RSS Feed

RSS Feed by Calculated Risk on 9/15/2010 08:30:00 AM

Wednesday, September 15, 2010

NY Fed: Manufacturing Index declines slightly in September

From the NY Fed: Empire State Manufacturing Survey

The Empire State Manufacturing Survey indicates that conditions held relatively steady in New York’s manufacturing sector in September. The general business conditions index remained positive, although it slipped 3 points to 4.1. The new orders and shipments indexes were both up moderately for the month, at levels signaling stable activity.These regional surveys have been showing a slowdown in manufacturing and are being closely watched right now. This was slightly below expectations.

...

Employment indexes were positive, suggesting that employment levels and the average workweek continued to expand over the month. The degree of optimism about the six-month outlook continued to deteriorate, with the future general business conditions index hitting its lowest level since early 2009.

MBA: Mortgage Purchase Activity decreases slightly

by Calculated Risk on 9/15/2010 07:14:00 AM

The MBA reports: Mortgage Applications Decrease in Latest MBA Weekly Survey

The Refinance Index decreased 10.8 percent from the previous week. The seasonally adjusted Purchase Index decreased 0.4 percent from one week earlier.

...

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.47 percent from 4.50 percent, with points increasing to 1.08 from 0.96 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

Purchase applications are at about the levels of 1996 or 1997, suggesting existing home sales (closed transactions) in August, September and even October, will only be slightly higher than in July. Note: economist Tom Lawler's "early read" is for August existing home sales of 4.1 million SAAR.

Tuesday, September 14, 2010

LA Port Traffic in August: Imports Surge, Exports down year-over-year

by Calculated Risk on 9/14/2010 09:28:00 PM

Notes: this data is not seasonally adjusted. There is a very distinct seasonal pattern for imports, but not for exports. LA area ports handle about 40% of the nation's container port traffic.

The following graph shows the loaded inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container). Although containers tell us nothing about value, container traffic does give us an idea of the volume of goods being exported and imported. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Loaded inbound traffic was up 24% compared to August 2009. Inbound traffic is now up 4% vs. two years ago (August '08).

Loaded outbound traffic was down 2.6% from August 2009. Unlike imports, exports are still off from 2 years ago (off 17%).

For imports there is usually a significant dip in either February or March, depending on the timing of the Chinese New Year, and then usually imports increase until late summer or early fall as retailers build inventory for the holiday season. So part of this increase in August imports is just the normal seasonal pattern.

Based on this data, it appears the trade deficit with Asia increased again in August. Not only have the pre-crisis global imbalances returned, but exports appear to have peaked in May (no clear seasonal pattern), and have moved sideways or down over the last 6 months.

Lawler: "Early read" on August existing home sales

by Calculated Risk on 9/14/2010 05:50:00 PM

CR Note: This is from housing economist Tom Lawler:

The “early read” on existing home sales based on regional data suggests that existing home sales ran at a seasonally adjusted annual rate of around 4.1 million in August, up around 7% from July’s pace.

My “best guess” right now on the pending home sales index is that it will show a seasonally adjusted increase from July to August of around 4%.

CR Note: some bounce back was expected. This would put the months of supply around 11.5 months. This sales rate would be at about the levels of 1996 or 1997. Existing home sales for August will be released next week on Thursday (Sept 23rd).

Ceridian-UCLA: Diesel Fuel index declines in August, "signals struggling economy"

by Calculated Risk on 9/14/2010 03:30:00 PM

This is the new UCLA Anderson Forecast and Ceridian Corporation index using real-time diesel fuel consumption data: Pulse of Commerce IndexTM

Press Release: August PCI Decline Signals Struggling Economy, but no Double-Dip

The Ceridian-UCLA Pulse of Commerce Index™ (PCI) by UCLA Anderson School of Management fell 1 percent in August, a disappointing number that closes out an erratic summer in the PCI.

...

“The August data is obviously discouraging after the cautious optimism created from July’s report,” said Ed Leamer, chief PCI economist. “There is not much to feel good about with the August data in terms of the unemployment picture, but there is a silver lining in that the August PCI is still far from double-dip territory."

...

“The restocking of inventory and exceptional growth in imports that were helping drive the transportation of goods and materials appears to be over,” said Craig Manson, senior vice president and index expert for Ceridian.

...

The PCI is based on an analysis of real-time diesel fuel consumption data from over the road trucking tracked by Ceridian ...

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the index since January 1999.

This is a new index, and doesn't have much of a track record in real time, although the data appears to suggest that the recovery has slowed - even stalled - over the last 4 months.

DataQuick: SoCal home sales decline in August

by Calculated Risk on 9/14/2010 02:57:00 PM

From DataQuick: Southern California Home Sales Fall in August; Median Price Dips

Southland home sales fell last month to the lowest level for an August in three years and the second-lowest in 18, the result of a worrisome job market and a lost sense of urgency among home shoppers. ... [sales were] down 2.1 percent from 18,946 sales in July, and down 13.8 percent from 21,502 sales in August 2009.The DataQuick data includes new home sales, but this suggests existing home sales in August were weak nationwide. I'll be looking for the compilation of regional reports from Tom Lawler!

Last month’s sales were the lowest for the month of August since 2007, when 17,755 homes sold, and the second-lowest since August 1992, when 16,379 sold. Last month’s sales were 31.5 percent lower than the August average of 27,070 sales since 1988, when DataQuick’s statistics begin. The average change in sales between July and August is a gain of 3.9 percent ...

“The loss of home buyer tax credits explains much of the sales weakness over the past two months. But other factors are suppressing sales, too, such as the lack of meaningful job growth and potential buyers’ concerns about job security. Also, for many out home shopping now, there’s little beyond ultra-low mortgage rates to pressure them to buy sooner rather than later, especially in areas where the number of homes for sale is climbing,” said John Walsh, MDA DataQuick president.

Goldman: Fed may announce QE2 as soon as November

by Calculated Risk on 9/14/2010 12:53:00 PM

From the WSJ: Goldman: Fed May Announce New Asset Purchases in November

“We don’t expect this at the Sept. 21 meeting, but in November or December there’s certainly a possibility that it will be announced,” Jan Hatzius, chief economist at the bank, said Tuesday. He added the Fed is likely to buy U.S. Treasurys worth around $1.0 trillion to kick-start the economy.I think it will take more evidence of a slowing economy or further disinflation for Fed Chairman Bernanke to persuade other members of the FOMC to embark on QE2.

...

[Goldman] expects the U.S. unemployment rate to creep back up to 10% by early 2011 from 9.6% in August and to stay around that level for most of the year.

Perhaps the unemployment rate ticking up in the September employment report will be enough, but that is the only employment report scheduled to be released before the two day FOMC meeting in November (on Nov 2nd and 3rd). The October employment report will be release on November 5th - two days after the FOMC meeting.

The advance Q3 GDP report (advance estimate) will be released on October 29th, and if that report shows further slowing - that might be enough.

NFIB: Small Businesses slightly less pessimistic

by Calculated Risk on 9/14/2010 10:08:00 AM

From NFIB: Small Business Confidence Remains Low

The National Federation of Independent Business Index of Small Business Optimism gained 0.7 points in August*, rising to 88.8. Most of the improvement was accounted for by gains in expected real sales and expectations for business conditions six months out, the two components that lowered the index in July. But despite their improvements, both measures are still in recession territory.On employment:

“Small business owners are expecting sub-par growth in the second half of 2010,” said Bill Dunkelberg, NFIB’s chief economist.

Average employment growth per firm has been negative since April of 2007 and remained negative for 10 of the 12 following quarterly (first month in each quarter) readings. August brought no improvement, with reported job loss averaging negative 0.3 employees per firm (seasonally adjusted).On capital spending:

The frequency of reported capital outlays over the past six months fell one point to 44 percent of all firms, again hitting the 35-year record low. ... Seventy-three percent of all owners said the current period was NOT a good time to expand.And the key problem:

“What businesses need are customers, giving them a reason to hire and make capital expenditures and then they may have the need to borrow to support those activities,” said Dunkelberg.Note: Small businesses have a large percentage of real estate related companies.

The key problem remains excess capacity - and a lack of customers. There is no reason to invest and hire until business picks up.

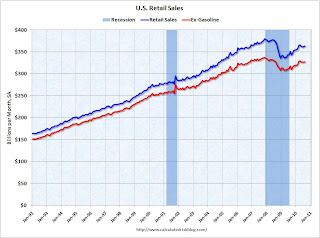

Retail Sales increase in August

by Calculated Risk on 9/14/2010 08:30:00 AM

On a monthly basis, retail sales increased 0.4% from July to August (seasonally adjusted, after revisions), and sales were up 3.6% from August 2009. Retail sales increased 0.6% ex-autos.  Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows retail sales since 1992. This is monthly retail sales, seasonally adjusted (total and ex-gasoline).

Retail sales are up 8.4% from the bottom, but still off 4.3% from the pre-recession peak.

Retail sales are still below the April level - and have mostly moved sideways for six months. The second graph shows the year-over-year change in retail sales (ex-gasoline) since 1993.

The second graph shows the year-over-year change in retail sales (ex-gasoline) since 1993.

Retail sales ex-gasoline increased by 3.0% on a YoY basis (3.6% for all retail sales). The year-over-year comparisons were easier earlier this year since retail sales collapsed in late 2008.

Here is the Census Bureau report:

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for August, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $363.7 billion, an increase of 0.4 percent (±0.5%)* from the previous month, and 3.6 percent (±0.5%) above August 2009. Total sales for the June through August 2010 period were up 4.7 percent (±0.3%) from the same period a year ago. The June to July 2010 percent change was revised from +0.4 percent (±0.5%)* to +0.3 percent (±0.2%).

TARP Deadbeat list grows to more than 120 banks

by Calculated Risk on 9/14/2010 12:01:00 AM

From Brady Dennis at the WaPo: More banks missing TARP dividend payments

The latest report ... shows that more than 120 institutions ... have missed their scheduled quarterly dividend payments ... a record six banks each missed six dividend payments. Saigon National Bank in Southern California has missed seven.

...

In addition, five banks that received capital injections from the controversial $700 billion Troubled Assets Relief Program have failed altogether, making it highly unlikely that taxpayers will recover the nearly $3 billion poured into those institutions.

Monday, September 13, 2010

Capital One CEO: "Very cautious about the housing market"

by Calculated Risk on 9/13/2010 07:15:00 PM

From William Alden at HuffPo: Home Prices Set To Fall Further: Richard Fairbank, Capital One CEO

"I think we feel very cautious about the housing market," [Capital One CEO Richard Fairbank] said. "I think that even despite some of the recent months where home prices have gone up, I think it's a very plausible case for home prices to go back down again."I think house prices started falling again in July, but it might take some time before we see prices falling in the repeat sales index. CoreLogic will probably release their July HPI this week, and that might show declining prices - but that is a weighted average of May, June and July.

...

"We are managing to a view that home prices are more likely to be headed down rather than up."

Investment Contributions to GDP: Leading and Lagging Sectors

by Calculated Risk on 9/13/2010 03:14:00 PM

By request, the following graph is an update to: The Investment Slump in Q2 2009

The following graph shows the rolling 4 quarter contribution to GDP from residential investment, equipment and software, and nonresidential structures. This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy.

For the following graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. The usual pattern - both into and out of recessions is - red, green, blue. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Residential Investment (RI) made a positive contribution to GDP in the Q2 2010, but RI will be a drag on GDP again in Q3.

RI was positively impacted in Q2 by the housing tax credit in two ways: first, builders rushed to complete homes by the end of June, and, second, real estate agent commissions were boosted in Q2 and will decline sharply in Q3 (just look at existing home sales in July).

The rolling four quarter change for RI just turned positive, but will turn negative again in Q3.

Equipment and software investment has made a significant positive contribution to GDP for four straight quarters (it is coincident).

The contribution from nonresidential investment in structures was flat in Q2 - only because of a surge of investment for petroleum and natural gas - while investment in hotels, malls and office buildings continued to decline. As usual nonresidential investment in structures is the last sector to recover.

The key leading sector - residential investment - has lagged the recovery because of the huge overhang of existing inventory. Usually RI is a strong contributor to GDP growth and employment in the early stages of a recovery, but not this time - and this is a key reason why the recovery has been sluggish so far.

On Retail Seasonal Hiring

by Calculated Risk on 9/13/2010 01:04:00 PM

October is the first month for seasonal retail hiring - and most hiring happens in November. So it is probably time to start looking ahead.

According to a survey released last week, most retailers plan on hiring about the same number of seasonal workers as last year (a weak year), however about one-fifth expect to hire more.

Here was an article from the WSJ: Holiday Job Outlook Stays Flat

Most major American retailers plan to hire the same number of temporary holiday workers as last year, according to a survey by a top industry consultant, underscoring that store chains continue to view the coming season with caution.

Still, the annual Hay Group survey ... found that more than one-fifth of respondents expected to hire more seasonal help than in 2009 ...

Click on graph for larger image.

Click on graph for larger image.The first graph shows that seasonally adjusted (blue) and not seasonally adjusted (red) retail employment. There is a clear seasonal pattern (no surprise).

Not only is overall retail employment down, but seasonal hiring was very low in 2008, and still weak in 2009.

The second graph shows the seasonal hiring by the three key months (October, November and December).

The second graph shows the seasonal hiring by the three key months (October, November and December). Although seasonal hiring bounced back last year, it was still the second weakest year since 1989 (only 2008 was worse). From this early survey, it sounds like there should be some increase in seasonal hiring - but it will still be a very weak year.

House Prices and Foreclosures

by Calculated Risk on 9/13/2010 08:48:00 AM

Nick Timiraos has an excellent article on house prices and foreclosures at the WSJ: Banks' Plans for Foreclosed Homes Will Drive Market

The speed at which house prices fall over the next few months could depend ... on how banks decide to manage the huge number of foreclosed homes they own or may take from delinquent borrowers in the near future.Usually house prices are sticky downwards and decline over several years, but the flood of foreclosures in late 2008 pushed down prices significantly in lower priced areas (Tom Lawler called this "destickification").

Unlike home owners, banks often are much quicker to slash prices to unload properties quickly.

...

"We see the perfect storm brewing with rising supply and falling demand," said Ivy Zelman ... She estimated that distressed sales could account for half of the market by year-end if traditional sales didn't rebound.

Something similar could happen again, especially in some mid-to-high end areas where prices are still too high, although it won't be the flood of foreclosures we saw at the end of 2008. But prices will fall.

There is much more in the article ...

Sunday, September 12, 2010

Geithner on Exchange Rate with China

by Calculated Risk on 9/12/2010 11:45:00 PM

From the WSJ: China Has Done ‘Very Little’ on Exchange Rate: Geithner

“China took the very important step in June of signaling that they’re going to let the exchange rate start to reflect market forces. But they’ve done very, very little, they’ve let it move very, very little in the interim."And from Paul Krugman at the NY Times: China, Japan, America

Back in June, Timothy Geithner, the Treasury secretary, praised China’s announcement that it would move to a more flexible exchange rate. Since then, the renminbi has risen a grand total of 1, that’s right, 1 percent against the dollar — with much of the rise taking place in just the past few days, ahead of planned Congressional hearings on the currency issue.Obviously China is a "currency manipulator" ... now what?

Geithner: "Important to avoid premature policy restraint"

by Calculated Risk on 9/12/2010 07:59:00 PM

A few excerpts from a WSJ interview with Treasury Secretary Timothy Geithner: Geithner Urges Action on Economy

"[The] typical error most countries make coming out of a financial crisis is they shift too quickly to premature restraint. ... It is very important for us to avoid that mistake. If the government does nothing going forward, then the impact of policy in Washington will shift from supporting economic growth to hurting economic growth."And on tax cuts for high income earners:

"We just don't think it would be responsible for this country, given the size of our future deficits, and given the substantial burden the middle class has been bearing over the past decade in particular, to go out and borrow $700 billion from our children so we can sustain those Bush tax cuts that only go to the wealthiest 2% of Americans."I agree with Geithner on both points.

Schedule for Week of Sept 12th

by Calculated Risk on 9/12/2010 03:40:00 PM

The key releases this week will be retail sales (on Tues for August), Industrial Production (Weds for August) and the Empire state and Philly Fed surveys (Weds and Thurs for Sept).

Possibly on Monday (update: I've been told Tuesday): Ceridian-UCLA Pulse of Commerce Index™ This is the diesel fuel index for August (a measure of transportation).

CoreLogic House Price Index for July. This release could show the first signs of price declines in July, although the index is a weighted 3 month average for May, June and July.

No releases scheduled.

8:30 AM: Retail Sales for August. The consensus is for a 0.3% increase from July.

Early: NFIB Small Business Survey for August. This survey has been showing declining optimism in the small business sector.

10:00 AM: Manufacturing and Trade: Inventories and Sales for July. Consensus is for a 0.6% increase in inventories in July.

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index declined sharply following the expiration of the tax credit, and the index has only recovered slightly over the last few weeks - suggesting reported home sales in August and September will be weak.

8:30 AM: Empire Manufacturing Survey for Sept. The consensus is for a reading of 5.0, down from 7.1 in August. These regional surveys have been showing a slowdown in manufacturing and are being closely watched right now.

9:15 AM: Industrial Production and Capacity Utilization for August. The consensus is for a 0.2% increase in August.

8:30 AM: The initial weekly unemployment claims report will be released. Consensus is for a slight increase to 455K from 451K last week. Claims for nine states were estimated last week because of the holiday.

8:30 AM: Producer Price Index for August. The consensus is for a 0.3% increase in prices.

10:00 AM: Philly Fed Survey for September. This survey declined sharply over the last few months, and showed contraction last month for the first time since July 2009. The consensus is for an increase to 3.8 (slow expansion) from minus 7.7 in August.

8:30 AM: Consumer Price Index for August. The consensus is for a 0.3% increase in prices. This is being closely watched for further disinflation, and also because Q3 is the quarter the annual annual cost-of-living adjustment (COLA) is calculated for Social Security (probably no change in 2011).

9:55 AM: Reuters/University of Mich Consumer Sentiment preliminary for September. The consensus is for a slight increase to 70.0 from 68.9 in August.

12:00 PM: Q2 Flow of Funds Report from the Federal Reserve.

After 4:00 PM: The FDIC has only closed one bank over the last 3 weeks. The pace will probably pickup soon ...

Report: Bank regulators reach agreement on Basel III capital requirements

by Calculated Risk on 9/12/2010 12:18:00 PM

The details will be released later today, but here is an overview from the Financial Times: Regulators agree to reforms on bank capital

Basel III ... is expected to include a new minimum core tier one ratio for banks worldwide. ... The current minimum is 2 per cent.Here is an article from the WSJ: Bank Regulators Reach Deal on New Capital Rules

[The] proposal [was] for a new minimum of 4½ per cent [with] an additional buffer of 2½ per cent ... Banks within the buffer zone would face restrictions on their ability to pay dividends and discretionary bonuses.

excerpt with permission

The details will be released later, and the agreement is expected to be approved in November. This will probably lead to more banks raising capital.

Summary for Week ending Sept 11th

by Calculated Risk on 9/12/2010 09:00:00 AM

It was a light week for economic news ...

The Census Bureau reports:

[T]otal July exports of $153.3 billion and imports of $196.1 billion resulted in a goods and services deficit of $42.8 billion, down from $49.8 billion in June, revised.

Click on graph for larger image.

Click on graph for larger image.The first graph shows the monthly U.S. exports and imports in dollars through June 2010.

Although imports declined in July, imports have been increasing much faster than exports.

The second graph shows the U.S. trade deficit, with and without petroleum, through July.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.The decrease in the deficit in July was across the board, although the oil deficit only declined slightly. The trade gap with China declined slightly to $25.92 billion from $26.15 billion in June - essentially unchanged.

This is the 2nd largest monthly trade deficit since the 2008 collapse in trade.

The Federal Reserve reports:

In July, total consumer credit decreased at an annual rate of 1-3/4 percent. Revolving credit decreased at an annual rate of 6-1/4

percent, and nonrevolving credit increased at an annual rate of 1/2 percent.

This graph shows the increase in consumer credit since 1978. The amounts are nominal (not inflation adjusted).

This graph shows the increase in consumer credit since 1978. The amounts are nominal (not inflation adjusted).Revolving credit (credit card debt) is off 15.2% from the peak. Non-revolving debt (auto, furniture, and other loans) is off 1.1% from the peak. Note: Consumer credit does not include real estate debt.

Best wishes to all.

Saturday, September 11, 2010

OECD Paper: "The EU Stress Test and Sovereign Debt Exposures"

by Calculated Risk on 9/11/2010 07:52:00 PM

Here is a new paper on EU Sovereign debt exposures. (ht Mark Whitehouse at the WSJ: Number of the Week: Hiding Europe’s Unpleasant Details)

From Blundell-Wignall, A. and P. Slovik (2010), “The EU Stress Test and Sovereign Debt Exposures”

The EU-wide stress test did not include haircuts for sovereign debt held in the banking books of banks on the grounds that over the 2 years considered default is virtually impossible in the presence of the EFSF [European Financial Stability Facility Special Purpose Vehicle], which is certainly large enough to meet funding needs of the main countries of concern over that period.

The haircuts applied to the trading book in the stress test are shown in the first block of Table 1. The trading book exposures (not reported in the stress test paper) are also shown. The EU wide loss from the haircut is around €26. bn. The contribution of the 5 countries where most of the market focus has been (Greece, Portugal, Ireland, Italy and Spain) is only €14.4bn.

Click on table for larger image in new window.

Click on table for larger image in new window.A different picture emerges when we consider the banking book. First it is important to note that the EU banking book sovereign exposures are very much larger than those of the trading book—around 83% of the total. If the same haircuts are applied to these exposures the loss amounts to €139bn, or 12% of the Tier 1 capital of the EU banks at the end of 2009 (and €165bn and over 14% of Tier 1 if trading book losses are added in). The haircuts of the 5 countries of market focus amount to €75.8bn in the banking book, and €90.2bn if the trading book amount is added in. This is around 8% of EU Tier 1 capital of stress tested banks.What happens in less than 2 years when the European Financial Stability Facility Special Purpose Vehicle is no longer providing funding?

...

This study has shown that most of the sovereign debt is held on the banking books of banks, whereas the EU stress test only considered their small trading book exposures. Sovereign debt held in the banking book cannot be ignored however. First, individual bank failures would see latent losses on the trading book realized, a fact that creditors and equity investors need to take into account. Second, and more importantly, the market is not prepared to give a zero probability to debt restructurings beyond the period of the stress test and/or the period after which the role of the EFSF SPV comes to an end. The main reasons for this are: the very large job ahead for fiscal consolidation in a period of weak economic growth; and the apparent difficulty of achieving structural/competitiveness reforms in some countries in a short period of time. The paper also showed that excessively exposed banks in principle can reduce their exposure by not re-financing maturing sovereign debt, with the government funding gap being met instead by the SPV. This would have the effect of transferring sovereign risk from the bank concerned to the public sector.