RSS Feed

RSS Feed by Calculated Risk on 6/30/2010 04:06:00 PM

Wednesday, June 30, 2010

Market Update

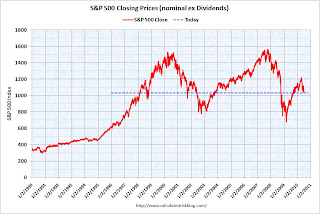

The end of Q2 ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

The first graph shows the S&P 500 since 1990 (this excludes dividends).

The dashed line is the closing price today. The S&P 500 was first at this level in February 1998; over 12 years ago.

Click on graph for interactive version in new window.

The graph has tabs to look at the different bear markets - "now" shows the current market - and there is also a tab for the "four bears".

Fed's Lockhart: Sustainable final demand not yet supporting growth

by Calculated Risk on 6/30/2010 01:39:00 PM

From Atlanta Fed President Dennis Lockhart: Recovery and the Challenge of Uncertainty

The central question is whether the recovery that is now well under way will be sustained or will falter, resulting in a slowdown or even a second recession—the so-called double dip.

...

Rising consumer activity surprised many in the first quarter of the year, but in April and May consumers seemed to put away their wallets to a certain extent. ... Business spending on equipment and software has been strong in the first half of the year. ... Manufacturing production is up about 8 percent over the past year through May.

...

Here's a key point about these contributors to recovery—each could be transitory. The economy has not yet arrived at a state where healthy and sustainable final demand is underpinning growth.

... I believe the recovery will move ahead at a modest pace and unemployment will gradually come down. Impediments to growth are being removed. Financial market function is being restored. Private balance sheets are being repaired. And necessary structural adjustments are under way.

The past few weeks, however, have seen a slight retrenchment from the mind-set of optimism and growing confidence that prevailed earlier in the year.

...

Several recent sources of uncertainty have clouded the outlook. I will cite four, including the oil spill in the Gulf.

First is European sovereign debt. ... Our financial system here in the United States has rather small and manageable direct exposure to the Greek government and the other sovereign borrowers. But as the situation has evolved, exposure to European banks as well as foreign and local corporations in the affected countries has complicated the estimation of risk.

...

A second source of uncertainty is ongoing state and local fiscal tightening.

...

A third area of uncertainty is commercial real estate. Banks across the country, especially small and regional banks, are heavily exposed to the commercial property sector and face a heavy docket of loan restructurings that may require sizable write-downs.

...

And there is the oil spill, which is, naturally, the central environmental and economic concern here in Louisiana and more broadly in the Gulf region. ...

The economic effect at the national level has been limited. I'm prepared to believe, however, that this relentless environmental disaster is an additional factor holding back consumer and business confidence. The spill disheartens us all and, I believe, makes the public a little more reticent to assume a smooth recovery path.

...

So, to pull this together, a recovery of the national economy is proceeding but not yet with solid and sustainable underpinnings. Inflation appears restrained. The outlook from here is beset by somewhat more than normal uncertainty.

Restaurant Index "Softened" in May

by Calculated Risk on 6/30/2010 11:57:00 AM

This is one of several industry specific indexes I track each month.  Click on graph for larger image in new window.

Click on graph for larger image in new window.

For the second consecutive month, same store sales and customer traffic both declined in May (year-over-year).

This has taken a toll on the positive outlook in the "expectations index" and the overall index showed contraction in May.

Unfortunately the data for this index only goes back to 2002.

Note: Any reading above 100 shows expansion for this index.

From the National Restaurant Association (NRA): Restaurant Industry Outlook Softened in May as Restaurant Performance Index Fell Below 100

The outlook for the restaurant industry softened in May, as the National Restaurant Association’s comprehensive index of restaurant activity fell below 100 for the first time in three months. The Association’s Restaurant Performance Index (RPI) – a monthly composite index that tracks the health of and outlook for the U.S. restaurant industry – stood at 99.7 in May, down 0.7 percent from April’s level of 100.4.Restaurants are a discretionary expense, and they tend to be 'first in, last out' of a recession for consumer spending (as opposed to housing that is usually first in and first out). Since restaurants both lead and lag recessions, this contraction could be because of the sluggish recovery or might suggest further weakness in consumer spending in the months ahead.

...

Restaurant operators reported a net decline in same-store sales for the second consecutive month in May.

...

Restaurant operators also reported softer customer traffic results in May.

...

Although sales and traffic results softened in May, restaurant operators reported an uptick in capital spending activity.

...

Although restaurant operators remain optimistic about sales growth in the months ahead, their optimism slipped somewhat in recent months.

emphasis added

Chicago PMI shows expansion in June

by Calculated Risk on 6/30/2010 09:45:00 AM

From the Institute for Supply Management – Chicago:

The Chicago Purchasing Managers reported the CHICAGO BUSINESS BAROMETER indicated the breadth of expansion showed little change, and chalked up a ninth month of growth.The overall index declined to 59.1 from 59.7 (just below expectations). Note: any number above 50 shows expansion.

Employment improved to 54.2 after showing a decline (below 50) in May.

The new orders index declined again to 59.1 from 62.7. This is the lowest level this year.

The national ISM manufacturing index will be released tomorrow.

ADP: Private Employment increased 13,000 in June

by Calculated Risk on 6/30/2010 08:15:00 AM

ADP reports:

Nonfarm private employment increased 13,000 from May to June 2010 on a seasonally adjusted basis, according to the ADP National Employment Report®. The estimated change in employment from April to May 2010 was revised up slightly, from the previously reported increase of 55,000 to an increase of 57,000.Note: ADP is private nonfarm employment only (no government jobs).

June’s rise in private employment was the fifth consecutive monthly gain. However, over these five months the increases have averaged a modest 34,000. Recent ADP Report data suggest that, following steady improvement through April, private employment may have decelerated heading into the summer.

This is below the consensus forecast of ADP showing an increase of 60,000 private sector jobs in June.

The BLS reports on Friday, and the consensus is for a decrease of 100,000 payroll jobs in June, on a seasonally adjusted (SA) basis, with the loss of around 250,000 temporary Census 2010 jobs (+150,000 ex-Census).