RSS Feed

RSS Feed by Calculated Risk on 5/21/2025 07:01:00 PM

Wednesday, May 21, 2025

Thursday: Existing Home Sales, Unemployment Claims

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for initial claims of 232 thousand, up from 229 thousand last week.

• Also at 8:30 AM, Chicago Fed National Activity Index for April. This is a composite index of other data.

• At 10:00 AM, Existing Home Sales for April from the National Association of Realtors (NAR). The consensus is for 4.15 million SAAR, up from 4.02 million. Housing economist Tom Lawler expects the NAR to report sales of 3.98 million SAAR.

ICE: "Annual home price growth nationally slowed to 1.6% in May"

by Calculated Risk on 5/21/2025 03:12:00 PM

The ICE Home Price Index (HPI) is a repeat sales index. ICE reports the median price change of the repeat sales.

From ICE (Intercontinental Exchange):

Annual home price growth nationally slowed to 1.6% in May from 2% in April, as inventory surpluses that began in the Sunbelt spread to the West.As ICE mentioned, cities in the South have been leading the way in inventory increases and price declines (especially Florida and Texas). Now the West Coast markets are following, although inventory levels are mostly still below the pre-pandemic levels.• 40% of the nation’s largest housing markets experienced seasonally adjusted month-over-month price declines from April to May, including 23 of the 24 top markets in the WestPrice declines appear to be inventory driven:

• The number of markets with year-over-year price declines increased from 9 to 23 by mid-May, with a majority (9) of the newcomers located in the West

• Those markets include: Denver (-1.6%), San Francisco and Stockton, Calif. (-1.5%), Phoenix (-1.2%), with more modest declines in Honolulu, Colorado Springs, Tucson, Sacramento, and San Diego

• That’s the largest number of markets with annual price declines since interest rates surged above 7.5% in late 2023• Western markets (led by California) have seen sharp rises in inventory, with every major California market now having at least +40% more homes available for sale than at the same time last year, led by Stockton (+87% ) and Oxnard and San Diego (+70% each)If current trends persist, we could see prices fall year over year in even more West Coast markets.

• Inventories in San Francisco, San Jose, and Stockton have already surpassed pre-pandemic levels, with other California markets on pace to ‘normalize’ later this year

AIA: "Billings continue to decline at architecture firms"

by Calculated Risk on 5/21/2025 01:01:00 PM

Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment.

From the AIA: ABI April 2025: Billings continue to decline at architecture firms

The AIA/Deltek Architecture Billings Index (ABI) score declined to 43.2 for the month. Billings have declined for 28 of the last 31 months, since they first dipped back into negative territory following the post-pandemic boom. Despite generally strong backlogs at firms, inquiries into new work declined for the third consecutive month in April, while the value of new design contracts declined at the majority of firms for the fourteenth consecutive month. Although the U.S. economy is not officially in a recession at this time, many architecture firms are reporting recession-like business conditions.• Northeast (40.2); Midwest (44.4); South (46.2); West (42.1)

Regionally, business conditions at architecture firms remained softest at firms located in the Northeast for the seventh consecutive month in April. Conditions have also softened significantly at firms located in the West since the beginning of the year. In addition, billings continued to decline at firms of all specializations this month, particularly at firms with commercial/industrial and multifamily residential specializations. The pace of the decline remains slower at firms with an institutional specialization, but billings have still declined nearly every month since mid-2023.

...

The ABI score is a leading economic indicator of construction activity, providing an approximately nine-to-twelve-month glimpse into the future of nonresidential construction spending activity. The score is derived from a monthly survey of architecture firms that measures the change in the number of services provided to clients.

emphasis added

• Sector index breakdown: commercial/industrial (40.5); institutional (46.3); multifamily residential (40.8)

Click on graph for larger image.

Click on graph for larger image.This graph shows the Architecture Billings Index since 1996. The index was at 43.2 in April, down from 44.1 in March. Anything below 50 indicates a decrease in demand for architects' services.

This index has indicated contraction for 28 of the last 31 months.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index usually leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment throughout 2025 and into 2026.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index usually leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment throughout 2025 and into 2026.

Multi-family billings have been below 50 for the 33 consecutive months. This suggests we will see continued weakness in multi-family starts.

In Q1 2025, 19% of Units Started Built-for-Rent were Single Family

by Calculated Risk on 5/21/2025 09:52:00 AM

Today, in the Real Estate Newsletter: In Q1 2025, 19% of Units Started Built-for-Rent were Single Family

Brief excerpt:

Along with the monthly housing starts report for April released last week, the Census Bureau also released Housing Units Started by Purpose and Design through Q1 2025.There is much more in the newsletter.

The first graph shows the number of single family and multi-family units started with the intent to rent. This data is quarterly and Not Seasonally Adjusted (NSA). Although the majority of units built-for-rent’ are still multi-family (blue) - even after the sharp decline in 2022 - there has been a significant pickup in single family units started built-for-rent (red).

A total of 102,000 units were started built-for-rent in Q1, with 19% single family units.

MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

by Calculated Risk on 5/21/2025 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 5.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 16, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 27 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 13 percent higher than the same week one year ago.

“Mortgage rates jumped to their highest level since February last week, with investors concerned about rising inflation and the impact of increasing deficits and debt,” said Mike Fratantoni, MBA’s SVP and Chief Economist. “Higher rates, including the 30-year fixed rate increasing to 6.92 percent, led to a slowdown across the board. However, purchase applications are up 13 percent from one year ago.

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.92 percent from 6.86 percent, with points increasing to 0.69 from 0.68 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is up 13% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is up from the lows in late October 2023 and is 5% above the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

The refinance index decreased and remained very low.

Tuesday, May 20, 2025

Wednesday: Architecture Billings Index

by Calculated Risk on 5/20/2025 07:41:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 10:00 AM, State Employment and Unemployment (Monthly) for April 2025

• During the day, The AIA's Architecture Billings Index for April (a leading indicator for commercial real estate).

May Vehicle Forecast: Sales "Cooling Off" to 15.9 million SAAR

by Calculated Risk on 5/20/2025 03:52:00 PM

From WardsAuto: U.S. Light-Vehicle Sales Cooling Off in May; Inventory Still Falling (pay content). Brief excerpt:

With inventory set to continue declining month-to-month, and the cost to automakers of the tariffs more strongly kicking in by July, sales are likely to continue sequential weakness into the summer – unless automakers decide to eat most of the increased cost. Based on the North America production outlook for the next several months, most are not planning to eat a lot of the cost.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for May (Red).

On a seasonally adjusted annual rate basis, the Wards forecast of 15.9 million SAAR, would be down 7.9% from last month, and up 0.5% from a year ago.

Car buyers rushed to buy over the previous couple of months to beat the tariffs. There will be further payback in coming months.

Energy expenditures as a percentage of PCE

by Calculated Risk on 5/20/2025 02:13:00 PM

During the early stages of the pandemic, energy expenditures as a percentage of PCE hit an all-time low of 3.3% of PCE. Energy expenditures as a percentage of PCE increased to 2018 levels by the end of 2021 and increased further in 2022 due to the Russian invasion of Ukraine.

Here is an update through the April 2025 PCE report.

This graph shows expenditures on energy goods and services as a percent of total personal consumption expenditures. This is one of the measures that Professor Hamilton at Econbrowser looks at to evaluate any drag on GDP from energy prices.

Click on graph for larger image.

Data source: BEA.

In general, energy expenditures as a percent of PCE has been trending down for decades. The huge spikes in energy prices during the oil crisis of 1973 and 1979 are obvious. As is the increase in energy prices during the 2001 through 2008 period.

This graph shows expenditures on energy goods and services as a percent of total personal consumption expenditures. This is one of the measures that Professor Hamilton at Econbrowser looks at to evaluate any drag on GDP from energy prices.

Click on graph for larger image.

Data source: BEA.

In general, energy expenditures as a percent of PCE has been trending down for decades. The huge spikes in energy prices during the oil crisis of 1973 and 1979 are obvious. As is the increase in energy prices during the 2001 through 2008 period.

In April 2025, energy expenditures were at 3.6% of PCE, down from 3.8% in March, and down from the recent peak of 5.2% in June 2022.

This is below the pre-pandemic level.

Update: Lumber Prices Up 13% YoY

by Calculated Risk on 5/20/2025 11:32:00 AM

This is something to watch again. Here is another monthly update on lumber prices.

SPECIAL NOTE: The CME group discontinued the Random Length Lumber Futures contract on May 16, 2023. I switched to a physically-delivered Lumber Futures contract that was started in August 2022. Unfortunately, this impacts long term price comparisons since the new contract was priced about 24% higher than the old random length contract for the period when both contracts were available.

This graph shows CME random length framing futures through August 2022 (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red).

On May 20, 2025, LBR was at $599.50 per 1,000 board feet, up 13% from a year ago.

Click on graph for larger image.

Click on graph for larger image.There is somewhat of a seasonal demand for lumber, and lumber prices frequently peak in the first half of the year.

Last year, prices bottomed in July at $449.00 per 1,000 board feet.

The recent year-over-year increase might be due to the tariffs.

California Home Sales "Retreat" in April; New Listings "Surge"

by Calculated Risk on 5/20/2025 08:21:00 AM

Today, in the Calculated Risk Real Estate Newsletter: California Home Sales "Retreat" in April; New Listings "Surge"

A brief excerpt:

From the California Association of Realtors® (C.A.R.): California home sales retreat for second straight month in April as median home price hits new all-time high, C.A.R. reportsThere is much more in the article.April’s sales pace fell 3.4 percent from the 277,030 homes sold in March and was down 0.2 percent from a year ago, when 268,170 homes were sold on an annualized basis. April’s sales level was the lowest in three months.

...

Total active listings in April rose on a year-over-year basis at the fastest pace since January 2023. The level of active listings last month reached a 66-month high (since October 2019) and recorded its 15th consecutive month of annual gain in housing supply.

Monday, May 19, 2025

"Mortgage Rates Briefly Over 7%"

by Calculated Risk on 5/19/2025 07:03:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Briefly Over 7% Before Mid-Day Improvement

From Matthew Graham at Mortgage News Daily: Mortgage Rates Briefly Over 7% Before Mid-Day Improvement

Mortgage rates jumped sharply over the weekend as financial markets reacted to Moody's credit rating downgrade of the U.S. News of the downgrade broke with only minutes left in Friday's market/business day, so most of the response played out when global markets opened again late last night.Tuesday:

...

Most mortgage lenders are deciding on rates for the day in the 9am-10am ET time frame. Because this was one of the weakest moments for the bond market, mortgage rates were sharply higher at first. The average lender was back over 7% for the 1st time since April 11th, and only the 2nd time in 3 months.

No sooner were these rates being published than the underlying market began moving back in the other direction. Mortgage lenders prefer to only set rates once per day, but will make mid-day updates when things change enough. Today's reversal was more than sufficient to prompt a re-price. After that, the average top tier 30yr fixed rate moved just barely back below 7.0%--still higher than Friday, but much more in line with last week's range. [30 year fixed 6.99%]

emphasis added

• No major economic releases scheduled.

LA Ports: April Inbound Traffic Up YoY, Outbound Down

by Calculated Risk on 5/19/2025 01:55:00 PM

There were still a large number of ships unloading in April. We should see a sharp drop in May traffic due to the tariffs.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.On a rolling 12-month basis, inbound traffic increased 0.7% in April compared to the rolling 12 months ending the previous month. Outbound traffic decreased 0.3% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year. Imports were up 10% YoY in April and exports were down 4% YoY.

Recently importers rushed to beat the tariffs. And port traffic will likely slow sharply in coming months.

"How do you grade the Spring housing market?"

by Calculated Risk on 5/19/2025 10:51:00 AM

Today, in the Calculated Risk Real Estate Newsletter: "How do you grade the Spring housing market?"

A brief excerpt:

Last week, Housing Wire Editor in Chief Sarah Wheeler asked Lead Analyst Logan Mohtashami the above question: "How do you grade the Spring housing market?"There is much more in the article.

My friend Logan replied: “Generally, just for how I look at housing, this kind of gets an A ...”

I almost fell out of my chair!

Housing May 19th Weekly Update: Inventory up 1.5% Week-over-week, Up 32.7% Year-over-year

by Calculated Risk on 5/19/2025 08:11:00 AM

Altos reports that active single-family inventory was up 1.5% week-over-week.

Inventory is now up 22.9% from the seasonal bottom in January and is increasing.

Usually, inventory is up about 13% from the seasonal low by this week in the year. So, 2025 is seeing a larger than normal pickup in inventory.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 32.7% compared to the same week in 2024 (last week it was up 32.9%), and down 15.6% compared to the same week in 2019 (last week it was down 15.7%).

This is the highest level since 2019.

It now appears inventory will be close to 2019 levels towards the end of 2025.

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of May 16th, inventory was at 767 thousand (7-day average), compared to 756 thousand the prior week.

Mike Simonsen discusses this data regularly on Youtube

Sunday, May 18, 2025

Sunday Night Futures

by Calculated Risk on 5/18/2025 06:16:00 PM

Weekend:

• Schedule for Week of May 18, 2025

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 43 and DOW futures are down 267 (fair value).

Oil prices were up over the last week with WTI futures at $62.49 per barrel and Brent at $65.41 per barrel. A year ago, WTI was at $82, and Brent was at $82 - so WTI oil prices are down about 24% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.14 per gallon. A year ago, prices were at $3.57 per gallon, so gasoline prices are down $0.43 year-over-year.

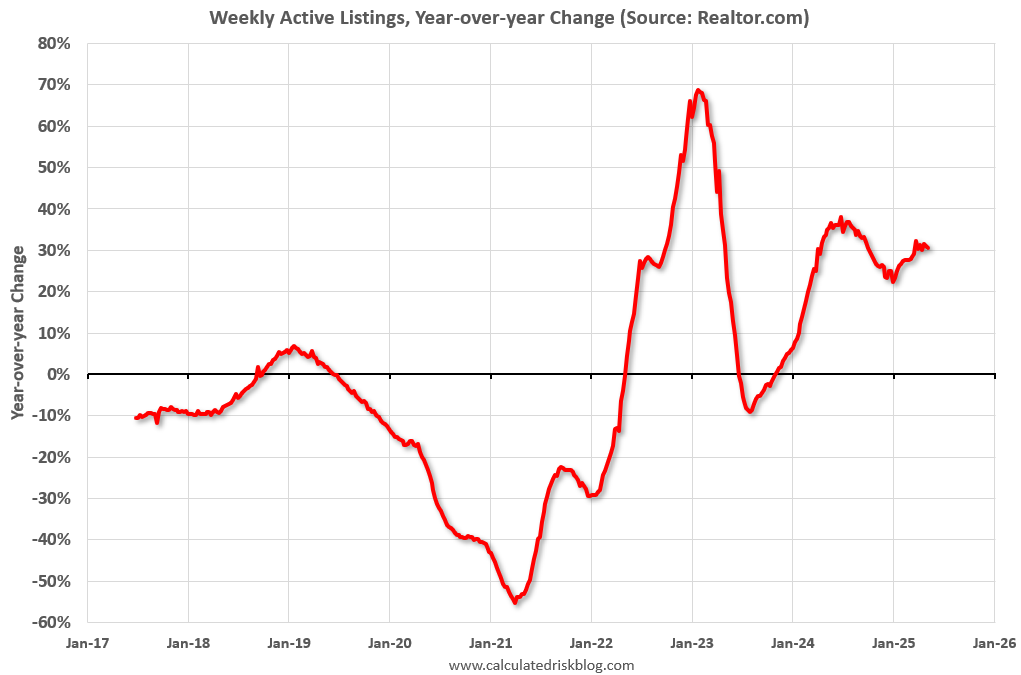

Realtor.com Reports Most Actively "For Sale" Inventory since 2019

by Calculated Risk on 5/18/2025 08:12:00 AM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For May, Realtor.com reported inventory was up 30.6% YoY, but still down 16.3% compared to the 2017 to 2019 same month levels.

Now - on a weekly basis - inventory is up 30.6% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending May 10, 2025 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 79th consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending May 10, 2025

• Active inventory climbed 30.6% year over year

The number of homes actively for sale remains on a strong upward trajectory, now 30.6% higher than this time last year. This represents the 79th consecutive week of annual gains in inventory. There were more than 1 million homes for sale last week, the highest inventory level since December 2019.

• New listings—a measure of sellers putting homes up for sale—rose 11.2% year over year

New listings rose again last week, up 11.2% compared with the same period last year. The momentum that began earlier this spring remains strong, signaling a vibrant market as we head into late spring and early summer.

• The median list price remained flat

After three consecutive weeks of gains, the national median list price remained flat year over year last week. Ongoing affordability challenges, along with growing concerns about personal finances and job security, continue to pose significant hurdles for many buyers. Nearly 4 in 5 home shoppers believe it’s a bad time to buy, which is dampening demand.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 79th consecutive week.

New listings were solid.

Median list prices were unchanged year-over-year.

Saturday, May 17, 2025

Real Estate Newsletter Articles this Week: Housing Starts Increased to 1.361 million Annual Rate in April

by Calculated Risk on 5/17/2025 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Housing Starts Increased to 1.361 million Annual Rate in April

• MBA: Mortgage Delinquencies Increased Slightly in Q1 2025

• Part 2: Current State of the Housing Market; Overview for mid-May 2025

• Lawler: Early Read on Existing Home Sales in April

• 3rd Look at Local Housing Markets in April

• Q1 NY Fed Report: Mortgage Originations by Credit Score, Delinquencies Increase, Foreclosures Increase

• 2nd Look at Local Housing Markets in April

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of May 18, 2025

by Calculated Risk on 5/17/2025 08:11:00 AM

The key reports this week are April New and Existing Home Sales.

No major economic releases scheduled.

No major economic releases scheduled.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

10:00 AM: State Employment and Unemployment (Monthly) for April 2025

During the day: The AIA's Architecture Billings Index for April (a leading indicator for commercial real estate).

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for initial claims of 232 thousand, up from 229 thousand last week.

8:30 AM ET: Chicago Fed National Activity Index for April. This is a composite index of other data.

10:00 AM: Existing Home Sales for April from the National Association of Realtors (NAR). The consensus is for 4.15 million SAAR, up from 4.02 million.

10:00 AM: Existing Home Sales for April from the National Association of Realtors (NAR). The consensus is for 4.15 million SAAR, up from 4.02 million.The graph shows existing home sales from 1994 through the report last month.

Housing economist Tom Lawler expects the NAR to report sales of 3.98 million SAAR.

10:00 AM: New Home Sales for April from the Census Bureau.

10:00 AM: New Home Sales for April from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 700 thousand SAAR, down from 724 thousand SAAR in March.

Friday, May 16, 2025

May 16th COVID Update: Weekly COVID Deaths Increased Slightly

by Calculated Risk on 5/16/2025 07:03:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So, I'm no longer tracking hospitalizations.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week | 358🚩 | 346 | ≤3501 | |

| 1my goals to stop weekly posts. 🚩 Increasing number weekly for Deaths. ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported since Jan 2023.

Although weekly deaths met the original goal to stop posting in June 2023 (low of 314 deaths), I've continued to post since deaths were above the goal again - and I'll continue to post until weekly deaths are once again below the goal for several weeks.

Weekly deaths were steadily decreasing following the winter pickup, however, weekly deaths increased this week.

This appears to be a leading indicator for COVID hospitalizations and deaths. This is moving towards the lows last May.

This appears to be a leading indicator for COVID hospitalizations and deaths. This is moving towards the lows last May.Nationally COVID in wastewater is "Low".

Q2 GDP Tracking: Low-to-Mid 2%

by Calculated Risk on 5/16/2025 12:35:00 PM

From BofA:

We initiated our 2Q GDP tracking after the April retail sales print. It moved up two-tenth to 2.2% q/q saar from our official forecast of 2.0% q/q saar. Meanwhile, our 1Q GDP tracking moved up a tenth to -0.3% q/q saar since our last weekly publication [May 16th estimate]From Goldman:

emphasis added

We lowered our Q2 GDP tracking estimate by 0.1pp to +2.1% (quarter-over-quarter annualized) and our Q2 domestic final sales estimate by the same amount to +0.1%. Our past-quarter GDP tracking estimate stands at -0.5%. [May 16th estimate]And from the Atlanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2025 is 2.4 percent on May 16, down from 2.5 percent on May 15. After this morning’s housing starts report from the US Census Bureau and the release of import and export price indexes from the US Bureau of Labor Statistics, the nowcast of second-quarter real residential fixed investment growth decreased from 0.4 percent to -3.0 percent. [May 1st estimate]