RSS Feed

RSS Feed by Calculated Risk on 11/08/2005 10:53:00 AM

Tuesday, November 08, 2005

Toll Brothers Warns

AP reports: Toll Brothers Cuts 2006 Home Deliveries View; Sees Weakened Demand in Some Markets

Toll Brothers Inc. cut its home deliveries forecast for fiscal 2006 on Tuesday, citing fewer than expected selling communities and weakened demand in several markets. Shares of the luxury home builder tumbled more than 11 percent in morning trading.

Toll Brothers projected home deliveries between 9,500 and 10,200 homes in fiscal year 2006, down from an earlier target of 10,200 to 10,600 homes. In fiscal 2005 it reported 8,769 deliveries.

"The shortage of selling communities, coupled with some softening of demand in a number of markets, negatively impacted our contract results," Toll Brothers said. "It appears we may be entering a period of more moderate home price increases, more typical of the past decade than the past two years."

Monday, November 07, 2005

Leaving California

by Calculated Risk on 11/07/2005 12:58:00 AM

My most recent post is up on Angry Bear: Will Boston Lead the Housing Bust?

Also, one of my friends is leaving California to take a job in Indiana. He currently lives in the Inland Empire and had a choice of living in Orange County or Indiana. The price of housing was the determining factor.

Apparently this is becoming more common - from the NY Times: Saying Goodbye California Sun, Hello Midwest

A growing number of people are leaving California after a decade of soaring home prices, according to separate data from the Census Bureau, the Internal Revenue Service and the state's finance department.

Last year, a half million people left California for other parts of the United States, while fewer than 400,000 Americans moved there. The net outflow has risen fivefold, to more than 100,000, since 2001, an analysis by Economy.com, a research company, shows, although immigration from other countries and births have kept the state's population growing.

The number of people leaving Boston, New York and Washington is also rising, and skyrocketing house prices appear to be a major reason, said Mark Zandi, chief economist at Economy.com. From New York, the net migration to Philadelphia more than doubled between 2001 and 2004, with 11,500 more people leaving New York for Philadelphia last year than vice versa. The number of New Yorkers who have moved to Albany, Charlotte, N.C., and Allentown, Pa., among other places, has also increased sharply.

Friday, November 04, 2005

Interest on the National Debt

by Calculated Risk on 11/04/2005 05:49:00 PM

The average weighted interest rate on the National Debt will most likely rise in fiscal 2006. For fiscal 2005 (ended Sept 30th), the average interest rate was 4.6%. The rate rose to 4.74% in October.

Click on graph for larger image.

With continued heavy borrowing, a significant amount of debt due to rollover in early 2006, and rising interest rates, the weighted average rate will probably rise to 5% or more for fiscal 2006.

NOTE: 2006 is estimated at 5%.

The implications for the budget deficit are serious. The National Debt has increased substantially in recent years, while interest rates have been falling. This has kept the debt service payments in the low to mid $300 Billion range.

Now that interest rates are rising, the additional interest payments will add significantly to the General Fund deficit. A small increase to 5% of the weighted average interest rate will add $59 Billion to the fiscal 2006 General Fund deficit compared to fiscal 2005 debt service.

NOTE: Graph shows an estimated fiscal 2006 interest payment of $411 Billion.

Debt service is part of the reason I believe the National Debt will increase by a record $650 Billion in fiscal 2006. The US set an October record debt increase of $94.4 Billion - well on the way to an annual record.

October Jobs Report

by Calculated Risk on 11/04/2005 11:24:00 AM

The BLS released the Emploment Situation Summary this morning.

On Housing: Kash has some interesting comments on construction employment at Angry Bear: Disappointing Job Growth Here are some stats for October: Total jobs added: 56K.

1.8K .... Residential building

20.0K .. Residential specialty trade contractors

5.4K ... Depository credit intermediation (includes mortgage brokers)

3.3K ... Real estate

Total RE related = 30.5K

Previous economic releases have shown that construction spending and new home starts are still rising. This employment report is further confirmation that the building boom is continuing, even though the housing market appears to be slowing.

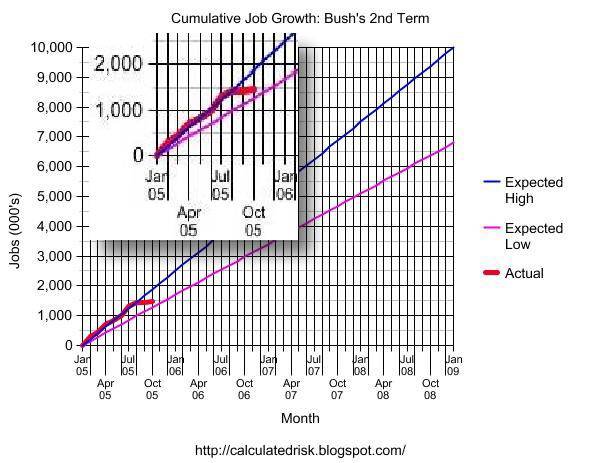

On overall employment: Bush's first term, with a net loss of 759K private sector jobs (a gain of 119K total jobs), was a disappointment. For Bush's 2nd term, anything less than 6.8 Million net jobs will have to be considered poor. And anything above 10 million net jobs as excellent. Of course, in additional to the number of jobs, the quality of the jobs and real wage increases are also important measures.

Click on graph for larger image.

For the quantity of jobs, this graph provides a measurement tool for job growth during Bush's 2nd term.

The blue line is for 10 million jobs created during Bush's 2nd term; the purple line for 6.8 million jobs.

The insert shows net job creation for the first 9 months of the 2nd term - the last three months have moved job creation towards the lower end of the acceptable range.

Bernanke and Asset Bubbles

by Calculated Risk on 11/04/2005 01:23:00 AM

From the New York Times article: To Fight Rising Prices, Fed Nominee May Need New Weapons

Mr. Bernanke ... has also asserted, like Mr. Greenspan, that he does not intend to use interest rates prematurely to puncture an asset bubble. But he has signaled a readiness to use a different set of tools to fight the new inflation, and in this he departs from Mr. Greenspan.I believe tighter lending requirements would have minimized the housing bubble. Of course its too late this time.

What lifts asset prices, Mr. Bernanke and others argue, is the willingness of lenders to offer riskier types of loans, which "juice up the housing market and are not very responsive to interest rates," as Mark Zandi, chief economist at the research firm Economy.com, put it.

Lenders can engage in riskier loans because they have developed techniques in recent years that make it far easier for them to shed their vulnerability to risk, doing so mainly by shifting the risk of default to others. The lenders operate in sophisticated markets that allow thousands of individual investors to purchase a slice of the original loan, and a slice of the risk.

In the past, the danger of default as rates rose tended to discourage lenders from making overly risky loans. The lender, often a bank, kept the loan and bore all the risk. Mr. Bernanke, in response to the risk shifting, has raised the possibility of limiting the dangers through the use of regulations - microregulatory policy, he calls it.

"There are two ways to approach bubbles: one is interest rate policy, the other is microregulatory policy," he said in a little noted interview published last year by the Federal Reserve Bank of Minneapolis. "Microregulatory policy is the much better approach, in my view," Mr. Bernanke said.

Pursuing his point, he added: "Research on historical episodes suggests that large asset price increases are sometimes preceded by credit booms. In many cases, this pattern results from the fact that the country in question deregulated its banking system, giving banks extra powers, but did not enhance the supervisory structure adequately at the same time."