RSS Feed

RSS Feed by Calculated Risk on 8/18/2005 02:11:00 PM

Thursday, August 18, 2005

EDAB/UCLA July Report

Economic Development Alliance for Business (EDAB) presents a monthly economic report for the East Bay (Northern California). Christopher Thornberg, Senior Economist for UCLA Anderson Forecast is the author. A few excerpts:

(Hat tip to Brian Smits who sent me this report)

"... unfortunately there is a big problem brewing out there that is unlikely to go away quietly: the massive run-up in real estate prices across the state. Housing prices have continued to grow at a truly spectacular rate across the state and again in the Bay Area. Rampant speculation continues to fuel the fire as investors have seemingly already forgotten the lessons learned so hard in the last major asset bubble that ended not even five years ago. While there are those who try and rationalize the rapid increase in prices, we see no justification for these increases—the fundamentals that drive the price of a housing asset have been pointing to a cool market, not a hot one. Rental growth remains weak, mortgage rates have been rising slowly, and contrary to common belief the pace of home building in the area is completely in line with the growth of the workforce—the so-called housing shortage does not exist. Yes, inventory levels are low but this is due to frantic behavior of buyers."But Thornberg believes the economic problems are a year away:

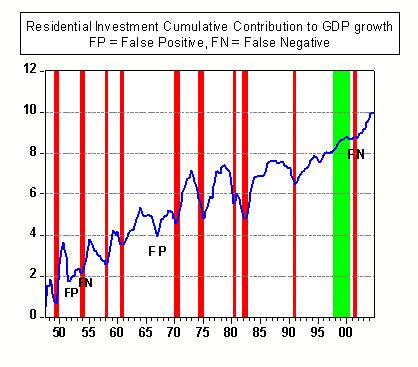

"There are some preliminary data that show what may be the beginning of the cooling of the market. But a major slowdown is at least a year away, if not more. Expect the recovery to continue well into 2006 and job growth in the East Bay to pick up speed during these 12 months. The end of 2006 or early 2007 will be the beginning of trouble, however."Thornberg presents the following graph showing that housing slowdowns have preceded eight of the 10 recessions since WWII.

Click on graph for larger image.

New Home Sales is one of my favorite leading indicators. Here are a couple of posts: New Home Sales as Leading Indicator and Update: New Home Sales as Leading Indicator.

I'm looking for a drop in housing transaction as an indicator of an economic slowdown and possible recession in '06. Thornberg also thinks its too early to predict a recession and compares the late '80s slump (leading to the early '90s recession) to today.

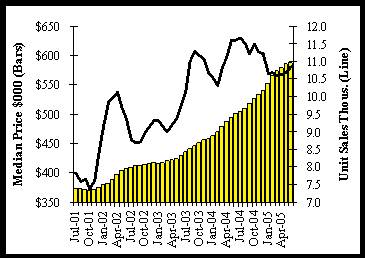

"The ... chart shows unit sales and median prices at the end of the late eighties run-up in prices. Market activity peaked in the end of 1988, and price appreciation began to slow within 6 months, and stopped within 18. So keep an eye on market activity, since this will be the first sign of impending problems. More recently unit sales have begun to fall, and you can see some slowdown in price appreciation. This may not be completely convincing evidence since you can see a similar slowdown in 2002 that quickly reversed itself. Of course this time prices are higher and more out of whack relative to income, and interest rates are rising rather than falling. This makes it considerably more likely to be the beginning of the end."

"... as of now the bubble continues to expand. And while there are certainly signs that we are past the peak in this state, activity remains at a historically high pace. There is almost no chance of a major economic slowdown in the next 12 months for the nation ..."There is much more in the report.

Homeowners Debt: "45% of Income not Uncommon"

by Calculated Risk on 8/18/2005 11:24:00 AM

The Mercury News reports: Home buyers get comfy with debt.

One out of five recent buyers have committed more than half their total earnings to homeownership, according to a new study. Slightly over half of home buyers in the past two years spend more than 30 percent of their total income on housing, exceeding a level recommended by the U.S. Department of Housing and Urban Development.If I remember correctly, the limits for borrowers with perfect credit were approximately 33% of income for housing and 40% of income for total debt not long ago. Now one in five of recent buyers are over 50% just for housing. That seems like extremely loose lending practices.

Because the study was based on data from 2003 and 2004, the situation now can only be worse because home prices have continued to rise dramatically since then.

The Public Policy Institute of California, in a study released today, reports that Californians are strategizing and willing to be house poor as never before.Here is the PPIC report: California's Newest Homeowners: Affording the Unaffordable

...

They've been helped by low interest rates and lenient lenders. But more than anything, their success in buying homes results from being inventive and ready to spend an awful lot of their earnings on owning a home.

Port of Los Angeles: Imports Up 5% over June

by Calculated Risk on 8/18/2005 12:46:00 AM

The Port of Los Angeles released their July statistics today. Inbound (loaded containers) was 352 thousand compared to 334 thousand in June - an increase of 5%.

Outbound volume was 97.5 thousand loaded containers vs. 96.6 thousand for June. This is an 1% increase from June.

Port of Long Beach traffic indicated a slight decline in imports for July. Looking at both numbers, I expect imports from China to be flat or off slightly from June to July.

NOTE: The OffPeak initiative (adds late night hours to port operations) started on July 23rd to handle the expected heavier late summer / fall imports.

Wednesday, August 17, 2005

Freddie Mac: Cash-Out Volume Prime Conventional Loans

by Calculated Risk on 8/17/2005 11:26:00 PM

Here is a table of the cash out volumes (according to Freddie Mac) since 1993 (note numbers don't exactly match earlier post - these are the revised numbers):

| YEAR | Equity Extraction | Equity Extraction |

| Billions ($) | Plus 2nd/Heloc $B | |

| 1993 | $19.9 | $39.3 |

| 1994 | $13.8 | $29.2 |

| 1995 | $11.2 | $21.7 |

| 1996 | $17.4 | $34.5 |

| 1997 | $21.4 | $39.1 |

| 1998 | $39.9 | $72.4 |

| 1999 | $37.0 | $71.1 |

| 2000 | $26.2 | $60.4 |

| 2001 | $82.9 | $135.5 |

| 2002 | $111.1 | $170.5 |

| 2003 | $146.9 | $224.4 |

| 2004 | $139.6 | $182.0 |

| 2005(est) | $161.7 | $200.0 |

| 2006(forecast) | $68.7 | $93.6 |

Freddie Mac reports that equity extraction was $102 Billion for the first 6 months of 2005 (they estimate $161.7B for the year).

Some of the surge in the late '90s was attributed at the time to borrowing to invest in the NASDAQ stock bubble. People were concerned by the large jump in equity extraction, especially in '98 and '99. Seems inconsequential now.

The projected drop off next year (of $100 Billion) is approximately 0.8% of GDP (GDP will be over $12 Trillion in '06).

DiMartino:Housing froth still bubbling

by Calculated Risk on 8/17/2005 09:47:00 PM

Danielle DiMartino surveys this week's housing stories for the Dallas Morning News: First the National Association of Home Builders survey:

The housing market index of the National Association of Home Builders declined three points to 67 in August.On the FED and lending standards:

...

"This relationship suggests to us that the purchases of new homes could turn soft in the near term," Northern Trust economist Asha Bangalore wrote recently.

... the Federal Reserve's latest Senior Loan Officer Opinion Survey, it was apparent that, as the Bank Credit Analyst put it, "The Fed speaks but banks don't hear it."And on the Housing ATM:

A quick history lesson: In the past, bankers tightened up lending standards to match the degree of Fed tightening.

"This makes sense, because rising rates boost the odds of loan defaults," the BCA noted. "This time, banks are ignoring the Fed. The new survey shows an increasing willingness to make consumer loans."

...fresh news out of mortgage giant Freddie Mac on Americans' insatiable appetite for cash to fuel their runaway spending habits.... Thanks more to increasing home values than interest rates, in the first half of this year, cash-out refinancings have totaled a record $102 billion.And from Freddie Mac:

Total equity cashed out in the second quarter is estimated at $59 billion, up from the revised cash-out estimate for the first quarter of 2005 of $43 billion.Home Equity Extraction:

... homeowners extracted $140 billion in home equity through first lien refinances in 2004."

2001: $83 Billion

2002: $96 Billion

2003: $139 Billion

2004: $140 Billion

2005: $102 Billion (first 6 months)

From former Fed chief Paul Volcker (quotes and video link - worth a repeat):

"Altogether, the circumstances seem as dangerous and intractable as I can remember."

"Boomers are spending like there is no tomorrow."

"Homeownership has become a vehicle for borrowing and leveraging as much as a source of financial security."