RSS Feed

RSS Feed by Calculated Risk on 6/02/2025 11:10:00 AM

Monday, June 02, 2025

Fannie and Freddie: Single Family Serious Delinquency Rates Decreased in April; Fannie Multi-Family Delinquency Rate Highest Since Jan 2011 (ex-Pandemic)

Today, in the Calculated Risk Real Estate Newsletter: Fannie and Freddie: Single Family Serious Delinquency Rates Decreased in April

Excerpt:

Freddie Mac reported that the Single-Family serious delinquency rate in April was 0.57%, down from 0.59% March. Freddie's rate is up year-over-year from 0.51% in April 2024, however, this is close to the pre-pandemic level of 0.60%.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic.

Fannie Mae reported that the Single-Family serious delinquency rate in March was 0.55%, down from 0.56% in March. The serious delinquency rate is up year-over-year from 0.49% in April 2024, however, this is below the pre-pandemic lows of 0.65%.

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

There is much more in the article.

Construction Spending Decreased 0.4% in April

by Calculated Risk on 6/02/2025 10:18:00 AM

From the Census Bureau reported that overall construction spending decreased:

Construction spending during April 2025 was estimated at a seasonally adjusted annual rate of $2,152.4 billion, 0.4 percent below the revised March estimate of $2,162.0 billion. The April figure is 0.5 percent below the April 2024 estimate of $2,163.2 billion. During the first four months of this year, construction spending amounted to $660.2 billion, 1.4 percent above the $651.3 billion for the same period in 2024.Private spending decreased and public spending increased:

emphasis added

Spending on private construction was at a seasonally adjusted annual rate of $1,638.9 billion, 0.7 percent below the revised March estimate of $1,650.8 billion. ...

In April, the estimated seasonally adjusted annual rate of public construction spending was $513.5 billion, 0.4 percent above the revised March estimate of $511.3 billion.

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Private residential (red) spending is 8.9% below the peak in 2022.

Private non-residential (blue) spending is 1.4% below the peak in February 2025.

Public construction spending (orange) is at a new peak.

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is down 4.8%. Private non-residential spending is up 1.0% year-over-year. Public spending is up 5.5% year-over-year.

This was below consensus expectations and spending for the previous two months were revised down significantly.

ISM® Manufacturing index Decreased to 48.5% in May

by Calculated Risk on 6/02/2025 10:00:00 AM

(Posted with permission). The ISM manufacturing index indicated expansion. The PMI® was at 48.5% in May, down from 48.7% in April. The employment index was at 46.8%, up from 46.5% the previous month, and the new orders index was at 47.6%, up from 47.2%.

From ISM: Manufacturing PMI® at 48.5% May 2025 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector contracted in May for the third consecutive month, following a two-month expansion preceded by 26 straight months of contraction, say the nation's supply executives in the latest Manufacturing ISM® Report On Business®.This suggests manufacturing contracted in May. This was below the consensus forecast and new export orders were weak and prices very strong.

The report was issued today by Susan Spence, MBA, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee:

“The Manufacturing PMI® registered 48.5 percent in May, 0.2 percentage point lower compared to the 48.7 percent recorded in April. The overall economy continued in expansion for the 61st month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index contracted for the fourth month in a row following a three-month period of expansion; the figure of 47.6 percent is 0.4 percentage point higher than the 47.2 percent recorded in April. The May reading of the Production Index (45.4 percent) is 1.4 percentage points higher than April’s figure of 44 percent. The index continued in contraction in March for the third straight month after two months of expansion preceded by eight months of contraction. The Prices Index remained in expansion (or ‘increasing’) territory, registering 69.4 percent, down 0.4 percentage point compared to the reading of 69.8 percent in April. The Backlog of Orders Index registered 47.1 percent, up 3.4 percentage points compared to the 43.7 percent recorded in April. The Employment Index registered 46.8 percent, up 0.3 percentage point from April’s figure of 46.5 percent.

“The Supplier Deliveries Index indicated a continued slowing of deliveries, registering 56.1 percent, 0.9 percentage point higher than the 55.2 percent recorded in April. (Supplier Deliveries is the only ISM® Report On Business® index that is inversed; a reading of above 50 percent indicates slower deliveries, which is typical as the economy improves and customer demand increases.) The Inventories Index registered 46.7 percent, down 4.1 percentage points compared to April’s reading of 50.8 percent.

“The New Export Orders Index reading of 40.1 percent is 3 percentage points lower than the reading of 43.1 percent registered in April. The Imports Index plunged into extreme contraction in May, registering 39.9 percent, 7.2 percentage points lower than April’s reading of 47.1 percent.”

emphasis added

Housing June 2nd Weekly Update: Inventory up 2.1% Week-over-week, Up 32.8% Year-over-year

by Calculated Risk on 6/02/2025 08:11:00 AM

Altos reports that active single-family inventory was up 2.1% week-over-week.

Inventory is now up 28.7% from the seasonal bottom in January and is increasing.

Usually, inventory is up about 16% from the seasonal low by this week in the year. So, 2025 is seeing a larger than normal pickup in inventory.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 32.8% compared to the same week in 2024 (last week it was up 32.4%), and down 14.6% compared to the same week in 2019 (last week it was down 15.5%).

This is the highest level since 2019.

It now appears inventory will be close to 2019 levels towards the end of 2025.

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of May 30th, inventory was at 804 thousand (7-day average), compared to 787 thousand the prior week.

Mike Simonsen discusses this data regularly on Youtube

Sunday, June 01, 2025

Monday: ISM Manufacturing, Construction Spending

by Calculated Risk on 6/01/2025 06:13:00 PM

Weekend:

• Schedule for Week of June 1, 2025

Monday:

• At 10:00 AM ET, ISM Manufacturing Index for May. The consensus is for the ISM to be at 49.2, up from 48.7 in April.

• Also at 10:00 AM, Construction Spending for April. The consensus is for a 0.4% increase in construction spending.

• At 1:00 PM, Speech, Fed Chair Jerome Powell, Opening Remarks, At the Federal Reserve Board’s International Finance Division 75th Anniversary Conference, Washington, D.C.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 20 and DOW futures are down 134 (fair value).

Oil prices were down over the last week with WTI futures at $60.79 per barrel and Brent at $62.78 per barrel. A year ago, WTI was at $78, and Brent was at $79 - so WTI oil prices are down about 22% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.10 per gallon. A year ago, prices were at $3.52 per gallon, so gasoline prices are down $0.42 year-over-year.

Update: Lumber Prices Up 17% YoY

by Calculated Risk on 6/01/2025 08:21:00 AM

This is something to watch again. Here is another monthly update on lumber prices.

SPECIAL NOTE: The CME group discontinued the Random Length Lumber Futures contract on May 16, 2023. I switched to a physically-delivered Lumber Futures contract that was started in August 2022. Unfortunately, this impacts long term price comparisons since the new contract was priced about 24% higher than the old random length contract for the period when both contracts were available.

This graph shows CME random length framing futures through August 2022 (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red).

On May 30, 2025, LBR was at $593.00 per 1,000 board feet, up 17% from a year ago.

Click on graph for larger image.

Click on graph for larger image.There is somewhat of a seasonal demand for lumber, and lumber prices frequently peak in the first half of the year.

Last year, prices bottomed in July at $449.00 per 1,000 board feet.

Note that the pickup in early 2018 was due to the Trump lumber tariffs in 2017. There were huge increases during the pandemic due to a combination of supply constraints and a pickup in housing starts.

The recent year-over-year increase might be due to the tariffs.

Saturday, May 31, 2025

Real Estate Newsletter Articles this Week: Case-Shiller National House Price Index Up 3.4% year-over-year

by Calculated Risk on 5/31/2025 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Case-Shiller: National House Price Index Up 3.4% year-over-year in March

• Inflation Adjusted House Prices 1.0% Below 2022 Peak

• Freddie Mac House Price Index Declined in April; Up 2.6% Year-over-year

• Final Look at Local Housing Markets in April and a Look Ahead to May Sales

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of June 1, 2025

by Calculated Risk on 5/31/2025 08:11:00 AM

The key report scheduled for this week is the May employment report.

Other key reports include the May ISM Manufacturing, Vehicle Sales and April trade balance.

10:00 AM: ISM Manufacturing Index for May. The consensus is for the ISM to be at 49.2, up from 48.7 in April.

10:00 AM: Construction Spending for April. The consensus is for a 0.4% increase in construction spending.

1:00 PM: Speech, Fed Chair Jerome Powell, Opening Remarks, At the Federal Reserve Board’s International Finance Division 75th Anniversary Conference, Washington, D.C.

10:00 AM ET: Job Openings and Labor Turnover Survey for April from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for April from the BLS. This graph shows job openings (black line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings decreased in March to 7.19 million from 7.48 million in February. The number of job openings (black) were down 11% year-over-year.

Quits were unchanged year-over-year.

Late: Light vehicle sales for May.

Late: Light vehicle sales for May.

The consensus is for light vehicle sales to be 16.4 million SAAR in May, down from 17.3 million in April (Seasonally Adjusted Annual Rate).

Late: Light vehicle sales for May.

Late: Light vehicle sales for May.The consensus is for light vehicle sales to be 16.4 million SAAR in May, down from 17.3 million in April (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the sales rate for last month.

----- Wednesday, June 4th -----

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for May. This report is for private payrolls only (no government). The consensus is for 120,000 payroll jobs added in May, up from 62,000 in April.

10:00 AM: the ISM Services Index for May. The consensus is for a reading of 52.0, up from 51.6.

----- Thursday, June 5th -----

8:30 AM: Trade Balance report for April from the Census Bureau.

8:30 AM: Trade Balance report for April from the Census Bureau.

This graph shows the U.S. trade deficit, with and without petroleum.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for May. This report is for private payrolls only (no government). The consensus is for 120,000 payroll jobs added in May, up from 62,000 in April.

10:00 AM: the ISM Services Index for May. The consensus is for a reading of 52.0, up from 51.6.

8:30 AM: Trade Balance report for April from the Census Bureau.

8:30 AM: Trade Balance report for April from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum surplus, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $117.3 billion. The U.S. trade deficit was at $140.5 Billion in March.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for initial claims of 230 thousand, down from 240 thousand last week.

----- Friday, June 6th -----

8:30 AM: Employment Report for May. The consensus is for 130,000 jobs added, and for the unemployment rate to be unchanged at 4.2%.

8:30 AM: Employment Report for May. The consensus is for 130,000 jobs added, and for the unemployment rate to be unchanged at 4.2%.

There were 177,000 jobs added in April, and the unemployment rate was at 4.2%.

This graph shows the jobs added per month since January 2021.

The consensus is the trade deficit to be $117.3 billion. The U.S. trade deficit was at $140.5 Billion in March.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for initial claims of 230 thousand, down from 240 thousand last week.

8:30 AM: Employment Report for May. The consensus is for 130,000 jobs added, and for the unemployment rate to be unchanged at 4.2%.

8:30 AM: Employment Report for May. The consensus is for 130,000 jobs added, and for the unemployment rate to be unchanged at 4.2%.There were 177,000 jobs added in April, and the unemployment rate was at 4.2%.

This graph shows the jobs added per month since January 2021.

Friday, May 30, 2025

May 30th COVID Update: Weekly COVID Deaths at New Pandemic Low

by Calculated Risk on 5/30/2025 07:39:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So, I'm no longer tracking hospitalizations.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week | 267✅ | 310 | ≤3501 | |

| 1my goals to stop weekly posts. 🚩 Increasing number weekly for Deaths. ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported since Jan 2020.

Although weekly deaths met the original goal to stop posting in June 2024 (previous pandemic low of 314 deaths), I've continued to post since deaths moved above the goal again - and I'll continue to post until weekly deaths are below the goal for several weeks.

This appears to be a leading indicator for COVID hospitalizations and deaths. This is close to the lows of May 2024.

This appears to be a leading indicator for COVID hospitalizations and deaths. This is close to the lows of May 2024.Nationally COVID in wastewater is "Very Low".

Q2 GDP Tracking: Wide Range due to Trade "Distortions"

by Calculated Risk on 5/30/2025 02:09:00 PM

From BofA:

Since our last weekly publication, our 2Q GDP tracking is down two-tenths to +1.8% q/q saar. [May 30th estimate]From Goldman:

emphasis added

The goods trade deficit narrowed by more than expected in April, reflecting a sharp decline in goods imports and a moderate increase in goods exports. The Advance Economic Indicators report indicated a significantly larger decline in imports than our previous GDP tracking assumptions, while the details of the personal income and spending report were modestly softer than our previous assumptions. On net, we boosted our Q2 GDP tracking estimate by 1.0pp to +3.3% (quarter-over-quarter annualized). Our Q2 domestic final sales estimate stands at -0.6%. We continue to see the headline Q1 and Q2 GDP growth readings as distorted measures of economic growth because of measurement challenges related to swings in imports around tariff increases. [May 30th estimate]And from the Atlanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2025 is 3.8 percent on May 30, up from 2.2 percent on May 27. After recent releases from the US Census Bureau and the US Bureau of Economic Analysis, the nowcast of the contribution of net exports to second-quarter real GDP growth increased from -0.64 percentage points to 1.45 percentage points, while the nowcasts of second-quarter real personal consumption expenditures growth and second-quarter real gross private domestic investment growth declined from 3.7 percent and -0.2 percent, respectively, to 3.3 percent and -1.4 percent. [May 30th estimate]

Hotels: Occupancy Rate Decreased 0.4% Year-over-year

by Calculated Risk on 5/30/2025 01:10:00 PM

The U.S. hotel industry reported mixed year-over-year comparisons, according to CoStar’s latest data through 24 May. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

18-24 May 2025 (percentage change from comparable week in 2024):

• Occupancy: 67.5% (-0.4%)

• Average daily rate (ADR): US$164.57 (+1.5%)

• Revenue per available room (RevPAR): US$111.02 (+1.1%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025, blue is the median, and dashed light blue is for 2024. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking last year and above the median rate for the period 2000 through 2024 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average will mostly move sideways for a couple more weeks until the summer travel season. We will likely see a hit to occupancy during the summer months due to less international tourism.

Freddie Mac House Price Index Declined in April; Up 2.6% Year-over-year

by Calculated Risk on 5/30/2025 10:09:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Freddie Mac House Price Index Declined in April; Up 2.6% Year-over-year

A brief excerpt:

Freddie Mac reported that its “National” Home Price Index (FMHPI) decreased -0.15% month-over-month (MoM) on a seasonally adjusted (SA) basis in April. On a year-over-year basis, the National FMHPI was up 2.6% in April, down from up 2.9% YoY in March. The YoY increase peaked at 19.0% in July 2021, and for this cycle, bottomed at up 0.9% YoY in April 2023. ...There is much more in the article!

As of April, 26 states and D.C. were below their previous peaks, Seasonally Adjusted. The largest seasonally adjusted declines from the recent peaks are in D.C. (-5.3), Colorado (-2.4%), Oregon (-2.0%), Montana (-1.7%) and Florida (-1.7%).

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted. Austin continues to be the worst performing city. However, 4 of the 5 cities with the largest price declines are in Florida.

PCE Measure of Shelter Decreases to 4.2% YoY in April

by Calculated Risk on 5/30/2025 08:53:00 AM

Here is a graph of the year-over-year change in shelter from the CPI report and housing from the PCE report this morning, both through April 2025.

CPI Shelter was up 4.0% year-over-year in April, unchanged from 4.0% in March, and down from the cycle peak of 8.2% in March 2023.

CPI Shelter was up 4.0% year-over-year in April, unchanged from 4.0% in March, and down from the cycle peak of 8.2% in March 2023.

Housing (PCE) was up 4.2% YoY in April, down from 4.3% in March and down from the cycle peak of 8.3% in April 2023.

Since asking rents are mostly flat year-over-year, these measures will slowly continue to decline over the next year as rents for existing tenants continue to increase.

Since asking rents are mostly flat year-over-year, these measures will slowly continue to decline over the next year as rents for existing tenants continue to increase.

The second graph shows PCE prices, Core PCE prices and Core ex-housing over the last 3 months (annualized):

The second graph shows PCE prices, Core PCE prices and Core ex-housing over the last 3 months (annualized):Key measures are slightly above the Fed's target on a 3-month basis.

3-month annualized change:

PCE Price Index: 2.1%

Core PCE Prices: 2.7%

Core minus Housing: 2.4%

Core PCE Prices: 2.7%

Core minus Housing: 2.4%

Note: It is likely there is still some residual seasonality distorting PCE prices in Q1.

Personal Income increased 0.8% in April; Spending increased 0.2%

by Calculated Risk on 5/30/2025 08:30:00 AM

From the BEA: Personal Income and Outlays, April 2025

Personal income increased $210.1 billion (0.8 percent at a monthly rate) in April, according to estimates released today by the U.S. Bureau of Economic Analysis. Disposable personal income (DPI)—personal income less personal current taxes—increased $189.4 billion (0.8 percent) and personal consumption expenditures (PCE) increased $47.8 billion (0.2 percent).The April PCE price index increased 2.1 percent year-over-year (YoY), down from 2.3 percent YoY in March, and down from the recent peak of 7.2 percent in June 2022.

Personal outlays—the sum of PCE, personal interest payments, and personal current transfer payments—increased $48.6 billion in April. Personal saving was $1.12 trillion in April and the personal saving rate—personal saving as a percentage of disposable personal income—was 4.9 percent.

From the preceding month, the PCE price index for April increased 0.1 percent. Excluding food and energy, the PCE price index also increased 0.1 percent.

From the same month one year ago, the PCE price index for April increased 2.1 percent. Excluding food and energy, the PCE price index increased 2.5 percent from one year ago.

emphasis added

The PCE price index, excluding food and energy, increased 2.5 percent YoY, down from 2.6 percent the previous month, and down from the recent peak of 5.6 percent in February 2022.

The following graph shows real Personal Consumption Expenditures (PCE) through April 2025 (2017 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.

The dashed red lines are the quarterly levels for real PCE.

Personal income was above expectations and PCE were at expectations.

The following graph shows real Personal Consumption Expenditures (PCE) through April 2025 (2017 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income was above expectations and PCE were at expectations.

Inflation was slightly below expectations.

Thursday, May 29, 2025

Friday: Personal Income and Outlays

by Calculated Risk on 5/29/2025 07:21:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Friday:

• At 8:30 AM ET, Personal Income and Outlays, April 2025. The consensus is for a 0.3% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.1%. PCE prices are expected to be up 2.2% YoY, and core PCE prices up 2.5% YoY.

• At 9:45 AM, Chicago Purchasing Managers Index for May.

• At 10:00 AM: University of Michigan's Consumer sentiment index (Final for May). The consensus is for a reading of 50.8.

Realtor.com Reports Most Actively "For Sale" Inventory since 2019

by Calculated Risk on 5/29/2025 01:08:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For May, Realtor.com reported inventory was up 30.6% YoY, but still down 16.3% compared to the 2017 to 2019 same month levels.

Now - on a weekly basis - inventory is up 29.7% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending May 24, 2025 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 81st consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending May 24, 2025

• Active inventory climbed 29.7% year-over-year

The number of homes actively for sale remains on a strong upward trajectory, now 29.7% higher than this time last year. This represents the 81st consecutive week of annual gains in inventory. There were more than 1 million homes for sale last week, the highest inventory level since December 2019.

• New listings—a measure of sellers putting homes up for sale—rising 8.2% year-over-year

New listings rose again last week, up 8.2% compared to the same period last year.

• The median list price was up 0.2% year-over-year

After a brief cooling period the previous week, the national median listing price resumed its upward trajectory last week. At the same time, the median listing price per square foot—which adjusts for changes in home size—rose 0.9% year-over-year.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 81st consecutive week.

New listings were solid.

Median list prices were mostly unchanged year-over-year.

NAR: Pending Home Sales Decrease 6.3% in April; Down 2.5% YoY

by Calculated Risk on 5/29/2025 10:00:00 AM

From the NAR: Pending Home Sales Declined 6.3% in April

Pending home sales decreased 6.3% in April, according to the National Association of REALTORS®. All four U.S. regions experienced month-over-month losses in transactions. Year-over-year, contract signings rose in the Midwest but descended in the Northeast, South and West – with the West suffering the greatest loss.Note: Contract signings usually lead sales by about 45 to 60 days, so this would usually be for closed sales in May and June.

The Pending Home Sales Index (PHSI)* – a forward-looking indicator of home sales based on contract signings – dove 6.3% to 71.3 in April. Year-over-year, pending transactions retracted by 2.5%. An index of 100 is equal to the level of contract activity in 2001.

"At this critical stage of the housing market, it is all about mortgage rates," said NAR Chief Economist Lawrence Yun. "Despite an increase in housing inventory, we are not seeing higher home sales. Lower mortgage rates are essential to bring home buyers back into the housing market."

...

The Northeast PHSI decreased 0.6% from last month to 62.1, down 3.0% from April 2024. The Midwest index condensed 5.0% to 73.5 in April, up 2.2% from the previous year.

The South PHSI sank 7.7% to 85.9 in April, down 3.0% from a year ago. The West index degraded 8.9% from the prior month to 53.3, down 6.5% from April 2024.

emphasis added

Q1 GDP Growth Revised up to -0.2% Annual Rate

by Calculated Risk on 5/29/2025 08:35:00 AM

From the BEA: Gross Domestic Product (Second Estimate), Corporate Profits (Preliminary Estimate), 1st Quarter 2025

Real gross domestic product (GDP) decreased at an annual rate of 0.2 percent in the first quarter of 2025 (January, February, and March), according to the second estimate released by the U.S. Bureau of Economic Analysis. In the fourth quarter of 2024, real GDP increased 2.4 percent.Here is a Comparison of Second and Advance Estimates. PCE growth was revised down from 1.8% to 1.2%. Residential investment was revised down from 1.3% to -0.6%.

The decrease in real GDP in the first quarter primarily reflected an increase in imports, which are a subtraction in the calculation of GDP, and a decrease in government spending. These movements were partly offset by increases in investment, consumer spending, and exports.

Real GDP was revised up 0.1 percentage point from the advance estimate, reflecting an upward revision to investment that was partly offset by a downward revision to consumer spending.

emphasis added

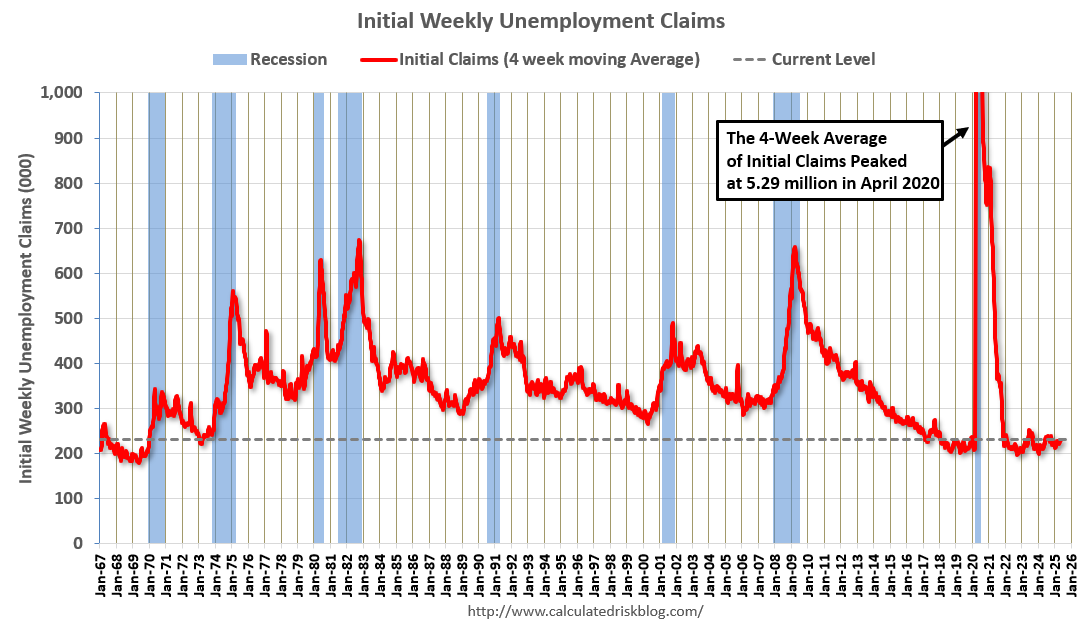

Weekly Initial Unemployment Claims Increase to 240,000

by Calculated Risk on 5/29/2025 08:30:00 AM

The DOL reported:

In the week ending May 24, the advance figure for seasonally adjusted initial claims was 240,000, an increase of 14,000 from the previous week's revised level. The previous week's level was revised down by 1,000 from 227,000 to 226,000. The 4-week moving average was 230,750, a decrease of 250 from the previous week's revised average. The previous week's average was revised down by 500 from 231,500 to 231,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 230,750.

The previous week was revised down.

Weekly claims were higher than the consensus forecast.

Wednesday, May 28, 2025

Thursday: GDP, Unemployment Claims, Pending Home Sales

by Calculated Risk on 5/28/2025 07:15:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM, The initial weekly unemployment claims report will be released. The consensus is for initial claims of 225 thousand, down from 227 thousand last week.

• Also at 8:30 AM, Gross Domestic Product, 1st quarter 2025 (Second estimate). The consensus is that real GDP decreased 0.3% annualized in Q1, unchanged from the advance estimate of -0.3%.

• At 10:00 AM, Pending Home Sales Index for April. The consensus is for a 0.4% decrease in the index.