RSS Feed

RSS Feed by Calculated Risk on 9/27/2005 01:49:00 AM

Tuesday, September 27, 2005

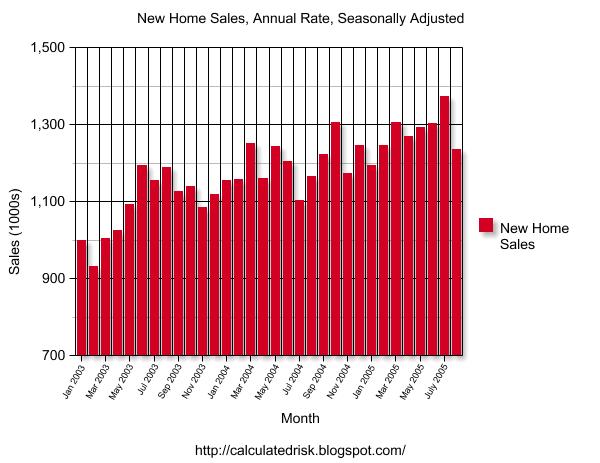

August New Home Sales: 1.237 Million

According to a Census Bureau report, New Home Sales in August were at a seasonally adjusted annual rate of 1.237 million vs. market expectations of 1.345 million. July sales were revised down to 1.373 million from 1.41 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in August 2005 were at a seasonally adjusted annual rate of 1,237,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

The Not Seasonally Adjusted monthly rate was 106,000 New Homes sold, down from a revised 118,000 in July.

The median sales price of new houses sold in August 2005 was $220,300; the average sales price was $283,400.

Both the average and median sales price rebounded.

The seasonally adjusted estimate of new houses for sale at the end of August was 479,000. This represents a supply of 4.7 months at the current sales rate.

The seasonally adjusted supply of New Homes was 4.7 months, a significant increase from recent months.

With the usually caveat that one month does not make a trend, this report shows a significant downturn in the New Home Sales market. Sales were off. Inventories were up. Revisions were negative.

This may be the beginning of the end for this housing cycle.

Monday, September 26, 2005

WSJ: Greenspan Warns of Reliance on Housing Loans

by Calculated Risk on 9/26/2005 09:51:00 PM

Greg Ip writes at the WSJ:

]"Federal Reserve Chairman Alan Greenspan, drawing on new research he has personally supervised, said American consumers have become enormously dependent on borrowing against their homes to fuel their spending, and that a rise in mortgage rates could trigger a spending pullback.

Mr. Greenspan's new data show that borrowing against home values added a stunning $600 billion to consumers' spending power last year, equivalent to 7% of personal disposable income -- compared with 3% in 2000 and 1% in 1994.

...

That reversal need not be "disruptive," Mr. Greenspan said. Indeed, he suggested that such a reversal would bring about a needed rise in U.S. saving and a narrower trade deficit. But he also sounded new warnings about speculation in the housing market, focusing on rising sales of second homes, though also playing down the threat of overleveraged homebuyers.

Mr. Greenspan's remarks were among his most extensive to date on the scope and risks of the rise in housing prices and mortgage debt in the past decade, developments to which his own policies have contributed. The remarks suggest that while in the near term higher energy prices may be the greatest threat to consumers, in the longer term Mr. Greenspan sees a cooling housing market as potentially more significant.

Last year's estimate of the value of "home equity extraction," as Mr. Greenspan calls it, was double the value of President Bush's tax cuts, as estimated by Brookings Institution scholar Peter Orszag. It's unclear how much of that home-financed borrowing was spent on goods and services, but Mr. Greenspan suggested it was about half.

...

Mr. Greenspan also repeated his warnings on the increased popularity of some exotic mortgages, which expose the borrower to a greater risk of rising rates or declining home prices.

...

Mr. Greenspan believes this home-equity extraction has been a powerful channel of support to the economy in recent years. Indeed, he believes it's how the Fed's low interest rates propped up the economy after the stock bubble burst in 2001. While the Fed has raised short-term interest rates since last summer, long-term mortgage rates, which are set by bond investors, have stayed surprisingly low. Thus, home-equity extraction has fueled consumer spending longer than Mr. Greenspan thought likely ...

Greenspan on Housing

by Calculated Risk on 9/26/2005 04:26:00 PM

Bloomberg reports: Greenspan Says Speculation Having 'Greater Role' in Home Prices

Sales of vacation houses, or homes that aren't always occupied by owners, are "arguably at historically unprecedented levels," Greenspan said in the text of his remarks to the American Bankers Association annual convention in Palm Desert, California. "This suggests that speculative activity may have had a greater role in generating the recent price increases than it customarily has had in the past."MarketWatch adds: Greenspan weighs in on home prices, Drops may not be fatal, even as housing fuels spending

A new study, co-authored by Greenspan, has found that about four-fifths of the rise in home-mortgage debt has been due to homeowners taking some cash out of the rise in their property's value.Here is the Greenspan study (PDF): Estimates of Home Mortgage Originations, Repayments, and Debt on One-to-Four-Family Residences

"It is difficult to dismiss the conclusion that a significant amount of consumption is driven by capital gains on some combination of both stocks and residences," Greenspan said.

As a result, consumer spending would decline if mortgage rates rise and home turnover and opportunities for mortgage refinancing cash-outs decline, he added.

There also would be some positive developments, as the personal savings rate would likely rise, and the trade deficit would narrow given the likely drop in imports of consumer goods.

"How significant and disruptive such adjustments turn out to be is an open question," Greenspan said.

A few comments: 80% of the increase in mortgage debt "has been due to homeowners taking some cash out". That is a huge amount. If cash refis were cut in half for the last year, GDP would have been flat and if there were no cash out refis, GDP would have declined 3.1%. (Update: assuming cash out goes to consumption) And that is just the direct impact and does not include any secondary effects of layoffs in the housing and retail industries.

I do agree with Greenspan's comment: it is difficult to predict how disruptive the coming adjustment will be, but a recession is likely.

Existing Homes: Sales Strong, Inventories Rise

by Calculated Risk on 9/26/2005 10:44:00 AM

CBS reports: Existing Home Sales Hit 2nd Highest Level

The National Association of Realtors reported Monday that sales of existing homes rose 2 percent in August to a seasonally adjusted annual rate of 7.29 million units, a sales pace that was exceeded only by an all-time high of 7.35 million units in June.Inventories increased from 2,759,000 in July to 2,856,000 in August. This is about what I expected. Existing Home Sales are a trailing indicator and are mostly sales in June and July. Tomorrow's New Home Sales is more interesting and might show the first signs of a slowing housing market.

...

The strong demand pushed prices up to a record level of $220,000 last month, a gain of 15.8 percent from August 2004. That was the biggest 12-month increase since a 17.2 percent increase in July 1979.

...

While the Realtors predicted that Hurricane Katrina, which came ashore in New Orleans in late August, would impact sales in September, they said the impact in August appeared to be minimal.

This and that ...

by Calculated Risk on 9/26/2005 12:03:00 AM

My most recent post is up on Angry Bear: Housing: Buy or Rent?

The inherent problem with the buy vs. rent calculation is estimating the future value of the house. As long as prices are going to continue to appreciate, it doesn't matter what you pay for the house. But when appreciation stops; price matters!

A couple of posts I recommend:

Dr. Duy's Fed Watch: Dejá Not A great series on trying to read the FED's mind.

"I continue to think that Greenspan & Co. are sending increasingly not-so-subtle messages that the days of low interest rates and easy policy are at their end. This is a message for Congress and the Administration, not just the financial markets. Indeed, something unexpected may be happening – a concerted effort to end any sense of a Greenspan-put in the markets or the economy as a whole. It will undoubtedly be interesting to watch this chapter in Fed history play out."Responding to supply shocks Dr. Hamilton cautions about future FED Funds increases, at least until the full impact of Katrina can be assessed.

UPDATE: Two more on the FED:

Macroblog: Funds Rate Probabilities: Keep On Truckin' *AT Least One More Time)

And Dr. Polley asks some questions: Differing opinions on the Fed

I'll throw out these questions to the blogosphere: What are the dangers of a pause in the rate hikes? What are the chances that the market would misinterpret it and see it as a signal that the Fed is done raising rates or that they see recession on the horizon? If you were on the FOMC, what would you do between now and the end of the year to minimize that risk? Do you think that these risks would cause the Fed not to want to pause at all, but treat "measured pace" as meaning 25 b.p. per meeting until they feel they're at the neutral funds rate? Would that be good policy?Best to all.