RSS Feed

RSS Feed by Calculated Risk on 1/19/2007 03:17:00 PM

Friday, January 19, 2007

First Horizon Hurt by Mortgage Unit

From Reuters: First Horizon profits fall, hurt by mortgage unit

First Horizon National Corp. said on Wednesday quarterly earnings fell a steeper-than-expected 28 percent as mortgage banking revenue plunged.UPDATE from Tanta (lifted from comments):

...

First Horizon of Memphis, Tennessee said pretax income from mortgage banking slid 91 percent to $3.5 million, while revenue from mortgage banking fell 27 percent to $111.9 million.

Lordy, the whole statement's worth a read. Looks like a perfect storm:

1. The carry trade died: "Net interest income decreased 41 percent to $20.4 million in fourth quarter 2006 from $34.7 million in fourth quarter 2005. An inverted yield curve resulted in compression of the spread on the warehouse, which was 1.24 percent in fourth quarter 2006 compared to 2.06 percent for the same period in 2005. Additionally, an 18 percent decrease in the warehouse related to lower origination activity negatively impacted net interest income."

2. Gain on sale dropped: "Net origination income decreased 22 percent to $69.2 million from $89.1 million in fourth quarter 2005 as loans delivered into the secondary market decreased 21 percent to $6.3 billion."

3. Keeping the loans rather than selling them didn't help credit quality: "Provision for loan losses increased to $23.0 million in fourth quarter 2006 from $16.2 million in fourth quarter 2005. This increase primarily reflects continued growth of the commercial and construction loan portfolios and an expectation of slowing economic growth. As a result of this increase, the allowance to loans ratio has increased from 92 basis points in fourth quarter 2005 to 98 basis points in fourth quarter 2006. Nonperforming assets were $139.0 million on December 31, 2006, compared to $79.7 million on December 31, 2005. The nonperforming assets ratio related to the loan portfolio increased to 58 basis points in fourth quarter 2006 from 33 basis points last year. The nonperforming asset ratio continues to migrate from historical low levels due to maturation of the loan portfolio, issues with several commercial credits in the retail commercial bank's traditional lending markets, and deterioration in the residential real estate portfolio reflecting the slow down in the housing market. The net charge-off ratio increased to 25 basis points in fourth quarter 2006 from 22 basis points in 2005 as net charge-offs grew to $13.5 million from $11.0 million during a period of strong loan growth."

I also see they increased their portfolio of residential construction loans by 11%, and also took a $7MM loss, part of which was "the result of employee misrepresentation in our construction lending business."

On Turning Bearish

by Calculated Risk on 1/19/2007 02:12:00 PM

I've recently turned bearish on the U.S. economy. This shouldn't be confused with my longer held negative views on housing.

For housing, I'm very confident that 2007 will be worse than 2006 by every material measure: prices, sales, residential construction employment, starts, MEW, percentage of homeowner equity, and the number of foreclosures.

But the impact of the continuing housing bust on the U.S. economy is far less certain. Although I think a recession is better than a "coin flip" in '07, the odds of a soft landing are still good.

Professor Leamer identified two key missing ingredients for a recession: enough job losses, and a credit crunch (see: Is a Recession Ahead? The Models Say Yes, but the Mind Says No). These are the two issues I wrestled with over the holidays, and I couldn't come to a definitive conclusion.

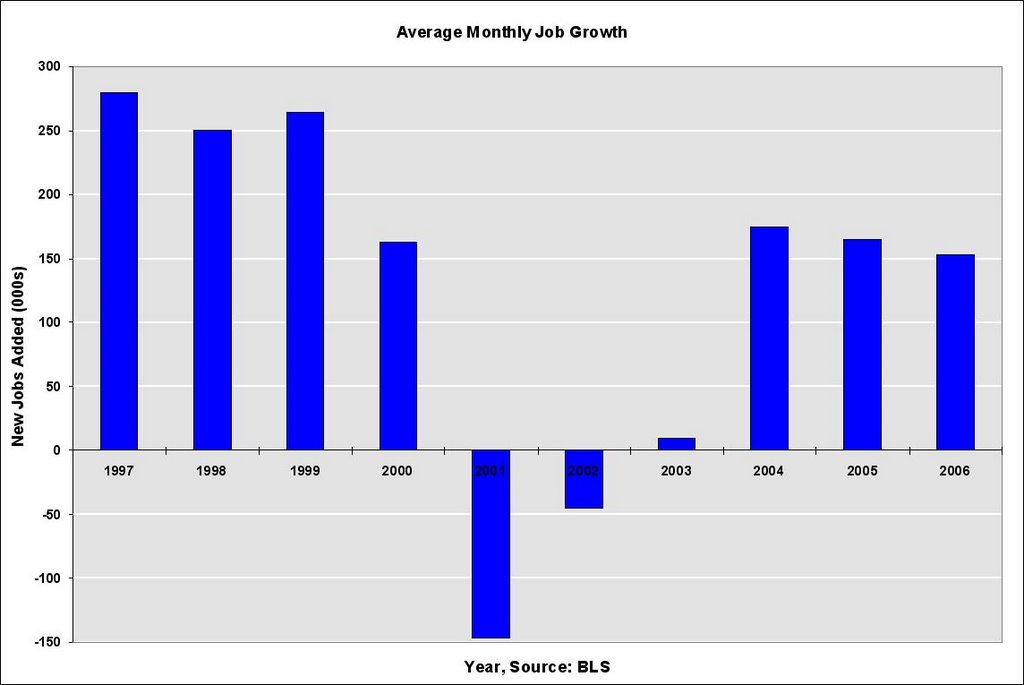

At the core, recessions are about jobs, and it is easy to imagine scenarios with job growth slowing to 100K per month, maybe even 50K per month. But that isn't a recession. Click on graph for larger image.

Click on graph for larger image.

This graph shows the average monthly job growth since 1997. In 2001, the economy lost an average of 147K jobs per month - and that was a fairly mild recession.

Over the last three years, the U.S. has added an average of 164K jobs per month. Right now, based on housing starts, it looks like residential construction employment will fall by 400K to 600K jobs by this Summer. Many of these workers will find new jobs, but it is easy to imagine job growth slowing to 100K per month. Adding in other housing related lost jobs, and some ripple effect, maybe growth will slow to 50K per month. Not enough for a recession.

So how can the U.S. economy slide into recession in '07?

Some possible sources: a credit crunch based on bad loans in the RE sector (and possibly in CRE and C&D too), less consumer spending based on falling MEW, and another downturn in the housing market. If all of these can be avoided, a recession is unlikely.

Right now I don't think these problems can be avoided.

Thursday, January 18, 2007

Pulte Homes Warns

by Calculated Risk on 1/18/2007 08:02:00 PM

Pulte Homes warns on Q4 results.

"Pulte Homes continues to navigate through a challenging operating environment, with demand for new homes during the fourth quarter still far below pre-2006 levels."Pulte had already guided earnings expectations lower. Now they are reducing their Q4 earnings estimates again:

Richard J. Dugas, Jr., President and CEO of Pulte Homes, Jan 18, 2007

The Company expects fourth quarter results to be in the range of a loss of $.05 to earnings of $.05 per diluted share from continuing operations. Pulte Homes had previously issued earnings guidance in the range of $.30 to $.70 per diluted share, guiding to the lower end of the range in its earnings conference call for the third quarter.Orders are getting worse:

The Company closed 12,566 homes during the fourth quarter of 2006, a decline of 20% from the fourth quarter of 2005. Net new orders for the quarter were 6,446 homes, a 34% decrease from last year's fourth quarter. For the full year 2006, home closings were 41,487, down 9% compared with 2005. Net new orders for the full year 2006 decreased 29% from the prior year to 33,925 homes.But the cancellation rate improved slightly:

"... [Pulte] experienced a stabilization to a slight improvement in our fourth quarter cancellation rate compared with the third quarter, as this metric showed progressive improvement throughout the period."Of course if orders fall to zero, the cancellation rate will decline to zero too. So this metric needs to be kept in context.

Impairments are much worse than expected:

On a preliminary basis, Pulte Homes anticipates that these impairments and land-related charges will be in the range of $330 million to $350 million for the fourth quarter, or $.83 to $.88 per diluted share. The Company previously issued guidance of $150 million for impairments and land-related charges.Perhaps the only good news is Pulte is reducing their production:

"[Pulte] continue[s] to reduce the number of homes we are starting, as evidenced by our meaningful reduction in speculative units under construction during the quarter."

DataQuick: 2006 California Sales Lowest Since 1996

by Calculated Risk on 1/18/2007 02:39:00 PM

DataQuick reports: California December Home Sales

Last month's sales made for the slowest December since 1996 when 33,591 homes were sold.Note that 1996 was the last year of the early '90s housing bust in California.

Click on graph for larger image.

Click on graph for larger image.A total of 41,100 new and resale houses and condos were sold statewide last month. That's up 4.8 percent from 39,200 for November and down 22.2 percent from a 52,800 for December 2005.Although some areas in California are already seeing YoY nominal price declines - like San Mateo, Sonoma, San Diego and Ventura - the median YoY price in California increased slightly.

Last month's sales made for the slowest December since 1996 when 33,591 homes were sold.

The median price paid for a home last month was $474,000. That was up 1.1 percent from November's $469,000, and up 3.5 percent from $458,000 for December a year ago.

Housing: Starts and Completions

by Calculated Risk on 1/18/2007 11:06:00 AM

The Census Bureau reports on housing Permits, Starts and Completions. Seasonally adjusted permits rose slightly:

Privately-owned housing units authorized by building permits in December were at a seasonally adjusted annual rate of 1,596,000. This is 5.5 percent above the revised November rate of 1,513,000, but is 24.3 percent below the December 2005 estimate of 2,107,000.Starts were up for the second straight month:

Privately-owned housing starts in December were at a seasonally adjusted annual rate of 1,642,000. This is 4.5 percent above the revised November estimate of 1,572,000, but is 18.0 percent below the December 2005 rate of 2,002,000.And Completions were flat, at just below the recent record levels:

Privately-owned housing completions in December were at a seasonally adjusted annual rate of 1,900,000. This is 0.4 percent above the revised November estimate of 1,893,000, but is 2.7 percent below the December 2005 rate of 1,953,000.

Click on graph for larger image.

Click on graph for larger image.The first graph shows Starts vs. Completions.

I'm a little surprised at the slight rebound in starts, especially since completions and inventories are still near record levels. Still Starts have fallen "off a cliff", and completions have just started to fall.

This graph shows starts, completions and residential construction employment. (starts are shifted 6 months into the future). Completions and residential construction employment are highly correlated, and Completions lag Starts by about 6 months.

Based on historical correlations, it is reasonable to expect Completions and residential construction employment to follow Starts "off the cliff". This would indicate the loss of 400K to 600K residential construction employment jobs by this Summer.

Wednesday, January 17, 2007

Worth a second look ...

by Calculated Risk on 1/17/2007 05:51:00 PM

If you missed Tanta's most recent post, it is definitely worth reading (and rereading): Information is Power, Which is Why You Don’t Get Any.

Make sure you read the comments too.

I just hope she wasn't referring to me when she wrote:

"... next time I'll write something calm and polite and professional and bland and get my case jumped by the readers who are tired of calm and polite and professional and bland because that's all you ever get in the newspaper and we come to blogs for some juice."

DataQuick: Bay Area home prices flat, slow sales

by Calculated Risk on 1/17/2007 05:14:00 PM

From DataQuick: Bay Area home prices flat, slow sales

Bay Area home prices were flat last month while the sales pace was the slowest pace in a decade ...Just six months ago, DataQuick reported "indicators of market distress are still largely absent" and "foreclosure rates are coming up from last year's low point, but are still below normal levels". Now foreclosures are in the "normal range", and from the information I'm receiving, foreclosures will be significantly above normal shortly.

A total of 7,488 new and resale houses and condos sold in the Bay Area last month. That was up 3.9 percent from 7,204 in November, and down 19.9 percent from 9,347 for December last year, according to DataQuick Information Systems.

Sales have declined on a year-over-year basis the last 21 months. Last month's sales count was the lowest for any December since 1996 when 7,180 homes were sold. The average for all Decembers since 1988 is 8,339.

...

The median price paid for a Bay Area home was $612,000 in December. That was down 0.6 percent from $616,000 in November and up 0.5 percent from $609,000 for December a year ago. The median peaked last June at $644,000.

...

Indicators of market distress are still in the normal range. Financing with adjustable-rate mortgages is flat. Foreclosure activity is rising but is still in the normal range. Down payment sizes are stable. Flipping rates and non-owner occupied buying activity are down, DataQuick reported.

Fed's Mishkin on Monetary Policy and House Prices

by Calculated Risk on 1/17/2007 01:12:00 PM

From Fed Governor Frederic Mishkin: The Role of House Prices in Formulating Monetary Policy

Once again the Fed is arguing against taking action when a possible bubble is forming. This is the same argument Greenspan made during the stock market bubble, but this time the issue is housing. However, the Fed stands ready to take action if the bursting of the bubble impacts the general economy.

Mishkin's conclusion:

Large run-ups in prices of assets such as houses present serious challenges to central bankers. I have argued that central banks should not give a special role to house prices in the conduct of monetary policy but should respond to them only to the extent that they have foreseeable effects on inflation and employment. Nevertheless, central banks can take measures to prepare for possible sharp reversals in the prices of homes or other assets to ensure that they will not do serious harm to the economy.

NAHB: Builder Confidence Improves in January

by Calculated Risk on 1/17/2007 12:59:00 PM

From NAHB: Builder Confidence Improves in January

Click on graph for larger image.

Click on graph for larger image.

Excerpts:

The HMI increased from an upwardly revised 33 in December to 35 in January, its highest level since July of 2006.

...

Two out of three component indexes registered improvement in January. The index gauging current single-family home sales and the index gauging traffic of prospective buyers each gained three points, to 36 and 26 respectively, while the index gauging sales expectations for the next six months remained unchanged at 49.

Meanwhile, three out of four regions surveyed in the HMI posted gains in January. Two-point gains were registered in the Northeast, Midwest and South, to 39, 24 and 41, respectively. The HMI for the West remained unchanged from the previous month at 32.

MBA: Purchase Applications Decrease

by Calculated Risk on 1/17/2007 10:39:00 AM

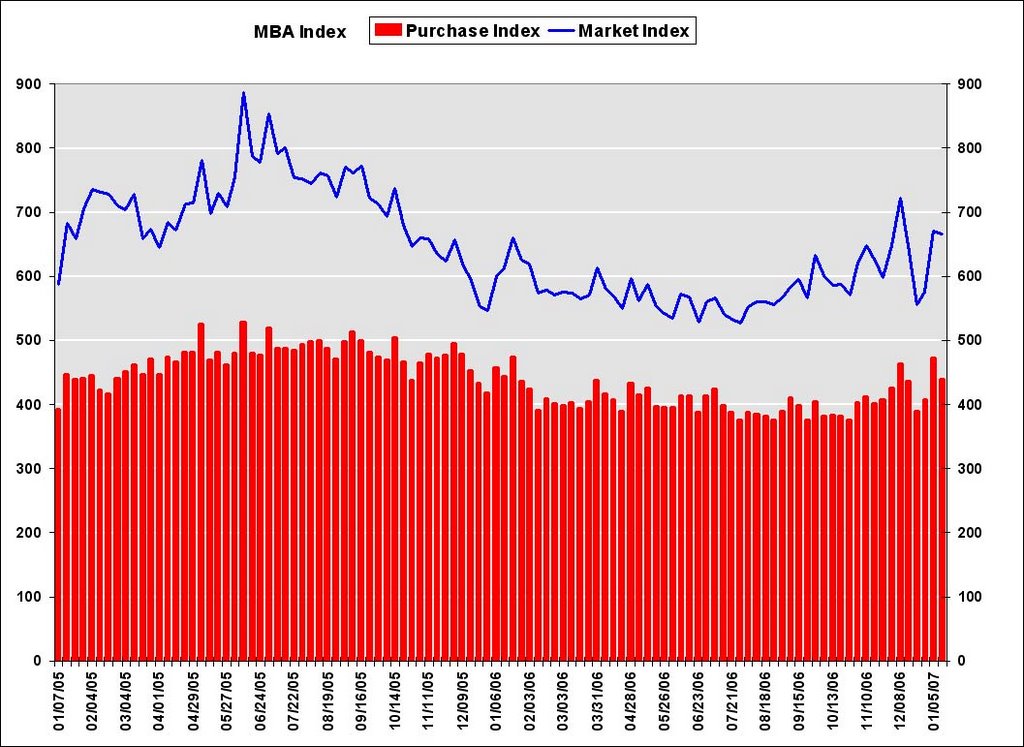

The Mortgage Bankers Association (MBA) reports: Refinance Applications Increase and Purchase Applications Decrease Click on graph for larger image.

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 667.2, a decrease of 0.6 percent on a seasonally adjusted basis from 671.1 one week earlier. On an unadjusted basis, the Index increased 28.9 percent compared with the previous week and was up 9.8 percent compared with the same week one year earlier.Mortgage rates increased:

The Refinance Index increased by 6.3 percent to 2045.8 from 1923.8 the previous week and the seasonally adjusted Purchase Index decreased by 7 percent to 439.7 from 472.8 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.19 from 6.13 percent ...

The average contract interest rate for one-year ARMs increased to 5.85 percent from 5.79 ...

The second graph shows the Purchase Index and the 4 and 12 week moving averages since January 2002. The four week moving average is up 0.2 percent to 427.4 from 426.6 for the Purchase Index.

The second graph shows the Purchase Index and the 4 and 12 week moving averages since January 2002. The four week moving average is up 0.2 percent to 427.4 from 426.6 for the Purchase Index.The refinance share of mortgage activity increased to 49.9 percent of total applications from 48.4 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 21.2 from 20.1 percent of total applications from the previous week.