RSS Feed

RSS Feed by Calculated Risk on 3/03/2025 10:17:00 AM

Monday, March 03, 2025

Construction Spending Decreased 0.2% in January

From the Census Bureau reported that overall construction spending decreased:

Construction spending during January 2025 was estimated at a seasonally adjusted annual rate of $2,192.5 billion, 0.2 percent below the revised December estimate of $2,196.0 billion. The January figure is 3.3 percent above the January 2024 estimate of $2,122.2 billion.Private spending decreased and public spending increased:

emphasis added

Spending on private construction was at a seasonally adjusted annual rate of $1,686.0 billion, 0.2 percent below the revised December estimate of $1,690.1 billion. ...

In January, the estimated seasonally adjusted annual rate of public construction spending was $506.6 billion, 0.1 percent above the revised December estimate of $505.9 billion.

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Private residential (red) spending is 4.9% below the peak in 2022.

Private non-residential (blue) spending is at a new peak.

Public construction spending is 0.1% below the peak in November 2024.

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is up 3.1%. Private non-residential spending is up 1.8% year-over-year. Public spending is up 5.9% year-over-year.

This was below consensus expectations; however, spending for the previous two months was revised up.

ISM® Manufacturing index Decreased to 50.3% in February

by Calculated Risk on 3/03/2025 10:00:00 AM

(Posted with permission). The ISM manufacturing index indicated expansion. The PMI® was at 50.3% in February, down from 50.9% in January. The employment index was at 47.6%, down from 50.3% the previous month, and the new orders index was at 48.6%, down from 52.1%.

From ISM: Manufacturing PMI® at 50.3%

February 2025 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector expanded for the second month in a row in February after 26 consecutive months of contraction, say the nation's supply executives in the latest Manufacturing ISM® Report On Business®.This suggests manufacturing expanded in February. This was below the consensus forecast.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee:

“The Manufacturing PMI® registered 50.3 percent in February, 0.6 percentage point lower compared to the 50.9 percent recorded in January. The overall economy continued in expansion for the 58th month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index dropped back into contraction territory after expanding for three months, registering 48.6 percent, 6.5 percentage points lower than the 55.1 percent recorded in January. The February reading of the Production Index (50.7 percent) is 1.8 percentage points lower than January’s figure of 52.5 percent. The index expanded for the second month in a row after eight months in contraction. The Prices Index surged further into expansion (or ‘increasing’) territory, registering 62.4 percent, up 7.5 percentage points compared to the reading of 54.9 percent in January. The Backlog of Orders Index registered 46.8 percent, up 1.9 percentage points compared to the 44.9 percent recorded in January. The Employment Index registered 47.6 percent, down 2.7 percentage points from January’s figure of 50.3 percent.

emphasis added

Housing March 3rd Weekly Update: Inventory down 0.1% Week-over-week, Up 28.3% Year-over-year

by Calculated Risk on 3/03/2025 08:11:00 AM

Altos reports that active single-family inventory was down 0.1% week-over-week.

Inventory is now up 2.4% from the seasonal bottom seven weeks ago in January and should start increasing seasonally in March.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 28.3% compared to the same week in 2024 (last week it was up 28.7%), and down 21.8% compared to the same week in 2019 (last week it was down 21.9%).

Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly!

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of Feb 28th, inventory was at 639 thousand (7-day average), compared to 640 thousand the prior week.

Mike Simonsen discusses this data regularly on Youtube

Sunday, March 02, 2025

Monday: ISM Mfg, Construction Spending, Vehicle Sales

by Calculated Risk on 3/02/2025 06:22:00 PM

Weekend:

• Schedule for Week of March 2, 2025

Monday:

• At 10:00 AM ET, ISM Manufacturing Index for February. The consensus is for the ISM to be at 50.8, down from 50.9 in January.

• At 10:00 AM, Construction Spending for January. The consensus is for a 0.2% increase in construction spending.

• All day, Light vehicle sales for February. Sales were at 15.6 million in January (Seasonally Adjusted Annual Rate). The consensus is for an increase in sales to 15.9 million SAAR.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 17 and DOW futures are up 55 (fair value).

Oil prices were down over the last week with WTI futures at $70.10 per barrel and Brent at $73.16 per barrel. A year ago, WTI was at $81, and Brent was at $85 - so WTI oil prices are down about 15% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.04 per gallon. A year ago, prices were at $3.33 per gallon, so gasoline prices are down $0.29 year-over-year.

Hotels: Occupancy Rate Decreased 2.7% Year-over-year

by Calculated Risk on 3/02/2025 09:19:00 AM

The U.S. hotel industry reported mixed year-over-year comparisons, according to CoStar’s latest data through 22 February. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

16-22 February 2025 (percentage change from comparable week in 2024):

• Occupancy: 60.3% (-2.7%)

• Average daily rate (ADR): US$159.90 (+2.5%)

• Revenue per available room (RevPAR): US$96.49 (-0.3%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025, blue is the median, and dashed light blue is for 2024. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking last year and is lower than the median rate for the period 2000 through 2024 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average will increase seasonally for the next several weeks.

Saturday, March 01, 2025

Real Estate Newsletter Articles this Week: New Home Sales Decrease to 657,000 Annual Rate in January

by Calculated Risk on 3/01/2025 02:22:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• New Home Sales Decrease to 657,000 Annual Rate in January

• Case-Shiller: National House Price Index Up 3.9% year-over-year in December

• Inflation Adjusted House Prices 1.0% Below 2022 Peak

• Freddie Mac House Price Index Increased in January; Up 3.9% Year-over-year

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of March 2, 2025

by Calculated Risk on 3/01/2025 08:11:00 AM

The key report scheduled for this week is the February employment report.

Fed Chair Powell speaks on the economic outlook on Friday.

10:00 AM: ISM Manufacturing Index for February. The consensus is for the ISM to be at 50.8, down from 50.9 in January.

10:00 AM: Construction Spending for January. The consensus is for a 0.2% increase in construction spending.

All day: Light vehicle sales for February. Sales were at 15.6 million in January (Seasonally Adjusted Annual Rate). The consensus is for an increase in sales to 15.9 million SAAR.

All day: Light vehicle sales for February. Sales were at 15.6 million in January (Seasonally Adjusted Annual Rate). The consensus is for an increase in sales to 15.9 million SAAR.This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the January sales rate.

No major economic releases scheduled.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for February. This report is for private payrolls only (no government). The consensus is for 140,000 payroll jobs added in February, down from 183,000 added in January.

10:00 AM: the ISM Services Index for February.

2:00 PM: the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 234 initial claims down from 242 thousand last week.

8:30 AM: U.S. International Trade in Goods and Services for January from the Census Bureau.

8:30 AM: U.S. International Trade in Goods and Services for January from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

TThe consensus is for a record U.S. trade deficit of $128.3 billion from $98.4 billion in December. Many importers were racing to beat potential tariffs.

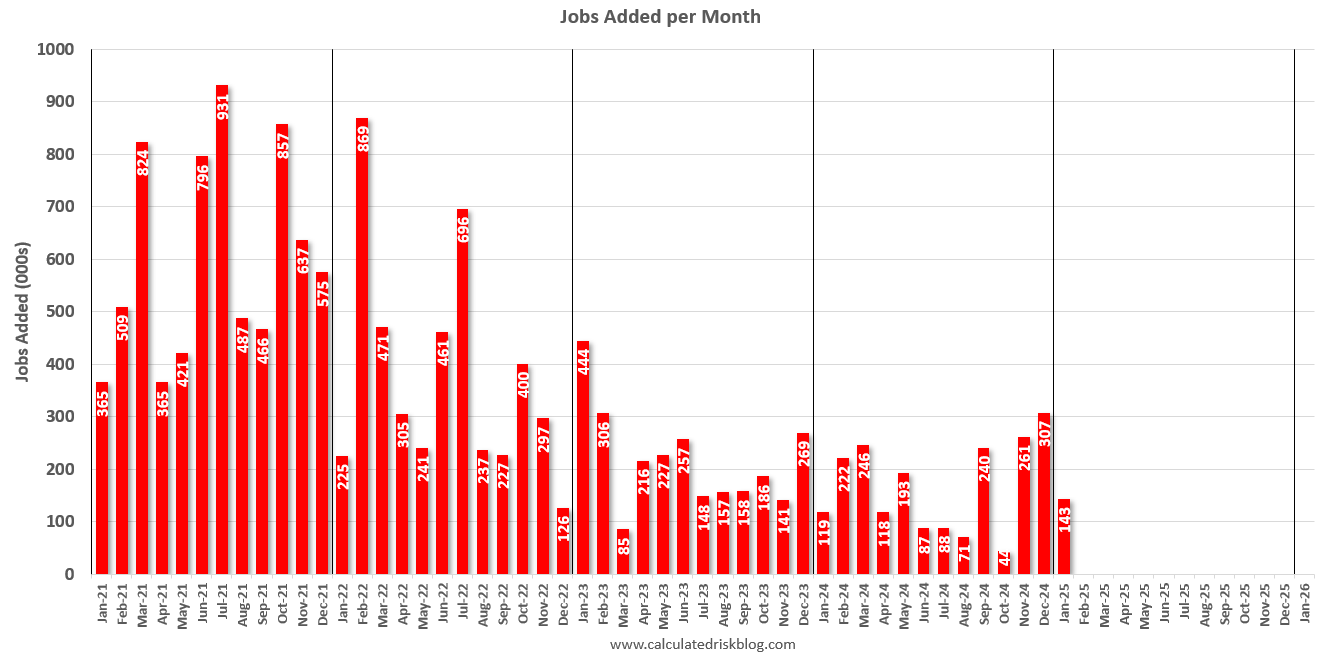

8:30 AM: Employment Report for February. The consensus is for 158,000 jobs added, and for the unemployment rate to be unchanged at 4.0%.

8:30 AM: Employment Report for February. The consensus is for 158,000 jobs added, and for the unemployment rate to be unchanged at 4.0%.There were 143,000 jobs added in January, and the unemployment rate was at 4.0%.

This graph shows the jobs added per month since January 2021.

12:30 PM: Speech, Fed Chair Jerome Powell, Economic Outlook, At The University of Chicago Booth School of Business 2025 U.S. Monetary Policy Forum, New York, N.Y.

Friday, February 28, 2025

February 28th COVID Update: COVID Deaths Declining

by Calculated Risk on 2/28/2025 07:03:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So I'm no longer tracking hospitalizations.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week | 850 | 893 | ≤3501 | |

| 1my goals to stop weekly posts. 🚩 Increasing number weekly for Deaths. ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported since Jan 2023.

Although weekly deaths met the original goal to stop posting in June 2023 (low of 314 deaths), I'm continuing to post now that deaths are above the goal again - and I'll continue to post until weekly deaths are once again below the goal.

Weekly deaths are now decreasing following the winter pickup.

This appears to be a leading indicator for COVID hospitalizations and deaths. This has moving down recently.

This appears to be a leading indicator for COVID hospitalizations and deaths. This has moving down recently.Nationally COVID in wastewater is "Moderate", down from "High" two weeks ago, according to the CDC.

Q1 GDP Tracking: Wide Range, GDPNow Goes Negative

by Calculated Risk on 2/28/2025 11:49:00 AM

From BofA:

The second print of 4Q GDP came in at 2.3% q/q saar, unchanged from the advance print and a tenth higher than our tracking estimate. Meanwhile, our 1Q GDP tracking is unchanged at 2.3% q/q saar since our last weekly publication. [Feb 28th]From Goldman:

emphasis added

We lowered our Q1 GDP tracking estimate by 0.4pp to +1.4% (quarter-over-quarter annualized). Our tracking estimate exaggerates the softness in Q1 to some extent because elevated gold imports ought to result in an offsetting increase in inventory accumulation, but the Q4 GDP data suggest this offset is unlikely to be captured in real time. [Feb 28th estimate]

And from the Atlanta Fed: GDPNow

And from the Atlanta Fed: GDPNowThe GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2025 is -1.5 percent on February 28, down from 2.3 percent on February 19. After recent releases from the US Bureau of Economic Analysis and the US Census Bureau, the nowcast of the contribution of net exports to first-quarter real GDP growth fell from -0.41 percentage points to -3.70 percentage points while the nowcast of first-quarter real personal consumption expenditures growth fell from 2.3 percent to 1.3 percent. [Feb 28th estimate]

Freddie Mac House Price Index Increased in January; Up 3.9% Year-over-year

by Calculated Risk on 2/28/2025 10:47:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Freddie Mac House Price Index Increased in January; Up 3.9% Year-over-year

A brief excerpt:

Freddie Mac reported that its “National” Home Price Index (FMHPI) increased 0.41% month-over-month on a seasonally adjusted (SA) basis in January. On a year-over-year basis, the National FMHPI was up 3.9% in January, down from up 4.1% YoY in December. The YoY increase peaked at 19.0% in July 2021, and for this cycle, bottomed at up 0.9% YoY in May 2023. ...There is much more in the article!

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted. Austin continues to be the worst performing city. However, 4 of the 6 cities with the largest price declines are in Florida (and Florida has 6 of the top 10 cities with the largest price declines).