RSS Feed

RSS Feed by Calculated Risk on 3/15/2005 09:46:00 AM

Tuesday, March 15, 2005

UCLA Anderson Forecast: False Sense of Wealth

2nd UPDATE: Another good article with more quotes and facts from the Anderson Forecast:

From 2001 to 2004, the value of California's 7 million homes has increased by about $175,000 per home, resulting in a total rise of more than $1.2 trillion according to UCLA Anderson Forecast. Appreciation of apartments has added an additional $440 billion.And on the Central Valley:

"To put this in context, the personal income for the state was $4.7 trillion over the same period of time," the forecast states. "Hence, Californians have been essentially given a 30 percent-plus boost to their annual incomes due to the housing bubble we are currently experiencing."

The forecast is especially ominous for the central San Joaquin Valley, where the building boom has fueled some of the strongest job growth in the state. Of the 3,900 net new nonfarm jobs created in Fresno County last year, for instance, 2,100 were created in construction, an amount 3 1/2 times greater than that added in manufacturing, according to state jobs data.

UPDATE: A couple more quotes:

“This year we are expecting trouble with housing in the second half that will make GDP growth a little weaker than normal, but it (is) unlikely that a recession could get started that quickly without more telltale signs today,” [UCLA Anderson Forecast Director Edward] Leamer’s report said.ORIGINAL POST:

“The key here is that at best the state economy can be expected to maintain slow growth over the next few years as the weak housing sector saps off strength created in other parts of the state’s recovering external economy,” the report stated. “On the other hand, a sudden rise in interest rates or some other spark that could cause the housing sector bubble to implode at a faster rate could instead cause another recession, both in California and the U.S.”

This morning, at a UCLA conference, forecasters will caution on the impact of a Real Estate slowdown on California and the Nation. From an LA Times article:

Half of the private-sector jobs created in California in the last two years are connected in some way to real estate. Meanwhile, property values in the last four years have swelled $1.7 trillion, the equivalent of about 35% of the total personal income in the state since 2001.

This sharp increase in home equity has spurred consumer spending that, in turn, has fueled more economic growth.

"We have an economy that's rolling along on the basis of a false sense of wealth," said Christopher Thornberg, a senior economist with the Anderson Forecast team.

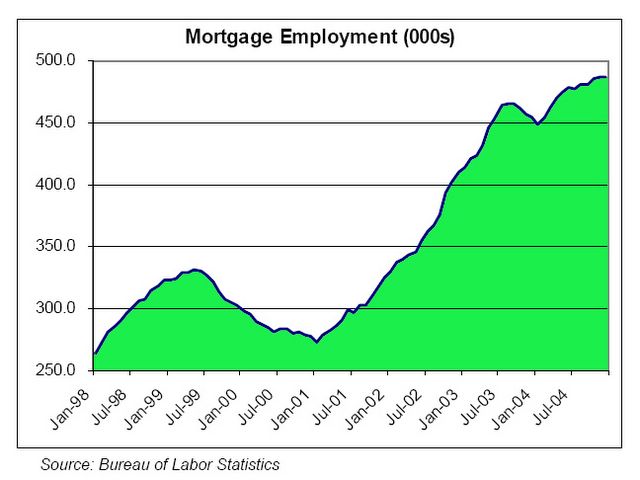

In a previous post, I discussed the impact of a housing slowdown on employment. The following graph shows the growth in employment in just one housing related area: mortgage employment.

We see that we have added 200K jobs in the mortgage industry alone in under 4 years. The mean salary (according to the BLS in 2001) was $45,380 for the mortgage industry.

Click on graph for larger image.

Graph thanks to ild and Elroy.

Another example: Just 2 years ago, there were 338,579 licensed RE Agents (brokers and salespeople) in California. Now, according to the Department of Real Estate, there are 423,315 licensees.

More from the article:

Thornberg said that in California, where home prices have increased faster than in the rest of the nation, the situation is precarious. Even a simple slowdown in the accumulation of equity in the state, he said, could harshly depress spending habits, job creation and economic expansion.

Real estate has become central to California's economy. Real estate-related jobs account for about 10% of private sector jobs in the state, according to the Anderson Forecast, and are growing rapidly.

Of the 243,000 private payroll jobs added in California since 2003, 122,000 are linked to the industry — jobs with construction companies, mortgage processing centers and the like.

And Thornberg's final comment: "The best-case scenario is mediocre."

Monday, March 14, 2005

Mortgage Debt and the Trade Deficit

by Calculated Risk on 3/14/2005 09:02:00 PM

Money flowing into the housing market works its way back into the economy by increasing consumption or savings (and investment). In recent years, aggregate savings have declined, therefore it appears money has flowed to consumption, both domestic (measured by the increase in GDP) and imports (measured by the increase in the trade deficit).

This is very simplistic but provides a general description of what I believe is happening. I will use the annual increase in mortgage debt as a measure of the money flowing into the economy from housing activities.

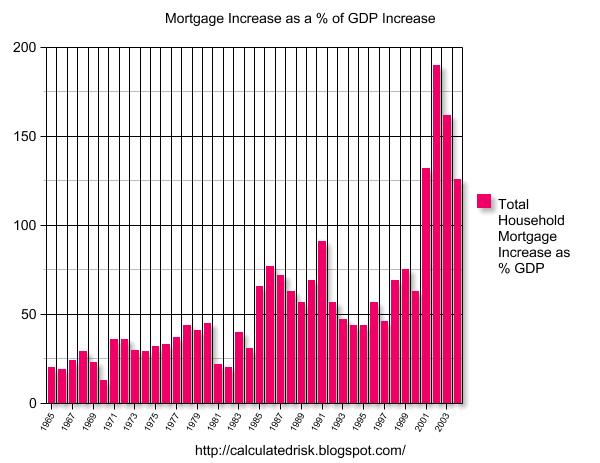

Previously I posted a graph of the annual Increase in Mortgage Debt vs. the Increase in GDP. The graph illustrated that during each of the preceding four years, U.S. households had assumed more mortgage debt than the increase in nominal GDP. I was asked if there were any other periods of similar increases in mortgage debt. The answer is NO, at least not in the last 40 years, as shown by the following graph:

The last four years have been atypical. There has been a surge in mortgage borrowing that far exceeded nominal GDP growth. It is unclear how much of GDP growth was driven by the increase in mortgage debt. However, since I believe most of the mortgage debt has flowed to consumption (not savings or investment); the portion that didn’t contribute to GDP growth must have flowed to imports.

Click on graph for larger image.

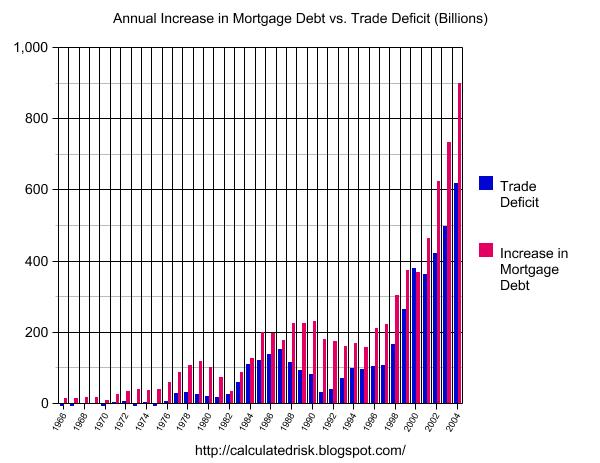

From the following chart it appears that the increase in mortgage debt is a factor in the increased trade deficit. The chart shows the annual trade deficit compared to the annual increase in mortgage debt. Data sources: trade deficit, GDP, New Home Sales, Mortgage Debt. There is a strong correlation between increases in mortgage debt and increases in the trade deficit. Although the correlation is high, it is very possible that there is no direct linkage, instead the same economic causes that led to higher trade deficits also led to more household borrowing. However, in recent years, with the dramatic increases in mortgage borrowing (far exceeding the increases in GDP) it is reasonable to expect that some of that money is flowing to imports.

There is a strong correlation between increases in mortgage debt and increases in the trade deficit. Although the correlation is high, it is very possible that there is no direct linkage, instead the same economic causes that led to higher trade deficits also led to more household borrowing. However, in recent years, with the dramatic increases in mortgage borrowing (far exceeding the increases in GDP) it is reasonable to expect that some of that money is flowing to imports.

The implications are important: if the housing market slows down, it will negatively impact both the domestic economy and the economies of our export driven trading partners: China, Japan, S. Korea and others.

The concern is obvious: If we slide into a global recession, we have limited tools available to stimulate the economy. Interest rates are already very low (although the Fed has recently put some arrows back into the quiver), and we are already running general fund budget deficits of close to 6% of GDP. And the concerns are not just economic. Historically, poor economic conditions are the precursors to civil unrest and wars.

One thing is certain, mortgages and housing play a much larger role in today's economy than in the past. In another recent post, I had suggested that the volume of New Home Sales seemed like a reasonable leading indicator of the consumer economy. The following graph shows New Home Sales since 1963.

The gray lines are approximate U.S. economic recessions as determined by NBER. With the exceptions of the 2001 (non-consumer recession) and '69-'70 recessions, New Home Sales were falling for 8 to 12 months prior to the onset of the recession. Since housing is a significantly larger portion of the economy today, a slowdown in housing would have a corresponding larger impact on the overall economy.

That is why I’m so focused on the housing market. I would like to see an orderly rebalancing of the World's economy, but I am not sanguine.

Friday, March 11, 2005

China Reduces Dollars in Its Reserves, Lehman Says

by Calculated Risk on 3/11/2005 01:39:00 AM

According to a Bloomberg article based on a Lehman report, China has "cut the share of its currency reserves held in dollars and raised its holdings of euros".

Lehman also predicts China will allow the yuan to fluctuate by the end of June.

First, in late February, Korea was rumored to be diversifying "the currencies in which it invests".

Then, two days ago, Japanese Prime Minister Junichiro Koizumi said his country ``in general'' needs to consider diversifying its foreign currency reserves.

Now China.

Thursday, March 10, 2005

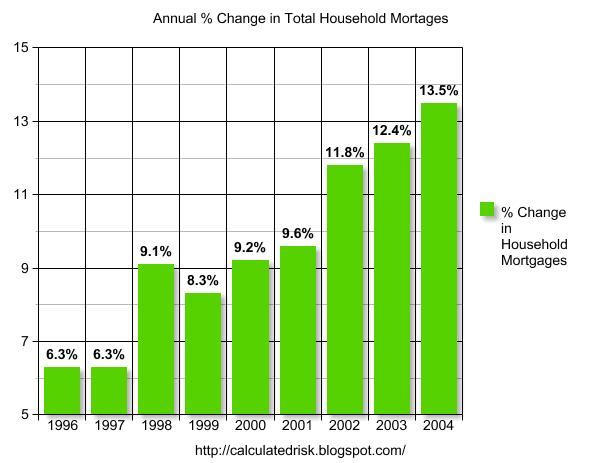

Mortgage Debt Increases 13% in 2004

by Calculated Risk on 3/10/2005 11:47:00 PM

Today the Federal Reserve released the "Flow of Funds Accounts" for 2004. The report shows that total household mortgage debt increased 13.5% in 2004. The following chart shows the annual rate of mortgage debt increase:

Click on graphs for larger image.

The rate of increase of mortgage debt has increased every year since 1999.

Household mortgage debt increased from $6.64 Trillion in 2003 to $7.54 Trillion in 2004.

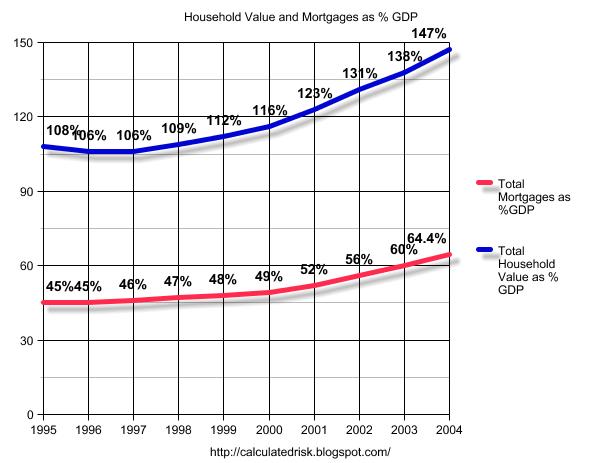

The next graph shows the Fed's estimate of the market value of all household real estate and household mortgage debt as a % of GDP.

Although mortgage debt has shown a substantial increase as a % of GDP (almost 20% over the last decade), the estimated value of household Real Estate has also increased substantially.

The appreciating value of household RE has kept the debt to value ratio under 50% based on the Fed's estimates.

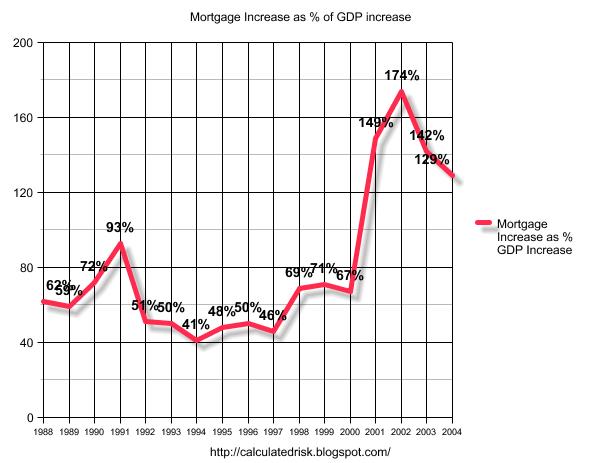

The final graph compares the annual increase in mortgage debt to the annual increase in GDP. This shows the impact of mortgage debt on GDP.

The economy was in recession for part of 2001, so it is not surprising that mortgage debt exceeded GDP growth for that year.

However, it is surprising that mortgage debt has substantially exceeded GDP growth for four consecutive years.

This lends credence to the idea that the American consumers are maintaining their lifestyles using their homes as ATMs. Please see these previous posts that expound on this supposition:

Mortgage Debt and the "Recovery"

A Recovery Built on a Marshland of Debt?

Volcker: Circumstances "dangerous and intractable"

The Other Trust Funds

by Calculated Risk on 3/10/2005 03:02:00 PM

With all of the attention on Social Security (OASI), perhaps we should also look at some of the other trust funds. As an example, the CSRS (Civil Service Retirement System) is similar to OASI program. CSRS is a defined benefit plan that uses contributions from today's employees to pay today's retirees. And like OASI, CSRS is running annual surpluses; $28 Billion in fiscal 2003. SOURCE: Monthly Treasury Statement.

But unlike OASI, CSRS is on-budget and is included in the President's budget report. In fact, with the exception of OASI and the Postal Service, all of the other trust funds (150+ in all) are included on-budget. This means that the surpluses from these programs are used to directly offset any deficit spending by the Federal Government. Of course, even Fed Chairman Greenspan talks about the "unified" budget that includes the OASI surplus as part of the budget - so the distinction between on-budget and off-budget is being lost.

This graph shows the growth of both OASI and the other trust funds. SOURCE: Treasury Dept.

Trust Fund reserves in Billions.

Click on Graph for larger image.

Many of these programs will suffer similar demographic issues as OASI. So when someone like victor at the Dead Parrot questions the existence of the OASI Trust Fund, he is also speaking to our military, Federal employees, Civil Service workers and many others who are paying into similar retirement insurance plans. Thanks to pgl at Angry Bear and William Polley for reminding me of this issue.