RSS Feed

RSS Feed by Calculated Risk on 2/07/2006 12:16:00 PM

Tuesday, February 07, 2006

Housing: PLEASE Buy this house

The Pioneer Press offers a few cautionary tales: Sellers juggle mortgages in tough market

[Bonnie] Cordy and her husband moved to Tennessee last year for his job. They rented an apartment until their new $325,000 house was ready in June. All the while they were making a mortgage payment in Minnesota.

The Apple Valley town home they'd originally listed at $329,900 in December 2004 wasn't selling, even after they dropped the price more than $20,000.

"I felt nervous as we were finishing up the house down here," she said. "There was no way to swing it all."

They dipped into retirement savings for the month or two they had double mortgage payments and taxes.

Then they switched to another agent, who slashed the price another $30,000. It finally sold at the end of August for $291,900, which was about $35,000 less than what they paid in 2003. She figures they lost another $5,000 in retirement savings.

"It's money we'll never get back again," said Cordy, 48.

Monday, February 06, 2006

National Debt: $10 Trillion When Bush Leaves Office

by Calculated Risk on 2/06/2006 03:39:00 PM

Today Bush submitted a budget for fiscal 2007 projecting a budget deficit of over $600 Billion. From AP:

The administration in its budget documents said the deficit for this year will soar to an all-time high of $423 billion, reflecting increased outlays for the Iraq war and hurricane relief.The article is referring to the Enron style unified budget deficit. The on-budget or General Fund deficit will be approximately $200 Billion more reflecting the surplus from Social Security Insurance. This means the projected General Fund deficit for 2007 will be over $600 Billion.

National Debt

The current National Debt is $8.195 Trillion. At $600 Billion per year, the Bush Administration will add $1.8 Trillion to the National Debt over the next 3 years. That will put the National Debt at approximately $10 Trillion when Bush leaves office - a stunning legacy.

Friday, February 03, 2006

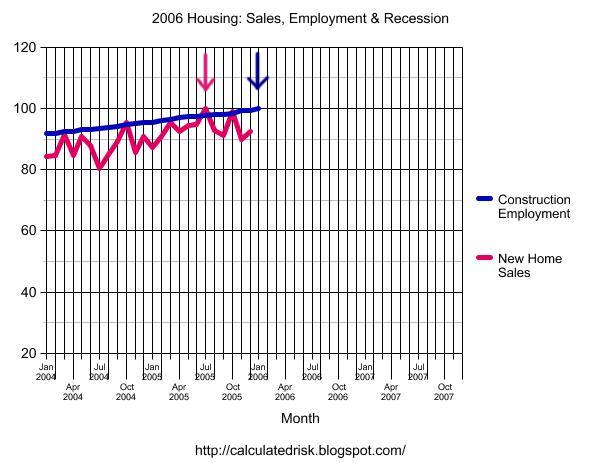

Housing: Sales, Employment and Recessions

by Calculated Risk on 2/03/2006 09:06:00 PM

Today's BLS employment report once again showed strong gains for construction employment. Dr. Kash noted this in his post: Job Growth by Industry

"Interestingly, construction employment still seems to be growing robustly, despite some concerns that the real estate market is cooling off; 46,000 of the new jobs created last month were in construction."Here is a look back at the last consumer recession (1990-1991):

Click on graph for larger image.

NOTE: New Home Sales and Construction employment were normalized to 100 for each peak (see arrows). The '90/'91 recession is in gray according to the NBER dates.

New Home Sales peaked in July of 1989 and construction employment peaked six months later in January of 1990. The recession started in July of 1990.

The 2nd graph is looking at the current situation. It appears New Home Sales peaked in July 2005, although October 2005 was very close. It might take a few more months and a few revisions to determine the actual peak.

If the peak did occur in July 2005, then January 2006 would be six months later - a similar lag in employment just like the early '90s. Of course, no two slowdowns are exactly alike.

So far the housing market is following a predictable pattern: rising inventories followed by a decrease in transactions and finally falling prices (like the early '90s in California, Massachusetts and other bubble areas). Housing related employment lags the peak in housing sales.

There are other factors that make the current situation more dangerous: a larger area of "frothy" prices, more leverage and use of exotic loans, and far more equity withdrawal (that supported consumer spending). On the other hand, in the early '90s, there was a huge shift away from defense work (the "peace dividend") and that impacted both California and Massachusetts.

I'll be watching construction employment over the next few months, and I expect to see a reduction in housing related employment.

ISM Report

by Calculated Risk on 2/03/2006 02:50:00 PM

Institute for Supply Management reports: Business Activity at 56.8%.

"Non-manufacturing business activity increased for the 34th consecutive month in January," Kauffman said. He added, "Business Activity and New Orders increased at slower rates in January than in December. Imports, Employment and New Export Orders also increased at slower rates while Prices increased at the same rate as in December. Eight of 16 non-manufacturing industry sectors report increased activity in January compared to 11 that reported increased activity in December. While in almost all indexes growth declined in January, they are still above the value of "50" indicating that growth continues, but at slower rates of growth. Members' comments in January continue to be generally positive concerning current business conditions. Several members mention concerns about the continued high level of energy prices and rising interest rates. The Prices Index held steady this month, but remains in a historically high range for the ISM Non-Manufacturing Business Survey. The overall indication in January is continued economic growth in the non-manufacturing sector, but at slower rates of increase."The weakest industries were: Agriculture; Wholesale Trade; Real Estate; Retail Trade; and Construction. This might be a hint of the housing slowdown, although the BLS numbers showed construction employment was solid in January.

Some of the details are interesting:

| Index | Jan. | Dec. | Change | Direction | Rate |

| Business Activity / Production | 56.8 | 61.0 | -4.2 | Increasing | slower |

| New Orders | 56.0 | 62.2 | -6.2 | Increasing | Slower |

| Employment | 51.1 | 56.9 | -5.8 | Increasing | Slower |

| Supplier Deliveries | 54.5 | 56.5 | -2.0 | Slowing | Slower |

| Inventories | 55.0 | 56.0 | -1.0 | Increasing | Slower |

| Prices | 67.2 | 67.2 | 0 | Increasing | At same rate |

| Backlog of Orders | 52.5 | 54.0 | -1.5 | Increasing | Slower |

| New Export Orders | 58.0 | 61.5 | -3.5 | Increasing | Slower |

| Imports | 49.5 | 56.5 | -7.0 | Decreasing | From Increasing |

| Inventory Sentiment | 63.0 | 59.0 | +4.0 | "Too High" | Greater |

Many activities are still increasing, but at a slower rate than in December. Employment is barely increasing (51.1) and prices are perceived to be a problem. Inventory sentiment is to too high and increasing at a greater rate. And imports are now decreasing (slightly). All signs that the expansion may be past its peak.

Employment Report

by Calculated Risk on 2/03/2006 01:32:00 PM

The employment report was mostly ho hum. The exception was the drop in the unemployment rate to 4.7%.

Click on graph for larger image.

This graph shows employment growth for Bush's second term. So far job growth has been about as expected. So why has the unemployment rate decreased?

The answer has to do with the employment participation rate. Over the last 5 years, the civilian noninstitutional population has added about 2.7 million people per year (those 16 years and over). Over the last 12 months the population has added 2.716 million - in line with previous years.

However, over the last 5 years, only about 1.2 million people per year have joined the civilian labor force. This is very puzzling, especially since it is unlikely that the baby boomers are retiring in significant numbers yet. More likely there is a fairly large group of people that would choose to join the labor force with higher incentives. Therefore I think, even with a 4.7% unemployment rate, there is still substantial slack in the labor market and the US will not see wage inflation pressures in the short term.

Once again, construction played a significant role in employment gains. For more, see Kash's Job Growth by Industry.