RSS Feed

RSS Feed by Calculated Risk on 10/19/2015 02:34:00 PM

Monday, October 19, 2015

Lawler: Preliminary Table of Distressed Sales and Cash buyers for Selected Cities in September

Economist Tom Lawler sent me a preliminary table below of short sales, foreclosures and cash buyers for a few selected cities in September.

On distressed: Total "distressed" share is down in most of these markets. Distressed sales are up in the Baltimore due to an increase in foreclosures.

Short sales are down in all of these areas.

The All Cash Share (last two columns) is declining year-over-year. As investors pull back, the share of all cash buyers will probably continue to decline.

| Short Sales Share | Foreclosure Sales Share | Total "Distressed" Share | All Cash Share | |||||

|---|---|---|---|---|---|---|---|---|

| Sep- 2015 | Sep- 2014 | Sep- 2015 | Sep- 2014 | Sep- 2015 | Sep- 2014 | Sep- 2015 | Sep- 2014 | |

| Las Vegas | 6.8% | 10.4% | 7.1% | 8.8% | 13.9% | 19.2% | 26.8% | 34.3% |

| Reno** | 3.0% | 7.0% | 3.0% | 7.0% | 6.0% | 14.0% | ||

| Phoenix | 2.4% | 3.8% | 3.5% | 5.8% | 5.9% | 9.6% | 22.5% | 25.7% |

| Sacramento | 2.9% | 5.3% | 4.1% | 5.3% | 6.9% | 10.7% | 17.6% | 19.4% |

| Minneapolis | 1.8% | 3.4% | 6.5% | 9.6% | 8.3% | 13.0% | ||

| Mid-Atlantic | 3.9% | 5.5% | 11.1% | 9.7% | 14.9% | 15.2% | 17.5% | 19.1% |

| Baltimore MSA**** | 4.3% | 5.6% | 18.6% | 15.4% | 22.9% | 21.0% | ||

| Orlando | 3.5% | 7.1% | 20.1% | 24.8% | 23.6% | 31.8% | 35.6% | 41.7% |

| Chicago (city) | 17.5% | 18.8% | ||||||

| Hampton Roads | 15.6% | 19.6% | ||||||

| Spokane | 7.8% | 12.6% | ||||||

| Northeast Florida | 23.8% | 29.7% | ||||||

| Chicago (city) | 17.5% | 18.8% | ||||||

| Colorado***** | 1.8% | 3.7% | ||||||

| Toledo | 26.5% | 31.4% | ||||||

| Tucson | 25.9% | 26.7% | ||||||

| Georgia*** | 22.3% | 27.4% | ||||||

| Omaha | 18.1% | 19.9% | ||||||

| Pensacola | 31.4% | 29.2% | ||||||

| Tucson | 25.9% | 26.7% | ||||||

| Richmond MSA | 10.5% | 11.7% | 15.2% | 18.4% | ||||

| Memphis* | 13.1% | 13.2% | ||||||

| Springfield IL** | 10.1% | 9.5% | ||||||

| *share of existing home sales, based on property records **Single Family Only ***GAMLS ****Baltimore is included in the Mid-Atlantic region, but is shown separately here *****As tabulated by the Colorado Association of Realtors | ||||||||

Ornithology: What is a "deficit hawk"?

by Calculated Risk on 10/19/2015 01:27:00 PM

Nick Timiraos wrote yesterday in the WSJ: Debt, Growth Concerns Rain on Deficit Parade

The U.S. budget deficit is lower than before the 2008 financial crisis. But the good news is tempered by concerns on two fronts, one about the nation’s debt load and the other about the economy.I'd like to see the definition of a "deficit hawk"!

Deficit hawks are concerned that the improvement will lead both parties to overlook the red ink set to rise later this decade from a surge in spending on health care and retirement benefits for the baby-boom generation.

They worry that while the deficit is at the lowest level since 2007, the U.S. has added nearly $8 trillion in debt, an increase of 140%. That has nearly doubled the nation’s debt-to-GDP ratio, which stands near 73%—based on federal debt held by the public—and isn’t projected to fall in the coming years.

I'd think a true deficit hawk would be truly concerned about, uh, the deficit. So they'd support both tax increases1 and spending cuts to reduce the deficit. They'd oppose policies that increase the deficit (like the Bush tax cuts, and the war in Iraq). They'd also be concerned about policies that led to the financial crisis and a deep recession - since the deficit increases during a recession.

Maybe I'm talking my own position since I opposed the Bush tax cuts (that created a structural deficit). I opposed the Iraq war. I frequently talked to regulators about lax lending in real estate (and posted some of those discussion on this blog in 2005) that led directly to the financial crisis and large deficits. And I support both intelligent tax increases and spending cuts.

Unfortunately, my experience is that most people who claims to be "deficit hawks", are really pushing a different agenda. I wish Timiraos would provide a few examples of deficit hawks!

Also the "red ink set to rise later this decade" is expected in increase the deficit from 2.5% of GDP to about 3.1% in 2020.

1 Note: Some people like to focus on "growth" to reduce the deficit, and they tend to focus on tax cuts to boost growth. However, all data and research shows that at the current marginal rates, tax cuts do not pay for themselves and lead to much larger deficits.

NAHB: Builder Confidence at 64 in October, Highest in 10 Years

by Calculated Risk on 10/19/2015 10:06:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 64 in October, up from 61 in September. Any number above 50 indicates that more builders view sales conditions as good than poor.

From the NAHB: Builder Confidence Rises Three Points in October

Builder confidence in the market for newly constructed single-family homes rose three points in October to a level of 64 on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI). This month’s reading is a return to HMI levels seen at the end of the housing boom in late 2005.

...

“With October’s three-point uptick, builder confidence has been holding steady or increasing for five straight months. This upward momentum shows that our industry is strengthening at a gradual but consistent pace,” said NAHB Chief Economist David Crowe. “With firm job creation, economic growth and the release of pent-up demand, we expect housing to keep moving forward as we start to close out 2015.”

...

Two of the three HMI components posted gains in October. The index measuring sales expectations in the next six months rose seven points to 75, and the component gauging current sales conditions increased three points to 70. Meanwhile, the index charting buyer traffic held steady at 47.

Looking at the three-month moving averages for regional HMI scores, all four regions posted gains. The West registered a five-point uptick to 69 while the Northeast, Midwest and South each rose one point to 47, 60 and 65, respectively.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph show the NAHB index since Jan 1985.

This was above the consensus forecast of 62.

Sunday, October 18, 2015

Sunday Night Futures

by Calculated Risk on 10/18/2015 09:17:00 PM

Weekend:

• Schedule for Week of October 18, 2015

Monday:

• At 10:00 AM, the October NAHB homebuilder survey. The consensus is for a reading of 62, unchanged from September. Any number above 50 indicates that more builders view sales conditions as good than poor.

From CNBC: Pre-Market Data and Bloomberg futures: currently S&P futures and DOW futures are mostly unchanged (fair value).

Oil prices were down over the last week with WTI futures at $47.31 per barrel and Brent at $50.50 per barrel. A year ago, WTI was at $82, and Brent was at $85 - so prices are down about 40% year-over-year (It was a year ago that prices were falling sharply).

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.26 per gallon (down about $0.75 per gallon from a year ago).

Goldman Sachs Expects "Fed Liftoff" in December

by Calculated Risk on 10/18/2015 09:46:00 AM

A few excerpts from a research piece by Goldman Sachs chief economist Jan Hatzius: Q&A on Fed Liftoff

We still expect a rate hike at the December FOMC meeting. The leadership has signaled that such a move is likely if the economy and markets evolve broadly as expected, and our forecast is similar to theirs. However, we are only about 60% confident. Most of the uncertainty relates to the possibility that the economic and market environment—or in a broad sense, “the data”—will be worse than the FOMC’s (and our) expectations.

...

The low market-implied probability of a December hike of only 30%-40% probably reflects a mixture of concerns about the data (which we find reasonable) and a belief among some market participants that the FOMC will find an “excuse” to stay on hold even if the economy does fine (which we find unreasonable). ...

Our own view is that it might make sense to start normalizing in December if we were perfectly confident in our baseline forecast for the economy. But uncertainty around that forecast still argues for waiting longer. The main reason is risk management.

Saturday, October 17, 2015

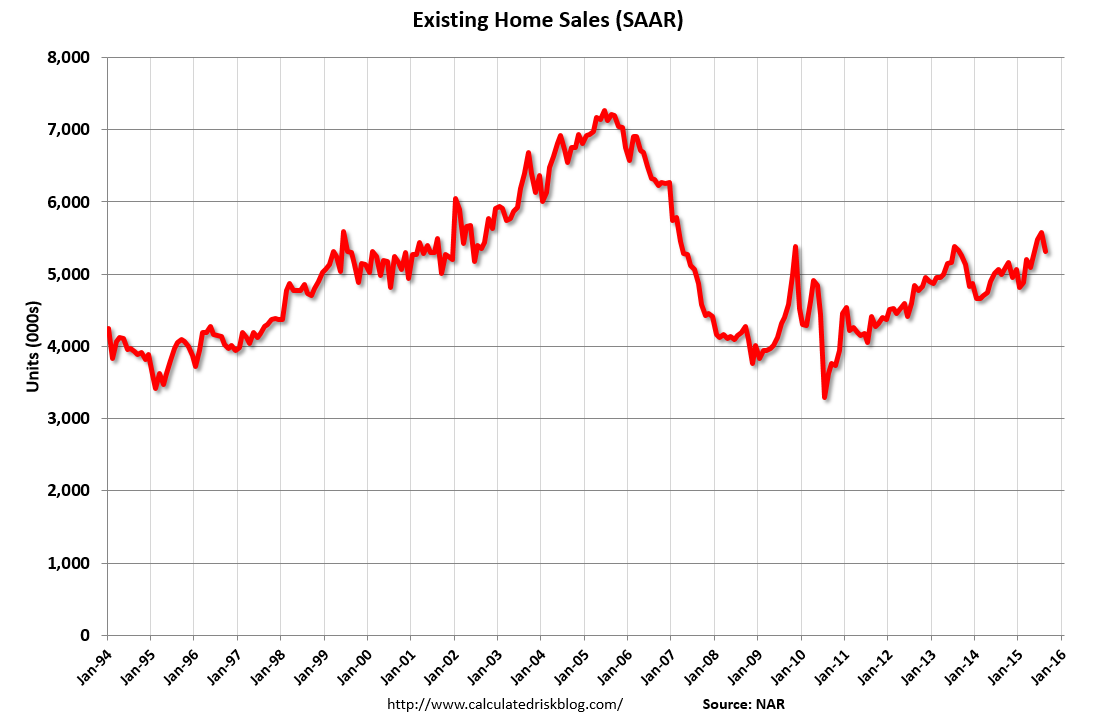

Existing Home Sales: Lawler vs. the Consensus

by Calculated Risk on 10/17/2015 04:01:00 PM

The NAR will report September Existing Home Sales on Thursday, October 22nd at 10:00 AM.

The consensus, according to Bloomberg, is that the NAR will report sales of 5.35 million. Housing economist Tom Lawler estimates the NAR will report sales of 5.56 million on a seasonally adjusted annual rate (SAAR) basis, up from 5.31 million SAAR in August.

Housing economist Tom Lawler has been sending me his predictions of what the NAR will report for over 5 years. The table below shows the consensus for each month, Lawler's predictions, and the NAR's initial reported level of sales.

Lawler hasn't always been closer than the consensus, but usually when there has been a fairly large spread between Lawler's estimate and the "consensus", Lawler has been closer.

NOTE: There have been times when Lawler "missed", but then he pointed out an apparent error in the NAR data - and the subsequent revision corrected that error. As an example, see: The “Curious Case” of Existing Home Sales in the South in April

Over the last five years, the consensus average miss was 146 thousand with a standard deviation of 150 thousand. Lawler's average miss was 69 thousand with a standard deviation of 50 thousand.

NOTE: Last month was Lawler's largest miss by 0.23 million SAAR (read his explanation here). For comparison, the consensus' largest miss was 0.83 million. Ouch.

Many analysts now change their "forecast" after Lawler's estimate is posted, so the consensus has improved a little recently!

| Existing Home Sales, Forecasts and NAR Report millions, seasonally adjusted annual rate basis (SAAR) | |||

|---|---|---|---|

| Month | Consensus | Lawler | NAR reported1 |

| May-10 | 6.20 | 5.83 | 5.66 |

| Jun-10 | 5.30 | 5.30 | 5.37 |

| Jul-10 | 4.66 | 3.95 | 3.83 |

| Aug-10 | 4.10 | 4.10 | 4.13 |

| Sep-10 | 4.30 | 4.50 | 4.53 |

| Oct-10 | 4.50 | 4.46 | 4.43 |

| Nov-10 | 4.85 | 4.61 | 4.68 |

| Dec-10 | 4.90 | 5.13 | 5.28 |

| Jan-11 | 5.20 | 5.17 | 5.36 |

| Feb-11 | 5.15 | 5.00 | 4.88 |

| Mar-11 | 5.00 | 5.08 | 5.10 |

| Apr-11 | 5.20 | 5.15 | 5.05 |

| May-11 | 4.75 | 4.80 | 4.81 |

| Jun-11 | 4.90 | 4.71 | 4.77 |

| Jul-11 | 4.92 | 4.69 | 4.67 |

| Aug-11 | 4.75 | 4.92 | 5.03 |

| Sep-11 | 4.93 | 4.83 | 4.91 |

| Oct-11 | 4.80 | 4.86 | 4.97 |

| Nov-11 | 5.08 | 4.40 | 4.42 |

| Dec-11 | 4.60 | 4.64 | 4.61 |

| Jan-12 | 4.69 | 4.66 | 4.57 |

| Feb-12 | 4.61 | 4.63 | 4.59 |

| Mar-12 | 4.62 | 4.59 | 4.48 |

| Apr-12 | 4.66 | 4.53 | 4.62 |

| May-12 | 4.57 | 4.66 | 4.55 |

| Jun-12 | 4.65 | 4.56 | 4.37 |

| Jul-12 | 4.50 | 4.47 | 4.47 |

| Aug-12 | 4.55 | 4.87 | 4.82 |

| Sep-12 | 4.75 | 4.70 | 4.75 |

| Oct-12 | 4.74 | 4.84 | 4.79 |

| Nov-12 | 4.90 | 5.10 | 5.04 |

| Dec-12 | 5.10 | 4.97 | 4.94 |

| Jan-13 | 4.90 | 4.94 | 4.92 |

| Feb-13 | 5.01 | 4.87 | 4.98 |

| Mar-13 | 5.03 | 4.89 | 4.92 |

| Apr-13 | 4.92 | 5.03 | 4.97 |

| May-13 | 5.00 | 5.20 | 5.18 |

| Jun-13 | 5.27 | 4.99 | 5.08 |

| Jul-13 | 5.13 | 5.33 | 5.39 |

| Aug-13 | 5.25 | 5.35 | 5.48 |

| Sep-13 | 5.30 | 5.26 | 5.29 |

| Oct-13 | 5.13 | 5.08 | 5.12 |

| Nov-13 | 5.02 | 4.98 | 4.90 |

| Dec-13 | 4.90 | 4.96 | 4.87 |

| Jan-14 | 4.70 | 4.67 | 4.62 |

| Feb-14 | 4.64 | 4.60 | 4.60 |

| Mar-14 | 4.56 | 4.64 | 4.59 |

| Apr-14 | 4.67 | 4.70 | 4.65 |

| May-14 | 4.75 | 4.81 | 4.89 |

| Jun-14 | 4.99 | 4.96 | 5.04 |

| Jul-14 | 5.00 | 5.09 | 5.15 |

| Aug-14 | 5.18 | 5.12 | 5.05 |

| Sep-14 | 5.09 | 5.14 | 5.17 |

| Oct-14 | 5.15 | 5.28 | 5.26 |

| Nov-14 | 5.20 | 4.90 | 4.93 |

| Dec-14 | 5.05 | 5.15 | 5.04 |

| Jan-15 | 5.00 | 4.90 | 4.82 |

| Feb-15 | 4.94 | 4.87 | 4.88 |

| Mar-15 | 5.04 | 5.18 | 5.19 |

| Apr-15 | 5.22 | 5.20 | 5.04 |

| May-15 | 5.25 | 5.29 | 5.35 |

| Jun-15 | 5.40 | 5.45 | 5.49 |

| Jul-15 | 5.41 | 5.64 | 5.59 |

| Aug-15 | 5.50 | 5.54 | 5.31 |

| Sep-15 | 5.35 | 5.56 | --- |

| 1NAR initially reported before revisions. | |||

Schedule for Week of October 18th

by Calculated Risk on 10/17/2015 08:11:00 AM

The key economic reports this week are September housing starts on Tuesday, and September Existing Home Sales on Thursday.

10:00 AM: The October NAHB homebuilder survey. The consensus is for a reading of 62, unchanged from September. Any number above 50 indicates that more builders view sales conditions as good than poor.

8:30 AM: Housing Starts for September.

8:30 AM: Housing Starts for September. Total housing starts decreased to 1.126 million (SAAR) in August. Single family starts decreased to 739 thousand SAAR in August.

The consensus for 1.147 million, up from August.

10:00 AM ET: Regional and State Employment and Unemployment for September.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

During the day: The AIA's Architecture Billings Index for September (a leading indicator for commercial real estate).

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 265 thousand initial claims, up from 255 thousand the previous week.

8:30 AM ET: Chicago Fed National Activity Index for September. This is a composite index of other data.

9:00 AM: FHFA House Price Index for August 2015. This was originally a GSE only repeat sales, however there is also an expanded index. The consensus is for a 0.5% month-to-month increase for this index.

10:00 AM: Existing Home Sales for September from the National Association of Realtors (NAR). The consensus is for 5.35 million SAAR, up from 5.31 million in August.

10:00 AM: Existing Home Sales for September from the National Association of Realtors (NAR). The consensus is for 5.35 million SAAR, up from 5.31 million in August. Economist Tom Lawler estimates the NAR will report sales of 5.56 million SAAR.

A key will be the reported year-over-year change in inventory of homes for sale.

11:00 AM: the Kansas City Fed manufacturing survey for September.

During the day: Q3 NMHC Apartment Tightness Index.

No economic released scheduled.

Friday, October 16, 2015

Lawler: Early Read on Existing Home Sales in September

by Calculated Risk on 10/16/2015 04:42:00 PM

From housing economist Tom Lawler:

Based on publicly-released realtor/MLS reports from across the country released through today, I project that US existing home sales as estimated by the National Association of Realtors ran at a seasonally adjusted annual rate of about 5.56 million in September, up about 4.7% from August’s preliminary pace and up 9.0% from last September’s seasonally-adjusted pace. I expect the NAR’s estimate of the inventory of existing homes for sale at the end of September to be down about 1.7% from August’s preliminary estimate, and down about 1.3% from last September. Finally, I expect the NAR’s median existing home sales price estimate for September to be up about 5.5% from last September.

Post-Mortem on August’s Existing Home Sales Report: NAR’s Estimate of the YOY % Change in Unadjusted Sales Seems Reasonable

On September 21st the NAR estimated that US existing home sales ran at a seasonally adjusted annual rate of 5.31 million in August – far below both the “consensus” forecast and my projection based on realtor/MLS reports available as of September 15th. As I acknowledged following the NAR EHS report for August, part of my “miss” reflected a “misread” of the likely seasonal factor used to adjust the “raw” sales data. However, my projection was also off because the “sample” of local realtor/MLS reports I had available as of September 15th proved to be a poor representation of the larger sample of local realtor/MLS reports for August that include reports subsequently released. Based on this larger sample, the NAR’s estimate of the YOY % change in existing home sales in August seems broadly consistent with local realtor/MLS reports.

If, in fact, my September projection for existing home sales is correct, then one might ask: why have there been such large month swings in seasonally-adjusted home sales over the past several months? My gut is that some of these swings have been less related to volatile markets, and more related to difficulties in accurately estimating the true “seasonal” component of existing home sales. Statistical estimates of this seasonal pattern of home sales have changed considerably over the past 10-15 years, and it is quite possible that some of the observed change in the “seasonal” pattern may actually be related to other forces (witness, e.g., the huge increase in the amplitude of “seasonal” swings in home prices since the housing collapse, which most analyst attribute to the combination of the surge in distressed sales and the seasonal pattern of the distressed-sales share of total home sales).

CR Note: The NAR is scheduled to release September Existing Home Sales on Thursday, Oct 22nd. The consensus forecast is for 5.36 million (this will move up after this is posted). Take the over!

Treasury: "There is Only One Solution to the Debt Limit"

by Calculated Risk on 10/16/2015 03:30:00 PM

From the U.S. Treasury: There is Only One Solution to the Debt Limit

Some commentators have suggested that the President could invoke the Fourteenth Amendment of the Constitution as a justification for issuing debt in excess of the debt limit. Others have suggested that Treasury could mint and issue a large-denomination platinum coin to obtain cash without exceeding the debt limit. But as we’ve said before, the Fourteenth Amendment does not give the President the power to ignore the debt ceiling. And neither the Treasury nor the Federal Reserve believes that the law can or should be used to produce platinum coins for the purpose of avoiding an increase in the debt limit.It is the responsibility of Congress - and Congress alone - to pay the bills. Default is not an option. They have less than 3 weeks to act ...

As the Chair of the Council of the Inspectors General on Financial Oversight (CIGFO) explained in 2012, Treasury found no option that could reasonably protect the full faith and credit of the United States and the American people from very serious harm. Additionally, CIGFO noted that Treasury viewed the option of delaying payments as the least harmful among these options. But this option would still be default. Fortunately, because Congress ultimately took action, no final decision was needed.

With some in Congress again suggesting that we prioritize principal and interest while missing payments on other obligations, it’s worth considering again why this is such an unacceptable outcome. It is simply default by another name.

...

Principal and interest on the debt are only part of our obligations. Prioritizing principal and interest would mean paying some of our creditors – many of whom are foreign institutions – while defaulting on across-the-board payments everywhere else. That would include payments to members of the military, veterans, and senior citizens. It would include payments on infrastructure projects. In this scenario that America defaults on its obligations, there would be no way to prevent significant disruptions and hardship for millions of Americans. Default would undermine confidence in the creditworthiness of the United States.

...

For 226 years, we have been a country that pays all our bills. We can’t break that trust with our creditors and investors and put the full faith and credit of the United States in question. And we can’t break that trust with our citizens.

emphasis added

Earlier: Preliminary October Consumer Sentiment increases to 92.1

by Calculated Risk on 10/16/2015 12:09:00 PM

The preliminary University of Michigan consumer sentiment index for October was at 92.1, up from 87.2 in September.

"The rebound in confidence signifies that consumers have concluded that the fears expressed on Wall Street did not extend to Main Street. Importantly, the renewed confidence did not simply represent a relief rally, but instead reflected renewed optimism. Personal financial expectations rose to their highest level since 2007, as did consumers' views toward purchases of durable goods. While consumers anticipate a continued economic expansion, many expected strong headwinds from falling commodity prices, weakened economies in China and elsewhere as well as continued stresses on European countries. Perhaps the most important finding is that low inflation and continued job growth have enabled consumers to adapt to a slower and more variable rate of economic growth by varying the pace of their spending without losing confidence that the expansion will continue. Overall, the data still indicate that consumption will expand at 2.9% during 2016."This was above the consensus forecast of 89.5.

Click on graph for larger image.