RSS Feed

RSS Feed by Calculated Risk on 11/09/2020 04:00:00 PM

Monday, November 09, 2020

MBA Survey: "Share of Mortgage Loans in Forbearance Decreases to 5.67%"

Note: This is as of November 1st.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 5.67%

The Mortgage Bankers Association’s (MBA) latest Forbearance and Call Volume Survey revealed that the total number of loans now in forbearance decreased by 16 basis points from 5.83% of servicers’ portfolio volume in the prior week to 5.67% as of November 1, 2020. According to MBA’s estimate, 2.8 million homeowners are in forbearance plans.

...

“With declines in the share of loans in forbearance across the board, the data this week align well with the positive news from October’s jobs report, which showed a gain of more than 900,000 private sector jobs, and a 1 percentage point decrease in the unemployment rate,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “A recovering job market, coupled with a strong housing market, is providing the support needed for many homeowners to get back on their feet.”

Added Fratantoni, “However, the data continue to show that servicers are still having difficulties reaching borrowers who have reached the six-month point of their forbearance period. Servicers are required to get borrowers’ consent to extend forbearance beyond six months. Homeowners who continue to be impacted by hardships related to the pandemic should contact their servicer.”

...

By stage, 22.25% of total loans in forbearance are in the initial forbearance plan stage, while 75.99% are in a forbearance extension. The remaining 1.76% are forbearance re-entries.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time. Most of the increase was in late March and early April, and has been trending down for the last few months.

The MBA notes: "Total weekly forbearance requests as a percent of servicing portfolio volume (#) remainedunchanged relative to the prior week at 0.10%."

There hasn't been a pickup in forbearance activity related to the end of the extra unemployment benefits.

Leading Index for Commercial Real Estate Decreased in October

by Calculated Risk on 11/09/2020 02:14:00 PM

From Dodge Data Analytics: Dodge Momentum Index Loses Ground in June

The Dodge Momentum Index fell 1.8% in October to 127.5 (2000=100) from the revised September reading of 129.8. The Momentum Index, issued by Dodge Data & Analytics, is a monthly measure of the first (or initial) report for nonresidential building projects in planning, which have been shown to lead construction spending for nonresidential buildings by a full year. The commercial component of the Momentum Index lost 4.4% over the month, but the institutional component gained 3.3%.

The Momentum Index has struggled to make consistent gains since passing its post-pandemic low in June. Economic growth has slowed over the past few months, creating weaker demand for commercial projects. The fear about a new wave of COVID-19 infections may also be impeding planning activity in consumer-focused projects such as hotels and retail, although planning for warehouse projects continues to impress. Even with this month’s gain, the institutional component of the Momentum Index remains well below levels seen prior to the pandemic as state and local entities come to grips with the widening budget chasm.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Dodge Momentum Index since 2002. The index was at 127.5 in October, down from 129.8 in September.

According to Dodge, this index leads "construction spending for nonresidential buildings by a full year". This index suggests a decline in Commercial Real Estate construction through early 2021.

The Projected Improvement in Life Expectancy

by Calculated Risk on 11/09/2020 11:07:00 AM

As we celebrate the awesome vaccine news, Pfizer’s Early Data Shows Vaccine Is More Than 90% Effective, here is the most recent life expectancy data from the CDC. This is well prior to the pandemic, but it is still interesting and is important when looking at demographics ...

The following data is from the CDC United States Life Tables, 2017 by Elizabeth Arias, Ph.D., and Jiaquan Xu, M.D.

In 2017, the overall expectation of life at birth was 78.6 years, decreasing from 78.7 in 2016. Between 2016 and 2017, life expectancy at birth decreased by 0.1 year for males (76.2 to 76.1) and did not change for females (81.1). Life expectancy at birth decreased by 0.1 year for the white population (78.9 to 78.8) and the non-Hispanic white population (78.6 to 78.5) between 2016 and 2017. Life expectancy at birth did not change from 2016 for the black population (75.3), the non-Hispanic black population (74.9), and the Hispanic population (81.8).Instead of look at life expectancy, here is a graph of survivors out of 100,000 born alive, by age for three groups: those born in 1900-1902, born in 1949-1951 (baby boomers), and born in 2017.

...

[The following] summarizes the number of survivors by age, race, Hispanic origin, and sex. To illustrate, 57,839 persons out of the original 2017 hypothetical life table cohort of 100,000 (or 57.8%) were alive at exact age 80. In other words, the probability that a person will survive from birth to age 80, given 2017 age-specific mortality rates, is 57.8%. ... In 2017, 99.4% of all infants born in the United States survived the first year of life. In contrast, only 87.6% of infants born in 1900 survived the first year. Of the 2017 period life table cohort, 57.8% survived to age 80 and 1.9% survived to age 100. In 1900, 13.5% of the life table cohort survived to age 80 and only 0.03% survived to age 100

emphasis added

Click on graph for larger image.

Click on graph for larger image.There was a dramatic change between those born in 1900 (blue) and those born mid-century (orange). The risk of infant and early childhood deaths dropped sharply, and the risk of death in the prime working years also declined significantly.

The CDC is projecting further improvement for childhood and prime working age for those born in 2017, but they are also projecting that people will live longer.

The second graph uses the same data but looks at the number of people who die before a certain age, but after the previous age. As an example, for those born in 1900 (blue), 12,448 of the 100,000 born alive died before age 1, and another 5,748 died between age 1 and age 5.

The second graph uses the same data but looks at the number of people who die before a certain age, but after the previous age. As an example, for those born in 1900 (blue), 12,448 of the 100,000 born alive died before age 1, and another 5,748 died between age 1 and age 5.The peak age for deaths didn't change much for those born in 1900 and 1950 (between 76 and 80, but many more people born in 1950 will make it).

Now the CDC is projection the peak age for deaths - for those born in 2017 - will increase to 86 to 90! Using these stats - for those born this year (in 2020) - almost 60% will make it to the next century.

Also the number of deaths for those younger than 20 will be very small (down to mostly accidents, guns, and drugs). Self-driving cars might reduce the accident components of young deaths.

An amazing statistic: for those born in 1900, about 31 out of 100,000 made it to 100. For those born in 1950, 199 are projected to make to 100 - a significant increase. Now the CDC is projecting that 1,894 out of 100,000 born in 2017 will make it to 100. Stunning!

Some people look at this data and worry about supporting all these old people. To me, this is all great news - the vast majority of people can look forward to a long life - with fewer people dying in childhood or during their prime working years.

Seven High Frequency Indicators for the Economy

by Calculated Risk on 11/09/2020 08:13:00 AM

These indicators are mostly for travel and entertainment. It will interesting to watch these sectors recover as the vaccine is distributed.

IMPORTANT: Be safe now - if all goes well, we could all be vaccinated by Q2 2021.

----- Airlines: Transportation Security Administration -----

The TSA is providing daily travel numbers.

Click on graph for larger image.

Click on graph for larger image.

This data shows the seven day average of daily total traveler throughput from the TSA for 2019 (Blue) and 2020 (Red).

The dashed line is the percent of last year for the seven day average.

This data is as of Nov 8th.

The seven day average is down 65% from last year (35% of last year).

There has been a slow increase from the bottom, but has been weak lately.

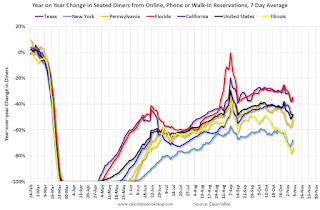

----- Restaurants: OpenTable -----

The second graph shows the 7 day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:

This data is updated through November 7, 2020.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Note that this data is for "only the restaurants that have chosen to reopen in a given market". Since some restaurants have not reopened, the actual year-over-year decline is worse than shown.

Note that dining is generally turning down more in the northern states - Illinois, Pennsylvania, and New York - but only turning down slightly in the southern states.

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week (red) and the maximum and minimum for the previous four years. Data is from BoxOfficeMojo through November 5th.

This data shows domestic box office for each week (red) and the maximum and minimum for the previous four years. Data is from BoxOfficeMojo through November 5th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales have picked up slightly over the last couple of months, and were at $12 million last week (compared to usually around $150 million per week in the early Fall).

Some movie theaters have reopened (probably with limited seating).

----- Hotel Occupancy: STR -----

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

The red line is for 2020, dash light blue is 2019, blue is the median, and black is for 2009 (the worst year since the Great Depression for hotels - prior to 2020).

This data is through October 31st. Hotel occupancy is currently down 29.0% year-over-year.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Since there is a seasonal pattern to the occupancy rate, we can track the year-over-year change in occupancy to look for any improvement. This table shows the year-over-year change since the week ending Sept 19, 2020:

This suggests little improvement over the last 7 weeks. Some of the recent decline in the occupancy rate is just seasonal.

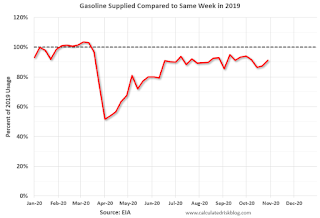

----- Gasoline Supplied: Energy Information Administration -----

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week last year of .

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week last year of .

At one point, gasoline supplied was off almost 50% YoY.

As of October 30th, gasoline supplied was off about 8.8% YoY (about 91.2% of last year).

Note: I know several people that have driven to vacation spots - or to visit family - and they usually would have flown. So this might have boosted gasoline consumption in the Summer and early Fall at the expense of air travel.

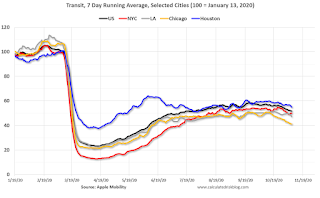

----- Transit: Apple Mobility -----

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

There is also some great data on mobility from the Dallas Fed Mobility and Engagement Index. However the index is set "relative to its weekday-specific average over January–February", and is not seasonally adjusted, so we can't tell if an increase in mobility is due to recovery or just the normal increase in the Spring and Summer.

This data is through November 7th for the United States and several selected cities.

This data is through November 7th for the United States and several selected cities.

The graph is the running 7 day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7 day average for the US is at 52% of the January level. It is at 41% in Chicago, and 55% in Houston - and declining recently.

----- New York City Subway Usage -----

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This is daily data for this year.

This graph is from Todd W Schneider. This is daily data for this year.

This data is through Friday, November 6th.

Schneider has graphs for each borough, and links to all the data sources.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

The TSA is providing daily travel numbers.

Click on graph for larger image.

Click on graph for larger image.This data shows the seven day average of daily total traveler throughput from the TSA for 2019 (Blue) and 2020 (Red).

The dashed line is the percent of last year for the seven day average.

This data is as of Nov 8th.

The seven day average is down 65% from last year (35% of last year).

There has been a slow increase from the bottom, but has been weak lately.

The second graph shows the 7 day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:This data is updated through November 7, 2020.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Note that this data is for "only the restaurants that have chosen to reopen in a given market". Since some restaurants have not reopened, the actual year-over-year decline is worse than shown.

Note that dining is generally turning down more in the northern states - Illinois, Pennsylvania, and New York - but only turning down slightly in the southern states.

This data shows domestic box office for each week (red) and the maximum and minimum for the previous four years. Data is from BoxOfficeMojo through November 5th.

This data shows domestic box office for each week (red) and the maximum and minimum for the previous four years. Data is from BoxOfficeMojo through November 5th.Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales have picked up slightly over the last couple of months, and were at $12 million last week (compared to usually around $150 million per week in the early Fall).

Some movie theaters have reopened (probably with limited seating).

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average. The red line is for 2020, dash light blue is 2019, blue is the median, and black is for 2009 (the worst year since the Great Depression for hotels - prior to 2020).

This data is through October 31st. Hotel occupancy is currently down 29.0% year-over-year.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Since there is a seasonal pattern to the occupancy rate, we can track the year-over-year change in occupancy to look for any improvement. This table shows the year-over-year change since the week ending Sept 19, 2020:

| Week Ending | YoY Change, Occupancy Rate |

|---|---|

| 9/19 | -31.9% |

| 9/26 | -31.5% |

| 10/3 | -29.6% |

| 10/10 | -29.2% |

| 10/17 | -30.7% |

| 10/24 | -31.7% |

| 10/31 | -29.0% |

This suggests little improvement over the last 7 weeks. Some of the recent decline in the occupancy rate is just seasonal.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week last year of .

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week last year of .At one point, gasoline supplied was off almost 50% YoY.

As of October 30th, gasoline supplied was off about 8.8% YoY (about 91.2% of last year).

Note: I know several people that have driven to vacation spots - or to visit family - and they usually would have flown. So this might have boosted gasoline consumption in the Summer and early Fall at the expense of air travel.

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

There is also some great data on mobility from the Dallas Fed Mobility and Engagement Index. However the index is set "relative to its weekday-specific average over January–February", and is not seasonally adjusted, so we can't tell if an increase in mobility is due to recovery or just the normal increase in the Spring and Summer.

This data is through November 7th for the United States and several selected cities.

This data is through November 7th for the United States and several selected cities.The graph is the running 7 day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7 day average for the US is at 52% of the January level. It is at 41% in Chicago, and 55% in Houston - and declining recently.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This is daily data for this year.

This graph is from Todd W Schneider. This is daily data for this year.This data is through Friday, November 6th.

Schneider has graphs for each borough, and links to all the data sources.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, November 08, 2020

November 8 COVID-19 Test Results; Hospitalizations almost 57,000

by Calculated Risk on 11/08/2020 08:23:00 PM

Note: I look forward to when I will not be posting this daily!

The US is now averaging close to 1 million tests per day. Based on the experience of other countries, for adequate test-and-trace (and isolation) to reduce infections, the percent positive needs to be well under 5% (probably close to 1%), so the US still needs to increase the number of tests per day significantly (or take actions to push down the number of new infections).

There were 881,251 test results reported over the last 24 hours.

There were 102,588 positive tests. This is a Sunday reporting record.

Almost 7,500 US deaths have been reported so far in November. See the graph on US Daily Deaths here.

Click on graph for larger image.

Click on graph for larger image.

This data is from the COVID Tracking Project.

The percent positive over the last 24 hours was 11.6% (red line is 7 day average).

For the status of contact tracing by state, check out testandtrace.com.

And check out COVID Exit Strategy to see how each state is doing.

The second graph shows the 7 day average of positive tests reported and daily hospitalizations.

The second graph shows the 7 day average of positive tests reported and daily hospitalizations.

The dashed line is the previous hospitalization maximum.

Note that there were very few tests available in March and April, and many cases were missed, so the hospitalizations was higher relative to the 7-day average of positive tests in July.

Now, there are many more tests, and many cases are being detected earlier - so hospitalizations have lagged. However, it is likely that hospitalizations will be at a new high in a few days.

This is a new record 7-day average cases for the USA.

This is a new record 7-day average cases for the USA.

Sunday Night Futures

by Calculated Risk on 11/08/2020 07:42:00 PM

Weekend:

• Schedule for Week of November 8, 2020

• GDP and Employment drag from State and Local Governments

Monday:

• At 2:00 PM ET, Senior Loan Officer Opinion Survey on Bank Lending Practices for October.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 34 and DOW futures are up 270 (fair value).

Oil prices were down over the last week with WTI futures at $37.83 per barrel and Brent at $40.11 barrel. A year ago, WTI was at $57, and Brent was at $62 - so WTI oil prices are down over 30% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.09 per gallon. A year ago prices were at $2.64 per gallon, so gasoline prices are down $0.55 per gallon year-over-year.

GDP and Employment drag from State and Local Governments

by Calculated Risk on 11/08/2020 11:24:00 AM

A key policy issue for 2021 will be how much disaster relief the Federal government will provide to state and local governments. If we look back at the Great Recession, most of the damage was done to the States after the recession. This is because state and local governments are required to run a balanced budget (or something close), and the state governments started cutting after the recession.

Here is a graph showing the contribution to percent change in GDP for state and local governments since 2005.

Click on graph for larger image.

Click on graph for larger image.

The red bars are the contribution to the percent change in real GDP from state and local governments.

Although state and local governments were a drag on GDP in Q2 and Q3 in 2020, the worst may happen in 2021 as state and local governments work to balance their budgets.

This next graph shows total state and government payroll employment since January 2005. Note that graph doesn't start at zero to better show the change in employment.

Following the Great Recession, most of the state and local government layoffs were after the recession. This was a drag on overall employment for a few years.

Following the Great Recession, most of the state and local government layoffs were after the recession. This was a drag on overall employment for a few years.

In 2020, there was a sharp decline in state and local government employment due to the pandemic (mostly in education employment).

Without Federal disaster relief, I expect state and local governments will have further layoffs in 2021.

Saturday, November 07, 2020

November 7 COVID-19 Test Results; Record Cases; Hospitalizations almost 56,000

by Calculated Risk on 11/07/2020 06:58:00 PM

Note: I look forward to when I will not be posting this daily!

The US is now averaging close to 1 million tests per day. Based on the experience of other countries, for adequate test-and-trace (and isolation) to reduce infections, the percent positive needs to be well under 5% (probably close to 1%), so the US still needs to increase the number of tests per day significantly (or take actions to push down the number of new infections).

There were 1,068,815 test results reported over the last 24 hours.

There were 128,396 positive tests. (New record)

Almost 7,000 US deaths have been reported so far in November. See the graph on US Daily Deaths here.

Click on graph for larger image.

Click on graph for larger image.

This data is from the COVID Tracking Project.

The percent positive over the last 24 hours was 12.0% (red line is 7 day average).

For the status of contact tracing by state, check out testandtrace.com.

And check out COVID Exit Strategy to see how each state is doing.

The second graph shows the 7 day average of positive tests reported.

The second graph shows the 7 day average of positive tests reported.

The dashed line is the July high.

Note that there were very few tests available in March and April, and many cases were missed (the percent positive was very high - see first graph). By June, the percent positive had dropped below 5%.

This is a new record 7-day average cases for the USA.

Hotels: Occupancy Rate Declined 29% Year-over-year

by Calculated Risk on 11/07/2020 10:43:00 AM

From HotelNewsNow.com: STR: US hotel results for week ending 31 October

U.S. weekly hotel occupancy was the lowest for any week since late June, according to the latest data from STR through 31 October.Since there is a seasonal pattern to the occupancy rate - see graph below - we can track the year-over-year change in occupancy to look for any improvement. This table shows the year-over-year change since the week ending Sept 19, 2020:

25-31 October 2020 (percentage change from comparable week in 2019):

• Occupancy: 44.4% (-29.0%)

• Average daily rate (ADR): US$91.56 (-27.4%)

• Revenue per available room (RevPAR): US$40.70 (-48.4%)

With rising COVID-19 case numbers and less leisure travel, the U.S. saw a second consecutive week with fewer hotel guests. During October 25-31, room demand fell 1.3 million from the prior week, leading to the country’s lowest occupancy level (44.4%) since the week of June 14-20.

emphasis added

| Week Ending | YoY Change, Occupancy Rate |

|---|---|

| 9/19 | -31.9% |

| 9/26 | -31.5% |

| 10/3 | -29.6% |

| 10/10 | -29.2% |

| 10/17 | -30.7% |

| 10/24 | -31.7% |

| 10/31 | -29.0% |

This suggests little improvement over the last 7 weeks, but not as bad as "lowest since June" would suggest. Some of the recent decline in the occupancy rate is just seasonal.

The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

Click on graph for larger image.The red line is for 2020, dash light blue is 2019, blue is the median, and black is for 2009 (the worst year since the Great Depression for hotels - before 2020).

Seasonally we'd expect the occupancy rate to decline into the new year. Note that there was little pickup in business travel that usually happens in the Fall.

Note: Y-axis doesn't start at zero to better show the seasonal change.

Schedule for Week of November 8, 2020

by Calculated Risk on 11/07/2020 08:11:00 AM

The key economic report this week is October CPI.

2:00 PM: Senior Loan Officer Opinion Survey on Bank Lending Practices for October.

6:00 AM: NFIB Small Business Optimism Index for October.

10:00 AM ET: Job Openings and Labor Turnover Survey for September from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for September from the BLS. This graph shows job openings (yellow line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings decreased in August to 6.493 million from 6.697 million in July.

Veterans Day Holiday: Most banks will be closed in observance of Veterans Day. The stock market will be open.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is initial claims decreased to 725 thousand from 751 thousand last week.

8:30 AM: The Consumer Price Index for October from the BLS. The consensus is for a 0.2% increase in CPI, and a 0.2% increase in core CPI.

8:30 AM: The Producer Price Index for October from the BLS. The consensus is for a 0.2% increase in PPI, and a 0.2% increase in core PPI.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for November).