RSS Feed

RSS Feed by Calculated Risk on 11/15/2011 04:04:00 PM

Tuesday, November 15, 2011

Lawler on FHA MMIF Actuarial Review for FY 2011

From economist Tom Lawler: HUD released the annual Actuarial Review of the FHA’s Mutual Mortgage Insurance Fund for FY 2011, which is required by law and which is performed by an independent entity (lately IFE Group) to assess the “economic net worth” and “financial soundness” of the fund. According to the latest review, the estimated “economic net worth” of the MMIF (ex HECMs) at the end of FY 2011 (9/30/11) – defined as the sum of existing capital resources plus the net present value of the current books of business (using “base-case” economic scenarios) – was just $1.19 billion, down from $5.16 billion at the end of FY 2010. The “base case” scenario for home prices is based on Moody’s July 2011 forecast for the FHFA home price index, which I guess IFE Group uses because the FHFA HPIs cover a large number of MSAs, even though these HPIs are widely viewed as not being the “best” measures of home price trends. This forecast shows home price declining modestly next year.

Last year, the actuarial review estimated that by the end of FY 2011 the MMIF’s “economic value” would rise to $10.969 billion, as opposed to the latest report’s decline to $1.1193 billion. The FHFA “national” HPI fell in 2010 and early 2011 by more than was projected in the “base-case” used for the FY2010 actuarial review. However, Moody’s forecast for home price appreciation is a bit above last July’s, and as a result the “base-case” economic assumptions actually were a PLUS to IFE’s estimate of the FY 2011 “economic value.”

The major “negative hit” to the MMIF EV was related to “updated econometric model and portfolio status” factors, especially (1) much slower prepayment forecasts, and (2) the elimination of last year’s questionable “policy year dummy variables.” In addition, there was a negative “adjustment for foreclosure loans,” reflecting the unusually large number of loans in the foreclosure process at the time of the review, including a larger-than-normal number of properties where foreclosures had apparently been completed but servicers had not yet filed claims.

Click on graph for larger image.

Click on graph for larger image.

CR Note: here are the house price scenarios used in the analysis.

As with last year, this year’s review included some “sensitivity analysis,” which suggested that the MMIF’s exposure to “bad” scenarios had worsened from last year. [Below] are tables showing the estimated “economic value” of the MMIF under alternative scenarios from the FY 2010 Actuarial Review, and from the FY 2011 Actuarial Review.

CR Note: This table is from the FY 2010 Actuarial Review.

CR Note: This table is from the FY 2010 Actuarial Review.

And the second table is from the 2011 review. As Tom Lawler notes, the FHA has performed worse than the base case for 2010 - and there are much bigger expected losses under the “Worse-than-Base-Case” scenarios.

Note that (1) the “economic value” of the 2011 book in a “near-term” rebound scenario in the FY 2011 AR is substantially lower that the projected economic value of the 2011 book in the “base-case” scenarios; and (2) the economic values of the FY 2011 under the “worse-than-base-case” scenarios are massively worse than was the case last year.

Note that (1) the “economic value” of the 2011 book in a “near-term” rebound scenario in the FY 2011 AR is substantially lower that the projected economic value of the 2011 book in the “base-case” scenarios; and (2) the economic values of the FY 2011 under the “worse-than-base-case” scenarios are massively worse than was the case last year.

Folks who want to read the whole thing can find it here.

Misc: Empire Manufacturing survey improves, Farmland Prices "surge"

by Calculated Risk on 11/15/2011 01:15:00 PM

From the NY Fed earlier today: Conditions for New York manufacturers held steady in November

The Empire State Manufacturing Survey indicates that conditions for New York manufacturers held steady in November. After a string of five consecutive months of negative readings, the general business conditions index rose nine points, to 0.6. While the new orders index edged down to -2.1, indicating that orders were a little lower, the shipments index rose to 9.4, indicating an increase in shipments. The inventories index fell to -12.2 — a sign that inventory levels dropped.This was slightly above the consensus forecast. The futures indexes really "surged" indicating

...

Employment indexes were mixed: employment levels were slightly lower and the average workweek slightly longer.

"a widespread expectation that conditions would improve in the months ahead".

And from the Chicago Fed: Third Quarter Midwest Farmland Values Surge

At 25 percent, the year-over-year gain in agricultural land values in the third quarter of 2011 for the Seventh Federal Reserve District was the largest in just over three decades. Moreover, at 7 percent, the quarterly increase in the value of “good” farmland matched the highest since the late 1970s.I just hope farmers and farm land lenders remember the lessons of the '80s - and that farmers don't borrow too much, and lenders think about tighter lending standards.

European Bond Yields Rising as Euro zone economy slows

by Calculated Risk on 11/15/2011 11:34:00 AM

From the WSJ: Recession Fears Haunt Euro Zone

The euro-zone economy barely grew in the third quarter despite a temporary bounce in Germany and France, raising fears that the euro bloc may already be sliding into recession ... Gross domestic product in the 17-nation euro zone grew 0.6% at an annualized rate during the third quarter ... Germany's economy recovered to post a 2% annualized growth rate ... France grew 1.6% after stagnating in the second quarter.Below is a table for several European bond yields (links to Bloomberg).

Those two countries comprise half of euro-zone GDP, indicating that the rest of the euro bloc contracted as a whole ...

The Italian 10 year bond yield is up to 7.07%. The Italian 2 year yield is up to 6.54%.

The Spanish 10 year bond yield has increased to 6.34%. The Spanish 2 year yield is up to 5.3%.

The French 10 year bond yield is at 3.67%. The Belgium 10 year yield is up to 4.9%.

| Greece | 2 Year | 5 Year | 10 Year |

| Portugal | 2 Year | 5 Year | 10 Year |

| Ireland | 2 Year | 5 Year | 10 Year |

| Spain | 2 Year | 5 Year | 10 Year |

| Italy | 2 Year | 5 Year | 10 Year |

| Belgium | 2 Year | 5 Year | 10 Year |

| France | 2 Year | 5 Year | 10 Year |

| Germany | 2 Year | 5 Year | 10 Year |

HUD report on FHA Financial Status

by Calculated Risk on 11/15/2011 10:04:00 AM

This report shows some improvement from the report last year, but the house price assumptions seem optimistic.

From HUD: FHA Issues Annual Financial Status Report to Congress

In reporting on findings of the annual independent actuarial study, HUD indicates that, in the midst of continued weakness in housing markets across the county, the MMI Fund capital ratio remains positive this year at 0.24 percent. With new risk controls and premiums put in place by the Obama Administration, the independent actuaries predict the Fund will return to the Congressionally-mandated threshold of two percent capital more quickly than was projected by last year’s review.Long term readers will remember the many posts by Tanta and myself warning about the negative impact of "DAPs" (the seller-funded downpayment assistance programs that allowed buyers to put no money down). The DAPs were finally banned, but they caused significant losses for the FHA.

...

As was the case last year, the new actuarial study shows that FHA is expected to sustain significant losses from loans insured prior to 2009, and thus its capital reserve remains below the congressionally mandated threshold of two percent of total insurance-in-force. However, the actuaries’ report concludes that, barring a further significant downturn in home prices, the MMI Fund will start to rebuild capital in 2012, and return to a level of two percent by 2014 – outpacing last year’s prediction.

...

Losses on loans insured through the first quarter of fiscal year 2009 continue to place a significant strain on the Fund and are expected to reach $26 billion within a few more years. Though they were prohibited in 2009, the ongoing effect of so-called “seller-funded downpayment assistance loans” is still significant. The net expected cost of those loans, as projected by the independent actuaries, grew by $1.8 billion over the past year to $14.1 billion. Conversely, the actuaries found that the FY2010 and FY2011 books are expected to be very profitable, providing significant net revenues to offset losses on earlier books.

This assumes prices increase slightly next year: "The base-case scenario provided by Moody’s Analytics indicates price declines in 2011 of 5.6% and predicts a small amount of growth in prices in 2012 (1.3%), followed by ore steady growth starting in 2013."

Here is the HUD report - and the graph below shows the house price scenarios included in the report.

Click on graph for larger image.NOTE: Prices are for the FHFA index (GSE loans only), and the FHFA index didn't increase as rapidly as Case-Shiller, and didn't decline as fast either (the GSE loans have performed significantly better than the Wall Street originate-to-distribute loans).

The “Mild Second Recession” utilized by the actuaries poses an additional 9 percent decline in home prices beyond the 5.6 percent base-case decline, for a total two-year decline of 14.6 percent.I don't think we will see another sharp decline in house prices - although I think prices will fall to new post-bubble lows this winter. I also don't think we will see the steady increase in prices as shown by all of these forecasts. Usually prices move sideways for a few years at the end of a housing bust (especially in real terms).

FHA estimates that the fund could withstand an additional decline in house prices of 4% beyond the base-case decline without experiencing a negative capital situation.

Special note: Tanta's birthday was November 15th. Tanta vive!

Retail Sales increased 0.5% in October

by Calculated Risk on 11/15/2011 08:30:00 AM

On a monthly basis, retail sales were up 0.5% from September to October (seasonally adjusted, after revisions), and sales were up 7.9% from October 2010. From the Census Bureau report:

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for October, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $397.7 billion, an increase of 0.5 percent (±0.5%) from the previous month and 7.2 percent (±0.7%) above October 2010. Total sales for the August through October 2011 period were up 7.6 percent (±0.5%) from the same period a year ago. The August to September 2011 percent change was unrevised from +1.1 percent (±0.3%).Retail sales excluding autos increased 0.6% in October. Sales for September were unrevised with a 1.1% increase.

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales are up 19.5% from the bottom, and now 5.1% above the pre-recession peak (not inflation adjusted)

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail sales ex-gasoline increased by 6.0% on a YoY basis (7.2% for all retail sales).

Retail sales ex-gasoline increased by 6.0% on a YoY basis (7.2% for all retail sales). This was well above the consensus forecast for retail sales of a 0.2% increase in October, and no change ex-auto.

This was a solid report, especially following the very strong September report.

Monday, November 14, 2011

State by state exports to Europe

by Calculated Risk on 11/14/2011 09:16:00 PM

From the Miami Herald: Florida’s economy faces ‘moderate’ risk from European recession

Florida would fare better than many states should Europe slip into recession, a new study [by Wells Fargo] found. ... The report makes no mention of another key concern for Florida: European tourism. The United Kingdom is Florida’s second largest source of international travelers behind Canada, with Germany holding the fifth slot behind Brazil and Mexico.Here is a map from the referenced report by economist Mark Vitner and Michael Brown at Wells Fargo. The map shows European exports as a percent of state GDP.

Click on graph for larger image.

Click on graph for larger image.Utah has a very high percentage of exports to Europe - mostly silver and gold to the United Kingdom. West Virginia exports coal.

As the Miami Herald article notes, Florida will probably also be impacted by less tourism too.

However the largest potential impact is probably from financial contagion as opposed to trade and tourism. Catherine Rampell has a summary of the various channels of contagion: The Euro Zone Crisis and the U.S.: A Primer

Schedule Update: MBA's 3rd Quarter 2011 National Delinquency Survey will be released Thursday

by Calculated Risk on 11/14/2011 06:31:00 PM

An update to the weekly schedule ...

10:00 AM: Mortgage Bankers Association (MBA) 3rd Quarter 2011 National Delinquency Survey (NDS)

The following graph shows the percent of loans delinquent by days past due for Q2.

The MBA reported 8.44% of mortgage loans were delinquent at the end of Q2, seasonally adjusted, and another 4.43% were in the foreclosure process (total of 12.87%, essentially unchanged from Q1).

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of loans delinquent by days past due in Q2. Based on other data, the delinquency rate probably decreased slightly in Q3.

However the key problem is the large number of seriously delinquent loans (90+ days and in the foreclosure process). And there probably was little change in those percentages in Q3.

SF Fed: Recession odds in 2012 are greater than 50% due to European Crisis

by Calculated Risk on 11/14/2011 03:37:00 PM

An economic letter from the SF Fed: Future Recession Risks: An Update(ht Rickkk)

Gathering storms across the Atlantic threaten a U.S. economy not yet recovered from the last recession. ... In the next few months, the odds of recession due to domestic factors appear reasonably contained. ... However, the curve reflecting the international odds suggests more imminent danger to the economy, although this threat is harder to calibrate using historical data and only indirectly reflects the health of the European financial system. Recession odds based on international factors peak at about 45% toward the end of 2011 ... The combination of these two recession coins, shown in the combined risks line of Figure 2, is quite disconcerting. It indicates that the odds are greater than 50% that we will experience a recession sometime early in 2012. Because the international odds of recession are more imprecisely estimated, one must be careful with a strict interpretation of this result. But the message is clear. Prudence suggests that the fragile state of the U.S. economy would not easily withstand turbulence coming across the Atlantic.Based on domestic data, I think a recession is unlikely. However the European crisis is definitely a significant downside risk to U.S. economic growth. The spillover from Europe depends on how the crisis unfolds ...

Europe: Italian and Spanish bond yields rising

by Calculated Risk on 11/14/2011 01:24:00 PM

The Italian 10 year bond yield is up to 6.7%.

And keep an eye on Spain ... The Spanish 10 year bond yield has increased to 6.1%. The Spanish 2 year yield is up to 5.0%

From Bloomberg: Merkel’s CDU Delegates at Party Gathering Support Allowing Exits From Euro

“We’re not throwing anybody out,” Finance Minister Wolfgang Schaeuble said in an interview from Leipzig with broadcaster Phoenix. “We want Greece to stay in, that everybody stays in,” he said. “But if a country can’t carry the burden or doesn’t want to carry the burden, and the Greek people have to carry a heavy load, then we have to respect the country’s decision.”Earlier today, the Greek New Democracy opposition leader Antonis Samaras was quoted as saying his party would not vote for any austerity measures, and he would not sign any letter pledging a commitment to austerity measures. If so, Greece will probably be leaving the euro sooner rather than later.

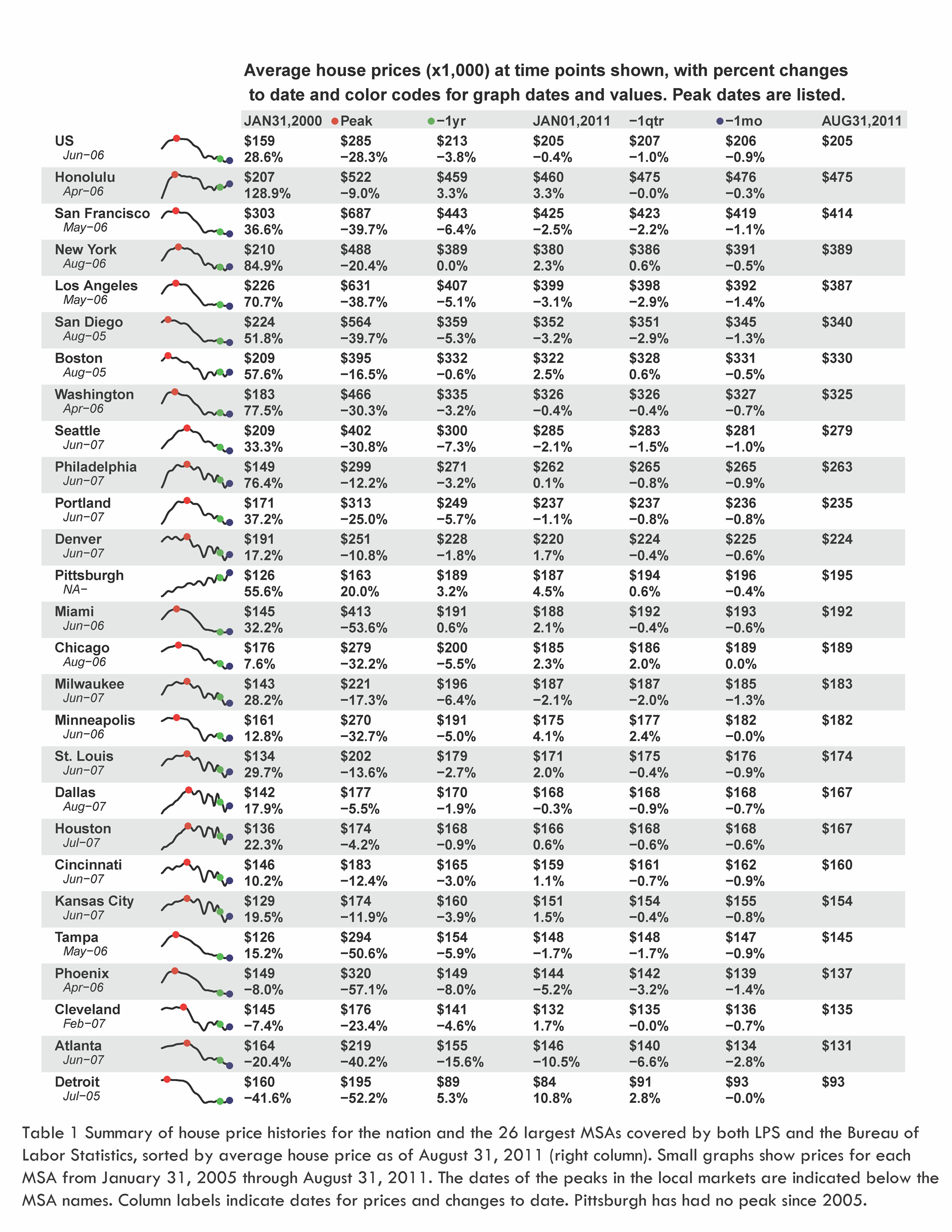

LPS: House Price Index Shows 3.8 Percent Year-Over-Year Decline in August

by Calculated Risk on 11/14/2011 09:47:00 AM

Another house price index ...

The LPS HPI is a repeat sales index that uses public disclosure by county recorders or loan origination data for purchase loans (if the sales price isn't disclosed).

From LPS: Lender Processing Services’ Home Price Index Shows 3.8 Percent Year-Over-Year Decline in U.S. Home Prices in August; Nearly 30 Percent Off Market Peak

“In August sales transactions data, we saw the national average home price decline 0.9 percent, following a decline of 0.4 percent in July. This ended a series of increases during the spring of this year; a pattern that has occurred each year since 2009. In addition, the early, partial data for September sales indicates a likely further decline of approximately 1.1 percent to come. As of the end of August, the national average home price was $205,000. This is down 3.8 percent from August last year, and down 0.4 percent from January 1, 2011.”

Click on graph for larger image.

Click on graph for larger image. Home prices in August continued the downward trend begun after the market peak in June 2006. The LPS HPI average national home price has declined 28.3 percent since then. The total value of U.S. housing inventory covered by the LPS HPI stood at $10.6 trillion at the peak. As of the end of August 2011, it was $7.65 trillion. During the period of most rapid price changes, from July 31, 2007, through December, 2009, prices declined $56,000 from $282,000. The average annual decline during that time was 13.8 percent.In 2005 - at the peak of the bubble - most reporting focused on NAR median house prices. However median prices can be distorted by the mix of homes sold. The most followed repeat sales price index in 2005 was the OFHEO HPI (now FHFA), but that index was only for the GSEs - and missed the worst loans. The Case-Shiller index didn't become widely followed until 2007, and now we have a number of house price indexes!

Since December 2009, prices have fallen more slowly, interrupted by brief seasonal intervals of rising prices. Since then, the LPS HPI national average home price has fallen $20,000 from $225,000. This corresponds to an average annual decline of 3.6 percent.

...

Average prices declined during August in all but three of the 26 largest MSAs in the country that both the LPS HPI and Bureau of Labor Statistics’ economic data cover: Chicago, Detroit and Minneapolis remained essentially unchanged. Changes ranged from -0.3 percent in Honolulu to -2.8 percent in Atlanta (Table 1).

It appears all of the indexes will show new post-bubble lows later this year - or early in 2012.

{kind=link}