RSS Feed

RSS Feed by Calculated Risk on 9/18/2007 08:29:00 PM

Tuesday, September 18, 2007

Gross, Rosenberg on the Fed and Rates

Update: From the Financial Times: Bank acts boldly to avert recession risk (hat tip Steve)

David Rosenberg, chief economist at Merrill Lynch, said it was hard to combat a deflating credit and asset bubble. He said that while markets soared when the Fed cut rates by 50 basis points in January 2001, they soon fell back.The S&P 500 closed at 1,276.05 on January 2nd, 2001. The Fed cut rates 50bps on Jan 3rd. The S&P 500 closed at 1,347.56, up 5.6% for the day. Then the market started to sell off, falling almost 20% by March. Rosenberg is correct (doesn't mean history will repeat).

Bloomberg video has several interviews concerning the Fed rate cuts. Here is PIMCO's Bill Gross:

| Gross of Pimco Sees 3.75% as `Destination' for Fed Rate September 18 (Bloomberg) -- Bill Gross, manager of the world's biggest bond fund at Pacific Investment Management Co., talks with Bloomberg's Michael McKee from Newport Beach, California, about today's decision by the Federal Reserve to lower its benchmark interest rate by a half point to 4.75 percent, the first cut by the central bank in four years. (Source: Bloomberg) |

Rate Cut Reactions

by Calculated Risk on 9/18/2007 04:26:00 PM

The reactions to the Fed funds rate cut are extremely varied - from relief to outrage. Here are a couple excerpts from the WSJ: Economists React: ‘One and Done’?

The FOMC makes it sound like “one and done” as it cuts both the Fed funds and discount rate by 50 basis points but continues to note inflation risks… As of this writing, we no longer look for the Fed to cut rates in October but that position, like the Fed’s, remains data dependent. –Drew Matus, Lehman BrothersAnd outrage:

Today’s irresponsible 50 basis point reduction is really just the hair of the dog that bit us and is a tacit admission that our economy is addicted to cheap money… A Fed bailout in the form of rate cuts will neither prevent the recession nor keep house prices from collapsing. It may slow the process down a few quarters, but it will cost us dearly. –Peter Schiff, Euro Pacific Capital

Fed Funds Rate Cut: Watch Long Rates

by Calculated Risk on 9/18/2007 02:49:00 PM

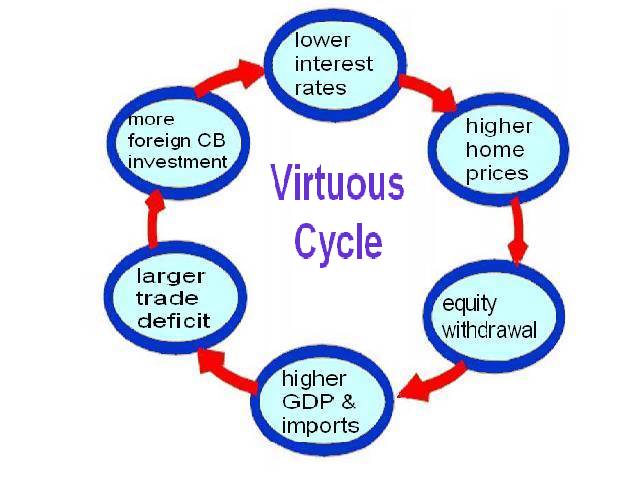

Virtuous cycle and vicious cycle:

In many parts of economics there is an assumption that a complex system of determinants will tend to lead to a state of equilibrium. When this tendency is absent terms like virtuous circle and vicious circle (or virtuous cycle and vicious cycle) to describe these unstable pattern of events are used. Both circles are complexes of events with no tendency towards equilibrium (at least in the short run). Both systems of events have feedback loops in which each iteration of the cycle reinforces the first (positive feedback). The difference between the two is that a virtuous cycle has favorable results and a vicious cycle has deleterious results. These cycles will continue in the direction of their momentum until an exogenous factor intervenes and stops the cycle.Perhaps, during the housing boom, a Virtuous Cycle was present as depicted in the following diagram:

Click on diagram for larger image.

Click on diagram for larger image.Starting from the top (during the housing boom): Lower interest rates led to an increase in housing prices. And those higher housing prices led to ever increasing mortgage equity withdrawal (MEW) by homeowners.

A large percentage of this equity withdrawal flowed to consumption, increasing both GDP and imports during the boom years. There is a strong correlation between the trade deficit and mortgage equity withdrawal, and although correlation doesn't imply causation, it appears mortgage equity withdrawal was a meaningful contributor to the widening trade and current account deficits during the housing boom.

To finance the current account deficit, foreign Central Banks (CBs) invested heavily in dollar denominated securities. Some analysts have suggested that these investments lowered interest rates by between 40 bps and 200 bps (Roubini and Setser: "Will the Bretton Woods 2 Regime Unravel Soon? The Risk of a Hard Landing in 2005-2006")

If these analysts are correct, and foreign CB intervention lowered treasury yields, then this also lowered mortgage interest rates ... and the cycle repeated. The result: a Virtuous Cycle with higher housing prices, more consumption and lower interest rates.

Now that the housing cycle has broken, what happens next?

The Vicious Cycle

The following diagram depicts the possible unwinding of the virtuous cycle.

As housing cools down (prices do not need to collapse), mortgage equity withdrawal declines. Then less MEW leads to a slow down in GDP growth and lower imports.

Lower imports might lead to a lower trade deficit, depending on the strength of exports. This could lead to less foreign CB investment in dollar denominated assets. And this could lead to higher interest rates followed by even lower housing prices and the cycle repeats.

The result: a Vicious Cycle with lower housing prices, less consumption leading to higher interest rates.

House prices are now falling. MEW is now falling. And the trade deficit is falling. And the LIBOR rate has increased.

An increase in long rates would be normal if the market expectations for the economy improve. What would be concerning is if long rates increased by more than normal because of the unwinding of investments by foreign CBs. This could lead - for the short term - to a vicious cycle as depicted in the second diagram.

Fed Cuts Rates 50bps

by Calculated Risk on 9/18/2007 02:15:00 PM

Fed Statement (FOMC site swamped, hat tip az_mtb):

The Federal Open Market Committee decided today to lower its target for the federal funds rate 50 basis points to 4-3/4 percent.

Economic growth was moderate during the first half of the year, but the tightening of credit conditions has the potential to intensify the housing correction and to restrain economic growth more generally. Today’s action is intended to help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and to promote moderate growth over time.

Readings on core inflation have improved modestly this year. However, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Developments in financial markets since the Committee’s last regular meeting have increased the uncertainty surrounding the economic outlook. The Committee will continue to assess the effects of these and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Timothy F. Geithner, Vice Chairman; Charles L. Evans; Thomas M. Hoenig; Donald L. Kohn; Randall S. Kroszner; Frederic S. Mishkin; William Poole; Eric Rosengren; and Kevin M. Warsh.

In a related action, the Board of Governors unanimously approved a 50-basis-point decrease in the discount rate to 5-1/4 percent. In taking this action, the Board approved the requests submitted by the Boards of Directors of the Federal Reserve Banks of Boston, New York, Cleveland, St. Louis, Minneapolis, Kansas City, and San Francisco.

NAHB: Builder Confidence Falls to Record Low in September

by Calculated Risk on 9/18/2007 01:00:00 PM

| Click on graph for larger image. The NAHB reports that builder confidence fell to 20 in September, from 22 in August. This ties the record low of 20 in January 1991. |  |

NAHB Press Release: Builder Confidence Continues Downward In September

Concerns about the substantial inventory of new homes for sale and the effects that deepening mortgage market problems are having on buyer demand caused builder confidence to decline for a seventh consecutive month in September, according to the latest National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today. The HMI dropped two points to 20, tying its record low reached in January of 1991 (the series began in January 1985).

...

Two out of three component indexes declined in September. The index gauging current single-family home sales declined two points to 20, while the index gauging sales expectations for the next six months fell five points to 26. The index gauging traffic of prospective buyers held steady at 16 for the month.

All four regions of the country reported declines in their September HMI readings. The Northeast posted a three-point decline to 26, while the Midwest posted a single-point decline to 13, the South posted a two-point decline to 22, and the West posted a four-point decline to 18.

The Hanging Out Revolution

by Anonymous on 9/18/2007 12:13:00 PM

We take a brief break from the failure to air the financial sector dirty laundry in order to report on one of my favorite bits of Total Insanity. Thanks, Yves, for the link. The WSJ reporteth:

BEND, Ore. -- It was a sunny, 70-degree day here in Awbrey Butte, an exclusive neighborhood of big, modern houses surrounded by native pines.In the 70s, we burnt our bras to teach you pigs a lesson. Thirty years later, we're hanging them out right in front of you! It's Laundry Liberation Front in the burbs. Out of the way, Stepford Wives! And take your "property values" with you when you go!

To Susan Taylor, it was a perfect time to hang her laundry out to dry. The 55-year-old mother and part-time nurse strung a clothesline to a tree in her backyard, pinned up some freshly washed flannel sheets -- and, with that, became a renegade.

The regulations of the subdivision in which Ms. Taylor lives effectively prohibit outdoor clotheslines. In a move that has torn apart this otherwise tranquil community, the development's managers have threatened legal action. To the developer and many residents, clotheslines evoke the urban blight they sought to avoid by settling in the Oregon mountains.

"This bombards the senses," interior designer Joan Grundeman says of her neighbor's clothesline. "It can't possibly increase property values and make people think this is a nice neighborhood." . . .

Brooks Resources repeated its threat of legal action, and then advised Ms. Taylor to "develop a plan to screen your outdoor laundry and submit the plan to the ARC for review." It also suggested the possibility of formal proceedings to get the rules amended, which would require 51% of homeowners' support in writing.

The following month, Ms. Taylor constructed a fabric screen to conceal her clothesline. The committee, which included Brooks Resources Chairman Michael P. Hollern, gave it a thumbs down. "It doesn't blend with the home or the native surroundings," says Ms. Haworth.

Mr. Hollern says, "Personally, I think people probably ought to screen their laundry from other people's view. If you feel differently, you should probably be living somewhere else."

Many neighbors agree. When Ms. Grundeman first noticed the Taylor clothesline, she assumed it was temporary. "My first thought was, 'Oh gosh, her dryer must have broken,' " says the interior designer.

Foreclosure Activity Increases in August

by Calculated Risk on 9/18/2007 11:05:00 AM

"A greater percentage of homes entering foreclosure are going back to the banks."From MarketWatch: Foreclosures more than double in past year

James Saccacio, chief executive for RealtyTrac

Nearly a quarter of a million foreclosure filings were reported in August, up 115% from a year ago and up 36% from July. Each home in foreclosure can have multiple filings as it moves from default status to bank repossession....See MarketWatch story for audio of full interview with a RealtyTrac executive.

"The jump in foreclosure filings this month might be the beginning of the next wave of increased foreclosure activity, as a large number of subprime adjustable-rate loans are beginning to reset," said James Saccacio, chief executive for RealtyTrac.

Quote of the Day

by Anonymous on 9/18/2007 09:47:00 AM

Thanks to Clyde, we see that Morgan Keegan is having a wee bit of a problem filing a report. Oh, Mommy, will those subprime bonds ever stop being so hard to price?

This, however, is classic:

The lack of liquidity in the fund's securities could result in the fund incurring greater losses on the sale of some its securities than under more stable market conditions, Morgan Keegan said in the supplement filing.How true. Back when the market was "stable" enough to let us all lever up twenty times, this kind of thing didn't happen.

LEND 10-Q: A Heapin' Helpin' of HorseHockey™

by Anonymous on 9/18/2007 09:25:00 AM

LEND finally got around to filing a 10-Q today for Q01. It's jam-packed with exciting self-serving revisionist history masquerading as opening the kimono. I recommend it to connoisseurs of first-rate HorseHockey™.

Lowlights:

In the third quarter of 2006, the non-prime mortgage market in which the Company operates was characterized by increased competition for loans and customers which simultaneously lowered profit margins on loans and caused lenders to be more aggressive in making loans to relatively less qualified customers. By the end of 2006, the non-prime mortgage industry was clearly being negatively impacted. The sustained pricing competition and higher risk portfolios of loans reduced the appetite for loans among whole loan buyers, who offered increasingly lower prices for loans, thereby shrinking profit margins for non-prime lenders. In addition, the higher levels of credit risk taken on by non-prime lenders resulted in higher rates of delinquency in the loans held for investment and in increasing frequency of early payment defaults and repurchase demands on loans that had been sold. These trends accelerated during the first quarter of 2007, and the industry experienced a period of turmoil which has continued into the second and third quarters of 2007. As of August 31 2007, more than 55 mortgage companies operating in the non-prime mortgage industry had failed and many others faced serious operating and financial challenges. The most notable of these failures is New Century Mortgage Corporation (“New Century”), one of the largest non-prime originators in recent years, which filed for bankruptcy protection in April 2007.Yeah, the funny business just happened to happen in Q04 06, which made it visible in Q01 07, which just happens to be the point at which LEND suddenly discovered that it could no longer prepare financial statements. Funny how that works.

It now appears that an underlying reason for the deterioration of industry conditions was the relatively poor performance of loans originated in 2006 in comparison to loans originated in 2004 and 2005. While real estate markets were booming during 2004 and 2005, and some areas experienced significant home price appreciation, many originators extended credit and underwriting standards to meet market demands. When home price appreciation leveled off, or in some areas declined, many of the loans originated in 2006 did not perform up to expectations. This decline in performance led to increases in the cost of securitizing non-prime loans as the rating agencies which rate non-prime securitizations increased loss coverage levels, requiring higher credit support for non-prime securitizations.

At minimum, may we remind everyone that the 2005 subprime mortgage vintage was on track to become the Worst Ever until . . . you know . . . we had data on 2006?

Roll Us Over, LEH Us Down

by Anonymous on 9/18/2007 08:18:00 AM

Daytraders and global stuffees bail out real estate specuvestors! Or something. (Hat tip Turbo, who observes that the TEOTWAWKI has been postponed another quarter):

Sept. 18 (Bloomberg) -- Lehman Brothers Holdings Inc., the largest U.S. underwriter of mortgage-backed bonds, said profit fell less than expected as fees from equities trading and investment banking offset some losses from subprime home loans.

Net income fell 3 percent to $887 million, or $1.54 a share, in the third quarter from $916 million, or $1.57, a year earlier, the New York-based company said today in a statement. The average estimate of 16 analysts surveyed by Bloomberg was $1.48 a share.

Chief Executive Officer Richard Fuld's efforts to reduce the reliance on fixed income by expanding stock trading and merger advice solidified earnings as contagion in the credit markets spread, led by defaults among home-loan borrowers with poor credit histories. Lehman is cutting about 2,000 mortgage-related jobs. Revenue from equities jumped 64 percent to $1.37 billion.