RSS Feed

RSS Feed by Calculated Risk on 8/10/2010 12:41:00 PM

Tuesday, August 10, 2010

FOMC Statement Preview

I think there are three things to look for in the statement today at 2:15 PM ET.

1) How will the statement discuss the recent economic slowdown?

From the June 23rd FOMC statement:

"Information received since the Federal Open Market Committee met in April suggests that the economic recovery is proceeding and that the labor market is improving gradually. ... [T]he Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, although the pace of economic recovery is likely to be moderate for a time."I expect the statement today to acknowledge the weaker data since the last meeting.

2) Will they express more concern about deflation?

Last month:

"[U]nderlying inflation has trended lower. With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to be subdued for some time."Those sentences might remain the same.

3) And the BIG one: Will the FOMC change their reinvestment strategy?

Currently the FOMC is not reinvesting maturing MBS. This is passively shrinking the Fed's balance sheet, and probably at a faster rate than expected because of recent refinance activity.

The Fed might decide to reinvest the maturing MBS. If they do, the questions are: For how long (end of 2011)? And what will they buy (probably Treasury Securities, but what duration)?

My guess is there will be no change to the current MBS run off strategy.

"Buy and Bail" Again

by Calculated Risk on 8/10/2010 10:34:00 AM

This is an update on an old story ...

From Bloomberg: `Buy and Bail' Homeowners Get Past Loan Restrictions (ht Mike in Long Island, Paulo)

Real estate professionals call it “buy and bail,” acquiring a new house before the buyer’s credit rating is ruined by walking away from the old one ...It is really only "buy and bail" if the home buyer intends to walk away from the original house. With these new restrictions, I doubt this is a significant problem any more.

Freddie Mac and larger rival Fannie Mae cracked down on buy and bail in 2008 by banning in most cases the use of rental income from an existing home to qualify for a new mortgage unless the first property has at least 30 percent equity.

“There were a number of policies put in place to squelch this type of activity, but people who are savvy can always find a way to circumvent policies,” said [Meg Burns, senior associate director for congressional affairs and communications at the Federal Housing Finance Agency] ...

In addition to the rental restrictions, the mortgage giants now usually require reserves equal to six months of loan payments for both homes. The measures have been sufficient to block most applicants who attempt to buy and bail, said Pete Bakel, a spokesman for Washington-based Fannie Mae.

NFIB: Small Business Optimism Declines

by Calculated Risk on 8/10/2010 08:10:00 AM

From the National Federation of Independent Business (NFIB): Small Business Economic Trends Click on graph for larger image in new window.

Click on graph for larger image in new window.

NFIB reported its optimism index fell 0.9 point to 88.1 in July. (Graph from NFIB)

Here are the details:

The Index of Small Business Optimism lost 0.9 points in July following a sharp decline in June. The persistence of Index readings below 90 is unprecedented in survey history. ...Note: A large percentage of small businesses are in real estate related fields and that will keep optimism down.

Labor Market

Ten (10) percent (seasonally adjusted) reported unfilled job openings, up one point from June but historically very weak. Over the next three months, nine percent plan to increase employment (down one point), and 10 percent plan to reduce their workforce (up two points) ...

Capital Spending

The frequency of reported capital outlays over the past six months fell one point to 45 percent of all firms, one point above the 35 year record low reached most recently in December 2009. The percent of owners planning to make capital expenditures over the next few months fell one point to 18 percent, two points above the 35 year record low.

Credit

[C]redit availability does not appear to be the cause of slow growth as many allege. Four percent of the owners reported “finance” as their top business problem, down two points. Pre-1983, as many as 37 percent cited financing and interest rates as their top problem. What businesses need are customers, giving them a reason to hire and make capital expenditures and borrow to support those activities.

Once again the key problem is lack of demand.

Monday, August 09, 2010

REO Inventory including private-label RMBS

by Calculated Risk on 8/09/2010 09:24:00 PM

Earlier I posted a graph of Fannie, Freddie and FHA inventory (new record total in Q2).

Economist Tom Lawler has added private-label RMBS REO in the following graph.

Note: The private-label securities have one advantage - they essentially stopped making new loans in mid-2007! (see Figure 3 from San Francisco Fed Senior Economist John Krainer: Recent Developments in Mortgage Finance)

Update: The private-label securities are the ones securitized by Wall Street. This was the worst of the worst securities. Click on graph for larger image in new window.

Click on graph for larger image in new window.

From Tom Lawler:

As the chart indicates, the SF REO inventory of “the F’s” has increased sharply since the end of 2008, while the SF REO inventory held in private-label RMBS has fallen considerably. This chart, of course, does NOT include anything close to all REO, as SF REO properties owned by banks, thrifts, credit unions, VA, USDA, finance companies, and “other” mortgage lenders/investors are not included.

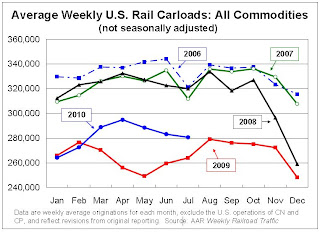

Rail Traffic increases 4.1% in July compared to July 2009

by Calculated Risk on 8/09/2010 04:15:00 PM

From the Association of American Railroads: Rail Time Indicators. The AAR reports traffic in July 2010 was up 4.1% compared to July 2009 - and traffic was 14.6% lower than in July 2008. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows U.S. average weekly rail carloads (NSA). Traffic increased in 14 of 19 major commodity categories year-over-year.

From AAR:

• U.S. freight railroads originated 1,122,308 carloads in July 2010, an average of 280,577 carloads per week — up 4.1% from July 2009 (see chart) but down 14.6% from July 2008 on a non-seasonally adjusted basis.As the graph above shows, rail traffic collapsed in November 2008, and now, a year into the recovery, traffic has only recovered part way.

• On a seasonally adjusted basis, U.S. rail carloads rose 3.2% in July 2010 from June 2010 after falling 1.2% in June 2010 and 0.9% in May 2010. The seasonally adjusted weekly average of 289,320 carloads in July 2010 was the highest such figure since November 2008.

excerpts with permission

Seasonally there is usually a decline in traffic in July, so seasonally adjusted traffic increased last month. However traffic is only up 4.1% compared to July 2009.