RSS Feed

RSS Feed by Calculated Risk on 1/28/2008 09:29:00 AM

Monday, January 28, 2008

Blackstone ADS Deal "Unlikely"

From the WSJ: ADS Says Blackstone Deal Unlikely

Alliance Data Systems Corp. ... Blackstone ... likely won't go through with its $6.4 billion acquisition ..."Extraordinary measures" are usually doable during better times. This seems like another way to leave your lover (from Paul Simon):

... Blackstone told the data processor and marketing firm in a letter late Friday it doesn't expect the deal to get the necessary approvals from OCC and that the regulator is demanding "extraordinary measures" which "represent operational and financial burdens ... that cannot be reasonably assumed."

You just slip out the back, Jack

Make a new plan, Stan

You don't need to be coy, Roy

Just get yourself free

Sunday, January 27, 2008

60 Minutes: House of Cards

by Calculated Risk on 1/27/2008 08:36:00 PM

House of Cards (video): "Steve Kroft reports on how the U.S. sub-prime mortgage meltdown, in which risky loans drove a housing boom that went bust, is now roiling capital markets worldwide."

Here is the foreclosure site mentioned in the story. I live in a neighborhood that is "immune" to the housing bust. Oh yeah, that site shows a number of REOs and preforeclosure homes in my neighborhood.

New Trend: "Intentional Foreclosure"

by Calculated Risk on 1/27/2008 12:23:00 PM

From CBS: New Trend In Sacramento: 'Intentional Foreclosure' (hat tip Shawn)

Linda Caoli helps lots of families on the verge of losing their homes, including a single mom working two jobs to pay her mortgage.This is similar to Peter Viles' story in the LA Times: A tipping point? "Foreclose me ... I'll save money".

"She says Linda the house across the street, same model, with more upgrades sold in foreclosure for $315,000!" explains Linda.

Her client isn't the only one thinking about ditching her house to buy the better deal across the street. A number of realtors CBS13 talked to say it's already happening.

Wachovia is seeing this too (from their Jan 22nd conference call):

“... people that have otherwise had the capacity to pay, but have basically just decided not to because they feel like they've lost equity ...”And from BofA CEO Kenneth Lewis in December:

"There's been a change in social attitudes toward default. We're seeing people who are current on their credit cards but are defaulting on their mortgages. I'm astonished that people would walk away from their homes."This change in social attitudes could lead to a flood of foreclosures. The following is from my post last December: Homeowners With Negative Equity

The following graph shows the number of homeowners with no or negative equity, using the most recent First American data, with several different price declines.

At the end of 2006, there were approximately 3.5 million U.S. homeowners with no or negative equity. (approximately 7% of the 51 million household with mortgages).

At the end of 2006, there were approximately 3.5 million U.S. homeowners with no or negative equity. (approximately 7% of the 51 million household with mortgages).By the end of 2007, the number will have risen to about 5.6 million.

If prices decline an additional 10% in 2008, the number of homeowners with no equity will rise to 10.7 million.

The last two categories are based on a 20%, and 30%, peak to trough declines. The 20% decline was suggested by MarketWatch chief economist Irwin Kellner (See How low must housing prices go?) and 30% was suggested by Paul Krugman (see What it takes).

Intentional foreclosure. Jingle Mail. Negative Equity. All terms that could be common in 2008.

Saturday, January 26, 2008

Mortgage Due Diligence Firm Granted Immunity, Cooperating with Prosecutors

by Calculated Risk on 1/26/2008 10:49:00 PM

Jenny Anderson and Vikas Bajaj at the NY Times report: Reviewer of Subprime Loans Agrees to Aid Inquiry (hat tip James)

Clayton Holdings, a company ... that vetted home loans for many investment banks, has agreed to provide important documents and the testimony of its officials to the New York attorney general, Andrew M. Cuomo, in exchange for immunity from civil and criminal prosecution in the state.It seems the key question here is: Did the investment banks adequately disclose the information from Clayton to the investors in the mortgage securities?

... Clayton has told the prosecutors that starting in 2005, it saw a significant deterioration of lending standards and a parallel jump in lending exceptions. In an another sign that the industry was becoming less careful, some investment banks directed Clayton to halve the sample of loans it evaluated in each portfolio, a person familiar with the investigation said.

...

It is unclear how many lending exceptions are contained in the $1 trillion subprime mortgage market, but industry participants cite figures ranging from about 50 percent to 80 percent for some loan portfolios they examined.

Bank and Thrift Failures

by Calculated Risk on 1/26/2008 06:05:00 PM

The FDIC announced the first bank failure of 2008 last night. To put that into context, here is a graph of bank and thrift failures since the FDIC was created in 1934.

| Click on graph for larger image. The huge spike in the '80s was due to the S&L crisis. It's interesting to note that even with the failure of almost 3,000 banks and thrifts during the S&L crisis, the overall economy was healthy. |  |

The second graph includes the 1920s and shows that failures during the S&L crisis were far less than during the '20s (before the FDIC was enacted).

The second graph includes the 1920s and shows that failures during the S&L crisis were far less than during the '20s (before the FDIC was enacted).Note how small the S&L crisis appears on this graph!

During the Roaring '20s, 500 bank failures per year was common - even with a booming economy - with depositors typically losing 30% to 40% of their bank deposits in the failed institutions. The number of bank failures soared to 4000 (estimated) in 1933.

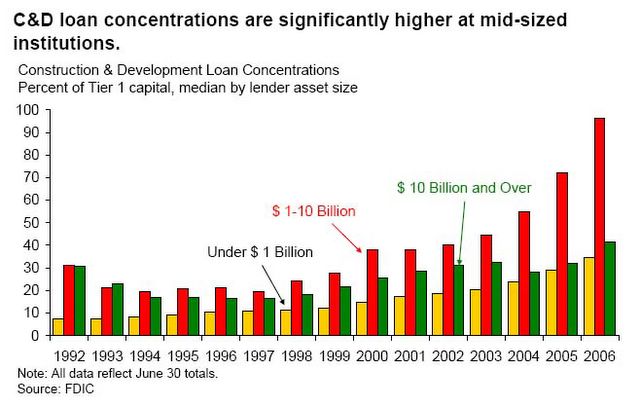

It's important to note that the housing bust hasn't hurt most small banks and institutions, because the banks didn't hold many of the residential mortgages they originated. Instead the small to mid-sized institutions focused on commercial real estate (CRE), construction and development (C&D) and other loans.

From the December 2006 FDIC report: Economic Conditions and Emerging Risks in Banking.

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. ... small and mid-size institutions have been ... assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loan concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.Now credit standards are being tightened, and many of these small and mid-sized institutions are seeing rising defaults on their CRE and C&D loans. So 2008 is when we would expect to see more of these small and mid-sized institutions start to fail, but the number of failures will probably be small as compared to the '80s.

Update: Here is an addition from the

Atlanta's residential bust is rapidly becoming a financial disaster on a par with the Savings and Loan Crisis of the 1980s.The article (subscription) reports that at the peak of the S&L crisis, the non-performing loans reached 4.4% for Altanta based banks (compared to 2.2% at the end of Q3 2007). However the article quotes several bankers and industry analysts that believe the percent of non-performing loans increased significantly in Q4, and will rise sharply in 2008.

Commenting

by Anonymous on 1/26/2008 04:08:00 PM

CR and I have discussed going to some kind of registration-based commenting software. There are many good reasons to do that.

The biggest problem I personally have with that is this being a business kind of blog, a lot of our readers are working in offices and cannot access commenting windows other than Haloscan because of network filters and blocks. I am not here to debate the wisdom of employers in the financial, housing, and regulatory sectors keeping their employees from using our blog as a resource. Of course that's stupid. You try telling them that.

But it gets to a point where, if the comment threads get stupid and pointless and Yahooified enough, our employed readers will not want to read them, so there goes that problem. With a registration/moderation system, we could at least assure our loyal employed readers of having something worth reading at night and on the weekends when they have access from home.

I cannot make anyone stop responding to pointless or nuisance comments. You have to want to restrain yourself, because you understand that the only way to get rid of them is to fail to give them the attention they want. A "troll" is not just someone whose comments you disagree with, or even just a nasty or badly-worded comment. A troll is someone who does not, under any possible set of circumstances, care what you think about him or his comments. He merely wants attention. Negative attention will do. The more you disagree with him, the more he is able to tell himself that he is persecuted and victimized or the only voice of reason or one of the elite few who has the God's-eye view of the world or whatever his current delusion is. If he isn't merely a narcissist who thrives on feeling attacked, he's just some putz who enjoys irritating other people. Therefore, you "feed" the troll by paying any attention to him at all. It does not matter what you say in response. Any response to a troll just encourages the troll.

Besides classic trolls, we have a few resident long-winded bores who believe that the rest of us have never been exposed to some trite, shallow, bombastic rant they just heard on the radio or read in Reader's Digest or saw in a vision, and feel compelled to share with the rest of us. These people lack any possible sense of context or audience; they are incapable of noticing that the bulk of our commenting community has been exposed to the world for a while now and is not interested in any comment that starts "there is one simple answer to this the rest of you aren't getting." It does you no good to respond to this type either; they'll just re-write the same comment again, at the same length, saying the same thing, until you "get it." They are bores with no self-awareness. The cool thing about the internet is that you can just scroll down to the next comment without being "rude." So take advantage of the medium.

Absolutely none of this is to say or imply that you are not invited to debate with each other or to correct misstatements of fact. You are also still allowed to make jokes and ramble occasionally and even from time to time introduce a new topic that is relevant. Most of you are grownups who understand intuitively where the line is, and if you cross it now and again you catch yourself and go on mostly behaving yourself. A few of you are those problem children who are not capable of taking only one cookie or talking quietly in the library or waiting until it's your turn and you ruin all group experiences for everyone else. You goad the authorities into instituting draconian rules for everybody in order to prevent you from getting out of control. You are probably going to be like this for the rest of your life, since such behavior patterns that persist past puberty usually don't go away. All I can say to you is that you really will get nowhere asking me personally to validate your feelings or demands. If you worked for me, I would foist you off on another department or just fire you immediately. I learned a long time ago that I can't fix you and I can't function with you and you need me a whole hell of lot more than I need you. Of course you don't recognize yourself in this description. That'd be your big problem. I'm really just writing this to once again remind your fellows that I am not trying to inhibit anyone having a good time in the comments. I am trying to inhibit those of you with no judgment and no ability to control yourselves.

So you tell me, folks. Do we need to ditch Haloscan and go to controlled comments, or is the sane majority willing to help me keep the comment threads readable by starving the trolls?

First Bank Closure of 2008

by Calculated Risk on 1/26/2008 09:06:00 AM

From the FDIC: FDIC Approves the Assumption of all the Deposits of Douglass National Bank, Kansas City, Missouri

The Board of Directors of the Federal Deposit Insurance Corporation (FDIC) today approved the assumption of all the deposits of Douglass National Bank, Kansas City, Missouri, by Liberty Bank and Trust Company, New Orleans, Louisiana.This is a small bank, and by itself this closing is inconsequential. However this might become a trend, with a number of small FDIC-insured banks going under because of bad loans. I suspect the over-under line for bank failures this year has to be much higher this year than in 2007.

Douglass National, with $58.5 million in total assets and $53.8 million in total deposits as of October 22, 2007, was closed today by the Office of the Comptroller of the Currency, and the FDIC was named receiver.

... the FDIC estimates that the cost to its Deposit Insurance Fund is approximately $5.6 million. Douglass National is the first FDIC-insured bank to fail this year, and the first in Missouri since Superior National Bank, Kansas City, was closed on April 14, 1994. Last year, three FDIC-insured institutions failed.

Friday, January 25, 2008

Traders: Don't Put Jumbos in my TBAs

by Anonymous on 1/25/2008 06:06:00 PM

This probably wasn't what Congress had in mind, ya think?

NEW YORK (Reuters) - A key element of the stimulus package aimed at jump-starting the ailing U.S. housing market may have the unintended consequence of raising mortgage rates, said analysts studying the plan.TBA works the way it does precisely because "agency" loans are basically interchangeable: the normal variation just isn't wide enough to prevent traders from pricing deals before seeing the exact loan composition.

A federal proposal to increase the size limit on loans eligible for purchase by mortgage finance giants Fannie Mae and Freddie Mac has unsettled traders in the $4.5 trillion market for bonds backed by the "conforming" mortgages.

Increasing the eligible loans to $729,750 from $417,000 would change the characteristics of mortgage-backed securities, leading traders to exact a premium for increased interest-rate risk.

Borrowers with large, jumbo loans are more likely to refinance since their savings are greater for each incremental drop in rates than for a smaller loan. The loans will taint the bonds since traders don't initially know the make-up of the securities known as "agency" MBS.

Higher mortgage rates would make it even harder to unload already high housing inventories and existing homes on the market, delaying any housing recovery and potentially extending the U.S. economic slowdown.

Potential damage to the "to-be-delivered" (TBA) market -- the most actively traded agency mortgage market where investors can buy bonds before they are actually created -- prompted Wall Street dealers to call a special meeting with the Securities Industry and Financial Markets Association at 3:30 p.m. Friday, market sources said. A SIFMA spokeswoman would only say the group is in ongoing discussions with its members.

"The amount of money that investors are willing to pay for agency mortgages (bonds) could be lower if these loans are TBA deliverable and so mortgage spreads could widen," said Ajay Rajadhyaksha, co-head of U.S. fixed income strategy at Barclays Capital in New York, who will listen to the SIFMA meeting by phone.

Mortgage rates would rise for the "vast majority" of agency-eligible borrowers, he said.

When falling rates prompt refinancing of loans in mortgage bonds, investors can be hurt since principal may be returned to them at a price below market value. The investor is also faced with reinvesting principal in bonds paying lower rates.

MBS paying low interest rates have been hurt in recent days amid expectations the addition of many jumbo loans will boost supply in those coupons, analysts said. As much as $500 billion in jumbo loans could qualify, according to Barclays research.

Wall Street MBS traders last beat down SIFMA's door in October when the advent of the Federal Housing Administration's FHA Secure program threatened to taint TBA pools of Ginnie Mae securities. The dealers got their way -- Ginnie Mae created new "specified" pools outside of their TBA issues for FHA Secure.

"The street is on high alert," one mortgage trader at a New York-based primary dealer said in an e-mail.

Rajadhyaksha and other analysts, including RBS Greenwich Capital's Noah Estrin, expect the TBA market will be protected if Congress and President George W. Bush approve the stimulus plan as written.

"When you start throwing a lot of jumbos into a pool you spoil the fungibility of the collateral," said Linda Lowell, a mortgage market veteran and principal of Offstreet Research LLC. "That has made the market as liquid as it is. Home owners have benefited from lower mortgage rates."

Certainly this problem can be solved by putting the LFKAJ* in their own pools--as with FHASecure. That might keep this plan from driving up rates for everybody, but it's not clear to me how it improves the spread on those LFKAJ-only pools. Hmmm.

*Loans Formerly Known as Jumbo

FirstFed: Delinquencies Up Sharply

by Calculated Risk on 1/25/2008 04:31:00 PM

From Housing Wire: Option ARM Specialist FirstFed: Delinquencies Up 231 Percent in One Quarter

... FirstFed said that option ARMs hitting a forced recapitalization were “a contributing factor in the higher level of delinquent loans.”Hitting the maximum level of negative amortization doesn't necessarily mean the homeowners will be in trouble. But the fear is that many of these homeowners used Option ARMs as affordability products (they could only buy the home making the neg-am payment), and that they will be in unable to make the payment when they no longer have the neg-am option.

During the fourth quarter of 2007, just over 1,800 borrowers, with loan balances of approximately $830 million, reached their maximum level of negative amortization and had a resulting increase in their required payment. The bank said that it estimated that another 2,400 loans totaling approximately $1.1 billion could hit their maximum allowable negative amortization during 2008.

Barclays: Banks may need $143B in Capital if Insurers Downgraded

by Calculated Risk on 1/25/2008 02:54:00 PM

From MarketWatch: Banks may need $143 bln in fresh capital

If bond insurers are downgraded a lot, banks will need as much as $143 billion in fresh capital to absorb the impact, Barclays Capital estimated on Friday.The Barclays analyst believes that the "regulators and banks will be strongly incentivised to reach a workable solution" and avoid the downgrades.