RSS Feed

RSS Feed by Calculated Risk on 6/13/2010 11:59:00 AM

Sunday, June 13, 2010

Weekly Summary and a Look Ahead

Two housing related reports will be released this week: the NAHB builder confidence survey on Tuesday and housing starts on Wednesday.

On Tuesday, the June Empire State manufacturing survey will be released at 8:30 AM. The consensus is for a slight increase from the May reading. Also on Tuesday, the June NAHB homebuilder survey will be released at 10 AM. The consensus is for about the same level as May.

Also on Tuesday, St. Louis Fed President James Bullard will speak on "Getting Serious About Asset Bubbles and Monetary Policy" in Hong Kong at 6:15 AM ET.

On Wednesday, Housing Starts for May will be released at 8:30 AM. The consensus is for a 3.3% decrease to 650K (SAAR) in May from 672K in April. Based on the sharp decline for permits in April, starts might fall even further in May (I'll take the under this month). Also at 8:30 AM, the BLS will release the Producer Price Index (PPI) for May. The consensus is for a decrease of 0.5%.

Also on Wednesday, the MBA will release the mortgage purchase applications index. This has been falling sharply suggesting a sharp decline in home sales after the expiration of the tax credit. And the Federal reserve will release the May Industrial Production and Capacity Utilization report at 9:15 AM. Expectations are for production to increase 1% and capacity utilization to increase to 74.5% (the highest levels since late 2008).

On Thursday, the May Consumer Price Index (CPI) will be released at 8:30 AM. The consensus is for a 0.2% decrease in prices. Also on Thursday, the closely watched initial weekly unemployment claims will be released. Consensus is for a decline to 450K from 456K last week. Also on Thursday, the Philly Fed survey and the Conference Board's index of leading indicators will both be released at 10 AM.

And on Friday, the BLS will release the Regional and State Employment and Unemployment report for May at 10 AM. And of course the FDIC will probably have another busy Friday afternoon ...

And a summary of last week:

On a monthly basis, retail sales decreased 1.2% from April to May (seasonally adjusted, after revisions), and sales were up 6.9% from May 2009 (easy comparison).

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows retail sales since 1992. This is monthly retail sales, seasonally adjusted (total and ex-gasoline).

The red line shows retail sales ex-gasoline and shows the increase in final demand ex-gasoline has been sluggish.

Retail sales are up 8% from the bottom, but still off 4.6% from the pre-recession peak.

This graph shows the MBA Purchase Index and four week moving average since 1990.

This graph shows the MBA Purchase Index and four week moving average since 1990.The purchase index has collapsed following the expiration of the tax credit suggesting home sales will fall sharply too. This is the lowest level for the purchase index since February 1997. From the MBA:

“Purchase and refinance applications dropped this week, even after an adjustment for the Memorial Day holiday. Purchase applications are now 35 percent below their level of four weeks ago, as homebuyers have not yet returned to the market following the expiration of the homebuyer tax credit at the end of April,” said Michael Fratantoni, MBA’s Vice President of Research and Economics.

The Association of American Railroads reported traffic in May 2010 was up 15.8% compared to May 2009 - and traffic was still 11.8% lower than in May 2008.

The Association of American Railroads reported traffic in May 2010 was up 15.8% compared to May 2009 - and traffic was still 11.8% lower than in May 2008.This graph shows U.S. average weekly rail carloads. Traffic increased in 18 of 19 major commodity categories YoY.

From AAR:

U.S. railroads averaged 294,758 carloads per week in April 2010 and 288,793 in March 2010. Thus, May 2010’s average was actually down slightly from those months ... One month does not a trend make, but it would obviously be worrisome if the decline continued.

The Census Bureau reports:

[T]otal April exports of $148.8 billion and imports of $189.1 billion resulted in a goods and services deficit of $40.3 billion, up from $40.0 billion in March, revised. April exports were $1.0 billion less than March exports of $149.8 billion. April imports were $0.8 billion less than March imports of $189.9 billion.

This graph shows the U.S. trade deficit, with and without petroleum, through April.

This graph shows the U.S. trade deficit, with and without petroleum, through April.The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

Although both imports and exports were off slightly in April, both have been increasing sharply - but are still below the pre-crisis levels. Once again China and oil are the major contributors to the trade deficit.

Best wishes to all.

Obama Pushes for $50 Billion in State Aid

by Calculated Risk on 6/13/2010 08:13:00 AM

From Jackie Calmes and Sheryl Gay Stolberg at the NY Times: Obama Presses for Aid to Cities and States

President Obama on Saturday implored Congress to provide more aid to states and cities to blunt “the devastating economic impact of budget cuts” by local governments that imperil the jobs of teachers, the police, firefighters and other public employees.The WaPo quotes Obama as writing there will be "massive layoffs of teachers, police and firefighters" without the additional funds.

In a letter to Democratic and Republican Congressional leaders, Mr. Obama said the “mounting employment crisis” in the states “could set back the pace of our economic recovery.” ... education secretary, Arne Duncan, has said that without federal aid, up to 300,000 fewer teachers would be in classrooms this fall ...

Saturday, June 12, 2010

FHA Reform Bill Passes House

by Calculated Risk on 6/12/2010 10:11:00 PM

Just an update on H.R. 5072: FHA Reform Act of 2010

The bill passed in the house 406-4. This bill has several provisions, but a key for the housing market is the increase in the maximum annual premium payments for mortgage insurance.

The current maximum is an annual premium of 0.50% of the outstanding principal balance for loans with the original principal obligation under 95% LTV, and 0.55% for loans with the original principal obligation over 95% LTV.

This legislation will increase the maximums to 1.50% and 1.55% respectively.

The proposed effective date is September 30, 2010. There is no senate version yet.

Unofficial Problem Bank List: 760 Institutions

by Calculated Risk on 6/12/2010 04:09:00 PM

This is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for June 11, 2010.

Changes and comments from surferdude808:

Extremely quiet week for the Unofficial Problem Bank List as the OCC did not release its actions for May. No doubt that will happen next week.CR Note: A special thanks to surferdude808 for tracking all the institutions and compiling this list (no one else is doing this).

Only three changes to report. There were two removals -- the failed Washington First International Bank ($521 million) and an action termination by the OCC against Mission Oaks National Bank ($187 million Ticker: MOKB).

The other change is an updated Prompt Corrective Action against Imperial Savings and Loan Association ($9.6 million).

The Unofficial Problem Bank List stands at 760 institutions with aggregate assets of $385 billion.

Q1 2010: Mortgage Equity Withdrawal strongly Negative

by Calculated Risk on 6/12/2010 01:15:00 PM

Note: This is not Mortgage Equity Withdrawal (MEW) data from the Fed. The last MEW data from Fed economist Dr. Kennedy was for Q4 2008. My thanks to Jim Kennedy and the other Fed contributors for the previous MEW updates. For those interested in the last Kennedy data, here is a post, and the spreadsheet from the Fed is available here.

The following data is calculated from the Fed's Flow of Funds data and the BEA supplement data on single family structure investment. This is an aggregate number, and is a combination of homeowners extracting equity (hence the name "MEW", but there is very little MEW right now!), normal principal payments and debt cancellation. Click on graph for larger image in new window.

Click on graph for larger image in new window.

For Q1 2010, the Net Equity Extraction was a record low of minus $122 billion, or a negative 4.4% of Disposable Personal Income (DPI). This is not seasonally adjusted.

This graph shows the net equity extraction, or mortgage equity withdrawal (MEW), results, using the Flow of Funds (and BEA data) compared to the Kennedy-Greenspan method.

The Fed's Flow of Funds report showed that the amount of mortgage debt outstanding declined sharply in Q1, and this was probably mostly because of debt cancellation per foreclosure sales, and some from modifications, and partially due to homeowners paying down their mortgages as opposed to borrowing more. Note: most homeowners pay down their principal a little each month unless they have an IO or Neg AM loan, so with no new borrowing, equity extraction would always be slightly negative.

Mark Whitehouse at the WSJ argues: Default, Not Thrift, Pares U.S. Debt

The falling debt burden conjures up images of a nation seeking to repent after a decade of profligacy, conscientiously paying down mortgages and credit-card balances. That may be true in some cases, but it’s not the norm. In fact, people are making much more progress in shedding their debts by defaulting on mortgages and reneging on credit cards.I think that is correct - most of the decline in mortgage debt outstanding is probably because of debt cancellations via foreclosures, short sales, and some modifications.

N.Y. State "classic budgetary sleight-of-hand"

by Calculated Risk on 6/12/2010 08:38:00 AM

From Danny Hakim at the NY Times: New York Plan Makes Fund Both Borrower and Lender (ht jb)

Gov. David A. Paterson and legislative leaders have tentatively agreed to allow the state and municipalities to borrow nearly $6 billion to help them make their required annual payments to the state pension fund.Oh my ...

And, in classic budgetary sleight-of-hand, they will borrow the money to make the payments to the pension fund — from the same pension fund.

Daily Show: More Spilling Fields

by Calculated Risk on 6/12/2010 12:49:00 AM

Since we all need a laugh ...

| The Daily Show With Jon Stewart | Mon - Thurs 11p / 10c |

| The Spilling Fields - BP Ad Campaign | |

Friday, June 11, 2010

Bank Failure #82: Washington First International Bank, Seattle, WA

by Calculated Risk on 6/11/2010 08:11:00 PM

Sucked up TARP funds like sponges

Wrung dry by losses

by Soylent Green is People

From the FDIC: East West Bank, Pasadena, California, Assumes All of the Deposits of Washington First International Bank, Seattle, Washington

As of March 31, 2010, Washington First International Bank had approximately $520.9 million in total assets and $441.4 million in total deposits. ...It wouldn't be Friday without a bank failure ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $158.4 million. .... Washington First International Bank is the 82nd FDIC-insured institution to fail in the nation this year, and the seventh in Washington. The last FDIC-insured institution closed in the state was Frontier Bank, Everett, on April 30, 2010.

Housing Tax Credit Fraud Extension

by Calculated Risk on 6/11/2010 06:20:00 PM

No one could have predicted ...

James Hagerty at the WSJ has the story: Tax Credit Extension Could Help Tax Cheaters. Hagerty discusses comments from two real estate agents: Glenn Kelman, chief executive of Redfin Corp. who noted that some customers who signed contracts after April 30th were pushing to close by June 30th. Kelman suspects fraud. And Schahrzad Berkland, an agent for Fidelity Pacific Real Estate in San Diego who noticed that pending sales for April have continued to rise ... something that is very odd. (Note to FBI: more fraud for you guys!)

I noted yesterday: "I'm sure some people will commit fraud and backdate documents."

Extending the closing date will encourage even more fraud. All the mortgage lenders have been giving priority to purchase applications over refinance applications, and 60 days is more than enough time.

If short sales are a problem, then make the extension very narrow - a 30 day extension for short sales, with the servicer processing the short sale certifying that it was 1) a short sale and 2) that they were in possession of a signed contract by April 30th (with a significant penalty for a false statement).

Otherwise this extension should be titled the "Housing Tax Credit Fraud Extension Amendment". Geesh ...

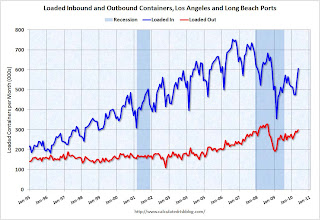

LA Port Traffic: Imports Surge Year-over-year in May

by Calculated Risk on 6/11/2010 03:58:00 PM

Notes: this data is not seasonally adjusted. There is a very distinct seasonal pattern for imports, but not for exports. LA area ports handle about 40% of the nation's container port traffic.

Sometimes port traffic gives us an early hint of changes in the trade deficit. The following graph shows the loaded inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container). Although containers tell us nothing about value, container traffic does give us an idea of the volume of goods being exported and imported. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Loaded inbound traffic was up 18.3% compared to May 2009. Inbound traffic was still down 5% vs. two years ago (May 08).

Loaded outbound traffic was up 9.4% from May 2009. Just as with imports, exports are still off from 2 years ago (off 7.3%).

For imports there is usually a significant dip in either February or March, depending on the timing of the Chinese New Year, and then usually imports increase until late summer or early fall as retailers build inventory for the holiday season. So this increase in May imports is part of the normal seasonal pattern.

Based on this data, it appears the trade deficit with Asia increased in May. Once again it appears imports are increasing faster than exports and the pre-crisis global imbalances have returned.