RSS Feed

RSS Feed by Calculated Risk on 12/21/2005 10:38:00 AM

Wednesday, December 21, 2005

MBA: Mortgage Application Volume Down

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Down In Latest Survey

The Market Composite Index — a measure of mortgage loan application volume was 594.6 -- a decrease of 4.0 percent on a seasonally adjusted basis from 619.3 one week earlier. On an unadjusted basis, the Index decreased 5.2 percent compared with the previous week and was down 15.2 percent compared with the same week one year earlier.

The seasonally-adjusted Purchase Index decreased by 5.2 percent to 453.1 from 477.9 the previous week, whereas the Refinance Index decreased by 1.6 percent to 1418.1 from 1441.8 one week earlier.

Click on graph for larger image.

The graph shows overall and purchase activity since June. Overall activity has fallen significantly due to the drop in refis.

Mortgage rates decreased slightly again last week:

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.22 percent from 6.28 percent on week earlier ...Overall this report shows purchase activity might be weakening, but it is still at a very high level.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 5.76 percent from 5.83 percent ...

Tuesday, December 20, 2005

New Proposed Guidance on Nontraditional Mortgage Products

by Calculated Risk on 12/20/2005 01:28:00 PM

From the FDIC: Federal Financial Regulatory Agencies Propose Guidance on Nontraditional Mortgage Products

UPDATE: I think this paragraph has the most teeth:

Collateral-Dependent Loans – Institutions should avoid the use of loan terms and underwriting practices that may result in the borrower having to rely on the sale or refinancing of the property once amortization begins. Loans to borrowers who do not demonstrate the capacity to repay, as structured, from sources other than the collateral pledged are generally considered unsafe and unsound. Institutions determined to be originating collateral-dependent mortgage loans, may be subject to criticism, corrective action, and higher capital requirements.This is essentially a warning not to rely on the value of the property to bail out the home buyer. The teeth are "criticism, corrective action, and higher capital requirements.", with the higher capital requirements being the only significant penalty.

The Press Release:

The federal financial regulatory agencies today issued for comment proposed guidance on residential mortgage products that allow borrowers to defer repayment of principal and sometimes interest.Interagency Guidance on Nontraditional Mortgage Products

These nontraditional mortgage products include "interest-only" mortgage loans where a borrower pays no principal for the first few years of the loan and "payment option" adjustable-rate mortgages where a borrower has flexible payment options, including the potential for negative amortization. Institutions are also increasingly combining these mortgages with other practices, such as making simultaneous second-lien mortgages and allowing reduced documentation in evaluating the applicant’s creditworthiness.

While innovations in mortgage lending can benefit some consumers, the agencies are concerned that these practices can present unique risks that institutions must appropriately manage. They are also concerned that these products and practices are being offered to a wider spectrum of borrowers, including subprime borrowers and others who may not otherwise qualify for more traditional mortgage loans or who may not fully understand the associated risks of nontraditional mortgages.

The proposed guidance discusses the importance of carefully managing the potential heightened risk levels created by these loans. Toward that end, management should:

* Assess a borrower’s ability to repay the loan, including any balances added through negative amortization, at the fully indexed rate that would apply after the introductory period. The agencies recognize that this requirement differs from underwriting standards at some institutions and are specifically requesting comment on this aspect of the guidance.

* Recognize that certain nontraditional mortgage loans are untested in a stressed environment and warrant strong risk management standards as well as appropriate capital and loan loss reserves.

* Ensure that borrowers have sufficient information to clearly understand loan terms and associated risks prior to making a product or payment choice.

Comment is requested on all aspects of the guidance, particularly on the section regarding comprehensive debt service qualification standards. Comments are due sixty days after publication in the Federal Registrar. The guidance is attached.

Monday, December 19, 2005

Real Estate: Is the party over?

by Calculated Risk on 12/19/2005 08:52:00 PM

CNN Money asks: Is the party over?

The article includes "exclusive forecasts" for the 100 largest markets.

... the overall outlook seems reasonable: 7 percent appreciation for 2006 and flat for 2007. But markets that have seen the greatest appreciation over the past five years appear to be vulnerable.Check out the table at the bottom of the article. I think some of these projections are a little optimistic. Will San Antonio home prices increase 15% over the next two years? Will Boston stay flat, even with 8+ months supply (and growing)?

Indeed, at some point in the next two years, according to the forecast, a third of the nation's 100 largest metro areas (accounting for 60 percent of the U.S. population) are expected to see modestly falling house prices.

Real estate bear markets often come in the form of steady declines over many years, rather than sudden sharp drops.

As inflation gradually gnaws away at the value of nominal home prices, regular folks might not take much notice. But in the long run the loss of wealth becomes all too real. From 1989 to 1997, for instance, Los Angeles residential real estate dropped more than 40 percent in inflation-adjusted terms.

The nation's most perilous regional market, according to the forecast data: Las Vegas, a speculator-infested hot spot. Prices there are projected to deflate by 7.9 percent next year, the year after by another 5 percent. For newcomers to the market and those with low-money-down deals who may have overleveraged themselves with adjustable-rate mortgages, even a modest downturn could mean financial jeopardy.

Home Builders Confidence Falls

by Calculated Risk on 12/19/2005 03:13:00 PM

Please see Angry Bear for National Association of Home Builders HMI excerpts and links to historical tables.

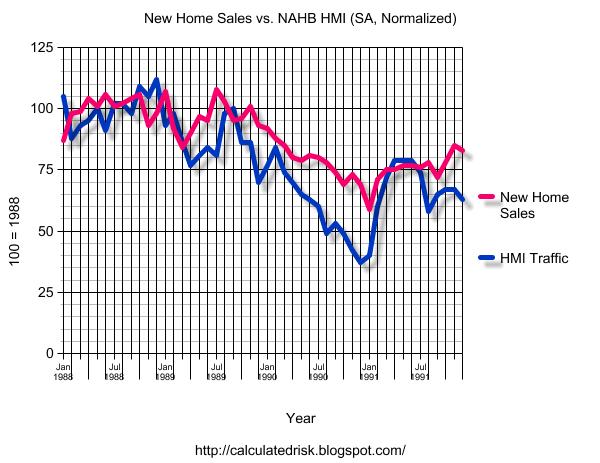

Click on graph for larger image.

This graph shows New Home Sales vs. the NAHB traffic index from 1988 to 1991. Both series are seasonally adjusted and are normalized to 1988 = 100.

It appears that the NAHB index was generally a coincident indicator for New Home Sales in the previous housing slowdown.

With the fall in the NAHB HMI, I expect a similar fall in New Home Sales on Friday.

Sunday, December 18, 2005

Comments on End of Housing Boom

by Calculated Risk on 12/18/2005 03:40:00 PM

From Knight Ridder: Boom likely over in housing market. The article contains comments from FDIC Chief Economist Richard Brown and Federal Reserve Bank of Chicago Senior Economist Richard Rosen.

...homeowners will no longer be able to use houses as piggybanks, cashing in on gains in appreciation periodically through low-cost refinancings. And many will be forced to hold on to a house or condominium for a long time as they wait for prices to rise.And from Federal Reserve Bank of Chicago Senior Economist Richard Rosen:

The problem is that rising mortgage rates are putting an end to the easy money that underpinned increasing home prices, said Richard Brown, chief economist of the Federal Deposit Insurance Corp. in Washington.

"Price increases have far outstripped income growth for a long time, particularly in the last two years, but that period is coming to an end," he said.

The so-called golden age for mortgage lending is about over after lasting about 20 years, he said.

"The end of the boom probably is not far away," Brown said. "It likely will lead to a long period of price stagnation, but not technically a bust."

Home prices "have been rising far more rapidly than rents for the last four years. This probably is what Federal Reserve Chairman Alan Greenspan meant when he pointed to froth in the housing market," said economist Richard Rosen of the Federal Reserve Bank of Chicago.Note: this article was orginally published on Dec 9th.

He said a huge drop in long-term mortgage rates since 1985, when they were around 12 percent, to a recent rate near 5 percent "meant that you could afford more house for the same monthly payment."

Rosen compared the United States with Britain, where mortgage rates have been rising for about two years. Here, the uptick in rates began later.

"In Britain, if housing was a bubble, it didn’t burst," he said. "When mortgage rates rise, prices flatten, but they may not actually decrease."

One warning sign for the housing market, Rosen said, is that more and more owners are putting property on the market, and real estate is taking longer to sell.

"The risk is that if sales slow, there will be too much supply, creating price risk," he said.