RSS Feed

RSS Feed by Anonymous on 12/07/2007 09:53:00 AM

Friday, December 07, 2007

Subprime ARM Initial Rates

There were a number of comments yesterday about the nitty gritty mechanics of subprime ARMs (the ones likely subject to the Freeze Now Plan). I have therefore prepared one of my badly-formatted childish-looking charts (you want nice visuals, you read my co-blogger's posts).

Note that interest only (IO) is not nearly as ubiquitous in subprime as in Alt-A and prime; only a quarter of these loans have an IO feature. I don't have a breakdown (on unreset outstandings) for the term of the IO feature. It does vary; the IO period can be the same as the initial fixed rate period, or it can be longer than that. The loans that have the IO period expiring at the first rate adjustment are the real "exploding ARMs," since that means there's a double-whammy: the rate goes up, and the payment is amortized over the remaining term all at the same time. There are at least some of these loans that have IO terms of ten years (meaning that during the first ten years of the loan the rate can change, but the borrower is still paying interest only.)

I assume that in most cases, a servicer who is "freezing" the start rate for some period of time is also extending the IO period, if necessary, for the same period of time. If the idea is that the borrower just can't take any payment increase, it wouldn't help much to forgo the rate adjustment but hit the borrower with amortization. There might, of course, be borrowers who could afford to begin amortization, but only at the start rate. Don't ask me what will happen for "fast track modifications," because frankly I can't tell. If I figure it out, I'll let you know.

At any rate, the vast majority of subprime ARMs are amortizing from the start, and the vast majority are also 2/28s, meaning that the initial rate is fixed for two years, followed by adjustments every 6 months for the next 28 years (unless and until the loan hits its maximum lifetime interest rate). There is a substantial minority of 3/27s and a handful of 5/25s.

The term "teaser rate" is very relative, and as I've noted before, in the context of subprime "teaser" doesn't mean "low" relative to prime or Alt-A product. As you can see, these loans have very large margins--the average for the 2/28 is 6.00%. On the assumption that the index value (the index is the 6-month LIBOR for all of these loans) at the time of origination was in the vicinity of 5.00%, that means that the "fully-indexed" rate at origination was around 11.00%. Therefore a start rate of 8.00% is "discounted" or, in popular terminology, a "teaser." That doesn't make it a fabulous deal; it means that the fully-indexed rate is ugly. (Compare to prime ARMs of the same vintage: they probably had a margin of 2.50%, or a fully-indexed value of 7.50%, and a discounted initial rate of 5.50-6.50%.)

The way ARM adjustments work, at the change date the current value of the index is determined and is added to the margin. That gives you "fully indexed." That raw number is compared to the sum of the start (initial) rate plus the cap that is specified in the note for the first adjustment. The lower of the two numbers (possibly rounded) gives you the actual adjusted rate.

I used the December 1, 2007 6-month LIBOR value of 4.8265 here to arrive at average adjusted rates for these loans. If you want to know how low LIBOR would have to go for these loans to stay at their start rate at the first adjustment, just subtract the margin from the start rate. For instance, for the plain 2/28s, the biggest bucket, the average start rate is 8.00% and the average margin is 6.05%. Therefore, the loan rate will increase at the first adjustment as long as LIBOR is greater than 1.95%.

It is not likely that the rates on any of these loans would go down, even if LIBOR dropped under 1.95%. That is because subprime ARMs (unlike prime ARMs) usually have a rate floor: they just never get lower than the start rate, regardless of what the index does. (Fannie and Freddie, by the way, will not under any circumstances buy an ARM with a rate floor. It is truly a subprime thing.)

All a "rate freeze" as such does is keep the loan at the current (initial) rate for some period of time. A servicer could make the "freeze" permanent; that would simply turn an ARM into a fixed-rate loan. It appears that the Hope Now Plan involves something less than a permanent freeze; the ASF document indicates that the "fast track" mod involves extending the intial rate out up to another five years from the original first adjustment date. That would mean a loan originally made as a 2/28 ARM becomes a 7/23 ARM. It is possible that the servicer can also extend the maturity on these loans--making them, say, a 7/33 ARM by pushing the maturity date out ten years, but I see no mention of this in the "fast track" part. So that would have to be one of those "case by case" things. I doubt this maturity extension would be very common; the deal documents for a lot of these securities depend on having all the loans paid in full by the original 30-year maturity date (or sooner), and as far as I can tell this whole plan is about not messing with the deal documents.

To sum up, then, a borrower who gets a five-year extension of the intital rate simply continues to pay under the other (unmodified) contractual terms. If the loan was amortizing from the beginning, the borrower simply continues to make an amortizing payment at the start rate. If the loan had an IO period that ended at the original first change date, then the borrower will start making amortizing payments at the initial rate, unless the servicer extends the IO term to match the new extended first rate change date. If the loan had an IO period of 10 years, then the borrower will continue to make IO payments at the start rate until the extended first change date.

Some folks seem to think that this means that the "forgone" interest is somehow carried over or tacked onto the loan. It isn't. This "freeze" thing is simply a matter of postponing the first contractual adjustment date on these loans. I'm guessing that the Option ARMs (which are a whole nuther subject) are confusing everyone. There is nothing in the Hope Later Plan that involves capitalizing the "forgone" interest. I am putting "forgone" interest in quotation marks because some people seem to think that there is "additional" interest that these borrowers would still owe under the freeze. There isn't. If you do not raise the borrower's contractual interest rate, the borrower doesn't owe you more interest than he is currently paying. The freeze plan is not creating negative amortization ARMs here. The rate at which interest accrues is the rate at which interest is paid for these loans (whether only interest is paid, or principal and interest is paid).

I hope that clears it up. If not, I'll be hiding under my desk if you need me . . .

November Employment Report

by Calculated Risk on 12/07/2007 08:30:00 AM

From MarketWatch: Payrolls up 94,000; jobless rate stays at 4.7% on household survey gains

The economy added 94,000 nonfarm payroll jobs last month, according to a survey of business establishments, the Labor Department said in a mixed report released Friday.

...

Goods-producing industries cut 33,000 jobs in November, including 24,000 in construction and 11,000 in manufacturing.

Services-producing industries added 127,000 jobs. Financial services cut 20,000 jobs.

Thursday, December 06, 2007

From AAA to Worthless in Less than a Year

by Calculated Risk on 12/06/2007 11:19:00 PM

Note: If you are looking for a discussion of the Mortgage Freeze plan, see Tanta's The Plan: My Initial Reaction

First, here is a great graphical explanation of a CDO from Felix Salmon at Portfolio.com: What's a C.D.O.?

Now back to the Adams Square Funding liquidation. Thanks to jck for sending me the prospectus for the deal. Here are the notes:

U.S.$48,000,000 CLASS A SENIOR FLOATING RATE NOTES DUE DECEMBER 2051And here were the initial ratings:

U.S.$51,000,000 CLASS B-1 SENIOR FLOATING RATE NOTES DUE DECEMBER 2051

U.S.$10,000,000 CLASS B-2 SENIOR FLOATING RATE NOTES DUE DECEMBER 2051

U.S.$15,250,000 CLASS C FLOATING RATE DEFERRABLE NOTES DUE DECEMBER 2051

U.S.$16,000,000 CLASS D FLOATING RATE DEFERRABLE NOTES DUE DECEMBER 2051

U.S.$5,000,000 CLASS E FLOATING RATE DEFERRABLE NOTES DUE DECEMBER 2051

U.S.$20,000,000 SUBORDINATED NOTES DUE DECEMBER 2051

Adams Square Funding I, Ltd. (the “Issuer”) will issue the Notes referenced above on or about December 15, 2006 ...

It is a condition of the issuance of the Notes on the Closing Date that (a) the Class A Notes be rated “Aaa” by Moody’s Investors Service, Inc. (“Moody’s”) and “AAA” by Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. (“S&P”), respectively, (b) the Class B-1 Notes be rated at least “Aa2” and “AA” by Moody’s and S&P, respectively, (c) the Class B-2 Notes be rated at least “Aa3” and “AA-” by Moody’s and S&P, respectively, (d) the Class C Notes be rated at least “A2” and “A” by Moody’s and S&P, respectively, (e) the Class D Notes be rated at least “Baa2” and “BBB” by Moody’s and S&P, respectively, and (f) the Class E Notes be rated at least “Ba1” and “BB+” by Moody’s and S&P, respectively. The Subordinated Notes will not be rated.All of the above notes are worthless, including the AAA rated (by S&P) Class A notes.

Even the $342 million in Super Senior notes were impaired. As S&P noted yesterday: "proceeds will not be sufficient to cover the funded portion of the super-senior swap in full and that no proceeds will be available for distribution to the class A, B, C, D, or E notes."

From AAA to worthless in less than a year.

Rabobank bails out SIV, "model is dead"

by Calculated Risk on 12/06/2007 10:23:00 PM

From the Financial Times: Rabobank bails out SIV

Rabobank on Thursday ... bail[ed] out a troubled structured investment vehicle ... The Dutch bank plans to take assets worth €5.2bn ($7.6bn) on to its balance sheet to prevent a fire sale of Tango Finance.Memo to Paulson and Citigroup: SIVs are dead.

The bank, which manages the SIV with Citigroup, has already sold almost half the vehicle’s assets because it could not find sufficient funding. ...

Eddie Villiers, responsible for European sales at Rabobank, said: "The current SIV business model is dead and so there is no prospect of its survival in its current form."

“Our decision has been made purely for liquidity reasons as the assets in the portfolio are of high quality, but there is no market for asset-backed commercial paper for SIVs. We have done this for reputational reasons as our exposure to the SIV is small,” Mr Villiers said.

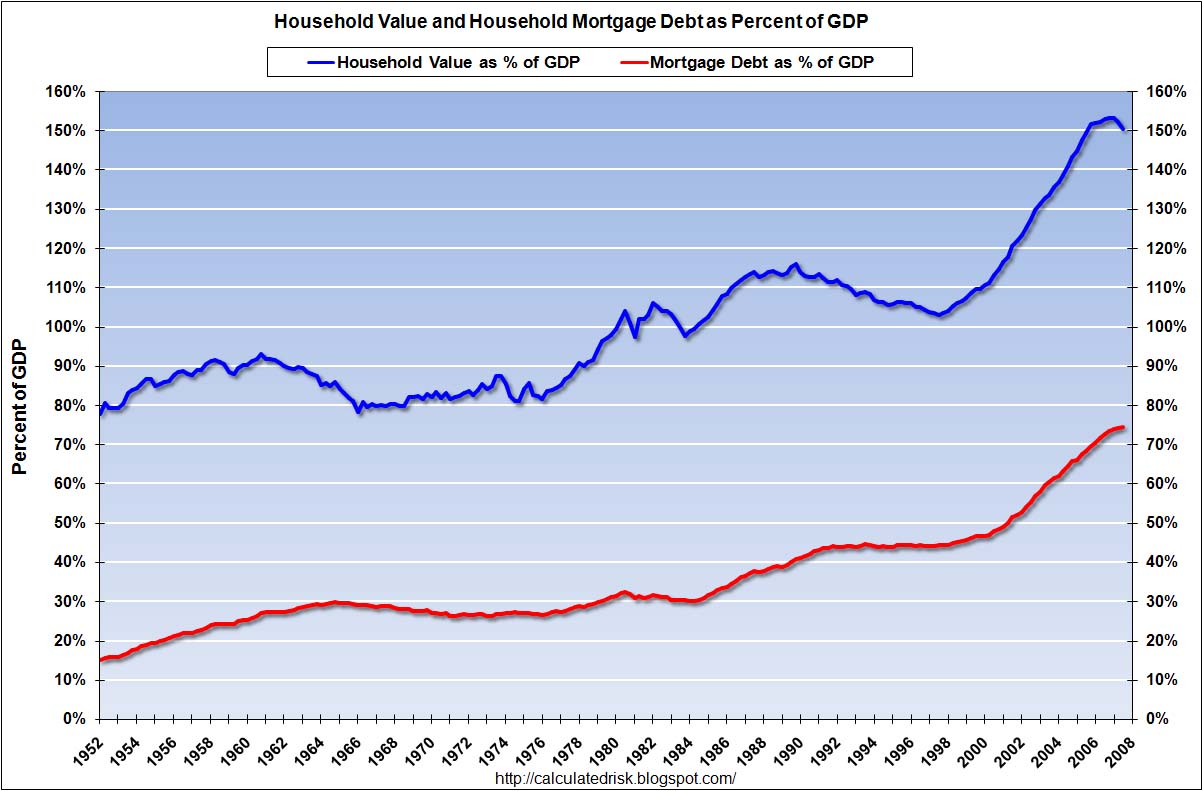

Fed: Existing Household Real Estate Assets Decline $67 Billion in Q3

by Calculated Risk on 12/06/2007 07:16:00 PM

Here is some more data from the Fed's Flow of Funds report.

The Fed report shows that household real estate assets increased from $20.94 Trillion in Q2 to $20.99 Trillion in Q3. However, when we subtract out new single family structure investment and residential improvement, the value of existing household real estate assets declined by $67 Billion.

The simple math: Increase in household assets: $20,991.18 Billion minus $20,937.62 Billion equals $53.56 Billion. Now subtract investment in new single family structures ($297.2 Billion Seasonally Adjusted Annual Rate) and improvements ($185.8 Billion SAAR). Note: to make it simple, divide the SAAR by 4.

Finally $53.56B minus $297.2B/4 minus $185.8B/4 equals a decline in existing assets of $67.2B. This was a quarterly price decline of about 0.3%, about the same as the OFHEO House Price index decline.

As mentioned earlier, household equity declined by $128 Billion in Q3.

Household debt increased by $182.1 Billion in Q3 (down from $213.6B in Q2, and up slightly from $181.48B in Q1 2007). The mortgage equity withdrawal numbers will probably still be fairly strong in Q3.

Household percent equity was at an all time low of 50.4%.

This graph shows homeowner percent equity since 1954. Even though prices have risen dramatically in recent years, the percent homeowner equity has fallen significantly (because of mortgage equity extraction 'MEW'). With prices now falling - and expected to continue to fall - the percent homeowner equity will probably decline rapidly in the coming quarters.

Also note that this percent equity includes all homeowners. Based on the methodology in this post, aggregate percent equity for households with a mortgage has fallen to 33% from 36% at the end of 2006.

If Goldman Sachs and Moody's are correct and house prices fall 15% nationally (30% in some areas), the value of existing household real estate assets will fall by $3 Trillion over the next few years.