RSS Feed

RSS Feed by Calculated Risk on 5/02/2010 09:01:00 AM

Sunday, May 02, 2010

Greece Reaches Bailout Deal

From the NY Times: Greece Reaches Agreement on Bailout

Prime Minister George Papandreou said Sunday that Greece had reached an agreement with the International Monetary Fund and European Union on a long-delayed rescue package that is expected to be as much as €120 billion.More details will be available later today. Greece might be in recession for several years ...

...

Finance Minister George Papaconstantinou set out some of the details of the austerity measures that are required for the bailout package, which were expected to be revealed in Brussels later Sunday. He said that Greece would make budget cuts of €30 billion, or $40 billion, to reduce the budget deficit to below 3 per cent by 2014.

...

Indicating that the steps would undermine economic growth, Mr. Papaconstantinou forecast a deeper than expected recession of 4 per cent for 2010, and 2.6 percent in 2011, before the economy returned to growth of 1.1 percent in 2012.

“We will be in recession for the next few years which means that we have to run faster to reduce the deficit,” he said.

More details from Bloomberg: Greece Accepts Terms of EU-Led Bailout, ‘Savage’ Cuts

Saturday, May 01, 2010

Fed Discussed Possible Housing Bubble in 2004

by Calculated Risk on 5/01/2010 08:53:00 PM

The Fed released the transcripts for the 2004 FOMC meeting this week. There definitely was some mention of a possible housing bubble, but little discussion.

From June 30, 2004:  Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the Fed estimate of the rent-to-price ratio in June 2004. Usually this is drawn inverted (Price-to-rent). And this was after the Fed made some technical adjustments - otherwise, in the words of a Fed researcher, the graph would "have looked more alarming".

MR. FERGUSON [Roger Ferguson, Fed Vice Chairman in 2004]: The other question I have deals with chart 3, on housing prices. My question is about the footnote, which says that the rent–price ratio is adjusted for biases in the trends of both rents and prices. Is that where you pick up demographics and lifecycle factors? What are these biases in the trends, and how does one think about changing demographics and the relative attractiveness of owning a home versus renting? Give me some sense of whether or not the shape of the curve that you show here is likely to reverse, as you imply, or likely to stay relatively low.

MR. OLINER [Stephen Oliner, Fed associate research director]: The biases referred to in that footnote were really technical biases in the construction of the two measures shown here, the rent measure and the price measure. Had we not adjusted for them, the rent-to-price ratio would have been much lower at the end point. So it would have looked more alarming. In part we think the published data have some technical problems that need to be taken care of before this analysis can be done in a way that is meaningful. With regard to the question of owning versus renting, it depends to some extent on what is happening to interest rates because that changes that calculation at the margin. So it’s really important to plot any kind of valuation measure relative to an opportunity cost. Just showing the rent-to-price ratio I think would have been somewhat misleading; it’s really that gap that we think is the meaningful measure of valuation. And it looks somewhat rich, taking account of the fact that interest rates are relatively low and income growth has been relatively strong. I don’t want to leave the impression that we think there’s a huge housing bubble. We believe a lot of the rise in house prices is rooted in fundamentals. But even after you account for the fundamentals, there’s a part of the increase that is hard to explain.

And a couple of comments from the March 2004 meeting:

MR. GUYNN [Atlanta Fed President]: We keep looking to our directors and other contacts for indications of imbalances and pricing pressures that they might see developing, and we’ve begun to get hints of both. A number of folks are expressing growing concern about potential overbuilding and worrisome speculation in the real estate markets, especially in Florida. Entire condo projects and upscale residential lots are being pre-sold before any construction, with buyers freely admitting that they have no intention of occupying the units or building on the land but rather are counting on “flipping” the properties—selling them quickly at higher prices.

...

MR. KOHN [Fed Governor]: House prices are elevated relative to rents—and will look even more so when rates begin to rise—but are more likely to correct by rising less rapidly than by crashing. Eggs will get broken when rates begin to rise, but the capital in most intermediaries is high, and the system is resilient.

CR: Rampant speculation, an "alarming" price-to-rent chart, prices rising faster than explained by fundamentals, "eggs will be broken" - and this was in 2004. And Kohn was wrong - the system wasn't "resilient".

Investment Contributions to GDP: Leading and Lagging Sectors

by Calculated Risk on 5/01/2010 03:57:00 PM

By request, the following graph is an update to: The Investment Slump in Q2 2009

The following graph shows the rolling 4 quarter contribution to GDP from residential investment, equipment and software, and nonresidential structures. This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy.

For the following graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. The usual pattern - both into and out of recessions is - red, green, blue. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Residential Investment (RI) made a small positive contribution to GDP in the second half of 2009, but was a drag in Q1 2010. The rolling four quarter change is moving up, but as expected there has been no strong boost to GDP from RI.

Equipment and software investment has made a positive contribution to GDP for three straight quarters (it is coincident).

Nonresidential investment in structures continues to be a drag on the economy, and as usual the economy is recovering long before nonresidential investment in structures recovers.

The key leading sector - residential investment - is lagging the recovery because of the huge overhang of existing inventory. Usually RI is a strong contributor to GDP growth and employment in the early stages of a recovery, but not this time - and this is a key reason why the recovery has been sluggish so far.

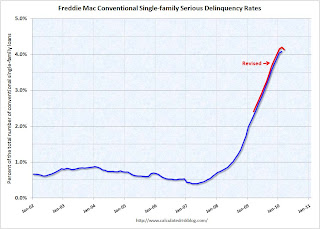

Freddie Mac: 90+ Day Delinquency Rate at 4.13% in March

by Calculated Risk on 5/01/2010 11:57:00 AM

Note: Freddie Mac reported the serious delinquency rate decreased in March from February, but that is only after the previous months were revised higher. Also there might be some distortion from the modification program - loans in trial mods were considered delinquent until the modifications were made permanent. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business decreased to 4.13% in March 2010, down from 4.20% in February - and up from 2.41% in March 2009.

"Single-family delinquencies are based on the number of mortgages 90 days or more delinquent or in foreclosure as of period end ..."

The data from Fannie Mae will be released next week ...

96.5% of Mortgages Backed by Government entities in Q1

by Calculated Risk on 5/01/2010 08:42:00 AM

From Nick Timiraos at the WSJ: U.S. Role in Mortgage Market Grows Even Larger

Government-related entities backed 96.5% of all home loans during the first quarter, up from 90% in 2009, according to Inside Mortgage Finance.The following graph from San Francisco Fed Senior Economist John Krainer puts this in perspective (from Oct 2009): Recent Developments in Mortgage Finance

As the U.S. housing market has moved from boom in the middle of the decade to bust over the past two years, the sources of mortgage funding have changed dramatically. The government-sponsored enterprises—Fannie Mae, Freddie Mac, and Ginnie Mae—now own or guarantee an overwhelming share of originations. At the same time, non-agency mortgage securitization and loans retained in lender portfolios have largely dried up.

Click on graph for slightly larger in new window.

Click on graph for slightly larger in new window.This is figure 3 from the Economic Letter.

[T]he sources of mortgage finance have shifted as the housing market has gone from boom to bust. Figure 3 plots the evolution of these funding sources over the past decade. Fannie Mae and Freddie Mac combined have consistently been the largest players in the market, owning or guaranteeing about half or more of the mortgages in the sample at any given time. Non-agency securitization peaked in the first quarter of 2006, when it accounted for nearly 40% of new originations. Finally, the share of mortgages retained in the originating institution's portfolio averaged about 15% throughout the boom, but has fallen considerably since.Without the government backed entities there would be almost no mortgage market. We are a long way from normal ...

...

With the vast majority of current mortgage lending now intermediated in some form by the GSEs, it will be difficult for the housing market to return to normal.

Friday, April 30, 2010

Unofficial Problem Bank List hits 722

by Calculated Risk on 4/30/2010 11:46:00 PM

This is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for April 30, 2010.

Changes and comments from surferdude808:

Failure Friday and the FDIC issuing its enforcement actions for March contributed to many changes in the Unofficial Problem Bank List.The list keeps growing ...

Of the seven failures this week, six were on the list including Westernbank Puerto Rico ($11.9 billion), R-G Premier Bank of Puerto Rico ($6.1 billion), Frontier Bank ($3.6 billion), Eurobank ($2.6 billion), CF Bancorp ($1.7 billion), and BC National Banks ($67 million). There was one other removal as the action against University Bank ($134 million) was terminated.

Thirty-five institutions with aggregate assets of $9.8 billion made their first appearance on the list this week. Among the additions are FSGBank, National Association, Chattanooga, TN ($1.4 billion Ticker: FSGI); Centennial Bank, Fountain Valley, CA ($848 million); Beach Community Bank, Fort Walton Beach, FL ($706 million Ticker: BCBF); and CIBM Bank, Champaign, IL ($698 million Ticker: CIBH). The additions include four institutions based in Illinois, Minnesota, and Nevada, and three in Florida, Georgia, Texas, and Washington.

The FDIC also issued Prompt Corrective Action orders against a few banks already on the Unofficial Problem Bank List including Nevada Security Bank, Reno, NV ($502 million) and Sun West Bank, Las Vegas, NV ($381 million). After the failures and additions, the Unofficial Problem Bank List stands at 722 institutions with aggregate assets of $349.8 billion.

This week, Cascade Bank, Everett, WA ($1.7 billion Ticker: CASB) disclosed that it now expects to sign a Consent Order in Q2."[I]n light of the current challenging operating environment, along with our elevated level of nonperforming assets and adversely classified assets and our recent operating results, we expect Cascade Bank to enter into a Consent Order with the FDIC and Washington State DFI during the second quarter. We expect that under the Order, Cascade Bank will be required, among other things, to improve asset quality and reduce classified assets; to improve profitability; and to increase Tier 1 capital.

We also expect the Company will enter into a similar Order with the Federal Reserve Bank of San Francisco."

Bank Failure #64: Frontier Bank, Everett, Washington

by Calculated Risk on 4/30/2010 09:14:00 PM

A limitless horizon

Much like our debt load.

by Soylent Green is People

From the FDIC: Union Bank, National Association, San Francisco, California, Assumes All of the Deposits of Frontier Bank, Everett, Washington

Frontier Bank, Everett, Washington, was closed today by the Washington Department of Financial Institutions, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ...Is that about $7 billion today?

As of December 31, 2009, Frontier Bank had approximately $3.50 billion in total assets and $3.13 billion in total deposits. ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $1.37 billion. ... Frontier Bank is the 64th FDIC-insured institution to fail in the nation this year, and the sixth in Washington. The last FDIC-insured institution closed in the state was City Bank, Lynnwood, on April 16, 2010.

Bank Failure #63: BC National Banks, Butler, Missouri

by Calculated Risk on 4/30/2010 07:33:00 PM

Deposits gone with the wind

I don't give a damn

by Soylent Green is People

From the FDIC:Community First Bank, Butler, Missouri, Assumes All of the Deposits of BC National Banks, Butler, Missouri

BC National Banks, Butler, Missouri, was closed today by the Office of the Comptroller of the Currency, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ..

As of December 31, 2009, BC National Banks had approximately $67.2 million in total assets and $54.9 million in total deposits. ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $11.4 million. ... BC National Banks is the 63rd FDIC-insured institution to fail in the nation this year, and the third in Missouri. The last FDIC-insured institution closed in the state was Champion Bank, Creve Coeur, earlier today.

Bank Failure #62: Champion Bank, Creve Coeur, Missouri

by Calculated Risk on 4/30/2010 06:34:00 PM

The breakfast of Champion

They drank our milk shake

by Soylent Green is People

From the FDIC: Bankliberty, Liberty, Missouri, Assumes All of the Deposits of Champion Bank, Creve Coeur, Missouri

Champion Bank, Creve Coeur, Missouri, was closed today by the Missouri Division of Finance, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ...Busy day ...

As of December 31, 2009, Champion Bank had approximately $187.3 million in total assets and $153.8 million in total deposits....

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $52.7 million. ... Champion Bank is the 62nd FDIC-insured institution to fail in the nation this year, and the second in Missouri. The last FDIC-insured institution closed in the state was Bank of Leeton, Leeton, on January 22, 2010.

Bank Failure #61: CF Bancorp, Port Huron, Michigan

by Calculated Risk on 4/30/2010 06:23:00 PM

Autos and banks only hope

Federal bailouts.

by Soylent Green is People

From the FDIC: First Michigan Bank, Troy, Michgan, Assumes All of the Deposits of CF Bancorp, Port Huron, Michigan

CF Bancorp, Port Huron, Michigan, was closed today by the Michigan Office of Financial and Insurance Regulation, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ...That makes four today ... "only" $615 million cost ...

As of December 31, 2009, CF Bancorp had approximately $1.65 billion in total assets and $1.43 billion in total deposits....

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $615.3 million. ... CF Bancorp is the 61st FDIC-insured institution to fail in the nation this year, and the second in Michigan. The last FDIC-insured institution closed in the state was Lakeside Community Bank, Sterling Heights, on April 16, 2010.