancy rate has risen to 63% - but that is just seasonal. The hotel occupancy rate is usually the highest during the peak vacation months of June, July and August.

Fed Extends Some Emergency Lending Facilities, Trims Others

by Calculated Risk on 6/25/2009 12:52:00 PM

The Federal Reserve on Thursday announced extensions of and modifications to a number of its liquidity programs. Conditions in financial markets have improved in recent months, but market functioning in many areas remains impaired and seems likely to be strained for some time. As a consequence, to promote financial stability and support the flow of credit to households and businesses, the Federal Reserve is extending a number of facilities through early 2010. At the same time, in light of the improvement in financial conditions and reduced usage of some facilities, the Federal Reserve is trimming the size and changing the terms of some facilities.The TSLF lent Treasury securities to primary dealers, secured by certain other securities, for a term of 28 days rather than the usual overnight. Suspending that program seems like a minor change, but it does show the panic has subsided.

Specifically, the Board of Governors approved extension through February 1, 2010, of the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF), the Commercial Paper Funding Facility (CPFF), the Primary Dealer Credit Facility (PDCF), and the Term Securities Lending Facility (TSLF). The expiration date for the Term Asset-Backed Securities Loan Facility (TALF) currently remains set at December 31, 2009. The Term Auction Facility (TAF) does not have a fixed expiration date.

The extension of the TSLF also required the approval of the Federal Open Market Committee (FOMC), as that facility is established under the joint authority of the Board and the FOMC.

In addition, the temporary reciprocal currency arrangements (swap lines) between the Federal Reserve and other central banks have been extended to February 1. The Federal Reserve action to extend the swap lines was taken by the FOMC.

The Federal Reserve also announced changes to certain liquidity programs in light of the improvement in financial conditions and the associated reduction in usage of some facilities. Specifically, the Federal Reserve trimmed the size of upcoming TAF auctions, because the amount of credit extended under that facility has been well below the offered amount. In view of very weak demand at TSLF Schedule 1 auctions and TSLF Options Program auctions over recent months, auctions under these programs will be suspended. The frequency of Schedule 2 TSLF auctions will be reduced to one every four weeks and the offered amount will be reduced. The authorization for the Money Market Investor Funding Facility (MMIFF) was not extended, and an additional administrative criterion was established for use of the AMLF. If necessary in view of evolving market conditions, the Federal Reserve will increase the size of TAF auctions and resume TSLF operations that have been suspended.

WSJ Real Time Economics: Housing Bubble and Consumer Spending

by Calculated Risk on 6/25/2009 11:00:00 AM

Earlier this week, Charles W. Calomiris, Stanley D. Longhofer and William Miles wrote in Real Time Economics that the wealth effect from housing on consumption should be small. Atif Mian and Amir Sufi of the University of Chicago Booth School of Business respond that their data indicate the opposite.I commented on the Calomiris et. al. piece here: The Housing Wealth Effect? and I noted that Mian and Sufi disagreed.

Here are excerpts from Atif Mian and Amir Sufi's piece today:

... In the June 22nd entry for Real Time Economics, Calomiris, Longhofer, and Miles argue that ... “the reaction of consumption to housing wealth changes is probably very small.”

Findings in our research suggest the exact opposite: the rise in house prices from 2002 to 2006 was a main driver of economic growth during this time period, and the subsequent collapse of house prices is likely a main contributor to the historic consumption decline over the past year.

We agree with two key points made by Calomiris, Longhofer, and Miles. First, from the perspective of economic theory, it is not obvious that housing wealth should affect consumption. Second, it is difficult to measure the causal effect of housing wealth on consumption because other economic factors confound the relation. ...

These factors highlight the importance of quality data and sound methodology to estimate the effect of house prices on real economic activity. Our study samples 70,000 consumers in 1998 who were already homeowners at the time. We then follow the borrowing decisions of these households for eleven years until the end of 2008. Our data set represents a major advantage over prior studies; it allows us to see exactly how existing homeowners respond to increases in house prices.

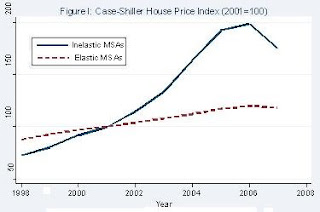

In order to isolate the effect of house prices on consumption, we rely on a simple insight: in response to an equivalent increase in local housing demand, house prices will increase more in cities where, due to geography based factors, the cost of building a house is high. For example, consider a homeowner living in San Francisco and a homeowner living in Atlanta as of 1998. From 2002 to 2006, house prices rose sharply in San Francisco where it is difficult to build additional houses because of the limited geography. In contrast, in Atlanta, where home construction is cheaper, house price growth was moderate. In economics jargon, cities where housing supply is relatively “inelastic” will experience larger movement in house prices relative to “elastic” cities (see Figure I).

Our experimental design exploits this insight in order to test how house prices affect borrowing behavior. The “treatment” group consists of homeowners in inelastic housing supply cities (e.g., San Francisco) that experienced a sharp increase and subsequent collapse of house prices. The “control” group consists of homeowners in elastic housing supply cities (e.g., Atlanta) that experienced little change in house prices.

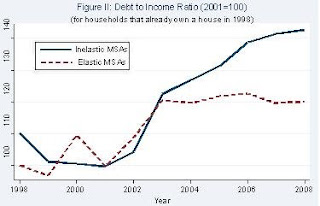

Using this methodology, we find striking results: from 2002 to 2006, homeowners borrowed $0.25 to $0.30 for every $1 increase in their home equity. Our microeconomic estimates suggest a large macroeconomic impact: withdrawals of home equity by households accounted for 2.3% of GDP each year from 2002 to 2006. Figure II illustrates the sharp increase in household leverage for homeowners living in inelastic cities.

A concern with our interpretation is that there are inherently different economic conditions in inelastic versus elastic housing supply cities that may have been responsible for the borrowing patterns we observe. However, several facts suggest that this is not a valid concern. First, inelastic cities do not experience a stronger income growth shock (i.e., a larger shock to their “permanent income”) during the housing boom. Second, the increase in debt among homeowners in high house price growth areas is concentrated in mortgage and home equity related debt.The results of Atif Mian and Amir Sufi fit with what I've observed.

Third, renters in inelastic areas did not experience a larger growth in their total debt. Finally, the effect of house prices on homeowner borrowing is isolated to homeowners with low credit scores and high credit card utilization rates. These “credit-constrained” households respond aggressively to house price growth, whereas the highest credit quality borrowers do not respond at all.

Our results demonstrate that homeowners in high house price areas borrowed heavily against the rise in home equity from 2002 to 2006. We also provide evidence that real outlays were a likely use of borrowed funds. Money withdrawn from home equity was not used to buy new homes, buy investment properties, or invest in financial assets. In fact, homeowners did not even use home equity withdrawals to pay down expensive credit card debt! These facts suggest that consumption and home improvement were the most likely use of borrowed funds, which is consistent with Federal Reserve survey evidence suggesting home equity extraction is used for real outlays.

...

Our analysis of the microeconomic data has led us to the conclusion that the severity of this economic downturn is rooted in the household leverage crisis, which in turn is closely related to the housing market. If the housing market continues to deteriorate, then further de-leveraging of the household sector will likely keep a lid on any rebound in consumption. In other words, the future of consumption and house prices are closely linked.

Bernanke to Testify on BofA and Merrill Lynch at 10 AM ET

by Calculated Risk on 6/25/2009 09:42:00 AM

Fed Chairman Ben Bernanke is to provide testimony before the House Committee on Oversight and Government Reform regarding the Bank of America's acquisition of Merrill Lynch. Might be interesting ...

UPDATE: Here is Bernanke's prepared testimony.

I appreciate the opportunity to discuss the Federal Reserve's role in the acquisition by the Bank of America Corporation of Merrill Lynch & Co., Inc. I believe that the Federal Reserve acted with the highest integrity throughout its discussions with Bank of America regarding that company's acquisition of Merrill Lynch. I will attempt in this testimony to respond to some of the questions that have been raised.Here is the CNBC feed.

And a live feed from C-SPAN.

Initial Unemployment Claims Increase

by Calculated Risk on 6/25/2009 08:30:00 AM

The DOL reports on weekly unemployment insurance claims:

In the week ending June 20, the advance figure for seasonally adjusted initial claims was 627,000, an increase of 15,000 from the previous week's revised figure of 612,000. The 4-week moving average was 617,250, an increase of 500 from the previous week's revised average of 616,750.

...

The advance number for seasonally adjusted insured unemployment during the week ending June 13 was 6,738,000, an increase of 29,000 from the preceding week's revised level of 6,709,000. The 4-week moving average was 6,759,750, a decrease of 3,250 from the preceding week's revised average of 6,763,000.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows weekly claims and continued claims since 1971.

Continued claims decreased to 6.74 million. This is 5.0% of covered employment.

Note: continued claims peaked at 5.4% of covered employment in 1982 and 7.0% in 1975.

The four-week average of weekly unemployment claims increased this week by 500, and is now 41,500 below the peak of 10 weeks ago. There is a reasonable chance that claims have peaked for this cycle.

However the level of initial claims (over 627 thousand) is still very high, indicating significant weakness in the job market.

There was plenty of discussion about the decline in continuing claims last week. A few comments:

If we look back 26 weeks from last week, there was a huge jump in NSA initial claims (from 536 thousand to 760 thousand) or 224 thousand in one week back in December. Any of those people who are still unemployed (and many probably are) were moving off the standard unemployment benefits to extended benefits and are no longer counted in the continued claims. That probably counts for most of the decline last week. But it is also important to remember they are still receiving unemployment benefits (extended benefits).

When looking at this report, I'd focus on the 4-week moving average of initial claims, not continued claims.

Wednesday, June 24, 2009

CRE and Residential RE Prices

by Calculated Risk on 6/24/2009 11:31:00 PM

Here is the CRE report mentioned yesterday, from RC Analytics: Moody’s/REAL Commercial Property Price Indices, June 2009

The Moody’s/REAL National All Property Type Aggregate Index for April measures 135.31, a decrease of 8.6% from the previous month. The index now stands 25.3% below the level seen a year ago and 29.5% below the peak measured in October 2007. The index is 27.4% lower than it was two years ago. This report is based on data through the end of April.Note that the Moody's CRE price index is a repeat sales index like Case-Shiller.

...

The Moody’s/REAL Commercial Property Price Indices (CPPI) measure the change in actual transaction prices for commercial real estate assets based on the repeat sales of the same assets at different points in time. ... A summary or short version of the repeat sales methodology is available in a Moody’s Special Report. US CMBS: Moody’s Publishes the First Commercial Property Price Indices Based on Commercial Real Estate Repeat Sales Data. Sept. 19, 2007. This is available on Moodys.com > Structured Finance > Commercial MBS > CRE Indices. A very detailed and complete explanation of the methodology is available in a White Paper from MIT. David Geltner and Henry Pollakowski. A Set of Indexes for Trading Commercial Real Estate Based on the Real Capital Analytics Transaction Prices Database. MIT Center for Real Estate. Sept. 26, 2007.

Click on graph for larger image in new window.

Click on graph for larger image in new window.Here is figure 1 from the report. CRE prices are back to 2004.

The Case-Shiller Composite 20 residential index is added in red (with Dec 2000 set to 100).

This shows residential leading CRE (although we usually talk about residential investment leading CRE investment, but in this case also for prices), and this also shows that prices tend to fall faster for CRE than for residential.

More on the New and Existing Homes Sales Gap

by Calculated Risk on 6/24/2009 08:51:00 PM

Earlier today I posted some analysis of the gap between existing and new home sales: Distressing Gap: Ratio of Existing to New Home Sales (see the post for several graphs - including the ratio between new and existing home sales)

Professor Brian Peterson has more (including some thoughts prices): House Prices and New versus Existing Homes Sales

To get a feel for how the two series [New and existing home sales] move together, figure 2 plots the percentage deviation for each series from its mean from 1975-2008. We see clearly that from 1975 to 2006 (the solid lines) that new home sales and existing homes sales move around together, with a correlation of 0.944 over the the time period up to 2006. However, as shown by the dashed lines, a gap has developed post 2006, resulting in the correlation for the sample from 1975-2008 falling to 0.876. There seems to be some type of a shock that is driving existing homes sale up relative to new homes sales.

I find it strange that most analysts are looking at existing home sales for stability in the housing market. I think the new home market is the place to look.

BofE Mervyn King: U.K. Recovery may be "long, hard slog"

by Calculated Risk on 6/24/2009 07:46:00 PM

From Bloomberg: King Says U.K. Recovery May Be ‘Long, Hard Slog’ (ht Jonathan)

“There has to be a risk that it will be a long, hard slog” because of the problems in the banking system, King told lawmakers in London today. “I feel more uncertain now than ever. This is not the pattern of a recession coming into recovery that we’ve seen since the 1930s. Having an open mind and not pretending to foresee the future when it’s so uncertain is important.”

...

King said that there’s “not much evidence to change our view” since the bank released forecasts in May showing that the economy won’t return to growth on an annual basis until the second half of next year.

emphasis added

Appraisals

by Calculated Risk on 6/24/2009 04:12:00 PM

Much is being written about the complaints of the NAR (Realtors) and the NAHB (Builders) concerning the Home Valuation Code of Conduct. And the response from the Appraisal Institute.

From Lawrence Yun, NAR chief economist:

"[T]he increase in sales is less than expected because poor appraisals are stalling transactions. Pending home sales indicated much stronger activity, but some contracts are falling through from faulty valuations that keep buyers from getting a loan.”From Joe Robson, chairman of the National Association of Home Builders (NAHB):

emphasis added

“In the midst of the prime home buying season, builders report that a number of factors are limiting new-home sales. These include consumer concerns about job security, potential buyers’ inability to sell their existing homes, and problems with appraisals coming in too low. The latter issue is directly related to the use of distressed properties (foreclosures and short sales) as comps, which disproportionately impacts assessed values of nearby homes.”This change started when NY Attorney General Andrew M. Cuomo sued First American for conspiring with WaMu to inflate real estate appraisals back in November 2007.

“The independence of the appraiser is essential to maintaining the integrity of the mortgage industry. First American and eAppraiseIT violated that independence when Washington Mutual strong-armed them into a system designed to rip off homeowners and investors alike,” said Attorney General Cuomo. “The blatant actions of First American and eAppraiseIT have contributed to the growing foreclosure crisis and turmoil in the housing market. By allowing Washington Mutual to hand-pick appraisers who inflated values, First American helped set the current mortgage crisis in motion.”The email evidence was pretty damning. And the HVCC was part of the settlement.

This has been coming for some time, and should be no surprise.

For a good background on the appraisal process, see Tanta's What's Wrong With Approved Appraiser Lists. Tanta was writing about approved appraiser lists, but her posts explains the appraisal problem. Here is an excerpt:

[W]hat WaMu is alleged to have done is itself the kind of conduct that is an automatic “red flag” for anyone who knows anything about how the appraisal management business works. Since most of you are fortunate enough to be entirely innocent of that, I thought I’d go through some issues here.The HVCC is addressing a very real and widespread appraisal problem. That doesn't mean the solution is perfect - and this shows once again that incentives matter.

First off, I’m talking about how the business works, not about how the principles of appraiser independence are derived by the Appraisal Foundation or why they matter so much. I’m taking as a given that we accept the axiom that when an appraiser’s compensation is based on his or her willingness to come up with the answer an interested party wants, instead of the answer he or she thinks the facts of the subject property, the transaction requested, and the local real estate market warrant, an appraisal is nothing more than a ratification of the loan amount someone has already decided on, and that “someone” isn’t the ultimate bagholder. The real bagholder wants to know whether it is lending too much or risking owning an unsalable piece of REO. That an individual loan officer or broker just wants to know how high we can make the loan amount—and thus a commission—is an artifact of a business structure in which a lender’s own employees or agents are not aligned with its own corporate best interests. At some level the appraisal problem will never get solved until the compensation of loan processing employees and intermediaries gets solved, but that’s not today’s argument.

In the olden days of local lenders, you had either staff appraisers or “fee appraisers.” You could actually have appraisers on your payroll because you lent in a defined local area: you didn’t have to worry about needing an appraisal for a property six states away that your staff appraisers couldn’t get to, even if they were licensed in that state. If you relied on fee appraisers, possibly because it was too expensive to keep appraisers on the payroll during down-cycles in RE, you still worked in a local market, you got to know all of them, and you could order appraisals from people whose work was familiar. If you were smart, you worked with the best appraisers there were. If you were stupid, you channeled business to your golf buddies. A number of S&Ls did the latter, and they did not live happily ever after. We have this thing called FIRREA, which brought into being USPAP, in large part because of that second option.

Once local lenders became regional lenders and then national lenders, the distance between corporate headquarters, the Appraisal Department, and the actual properties and markets grew to the point that having staff appraisers was impractical and hiring fee appraisers was a crap-shoot. You can pick up the Yellow Pages to find an appraiser in a market you just entered, but this means you will learn by doing in terms of quality. That goes double if you entered this market via wholesale lending: you now have a broker you don’t know much about hiring an appraiser you don’t know anything about in an RE market you’ve never done business in before.

The early years of national wholesale lending supplied lots of excitement, as Podunk National Bank changed its name to Ubiquitous, Inc. and charged into market areas about which it knew nothing, on the assumption that, say, Miami is just like Podunk except the loan amounts are bigger. Sometimes this was actually retail lending: Ubiquitous, Inc. started buying up branches in all these new and exciting markets, with the plan of managing them long-distance from corporate headquarters. Often those branches (complete with their employees) could be acquired for amazingly cheap sums of money. The Lender Formerly Known As Podunk often didn’t ask itself why the current owner of that branch wanted out so badly, but that’s hardly a problem unique to mortgage lending or banking.

Eventually, everyone had to deal with the hard knocks. You might be able to justify taking risks on the unknown when you move into a new market, but you still have to do something about the problems that crop up. Everyone got at least some really bad appraisals from the Yellow Pages approach, and had to start making some lists. I really think that a major problem lurking in the industry happened right here, when wholesalers and correspondent lenders made a decision about what kind of list to make. Do you make an “Approved Appraiser” list of the ones you haven’t had problems with, or do you make an “Excluded Appraiser” list of the ones you have had problems with?

There is no question that logically, the most efficient thing to do is make the exclusion list. Even if you believe that there are more than just a few bad apples, you don’t get into the national mortgage lending business if you believe that bad appraisers outnumber good appraisers by a wide margin. Exclusionary lists are just shorter and easier to administrate.

If you’re still a retail lender (just a long-distance one), you can keep the shorter exclusionary list internal to your own organization. The major disadvantage of exclusionary lists developed for the wholesale and correspondent lenders, and for any lender in the “originate and sell” rather than “originate and hold” business. If you are contracting with brokers, correspondent lenders, third-party investors and servicers and other folks who need to conduct due diligence on your loans, you end up having to make your list available to all those parties. It becomes nearly impossible to keep it confidential.

And that started the defamation fear. Too many lenders faced real or imagined threats of lawsuits from appraisers who did not want their names appearing on what had basically become a public hall of shame list. (I hasten to add that these things were not “public” to you, the consumer. They were an open secret to everyone in the business except the consumer.) So even though an approved appraiser list was a much more expensive, time-consuming, cumbersome way to get there, more and more big operations started keeping one. (Why not go to the regulators and beg for a "safe harbor" against defamation liability for exclusion lists? Because lenders are almost never long-sighted enough to ask for regulation that benefits them. They're too afraid that it always comes with the wrong strings attached. Then after the criminal probes and class actions and general shirt-losing, we look back wistfully on those strings we were so afraid of, wondering why we didn't snap that deal right up.)

An appraiser who is paid only if the loan is made, and is given the target number in advance, has a perverse incentive to "hit the number". However an appraiser that is paid no matter what, possibly has an incentive to be overly conservative and deliver a low ball appraisal that the NAR and NAHB and others are complaining about.

However lenders are still in the business of making loans (hopefully loans that will be repaid) - and the appraisers work for the lenders - and the lenders don't make money if the loan isn't made. So there is still an incentive to get deals done.

Report: Record Credit Card Charge-offs

by Calculated Risk on 6/24/2009 03:26:00 PM

From Reuters: US credit card chargeoffs break new record - Moody's

The U.S. monthly credit card chargeoff rate surpassed 10 percent and hit a sixth straight record high in May, Moody's Investors Services said on Wednesday ...Another month, another record.

The chargeoff rate index -- which measures credit card loans the banks do not expect to be repaid -- rose to 10.62 percent in May from 9.97 percent in April.

"We expect the chargeoff rate index to continue to rise in the coming months but at a slower pace, as it peaks at around 12 percent in the second quarter of 2010," Moody's senior vice president William Black said in a statement.

I wouldn't be surprised if Chase sees an increase in chargeoffs after raising the monthly minimum payment from 2% to 5% for some credit card users.

As a reminder, the credit card indicative loss rates for the "more adverse" stress test scenario were 18% to 20% over two years. That might have been a little optimistic. The baseline scenario was 12% to 17% over two years - way too low.