RSS Feed

RSS Feed by Calculated Risk on 5/13/2015 07:00:00 AM

Wednesday, May 13, 2015

MBA: Mortgage Applications Decrease in Latest Weekly Survey

From the MBA: As Rates Climb, Refinance Applications Continue to Drop

Mortgage applications decreased 3.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 8, 2015. ...

The Refinance Index decreased 6 percent from the previous week. The seasonally adjusted Purchase Index decreased 0.2 percent from one week earlier. The unadjusted Purchase Index increased 0.1 percent compared with the previous week and was 12 percent higher than the same week one year ago.

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.00 percent, its highest level since March 2015, from 3.93 percent, with points increasing to 0.36 from 0.35 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index.

2014 was the lowest year for refinance activity since year 2000.

It would take much lower rates - below 3.5% - to see a significant refinance boom this year.

The second graph shows the MBA mortgage purchase index.

The second graph shows the MBA mortgage purchase index. According to the MBA, the unadjusted purchase index is 12% higher than a year ago.

Tuesday, May 12, 2015

Wednesday: Retail Sales

by Calculated Risk on 5/12/2015 10:26:00 PM

From the WSJ: Don’t Expect Cheap Gasoline to Fuel Retail Sales

The slump in crude oil had, as of February, led to pump-price savings estimated at over $100 billion annually for American households. But tepid retail-sales data from December through February left forecasters scratching their heads about consumers’ failure to spend much of it.Wednesday:

Back in November, year-over-year growth in retail sales was running at 4.7%. It had slipped to 1.26% by March. Even stripping out gas-station sales, it had slowed to 4% from 5.8% over the same period.

There are two likely explanations: the weather and the fact spending is sticky.

• At 7:00 AM ET, the Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, the Retail sales for April will be released. The consensus is for retail sales to increase 0.2% in April, and to increase 0.5% ex-autos.

• At 10:00 AM, Manufacturing and Trade: Inventories and Sales (business inventories) report for March. The consensus is for a 0.2% increase in inventories.

Mortgage News Daily: Mortgage Rates at 2015 Highs, Average Lender at 4%

by Calculated Risk on 5/12/2015 05:32:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Keep Pushing 2015 Highs

Mortgage rates moved disconcertingly higher again today, despite the fact that underlying market levels actually improved during the day. Guaranteeing rates in such a volatile environment is expensive for lenders. The result is yet another high for 2015. The average lender is quoting conventional 30yr fixed rates of 4.0% on top tier scenarios. Just a few short weeks ago, the average rate was 3.625%. That makes this the most abrupt move higher in roughly 2 years, with the last notable example being the mid-2013 'taper tantrum.'Here is a table from Mortgage News Daily:

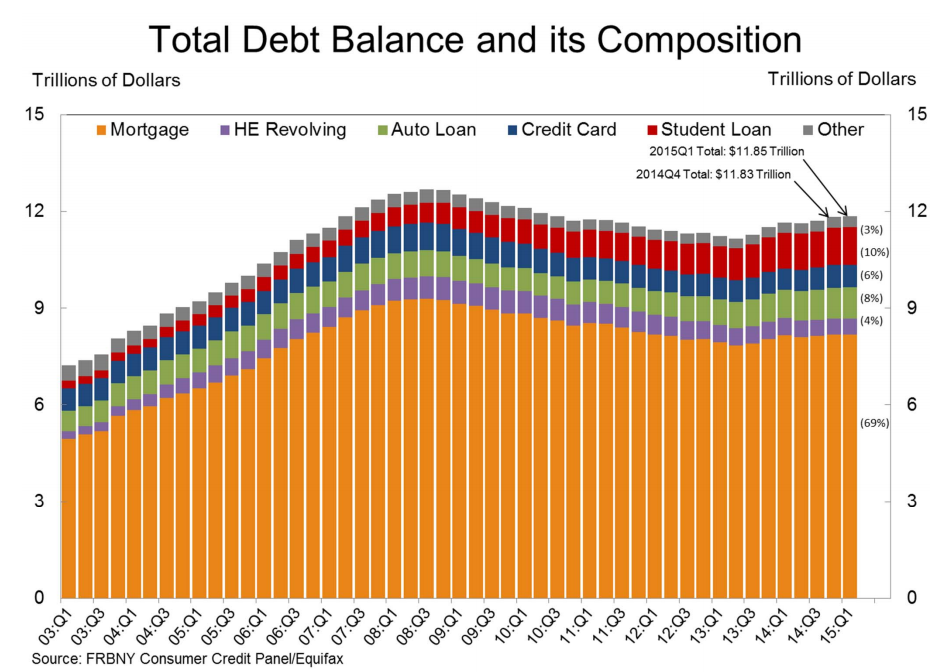

NY Fed: Household Debt increased slightly in Q1 2015

by Calculated Risk on 5/12/2015 01:11:00 PM

Here is the Q1 report: Household Debt and Credit Report.

From the NY Fed: Delinquencies, Foreclosures and Bankruptcies Improve as Household Debt Stays Flat

The Federal Reserve Bank of New York’s Household Debt and Credit Report revealed that aggregate household debt balances were largely flat in the first quarter of 2015. As of the end of March, total household indebtedness was $11.85 trillion, a $24 billion, or 0.2 percent, increase during the first quarter of this year. The report is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample drawn from anonymized Equifax credit data.

The slowdown in growth can be attributed to a negligible uptick in mortgage balances, which are the largest component of household debt. Mortgage balances stood at $8.17 trillion in the first quarter. Additionally, balances on home equity lines of credit (HELOC), which were $510 billion at the end of fourth quarter, 2014, were unchanged in the first quarter of this year.

Non-housing debt balances increased by 0.7 percent from the end of last year, largely due to increases in student loans ($32 billion) and auto loans ($13 billion). These gains were partially offset by a $16 billion decline in credit card balances.

Measures on delinquencies, foreclosures and bankruptcies all improved in the first quarter. The percentage of outstanding debt in some stage of delinquency fell to 5.7 percent from 6.0 percent in the fourth quarter of 2014, with continuing improvements in mortgages. About 112,000 individuals had a new foreclosure notation added to their credit reports in the first quarter of this year, the lowest total since at least 1999. Four percent fewer consumers had a bankruptcy notation added to their credit reports, bringing the quarterly total to its lowest point since early 2006.

“Tight standards on mortgage lending are reflected in both sluggish growth in housing debt as well as substantial reductions in mortgage delinquency and defaults,“ said Andrew Haughwout, senior vice president and economist at the New York Fed.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here are two graphs from the report:

The first graph shows aggregate consumer debt increased slightly in Q1. Household debt peaked in 2008, and bottomed in Q2 2013.

The recent increase in debt suggests households (in the aggregate) deleveraging is over.

The second graph shows the percent of debt in delinquency. The percent of delinquent debt is generally declining, although there is still a large percent of debt 90+ days delinquent (Yellow, orange and red).

The second graph shows the percent of debt in delinquency. The percent of delinquent debt is generally declining, although there is still a large percent of debt 90+ days delinquent (Yellow, orange and red). The overall delinquency rate decreased to 5.7% in Q1, from 6.0% in Q4.

There are a number of credit graphs at the NY Fed site.

BLS: Jobs Openings at 5.0 million in March, Up 19% Year-over-year

by Calculated Risk on 5/12/2015 10:09:00 AM

From the BLS: Job Openings and Labor Turnover Summary

There were 5.0 million job openings on the last business day of March, little changed from 5.1 million in February, the U.S. Bureau of Labor Statistics reported today. Hires were little changed at 5.1 million in March and separations were little changed at 5.0 million....The following graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

...

Quits are generally voluntary separations initiated by the employee. Therefore, the quits rate can serve as a measure of workers’ willingness or ability to leave jobs. ... There were 2.8 million quits in March, little changed from February.

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for March, the most recent employment report was for April.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

Jobs openings decreased in March to 4.994 million from 5.144 million in February.

The number of job openings (yellow) are up 19% year-over-year compared to March 2014.

Quits are up 14% year-over-year. These are voluntary separations. (see light blue columns at bottom of graph for trend for "quits").

This is another solid report. It is a good sign that job openings are around 5 million, and that quits are increasing solidly year-over-year.