RSS Feed

RSS Feed by Calculated Risk on 11/03/2005 05:47:00 PM

Thursday, November 03, 2005

More Evidence of a Housing Slowdown

From TheStreet.com: Zip Realty Warns

"It is important to appreciate that our fourth quarter and preliminary 2006 guidance is being provided in the context of what we believe to be a transitioning market, slowly shifting the advantage from sellers to buyers," said CEO Eric Danziger. "Evidence of this shift is seen in rapidly rising inventory levels in September and slightly declining median selling prices across our markets for the past two months." emphasis addedAnd from DataQuick:

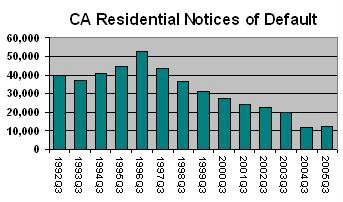

California Foreclosures Edge Up

Foreclosure activity in California showed a year-over-year increase during the last quarter for the first time in more than three years, the result of lower appreciation rates and riskier loans...Just more evidence of a slowing housing market.

"Current foreclosure levels are extremely low and this increase is a step towards more normal activity. Foreclosures decline when home prices go up. As home appreciation rates come down, we expect the foreclosure numbers to go up. They could double by the end of 2006," said Marshall Prentice, DataQuick president.

Mortgage lenders see profits shrink

by Calculated Risk on 11/03/2005 12:32:00 PM

The OC Register reports: Mortgage lenders see profits shrink

Rising interest rates are hitting mortgage lenders in the wallet.And this "difficult environment" will probably hit employment soon:

The owner of Irvine-based Option One Mortgage Corp. on Wednesday joined a chorus of profit-starved lenders. H&R Block,best known for its tax services, says its profit may be trimmed due to costlier mortgage making.

H&R Block CEO Mark Ernst told analysts Wednesday that profits may be at the low end of analysts' expectations because of increased borrowing expenses for its mortgage unit. He said rising short-term interest rates create "a difficult environment for anybody in this industry."

Lenders and related businesses added 15,000 workers - a 42 percent jump - in the past four years. One in four jobs created in [Orange County, CA] since 2001 have been in lending-related fields.And "lending-related fields" are only a portion of the jobs directly related to the housing boom; other home related employment would include RE agents, construction, home inspectors and escrow officers.

And some interesting tidbits from the article:

But many lenders' profits are now shrinking. For example, Los Angeles-based lender and mortgage investor Aames said Wednesday that its pre-tax net interest margin - the gap between what it lends money at and the costs to acquire those funds - shrank to 2.12 percent in the third quarter from 2.39 percent in the previous three months.

...

Mortgage bankers made $4trillion in mortgages in 2003, a banner year. While business in the past two years has been exceptional - twice the annual average in the 1990s - it is expected to fall off some 18 percent in 2006 from 2005's projected $2.78 trillion, according to the Mortgage Bankers Association.

...

According to the National Association of Realtors, buyers were spending close to 21 cents out of every $1 earned on monthly mortgage payments during the second quarter of 2005. The group's housing affordability index - a measure of consumers' ability to make monthly mortgage payments started in 1970 - was at a low during the second quarter of 2005 not seen since 1991.

...

Roughly three-quarters of Orange County's homebuyers use adjustable-rate mortgages that help borrowers qualify for bigger loans.

...

Prashant Kothari, president of String Information Services, estimates that as much as $300 billion in adjustable-rate mortgages could be refinanced nationwide next year and $1trillion in 2007.

Wednesday, November 02, 2005

MBA: Mortgage Activity Continues to Fall

by Calculated Risk on 11/02/2005 10:32:00 AM

The Mortgage Bankers Association (MBA) released its weekly survey today:

The Market Composite Index — a measure of mortgage loan application volume – was 646.7, a decrease of 4.8 percent on a seasonally adjusted basis from 679.1, one week earlier. On an unadjusted basis, the Index decreased 5.2 percent compared with the previous week but was down 15.2 percent compared with the same week one year earlier.

...

"The seasonally adjusted purchase index is down 7.6 percent since last month. This decline is consistent with our expectations of a softening from the record level of new home sales during the first three quarters of 2005," said Doug Duncan, Chief Economist for the Mortgage Bankers Association.

Click on graph for larger image.

This graph show the seasonally adjusted MBA Market and Purchase indices since the beginning of July. The market index has been steadily declining for several months, mostly reflecting a slowing in refinance activity.

The purchase index had stayed steady, reflecting the continued strength in new and existing homes sales. Over the last month, the Purchase index has started to fall, probably indicating slowing home sales (these numbers are seasonally adjusted).

Mortgage interest rates continued to rise:

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.21 percent from 6.06 percent on[e] week earlier...First we saw rising inventories, now it appears we are seeing more signs of falling activity. Next I would expect to see prices flatten out or even start to decline.

The average contract interest rate for 15-year fixed-rate mortgages increased to 5.75 percent from 5.57 percent...

The average contract interest rate for one-year ARMs increased to 5.39 percent from 5.37 percent one week earlier...

USA Today: Overheated housing market is cooling off

by Calculated Risk on 11/02/2005 12:37:00 AM

The USA Today reports: Overheated housing market is cooling off

...there's nervous chatter about the recent increase in the number of homes for sale, sellers cutting their asking prices and builders wooing buyers with incentives.The USA Today article covers familiar ground and adds these anecdotes:

The reason: There are signs that the overheated market might finally be cooling. The Commerce Department, for example, said sales of new homes in September fell shy of expectations, median prices declined 5.7%, and the number of new homes for sale shot up to a record 493,000. Freddie Mac also said October mortgage applications seem to be "tapering off."

• Ricardo Cortazar, a Realtor in Tempe, Ariz., says it now takes 35 days, on average, to sell a home. Six months ago, it took a week. Inventory in Arizona has swelled to 15,000 homes, vs. 6,000 in May.The housing market does appear to be slowing.

• Vaughn Bryan, a real estate agent in San Bernardino County, has spotted another ominous trend: a rise in the number of 90-day listing contracts that expire without a sale.

• Dan Elsea, a Detroit Realtor, says it's common for sellers in the job-starved Motor City to reduce asking prices two, three or four times before signing a deal.

• Kelly Haslam of Madison, Wis., hasn't been able to sell her bungalow-style home despite putting it up for sale "by owner" seven weeks ago, hosting four open houses and dropping her price once.

• Judi Keenholtz, CEO of Empire Realty, which serves San Francisco's East Bay, says desirable homes in good school districts that used to fetch eight to 10 bids now get three or four.

Tuesday, November 01, 2005

Fiscal 2006: A Record October

by Calculated Risk on 11/01/2005 02:57:00 PM

Fiscal 2006 is off to a poor start as the increase in the National Debt set a record for the month of October. The National Debt increased $94.4 Billion to $8.027 Trillion as of Oct 31, 2005.

Click on graph for larger image.

The previous record for October was in 2003 (fiscal 2004) when spending for the Iraq war lead to an increase in the National Debt of $89.4 Billion. This October was negatively impacted by spending related to hurricanes Katrina and Rita.

Each month I will plot the YTD increase in the National Debt and compare it to the proceeding years. Even without the hurricane spending, I expect fiscal 2006 to set a new record for National Debt accumulation.