RSS Feed

RSS Feed by Calculated Risk on 6/25/2025 02:11:00 PM

Wednesday, June 25, 2025

A few comments on the Seasonal Pattern for House Prices

Another update ... a few key points:

1) There is a clear seasonal pattern for house prices.

2) The surge in distressed sales during the housing bust distorted the seasonal pattern. This was because distressed sales (at lower price points) happened at a steady rate all year, while regular sales followed the normal seasonal pattern. This made for larger swings in the seasonal factor during the housing bust.

3) The seasonal swings have increased recently without a surge in distressed sales.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the month-to-month change in the NSA Case-Shiller National index since 1987 (through April 2025). The seasonal pattern was smaller back in the '90s and early '00s and increased once the bubble burst.

The seasonal swings declined following the bust, however the pandemic price surge changed the month-over-month pattern.

Click on graph for larger image.

Click on graph for larger image.This graph shows the month-to-month change in the NSA Case-Shiller National index since 1987 (through April 2025). The seasonal pattern was smaller back in the '90s and early '00s and increased once the bubble burst.

The seasonal swings declined following the bust, however the pandemic price surge changed the month-over-month pattern.

The peak MoM increase in NSA prices this year was the smallest since 2008!

The second graph shows the seasonal factors for the Case-Shiller National index since 1987. The factors started to change near the peak of the bubble, and really increased during the bust since normal sales followed the regular seasonal pattern - and distressed sales happened all year.

The second graph shows the seasonal factors for the Case-Shiller National index since 1987. The factors started to change near the peak of the bubble, and really increased during the bust since normal sales followed the regular seasonal pattern - and distressed sales happened all year.

The swings in the seasonal factors were decreasing following the bust but have increased again recently - this time without a surge in distressed sales.

The second graph shows the seasonal factors for the Case-Shiller National index since 1987. The factors started to change near the peak of the bubble, and really increased during the bust since normal sales followed the regular seasonal pattern - and distressed sales happened all year.

The second graph shows the seasonal factors for the Case-Shiller National index since 1987. The factors started to change near the peak of the bubble, and really increased during the bust since normal sales followed the regular seasonal pattern - and distressed sales happened all year. The swings in the seasonal factors were decreasing following the bust but have increased again recently - this time without a surge in distressed sales.

Newsletter: New Home Sales Decrease to 623,000 Annual Rate in May

by Calculated Risk on 6/25/2025 10:51:00 AM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales Decrease to 623,000 Annual Rate in May

Brief excerpt:

The Census Bureau reported New Home Sales in May were at a seasonally adjusted annual rate (SAAR) of 623 thousand. The previous three months were revised down.There is much more in the article.

...

The next graph shows new home sales for 2024 and 2025 by month (Seasonally Adjusted Annual Rate). Sales in May 2025 were down 6.3% from May 2024.

New home sales, seasonally adjusted, have been down year-over-year in 4 of the last 5 months.

New Home Sales Decrease to 623,000 Annual Rate in May

by Calculated Risk on 6/25/2025 10:00:00 AM

The Census Bureau reports New Home Sales in May were at a seasonally adjusted annual rate (SAAR) of 623 thousand.

The previous three months were revised down.

Sales of new single-family houses in May 2025 were at a seasonally-adjusted annual rate of 623,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 13.7 percent below the April 2025 rate of 722,000, and is 6.3 percent below the May 2024 rate of 665,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales were below pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply increased in May to 9.8 months from 8.3 months in April.

The months of supply increased in May to 9.8 months from 8.3 months in April. The all-time record high was 12.2 months of supply in January 2009. The all-time record low was 3.3 months in August 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally-adjusted estimate of new houses for sale at the end of May 2025 was 507,000. This is 1.4 percent above the April 2025 estimate of 500,000, and is 8.1 percent above the May 2024 estimate of 469,000.Sales were well below expectations of 710 thousand SAAR and sales for the three previous months were revised down. I'll have more later today.

This represents a supply of 9.8 months at the current sales rate. The months' supply is 18.1 percent above the April 2025 estimate of 8.3 months, and is 15.3 percent above the May 2024 estimate of 8.5 months. "

MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

by Calculated Risk on 6/25/2025 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 1.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 20, 2025. This week’s results include an adjustment for the Juneteenth holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 1.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 10 percent compared with the previous week. The Refinance Index increased 3 percent from the previous week and was 29 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 0.4 percent from one week earlier. The unadjusted Purchase Index decreased 11 percent compared with the previous week and was 12 percent higher than the same week one year ago.

“The combination of the ongoing conflict in the Middle East, current economic conditions, and last week’s FOMC meeting resulted in slightly lower Treasury rates on average. However, mortgage rates still edged higher but remained in the same narrow range, with the 30-year fixed rate increasing to 6.88 percent last week,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Applications increased slightly overall driven by FHA refinances, but conventional applications saw declines over the week. The average loan size for purchase applications declined to $436,300, the lowest level since January 2025, driven by decreasing conventional purchase loan sizes.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.88 percent from 6.84 percent, with points decreasing to 0.63 from 0.66 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is up 12% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is still depressed, but above the lows of October 2023 and is 9% above the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

The refinance index increased but remained very low.

Tuesday, June 24, 2025

Wednesday: New Home Sales, Fed Chair Powell Testimony

by Calculated Risk on 6/24/2025 07:45:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 10:00 AM, New Home Sales for May from the Census Bureau. The consensus is for 710 thousand SAAR, down from 743 thousand in April.

• Also at 10:00 AM, Testimony, Fed Chair Jerome Powell, Semiannual Monetary Policy Report to Congress, Before the U.S. Senate Committee on Banking, Housing, and Urban Affairs

ICE First Look at May Mortgage Performance: "Delinquencies Hold Steady and Foreclosure Sales Rise to Highest Level Since Early 2023"

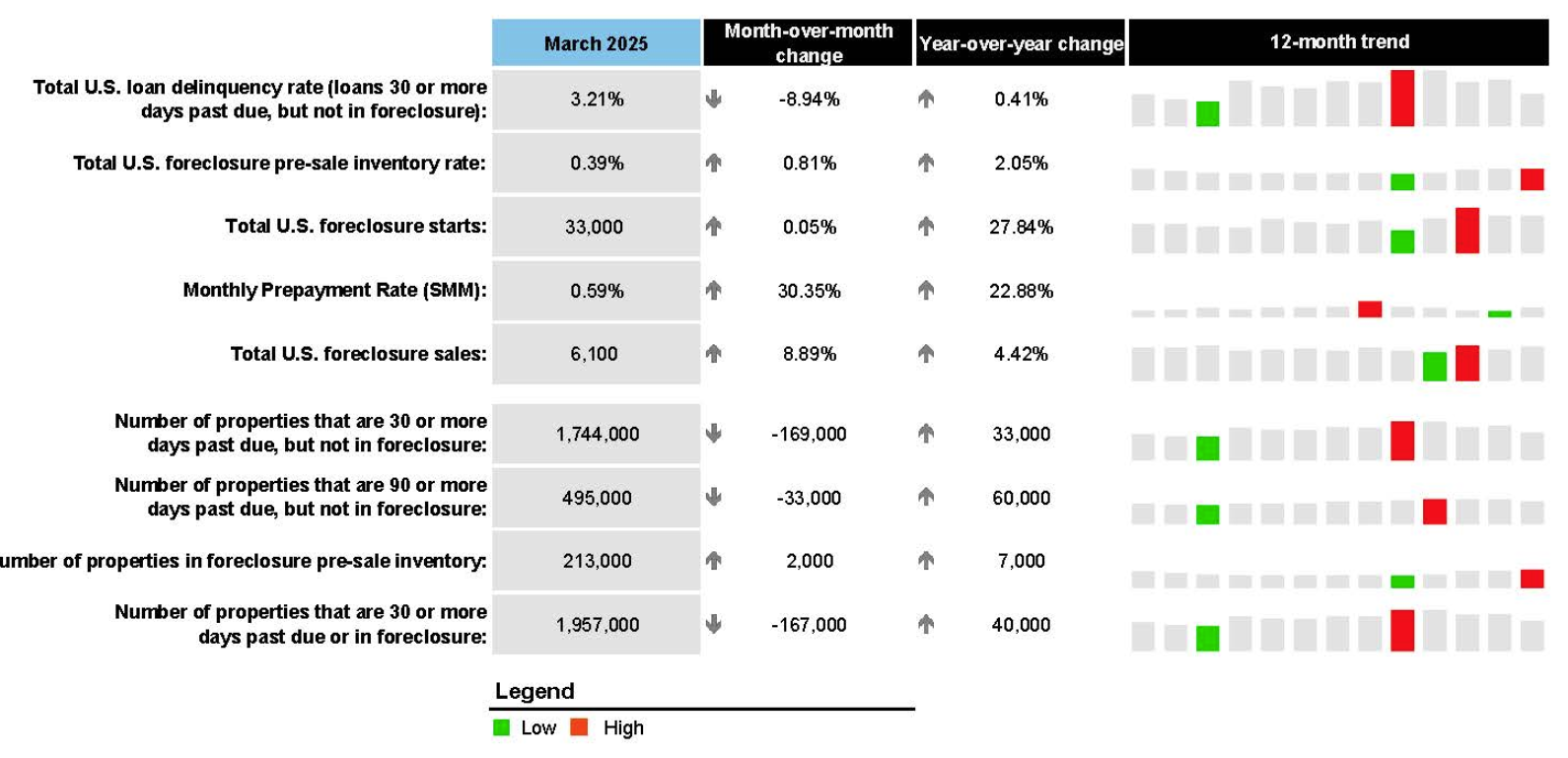

by Calculated Risk on 6/24/2025 04:06:00 PM

From Intercontinental Exchange: ICE First Look at Mortgage Performance: Delinquencies Hold Steady and Foreclosure Sales Rise to Highest Level Since Early 2023

Intercontinental Exchange, Inc. (NYSE:ICE) ... today released its May 2025 ICE First Look, which shows that delinquencies and foreclosure activity continues to trend slightly higher on an annual basis despite some seasonal and disaster recovery related improvement.

The ICE First Look reports on month-end delinquency, foreclosure and prepayment statistics sourced from its loan-level database, which covers a majority of the U.S. mortgage market. Key takeaways from this month’s findings include:

• The national delinquency rate ticked down 2 basis points (bps) to 3.20% in May, though it is up 5.2% (16 bps) year over year (YoY).

• Serious delinquencies – loans 90+ days past due but not in foreclosure – improved seasonally for the fifth consecutive month, but are still up 56K (14%) from the same time last year.

• Disaster-related delinquencies also improved, with those related to the 2024 hurricane season falling by nearly 5K (26%) month over month (MoM) and Los Angeles wildfire-related delinquencies falling by a more modest 9% MoM.

• Foreclosure starts and active foreclosure inventories climbed YoY, with May’s 7K foreclosure sales marking the largest single-month volume in more than two years.

• Prepayment activity, as measured by single month mortality, inched up to 0.71%, the highest level since October 2024, driven by a seasonal rise in home sale-related prepayments. Prepayments were up 23.4% YoY.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here is a table from ICE.

Hotels: Occupancy Rate Decreased 2.4% Year-over-year

by Calculated Risk on 6/24/2025 01:16:00 PM

The U.S. hotel industry reported mostly negative year-over-year comparisons, according to CoStar’s latest data through 14 June. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

8-14 June 2025 (percentage change from comparable week in 2024):

• Occupancy: 68.6% (-2.4%)

• Average daily rate (ADR): US$163.43 (+0.6%)

• Revenue per available room (RevPAR): US$112.11 (-1.8%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025, blue is the median, and dashed light blue is for 2024. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking behind both last year and the median rate for the period 2000 through 2024 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average will increase during the summer travel season; however, we will likely see a hit to occupancy during the summer months due to less international tourism.

Newsletter: Case-Shiller: National House Price Index Up 2.7% year-over-year in April

by Calculated Risk on 6/24/2025 09:39:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Case-Shiller: National House Price Index Up 2.7% year-over-year in April

Excerpt:

S&P/Case-Shiller released the monthly Home Price Indices for April ("April" is a 3-month average of February, March and April closing prices). February closing prices include some contracts signed in December, so there is a significant lag to this data. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The MoM decrease in the seasonally adjusted (SA) Case-Shiller National Index was at -0.51% (a -4.8% annual rate). This was the second consecutive MoM decrease.

On a seasonally adjusted basis, prices increased month-to-month in just 5 of the 20 Case-Shiller cities. San Francisco has fallen 6.4% from the recent peak, Tampa is down 2.7% from the peak, and Denver down 2.0%.

Case-Shiller: National House Price Index Up 2.7% year-over-year in April

by Calculated Risk on 6/24/2025 09:00:00 AM

S&P/Case-Shiller released the monthly Home Price Indices for April ("April" is a 3-month average of February, March and April closing prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

From S&P S&P CoreLogic Case-Shiller Index Records 2.7% Annual Gain in April 2025

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 2.7% annual return for April, down from a 3.4% annual gain in the previous month. The 10-City Composite saw an annual increase of 4.1%, down from a 4.8% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 3.4%, down from a 4.1% increase in the previous month. New York again reported the highest annual gain among the 20 cities with a 7.9% increase in April, followed by Chicago and Detroit with annual increases of 6.0% and 5.5%, respectively. Tampa posted the lowest return, falling 2.2%.

...

The pre-seasonally adjusted U.S. National Index saw slight upward trends in April, posting gains of 0.6%. The 10-City Composite and 20-City Composite Indices both reported gains of 0.7%.

After seasonal adjustment, the U.S. National Index posted a decrease of -0.4%. Both the 10-City Composite and the 20-City Composite Indices saw a -0.3% decrease.

“The housing market continued its gradual deceleration in April, with annual price gains slowing to their most modest pace in nearly two years,” said Nicholas Godec, CFA, CAIA, CIPM, Head of Fixed Income Tradables & Commodities at S&P Dow Jones Indices. “What's particularly striking is how this cycle has reshuffled regional leadership—markets that were pandemic darlings are now lagging, while historically steady performers in the Midwest and Northeast are setting the pace. This rotation signals a maturing market that's increasingly driven by fundamentals rather than speculative fervor.

“The National Composite Index posted a 2.7% annual gain in April, marking its slowest year-over-year appreciation since mid-2023. This deceleration was broad-based, with the 20-City Composite advancing 3.4% and the 10-City Composite up 4.1%—both substantially below their recent peaks. The composition of these gains tells an important story: Approximately 1.7 percentage points of April's annual increase occurred over the past six months, indicating that price momentum has been concentrated in the recent spring selling season rather than sustained throughout the year. "

emphasis added

Click on graph for larger image.

Click on graph for larger image. The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index was down 0.3% in April (SA). The Composite 20 index was down 0.3% (SA) in April.

The National index was down 0.4% (SA) in April.

The second graph shows the year-over-year change in all three indices.

The second graph shows the year-over-year change in all three indices.The Composite 10 NSA was up 4.1% year-over-year. The Composite 20 NSA was up 3.4% year-over-year.

The National index NSA was up 2.7% year-over-year.

Annual price changes were lower than expectations. I'll have more later.

Monday, June 23, 2025

Tuesday: Case-Shiller House Prices, Fed Chair Powell Testimony

by Calculated Risk on 6/23/2025 08:11:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Lowest Since May 1st

From Matthew Graham at Mortgage News Daily: Mortgage Rates Lowest Since May 1st

Mortgage rates ended the previous week roughly in line with the best levels since May 1st. Today's modest improvement made it official.Tuesday:

Mortgage rates are primarily a function of trading levels in the bond market and bonds have had a few reasons to move at the start of the new week.

There's a small case to be made that U.S. involvement in the conflict between Israel and Iran contributed to bond market strength and, thus, lower mortgage rates today. [30 year fixed 6.84%]

emphasis added

• At 9:00 AM ET, S&P/Case-Shiller House Price Index for April. The National index was up 3.4% year-over-year in March.

• Also at 9:00 AM, FHFA House Price Index for April. This was originally a GSE only repeat sales, however there is also an expanded index.

• At 10:00 AM, Richmond Fed Survey of Manufacturing Activity for June.

• Also at 10:00 AM, State Employment and Unemployment (Monthly) for May 2024.

• Also at 10:00 AM, Testimony, Fed Chair Jerome Powell, Semiannual Monetary Policy Report to Congress, Before the U.S. House Financial Services Committee