RSS Feed

RSS Feed by Anonymous on 12/05/2007 08:07:00 AM

Wednesday, December 05, 2007

Cuomo Lifts Another Rock

And it will be interesting to see what crawls out from under this one:

NEW YORK (Reuters) - New York state prosecutors have sent subpoenas to Wall Street firms seeking information related to the packaging and selling of debt tied to high-risk mortgages, the Wall Street Journal reported, citing people familiar with the matter. . . .Well, well, well. I'm guessing there will be all kinds of interesting stuff on those potted plant reports. Somebody's aspidistra is going to be in a sling . . .

The probe appears to be examining the relationships between mortgage companies, third-party due-diligence firms, securities firms and credit-rating firms as they relate to the role securities firms played in the subprime mortgage crisis, the Journal said.

O.C. Register on CRE: Turn out the lights ...

by Calculated Risk on 12/05/2007 01:00:00 AM

"The party is over"From Jon Lansner at the O.C. Register: Commercial real estate ‘party is over’

Jerry Anderson, President, Irvine-based commercial real estate brokerage

Stan Ross, chair of USC Lusk Center for Real Estate ... said today that the nation likely will have a weaker economy next year, and “that spills over into the commercial sector.” Ross stopped short of predicting a commercial downturn. ...Historically non-residential investment in structures follows residential investment by between 3 and 8 quarters; with the normal lag of about 5 quarters. Based on this typical relationship, at the end of 2006 I started forecasting a slowdown in CRE at the end of '07.

Commercial real estate “will clearly be impacted” by a weaker economy, Ross said. “The question is how much and where and what products.”

...

Jerry Anderson, newly appointed president of Sperry Van Ness, an Irvine-based commercial real estate brokerage ... forecast an end to a 7-year-long boom, saying that “the party is over.” issued a prediction today that commercial real estate values will decrease by 10% to 12% next year. ... “It’s been a wild ride, but now it’s over.”

Click on graph for larger image.

Click on graph for larger image.Investment in non-residential structures continues to be very strong, increasing at a 14.3% annualized rate in Q3 2007.

This graph shows the YoY change in Residential Investment (shifted 5 quarters into the future) and investment in Non-residential Structures. In a typical cycle, non-residential investment follows residential investment, with a lag of about 5 quarters (although the lag can range from 3 to about 8 quarters). Residential investment has fallen significantly for six straight quarters. So, if this cycle follows the typical pattern, non-residential investment will start declining about now.

Due to the deep slump for CRE during the business led recession in 2001, CRE is nowhere near as overbuilt as residential - even though the CRE lending standards were very loose. Still, it appears there is a slowdown in non-residential investment starting now.

The second graph shows the YoY change in nonresidential structure investment (dark blue) vs. loan demand data (red) and CRE lending standards (green, inverted) from the Fed Loan survey.

The second graph shows the YoY change in nonresidential structure investment (dark blue) vs. loan demand data (red) and CRE lending standards (green, inverted) from the Fed Loan survey.The net percentage of respondents tightening lending standards for CRE has risen to 50%. (shown as negative 50% on graph).

The net percentage of respondents reporting stronger demand for CRE has fallen to negative 34.6%.

Loan demand (and changes in lending standards) lead CRE investment for an obvious reason - loans taken out today are the CRE investment in the future. This report from the Fed also suggests an imminent slowdown in CRE investment.

Data Source: Net Percentage of Domestic Respondents Reporting Stronger Demand for Commercial Real Estate Loans

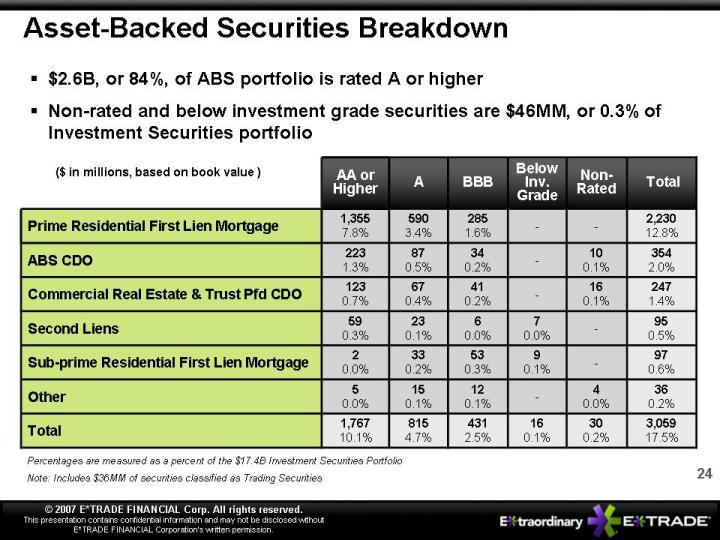

NYTimes on Those E*Trade ABS Haircuts

by Calculated Risk on 12/05/2007 12:01:00 AM

Kudos to Brian who caught this last Thursday: ETrade ABS Haircuts

From the NYTimes: In E*Trade Deal, Pain Went Far Beyond Subprime

... here is a point worth considering: Only about $450 million of E*Trade’s $3 billion portfolio was made up of the riskiest kinds of securities — C.D.O.’s and second-lien mortgages — that have made headlines recently.

What was the other $2.6 billion or so? In E*Trade’s own words, it was “other asset-backed securities, mainly securities backed by prime residential first-lien mortgages.”

In other words, E*Trade’s enormous haircut went far beyond subprime.

A large part of E*Trade’s basket of assets was securities backed by high-quality mortgages — loans to homeowners with strong credit ratings and reasonably large equity cushions. That could raise troubling questions on Wall Street about the true value of “prime” mortgage assets, especially when they need to be liquidated in a hurry.

The picture becomes clearer when you look at this breakdown, which E*Trade shared with investors in October. It shows that more than $1.35 billion of E*Trade’s asset-backed portfolio consisted of prime, first-lien residential mortgages rated “AA” or better — hardly toxic sludge by any stretch of the imagination.

So consider this: Even if E*Trade got nothing — not a cent — for anything but these top-quality mortgage securities, it still sold $1.35 billion in prime mortgage assets for $800 million, or less than 60 cents on the dollar.

That’s just a back-of-the-envelope calculation, but a potentially unnerving one.

Tuesday, December 04, 2007

Moody's: Loss Estimates for Alt-A Double

by Calculated Risk on 12/04/2007 05:15:00 PM

From Reuters: Subprime bond losses to climb to 20 pct -analysts (hat tip Cal)

Moody's Investors Service on Tuesday raised its forecast for expected losses for U.S. mortgages known as "Alt-A" residential mortgage debt. Loss estimates for Alt-A bonds reviewed by Moody's increased by an average of 110 percent from initial expectations, with some loss estimates up by as much as 270 percent, Moody's said in a report.Well, I'm stunned, but not surprised.

Fannie Mae Cuts Dividend, to Sell Preferred

by Calculated Risk on 12/04/2007 05:10:00 PM

From the WSJ: Fannie Looks to Raise $7 Billion, Cuts Common-Stock Dividend

... Fannie Mae said Tuesday that it planned to issue $7 billion in non-convertible preferred stock and cut its quarterly common stock dividend by 30% in an effort to boost capital and "conservatively manage increased risk in the housing and credit markets."Fannie does a Freddie.

{kind=link}