RSS Feed

RSS Feed by Calculated Risk on 12/05/2007 12:01:00 AM

Wednesday, December 05, 2007

NYTimes on Those E*Trade ABS Haircuts

Kudos to Brian who caught this last Thursday: ETrade ABS Haircuts

From the NYTimes: In E*Trade Deal, Pain Went Far Beyond Subprime

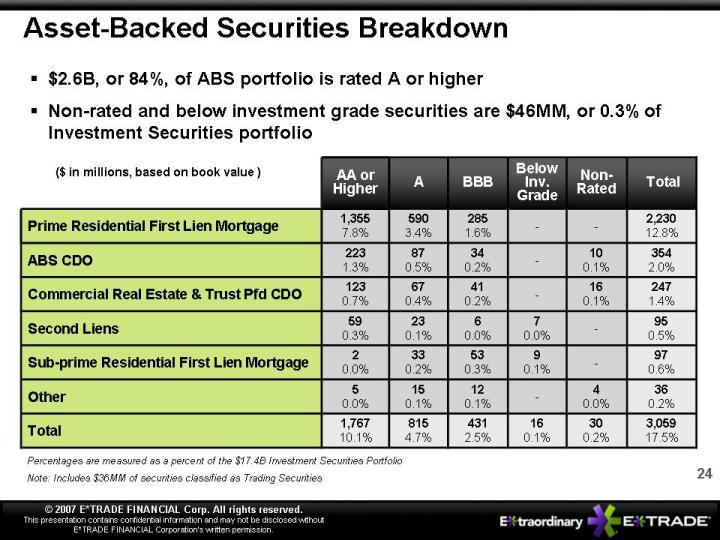

... here is a point worth considering: Only about $450 million of E*Trade’s $3 billion portfolio was made up of the riskiest kinds of securities — C.D.O.’s and second-lien mortgages — that have made headlines recently.

What was the other $2.6 billion or so? In E*Trade’s own words, it was “other asset-backed securities, mainly securities backed by prime residential first-lien mortgages.”

In other words, E*Trade’s enormous haircut went far beyond subprime.

A large part of E*Trade’s basket of assets was securities backed by high-quality mortgages — loans to homeowners with strong credit ratings and reasonably large equity cushions. That could raise troubling questions on Wall Street about the true value of “prime” mortgage assets, especially when they need to be liquidated in a hurry.

The picture becomes clearer when you look at this breakdown, which E*Trade shared with investors in October. It shows that more than $1.35 billion of E*Trade’s asset-backed portfolio consisted of prime, first-lien residential mortgages rated “AA” or better — hardly toxic sludge by any stretch of the imagination.

So consider this: Even if E*Trade got nothing — not a cent — for anything but these top-quality mortgage securities, it still sold $1.35 billion in prime mortgage assets for $800 million, or less than 60 cents on the dollar.

That’s just a back-of-the-envelope calculation, but a potentially unnerving one.

Tuesday, December 04, 2007

Moody's: Loss Estimates for Alt-A Double

by Calculated Risk on 12/04/2007 05:15:00 PM

From Reuters: Subprime bond losses to climb to 20 pct -analysts (hat tip Cal)

Moody's Investors Service on Tuesday raised its forecast for expected losses for U.S. mortgages known as "Alt-A" residential mortgage debt. Loss estimates for Alt-A bonds reviewed by Moody's increased by an average of 110 percent from initial expectations, with some loss estimates up by as much as 270 percent, Moody's said in a report.Well, I'm stunned, but not surprised.

Fannie Mae Cuts Dividend, to Sell Preferred

by Calculated Risk on 12/04/2007 05:10:00 PM

From the WSJ: Fannie Looks to Raise $7 Billion, Cuts Common-Stock Dividend

... Fannie Mae said Tuesday that it planned to issue $7 billion in non-convertible preferred stock and cut its quarterly common stock dividend by 30% in an effort to boost capital and "conservatively manage increased risk in the housing and credit markets."Fannie does a Freddie.

PricewaterhouseCoopers Forecast: CRE expected to Slow

by Calculated Risk on 12/04/2007 04:26:00 PM

Jon Lansner at the O.C. Register reports: Outlook dimmer for commercial real estate in 2008, forecast says

The boom that boosted commercial real estate ... is expected to slow in 2008 in the face of a slowing economy and a credit crunch ... according to the 29th annual forecast by PricewaterhouseCoopers and the Urban Land Institute.They could have just read this blog earlier this year!

...

A panel of local industry leaders noted that values for commercial properties in Orange County will decline next year from 3% to 15%, depending on the type and quality of the building. The panel provided the following outlooks for Orange County’s office, apartment, retail and housing markets:

...

William Flaherty, senior vice president for marketing, Maguire Properties Inc. on the office market: The outlook for the O.C. office market is cloudy, while a year or two ago it was incredibly bright. Today vacancies are under 10%, but they are expected to go up due to the collapse of many subprime lenders based here (New Century was a tenant of Maguire’s until it went bankrupt) and to new construction. Flaherty added that the global credit crunch has crunched demand and prices for office buildings, which had quickly traded hands at the start of 2007. “It’s clear that the world’s changed on Aug. 2 with the credit crunch,” he said.

Citi: Losses "greatly exceeded" Profits from Subprime

by Calculated Risk on 12/04/2007 03:45:00 PM

Here is an interesting question for the Wall Street firms: Was it worth it? Were the recent losses just a small price to pay for the outsized profits in previous years? Goldman and Deutsche Bank say yes, they made money. Citi says no.

From Bloomberg: Citi's Losses `Greatly Exceeded' Profits for Subprime

Citigroup Inc. ... lost more money than it made from financial instruments based on U.S. subprime mortgages, a senior company executive said in a meeting at the British Parliament.

...

``Our losses greatly exceeded the profits we made in this field over several years,'' Mills said at a hearing of the Treasury Committee today.

...

Gerald Corrigan, the managing director in charge of risk management at Goldman Sachs Group Inc., said that his bank had fared better than Citi.

``On balance, we probably made money,'' Corrigan told lawmakers. ``We have had a measure of success in hedging some of our exposure.''

...

Deutsche Bank probably made more money from marketing CDOs than it lost, said Charles Aldington, chairman of its London unit.

{kind=link}