RSS Feed

RSS Feed by Calculated Risk on 12/15/2014 08:32:00 PM

Monday, December 15, 2014

Tuesday: Housing Starts

Two related articles ...

From the NY Times: Russia’s Central Bank Abruptly Raises Key Rate to 17%

With Russia scrambling to contain a currency crisis, the country’s central bank, in a surprise middle-of-the-night move, increased its key interest rate to 17 percent, from 10.5 percent.From the WSJ: Oil Prices Fall to Fresh Lows

...

The rate increase came after the ruble plummeted yet again on Monday, by more than 10 percent, to around 64 per dollar. The ruble has lost nearly half its value this year.

Oil for January delivery fell $1.90, or 3.3%, to close at $55.91 a barrel, the lowest level since May 2009 on the New York Mercantile Exchange.There is more to the ruble collapse than declining oil prices, but it is a huge factor.

Brent crude, the global benchmark, slid 1.3% to $61.06 a barrel, the lowest level since July 2009, on ICE Futures Europe.

Tuesday:

• At 8:30 AM ET, Housing Starts for November. Total housing starts were at 1.009 million (SAAR) in October. Single family starts were at 696 thousand SAAR in October. The consensus is for total housing starts to increase to 1.038 million (SAAR) in November.

Lawler: Updated Table of Distressed Sales and Cash buyers for Selected Cities in November

by Calculated Risk on 12/15/2014 06:25:00 PM

Economist Tom Lawler sent me the updated table below of short sales, foreclosures and cash buyers for a few selected cities in November.

On distressed: Total "distressed" share is down in these markets mostly due to a decline in short sales (the Mid-Atlantic and Orlando were unchanged).

Short sales are down significantly in these areas.

Foreclosures are up in several areas (working through the logjam).

The All Cash Share (last two columns) is declining year-over-year. As investors pull back, the share of all cash buyers will probably continue to decline.

| Short Sales Share | Foreclosure Sales Share | Total "Distressed" Share | All Cash Share | |||||

|---|---|---|---|---|---|---|---|---|

| Nov-14 | Nov-13 | Nov-14 | Nov-13 | Nov-14 | Nov-13 | Nov-14 | Nov-13 | |

| Las Vegas | 9.5% | 21.0% | 8.7% | 7.0% | 18.2% | 28.0% | 32.8% | 43.7% |

| Reno** | 6.0% | 17.0% | 6.0% | 6.0% | 12.0% | 23.0% | ||

| Phoenix | 4.1% | 7.8% | 5.7% | 8.0% | 9.7% | 15.8% | 28.0% | 34.0% |

| Sacramento | 6.1% | 11.0% | 5.4% | 4.6% | 11.5% | 15.6% | 16.9% | 25.0% |

| Minneapolis | 3.1% | 5.0% | 10.2% | 16.9% | 13.4% | 21.9% | ||

| Mid-Atlantic | 4.7% | 7.5% | 11.0% | 8.1% | 15.7% | 15.7% | 19.1% | 19.6% |

| Orlando | 6.2% | 13.7% | 27.8% | 20.3% | 34.0% | 34.0% | 42.1% | 46.2% |

| So. California* | 6.2% | 10.5% | 5.3% | 6.3% | 11.5% | 16.8% | 23.9% | 28.1% |

| Northeast Florida | 29.7% | 38.1% | ||||||

| Chicago (City) | 20.2% | 32.8% | ||||||

| Hampton Roads | 20.4% | 26.9% | ||||||

| Toledo | 35.4% | 37.2% | ||||||

| Tucson | 26.3% | 32.2% | ||||||

| Des Moines | 19.3% | 19.9% | ||||||

| Peoria | 19.7% | 21.8% | ||||||

| Georgia*** | 26.5% | N/A | ||||||

| Omaha | 21.1% | 21.6% | ||||||

| Memphis* | 15.1% | 20.5% | ||||||

| Springfield IL** | 11.8% | 17.6% | ||||||

| *share of existing home sales, based on property records **Single Family Only ***GAMLS | ||||||||

Lawler: Early Read on Existing Home Sales in November (look for big dip)

by Calculated Risk on 12/15/2014 04:06:00 PM

From housing economist Tom Lawler

Based on local realtor/MLS reports from across the country, I estimate that US existing home sales as measured by the National Association of Realtors ran at a seasonally adjusted annual rate of about 4.93 million in November, down 6.3% from October’s preliminary pace but up 2.1% from last November’s pace. On the inventory front, the vast majority of local reports showed a larger monthly decline in listings this November compared to last November, and I estimate that the inventory of existing homes for sale as measured by the NAR for the end of November will be 2.12 million, down 4.5% from October and up 3.4% from a year ago.

Finally, a median existing SF home sales price for November that was up about 4.7% from last November would be consistent with local realtor/MLS reports. On this latter point, I should note that the YOY increases shown in the NAR’s median sales prices for the last several months have been higher than local realtor/MLS reports would have suggested.

CR Note: Existing home sales will be released next week on Monday, December 22nd.

A Comment on Oil Prices

by Calculated Risk on 12/15/2014 02:20:00 PM

Recently there has been a dramatic decline in oil prices. This has led to some wild and confusing articles. As an example, Barry Ritholtz excerpted from an article that started: "Most observers thought the Organization of Petroleum Exporting Countries (OPEC) would cut its production to protect its members’ incomes and slash frackers’ profits."

That is wrong. If OPEC cut production, that would help the frackers (not hurt them). And most analysts I know didn't except OPEC to cut production.

For example, from Professor Hamilton on Oct 19th: How will Saudi Arabia respond to lower oil prices?

Oil prices (along with prices of many other commodities) have fallen dramatically since last summer. Some observers are waiting to see if Saudi Arabia responds with significant cutbacks in production. I say, don’t hold your breath.So it was no surprise that OPEC didn't cut production.

...

[In October] I discussed the three main factors in the recent fall in oil prices: (1) signs of a return of Libyan production to historical levels, (2) surging production from the U.S., and (3) growing indications of weakness in the world economy.

As far as Libya is concerned, the politics on the ground remain quite unsettled. It makes sense to wait and see if anticipated production gains are really going to hold before anybody makes major adjustments.

In terms of surging U.S. production, the key question is how low the price can get before significant numbers of U.S. producers decide to pull out. If world economic growth indeed slows, and if most of the frackers are willing to keep going strong ... trying to maintain the price ... could be a losing bet for the Saudis. They’d be giving up their own revenue just in order to keep the money flowing into ever-growing operations in Texas and North Dakota.

...

And as for worries of another global economic downturn, so far they are only that– worries. If and when we see a downturn materialize, then I would expect to see the Saudis cut back production.

But until then it’s primarily a question of responding to surging output of U.S. tight oil. My guess is that Saudi Arabia would lower prices rather than cut production as long as that’s the name of the game.

emphasis added

And the speculation that oil producers are trying to hurt Iran, Russia, or terrorists ... that is also incorrect.

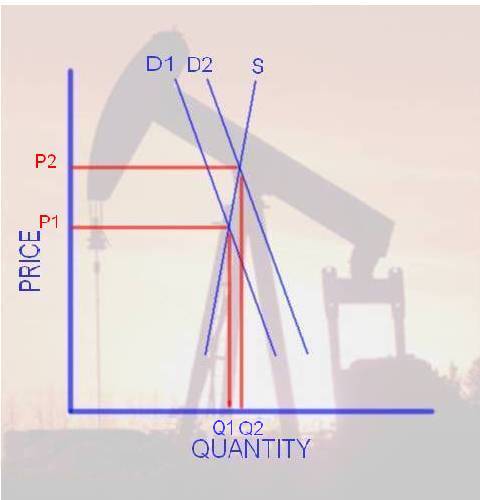

The reason prices have fallen sharply is supply and demand. It is important to remember that the short term supply and demand curves for oil are very steep.

If there is little unused capacity, it takes time for more oil production to become available since this involves huge capital intensive projects. And, in the short term, demand is fairly inelastic over a wide range of prices; for the most part people stay with their routines and keep their same vehicle. With two steep curves (supply and demand) we get the following:

Click on graph for larger image.

Click on graph for larger image.This is a graph I post in 2005. Back in 2005, I pointed out that with a small increase in Demand (from D1 to D2), we would see a small increase in Quantity (Q1 to Q2), but a large change in Price (from P1 to P2). Also a large price increase would also occur if we had a small decrease in supply such as a disruption to production, transport or refining.

And the opposite is also true. A relatively small decrease in demand or increase in supply (fracking) could cause a significant decline in prices. Especially now with OPEC's diminished role (since cutting production helps other producers).

In the long run, supply and demand will adjust to price changes. But if someone asks why prices have fallen so sharply recently, the answer is "supply and demand" and that the short term supply and demand curves are steep for oil.

NAHB: Builder Confidence decreased to 57 in December

by Calculated Risk on 12/15/2014 10:00:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 57 in December, down from 58 in November. Any number above 50 indicates that more builders view sales conditions as good than poor.

From the NAHB: Builder Confidence Drops One Point in December

Following a four-point uptick last month, builder confidence in the market for newly built single-family homes fell one point in December to a level of 57 on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today.

“Members in many markets across the country have seen their businesses improve over the course of the year, and we expect builders to remain confident in 2015,” said NAHB Chairman Kevin Kelly, a home builder and developer from Wilmington, Del.

“After a sluggish start to 2014, the HMI has stabilized in the mid-to-high 50s index level trend for the past six months, which is consistent with our assessment that we are in a slow march back to normal,” said NAHB Chief Economist David Crowe. “As we head into 2015, the housing market should continue to recover at a steady, gradual pace.”

...

Two of the three HMI components posted slight losses in December. The index gauging current sales conditions fell one point to 61, while the index measuring expectations for future sales dropped a single point to 65 and the index gauging traffic of prospective buyers held steady at 45.

Looking at the three-month moving averages for regional HMI scores, the West rose by four points to 62 and the Northeast edged up one point to 45, while the Midwest registered a three-point loss to 54 and the South dropped two points to 60.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph show the NAHB index since Jan 1985.

This was below the consensus forecast of 59.