RSS Feed

RSS Feed by Calculated Risk on 10/19/2010 08:30:00 AM

Tuesday, October 19, 2010

Housing Starts increase in September

Click on graph for larger image in new window.

Click on graph for larger image in new window.

Total housing starts were at 610 thousand (SAAR) in September, up 0.3% from the revised August rate of 608 thousand (revised up from 598 thousand), and up 28% from the all time record low in April 2009 of 477 thousand (the lowest level since the Census Bureau began tracking housing starts in 1959).

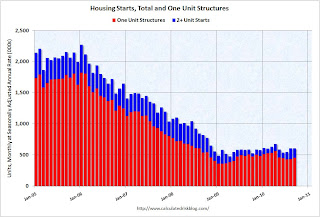

There has been an increase in multi-family starts over the last two months, although single family starts are significantly below the levels of earlier this year.

Single-family starts increased 4.4% to 452 thousand in August. This is 25% above the record low in January 2009 (360 thousand).

The second graph shows total and single unit starts since 1968. This shows the huge collapse following the housing bubble, and that housing starts have mostly been moving sideways for almost two years - with a slight up and down over the last six months due to the home buyer tax credit.

The second graph shows total and single unit starts since 1968. This shows the huge collapse following the housing bubble, and that housing starts have mostly been moving sideways for almost two years - with a slight up and down over the last six months due to the home buyer tax credit.

Here is the Census Bureau report on housing Permits, Starts and Completions.

Housing Starts:This was above expectations of 580 thousand starts, mostly because of the volatile multi-family starts. As I've mentioned many times - this low level of starts is good news for the housing market longer term (there are too many housing units already), but bad news for the economy and employment short term.

Privately-owned housing starts in September were at a seasonally adjusted annual rate of 610,000. This is 0.3 percent (±10.3%)* above the revised August estimate of 608,000 and is 4.1 percent (±12.0%)* above theSeptember 2009 rate of 586,000.

Single-family housing starts in September were at a rate of 452,000; this is 4.4 percent (±13.9%)* above the revised August figure of 433,000.

Building Permits:

Privately-owned housing units authorized by building permits in September were at a seasonally adjusted annual rate of 539,000. This is 5.6 percent (±1.4%) below the revised August rate of 571,000 and is 10.9 percent (±2.3%) below the September 2009 estimate of 605,000.

Single-family authorizations in September were at a rate of 405,000; this is 0.5 percent (±1.3%)* above the revised August figure of 403,000.

Monday, October 18, 2010

Foreclosure-Gate: GMAC resumes some foreclosures

by Calculated Risk on 10/18/2010 09:48:00 PM

Statement from GMAC: GMAC Mortgage Statement on Independent Review and Foreclosure Sales

GMAC Mortgage ... has engaged several leading legal and accounting firms to conduct independent reviews of its foreclosure procedures in each of the 50 states.Earlier I posted the BofA and Citi comments (BofA is resuming foreclosures, Citi said their foreclosure process was "sound".) Several large banks report Q3 results over the next two days (BofA, Goldman Sachs, Wells Fargo and Morgan Stanley), and I expect more comments on foreclosure issues (and possibly more questions).

...

In addition to the nationwide measures, the review and remediation activities related to cases involving judicial affidavits in the 23 states continues and has been underway for approximately two months. As each of those files is reviewed, and remediated when needed, the foreclosure process resumes. GMAC Mortgage has found no evidence to date of any inappropriate foreclosures.

On the Citi conference call this morning there were no questions on foreclosure-gate and only one on securitization issues - and that didn't provide any new information.

2010 Census: Final Weekly Payroll Update

by Calculated Risk on 10/18/2010 06:59:00 PM

The Census Bureau has released the final weekly payroll report for the 2010 Census. The report shows only 2,766 temporary workers were on the payroll for the week ending Oct 2nd.

Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the number of Census workers paid each week. The red labels are the weeks of the BLS payroll survey.

I'm providing this update because every month there is some confusion over how to report the payroll numbers in the employment report. Starting with the October employment report (to be released on November 5th), we can go back to reporting the headline number (not ex-Census), and we can ignore the impact of the temporary Census hiring on the monthly payroll numbers - well, until the next decennial Census!

Citigroup: Foreclosure Process is 'Sound', BofA expects to submit new affidavits next week

by Calculated Risk on 10/18/2010 03:38:00 PM

From Dow Jones: Citigroup Says Its Foreclosure Processing Is 'Sound' Dow Jones is reporting that the Citigroup CFO John Gerspach said they have found no issues with the foreclosure process, and they see no reason to halt foreclosures.

"While we use external attorneys to prepare [foreclosure] documents, each package is reviewed by a Citi employee, who verifies the information and signs the foreclosure affidavit in the presence of a notary," Gerspach said ...And from the WSJ: BofA Sets Timetable for Foreclosure Review. The WSJ is reporting that BofA will resubmit new affidavits for 102,000 pending foreclosures, and that they expect to resubmit the affidavits, with the proper reviews and new signatures, by October 25th.

Fed's Lockhart: QE2 is an "insurance policy" against further disinflation

by Calculated Risk on 10/18/2010 01:03:00 PM

From Atlanta Fed President Dennis Lockhart: The Challenges of Monetary Policy in Today's Economy

To opt for more quantitative easing at this juncture is a big decision. Today I will walk you through the thicket of considerations that lead me, at this moment, to be sympathetic to more monetary stimulus in the near future.Lockhart is not currently on the FOMC.

...

With current inflation running at about 1 percent or a little higher and with official unemployment measured at 9.6 percent, it's clear that the economy is not where we want it to be. In my mind, the question is whether this situation is a call to immediate action.

...

As a starting point, I expect final measures of third quarter GDP growth to be close to that in the second quarter which came in at 1.6 percent. My current forecast sees a modest increase in the rate of growth in the fourth quarter and further, but still modest, improvement in 2011. In this forecast, inflation remains low but with no further disinflation, and unemployment comes down very gradually.

In my thinking, the range of plausible divergence from this forecast is quite wide, and the risks are more to the downside.

...

In my view, the decision is not clear cut. We policymakers have to weigh these arguments pro and con, potential costs versus benefits, and competing risks. As I said earlier, I am leaning in favor of additional monetary stimulus while acknowledging the longer-term risks the policy may present. At this juncture, and given the circumstances of sluggish growth and measured inflation that is too low, I give greater weight to the risk of further disinflation leading to deflation. In my mind, QE2 is a form of risk management—an insurance policy that is prudent to put in place at this time.

Note: Lockhart see modest improvment in both GDP growth and unemployment, but I think we will see a little more weakness in GDP growth and the unemployment rate will even tick up a little from 9.6%.

NAHB Builder Confidence increases in October

by Calculated Risk on 10/18/2010 10:00:00 AM

The National Association of Home Builders (NAHB) reports the housing market index (HMI) was at 16 in October. This is a 3 point increase from 13 in September, and is the highest level since June. The record low was 8 set in January 2009, and 16 is still very low ...

Note: any number under 50 indicates that more builders view sales conditions as poor than good.

Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph compares the NAHB HMI (left scale) with single family housing starts (right scale). This includes the October release for the HMI and the August data for starts (September starts will be released tomorrow).

This shows that the HMI and single family starts mostly move in the same direction - although there is plenty of noise month-to-month.

Press release from the NAHB: Builder Confidence Improves in October

Builder confidence in the market for newly built, single-family homes rose three points to 16 on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI) for October, released today. This was the first improvement registered by the HMI in five months, and returns the index to a level last seen in June of this year.

...

All three of the HMI's component indexes registered gains in October. The index gauging current sales conditions rose three points to16, while the index gauging sales expectations in the next six months rose five points to 23 and the index gauging traffic of prospective buyers rose two points to 11.

Industrial Production, Capacity Utilization decreased in September

by Calculated Risk on 10/18/2010 09:15:00 AM

From the Fed: Industrial production and Capacity Utilization

Industrial production decreased 0.2 percent in September after having increased 0.2 percent in August. ... The capacity utilization rate for total industry edged down to 74.7 percent, a rate 4.2 percentage points above the rate from a year earlier but 5.9 percentage points below its average from 1972 to 2009.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows Capacity Utilization. This series is up 9.5% from the record low set in June 2009 (the series starts in 1967).

Capacity utilization at 74.7% is still far below normal - and well below the pre-recession levels of 81.2% in November 2007.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production declined slightly in September, and production is still 7.5% below the pre-recession levels at the end of 2007.

This is below consensus expectations of a 0.2% increase in Industrial Production, and an increase to 74.8% (from 74.7% before revision) for Capacity Utilization.

Sunday, October 17, 2010

Schedule additions: Large Bank Financial Results

by Calculated Risk on 10/17/2010 09:53:00 PM

Here is the Schedule for Week of Oct 17th

Here is the Summary for Week ending Oct 16th (with plenty of graphs).

I've updated the schedule to include financial results for several large banks (ht Tony). Usually I wouldn't include an earnings calendar, but I'll be looking for comments on Foreclosure-Gate (and other comments).

The additions are:

HUD Secretary on Foreclosure-Gate: "Will respond with full force of the law"

by Calculated Risk on 10/17/2010 07:49:00 PM

From the HuffPo: How We Can Really Help Families

The recent revelations about foreclosure processing -- that some banks may be repossessing the homes of families improperly -- has rightly outraged the American people. The notion that many of the very same institutions that helped cause this housing crisis may well be making it worse is not only frustrating -- it's shameful.I hope actions follow words.

...

[T]he Obama Administration has a comprehensive review of the situation underway and will respond with the full force of the law where problems are found. The Financial Fraud Enforcement Task Force that President Obama established last November has made this issue priority number one.

Schedule for Week of Oct 17th

by Calculated Risk on 10/17/2010 02:15:00 PM

Note: The previous post was the weekly summary for last week.

Two key housing reports will be released this week: September housing starts (Tuesday) and October homebuilder confidence (Monday). Also the Fed will release September industrial production and capacity utilization (Tuesday).

Update: Large bank earnings added for comments on Foreclosure-Gate.

CoreLogic House Price Index for August. This release will probably show further declines in house prices. The index is a weighted 3 month average for June, July and August.

Making Home Affordable Program (HAMP) for September and the “Housing Scorecard”

8:00 AM ET: Citigroup Third Quarter 2010 Earnings Review

9:15 AM ET: The Fed will release Industrial Production and Capacity Utilization for September. The consensus is for a 0.2% increase in Industrial Production, and an increase to 74.8% (from 74.7%) for Capacity Utilization.

10 AM: The October NAHB homebuilder survey. This index collapsed following the expiration of the home buyer tax credit. The consensus is for a slight increase to 14 from 13 in September (still very depressed).

12:55 PM Atlanta Fed President Dennis Lockhart speaks at Savannah Rotary Club.

8:00 AM: Bank of America Q3 2010 Earnings

8:00 AM: Goldman Sachs earnings

8:30 AM: Housing Starts for September. Housing starts also collapsed following the expiration of the home buyer tax credit. The consensus is for a decrease to 580,000 (SAAR) in September from 598,000 in August. Note: the August increase was mostly from multi-family starts.

Morning: Moody's/REAL Commercial Property Price Index (CPPI) for August.

Various Fed Speeches scheduled: NY Fed's Dudley, Chicago Fed’s Evans at about 10 AM, Dallas Fed’s Fisher and Minneapolis Fed’s Kocherlakota at about 1:00 PM.

Early: The AIA's Architecture Billings Index for September will be released (a leading indicator for commercial real estate). This has been showing ongoing contraction, and usually this leads investment in non-residential structures (hotels, malls, office) by 9 to 12 months.

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index declined sharply following the expiration of the tax credit, and the index has only recovered slightly over the last few months even with record low mortgage rates.

7:30 AM: Morgan Stanley third quarter 2010 financial results

8:00 AM: Wells Fargo earnings

2:00 PM: The Fed’s Beige Book for early October. This is anecdotal information on current economic conditions.

Fed Speeches: Philly Fed's Plosser at about 1:00 PM and Richmond Fed's Lacker at 4:00 PM.

8:30 AM: The initial weekly unemployment claims report will be released. Consensus is for about a decrease to 455,000 from 462,000 last week (still elevated).

10:00 AM: Philly Fed Survey for October. This survey showed contraction over the last two months. The consensus is for a slight increase to 1.8 from -0.7 in September.

10:00 AM: Conference Board's index of leading indicators for August. The consensus is for a 0.3% increase in this index.

Fed Speeches: St Louis Fed's Bullard at about 10:00 AM, and Kansas City Fed's Hoenig at 9:45 PM.

10:00 AM: the BLS will release the Regional and State Employment and Unemployment report for September.

After 4:00 PM: The FDIC will probably have another busy Friday afternoon ...