RSS Feed

RSS Feed by Anonymous on 4/13/2007 07:10:00 AM

Friday, April 13, 2007

Foreclosure Moratorium: See "Details, Devil In"

From the Philadelphia Business Journal, we get "N.J. legislator wants freeze on subprime-related foreclosures":

I realize that a subject involving local politics and homeowners does, in the wonderful world of journalism, demand that no useful questions be asked prior to publication, but on the off chance that some reporter out there cares to follow up on this scoop . . . could you ask next time whether this is also a moratorium on charging interest on delinquent loans? Does it require the lender to keep the asset in accrual status--even though normal accounting rules would suggest otherwise--because the collectability of the loan is now a matter of politics? If the moratorium expires without new magical escape routes being invented, and the delinquent borrower now owes six months worth of additional interest on the debt, effectively wiping out whatever tiny slice of equity that borrower might have had, will the taxpayers of New Jersey happily pay that? Will the lender eat it? The mortgage insurer? The HELOC holder? Or will the borrower just be screwed later rather than sooner? At least one inquiring mind would like to know.A New Jersey lawmaker called upon the state's attorney general on Wednesday to impose a moratorium on subprime mortgage loan foreclosures, to give the state time to investigate and address problems.

The moratorium, requested by Assembly Deputy Speaker Neil M. Cohen in a letter to Attorney General Stuart Rabner, would bar subprime lending firms from initiating new foreclosures, pursuing pending foreclosures and evicting homeowners for up to six months.

I'd also kind of like to know what the state of New Jersey (or anyone else, frankly) thinks it can figure out in six months that hasn't become painfully obvious by now, but let's consider that an extra-credit question.

Thursday, April 12, 2007

DataQuick on Bay Area, CA: Home prices up, Sales Still Slow

by Calculated Risk on 4/12/2007 05:53:00 PM

From DataQuick: Bay Area home prices up, sales still slow

The median price paid for a Bay Area home moved up in March, regaining much of the decline since last summer even as sales remained at the lowest level in 11 years, a real estate information service reported.Different month, same story. Falling demand and rising supply will probably start impacting the median price soon.

The median price paid for a home in the nine-county Bay Area was $639,000 last month ... up 2.1 percent from $626,000 for March last year, according to DataQuick Information Systems.

...

A total of 8,317 new and resale houses and condos were sold in the Bay Area last month. That was ... down 19.6 percent from 10,343 for March last year.

DataQuick on SoCal: Slow sales, Record Median Price

by Calculated Risk on 4/12/2007 04:43:00 PM

From DataQuick: Slow sales, record median for Southland homes

Southern California's housing market continued to send contradicting messages in March. Sales remained at a ten-year low while the median sales price increased to a new peak. The rise in median is in part due to a drop-off in sales of entry-level homes, a real estate information service reported.

A total of 21,856 new and resale homes sold in Los Angeles, Riverside, San Diego, Ventura, San Bernardino and Orange counties last month. That was up 23.6 percent from 17,680 for the month before, and down 32.4 percent from 32,320 for March last year, according to DataQuick Information Systems.

Last month's sales were the lowest for any March since 1997 when 20,024 homes were sold. ...

The median price paid for a Southland home was $505,000 in March, a new record and the first time it was above $500,000.

Heebner: "Biggest housing-price decline since the Great Depression"

by Calculated Risk on 4/12/2007 04:25:00 PM

From Bloomberg: Heebner Says Home Prices May Fall 20% Amid Bad Loans (hat tip Brian)

Kenneth Heebner, manager of the top-performing real-estate fund over the past decade, said U.S. home prices may plunge as much as 20 percent because of rising defaults on riskier mortgages.

...

``It will be the biggest housing-price decline since the Great Depression,'' Heebner, 66, said today in an interview in Boston. Prices may fall by a fifth in some markets, he said.

That would leave home prices at levels last seen in 2003 and 2004 ... The damage from high-risk mortgages will slow the U.S. economy, though not enough to send it into a recession ...

Weekly Unemployment Claims

by Calculated Risk on 4/12/2007 01:00:00 PM

From the Department of Labor:

In the week ending April 7, the advance figure for seasonally adjusted initial claims was 342,000, an increase of 19,000 from the previous week's revised figure of 323,000. The 4-week moving average was 323,250, an increase of 7,000 from the previous week's revised average of 316,250.

Click on graph for larger image.

Click on graph for larger image.Here is a different way of looking at the weekly claims data. This graph lines up the last two recessions (1990 and 2001) at week zero, and looks at the 4-week moving average for 2 years before the recession and 3 quarters after the recession starts (gray area is recession).

For the current period, I assumed a recession starts in July 2007 - just to compare to the previous periods. The rise in weekly claims due to hurricane Katrina is very evident.

Although there are historical periods when weekly claims didn't provide any advance warning of a recession, in general claims do start creeping up before the onset of an economic recession. So far weekly claims are not suggesting an imminent (with the next month or two) recession.

Fannie Mae on 2007 ARM Resets

by Anonymous on 4/12/2007 12:39:00 PM

Fannie Mae's newest Economic and Mortgage Market Developments report (thanks, Lurker!) has some interesting charts on projected ARM resets for 2007.

First, which ARMs are we talking about? Subprime and Alt-A appear to be the clear winners on volume.

Second, how have borrowers in recent vintages responded to imminent rate resets? By refinancing, of course.

Finally, how eligible for refinance are those subprime loans that will reset this year? I suggest that we carefully ponder this third chart.

Finally, how eligible for refinance are those subprime loans that will reset this year? I suggest that we carefully ponder this third chart.

If you are like me, you might be wondering how that big chunk of loans with a FICO over 700 and a CLTV of 80% or less found its way into a subprime security.

Washington Post: Bailout Update

by Anonymous on 4/12/2007 09:46:00 AM

As is all too typical, the Post serves up a nice issue salad today on foreclosures, loss mitigation, and bailouts. It takes a fair amount of effort to untoss the thing and figure out what information you might want that you didn't get. The title of the piece, "$1 Billion Pledged to Help Fend Off Foreclosures," appears to refer to existing commitments by banks--Citi and Bank of America--to Neighborhood Assistance Corporation of America. The funds were originally earmarked for low-to-moderate income borrower purchase loans, but have been reallocated to refinancing troubled mortgages currently held by subprime lenders. This issue is happily tossed with potential federal bailout legislation in the works:

If the "proposal" being "applauded" here by NACA is that any rescue funds should be administered by community-based nonprofits like NACA with a track record of decent performance on its own purchase-money mortgages, then I'd have to agree it's probably a wise idea, even if I'm not ready to start clapping. If this is going to be another one of those "faith-based initiatives," I consider that we've already been fleeced enough there.Sen. Charles E. Schumer (D-N.Y.), the committee's chairman, plans to propose legislation that would provide "hundreds of millions of dollars, maybe more," in federal money to help borrowers avoid foreclosure by refinancing mortgages they cannot afford.

That money should reach borrowers primarily through community nonprofit groups that are already helping homeowners refinance burdensome mortgages, Schumer said. But he has not worked out the details of whether banks and other groups would be conduits for the aid or where the money would come from. Schumer has said it might come from a federal appropriation or perhaps the Federal Housing Administration or mortgage financiers Fannie Mae and Freddie Mac.NACA, the housing advocacy group, applauded the proposal, saying it has a better track record of keeping people in their homes than subprime lenders, whom it characterized as predators that mislead borrowers into taking on loans they cannot repay. NACA requires that people who ask for its help attend intensive housing counseling workshops. It also assesses the person's ability to own and maintain a home. It then helps the person obtain a mortgage with one of its partner lending institutions, the biggest ones being CitiGroup and Bank of America. In 2003, Citigroup made available $3 billion in mortgage loans to NACA through 2013. Bank of America, which has worked with NACA since 1995, committed at least $6 billion through 2015.

The group traditionally found the money was best used to finance new home loans for low- and moderate-income buyers. But with the mortgage crisis unfolding, it decided that $1 billion should be used to refinance the loans of people preyed upon by abusive lenders. The group expects to refinance about 7,000 mortgages -- a small number, given estimates that more than 1 million homeowners nationwide could be at risk of foreclosure.

The rest of this proposal is, of course, another story. It's not that I object to Citi or BoA committing loan dollars here, but there's something about them being "conduits" for such funds that does things to my eyebrows. Taxpayers, beware of "conduits."

But of course, the question of what Citi or BoA is actually committing to fund here is left unanswered. Here are the questions I have (hint, reporters, hint):

- Are the 7,000 or so loans NACA wants to work out with a subsidized refinance originally purchase loans? In other words, is the current unaffordable mortgage a result of "ownership society" push to make home purchase money funds available to subprime buyers, or is this an effect of homeowners using the subprime lending market to extract equity?

- The above item might matter if we addressed the question of who, actually, holds the loans being refinanced. Aside from the question of which homeowners are being bailed out, we have the question of which lenders are being bailed out by having a nonperforming loan taken off their books. Are we clear that Citi and BoA are not holders of the existing notes?

- If NACA is using these funds to refinance loans that were originally made at predatory terms--predatory lending being not the same thing as subprime lending, necessarily--what is the provision for penalizing the originator or holder of the current loan? Is Citi or BoA paying "the fine" here for illegal lending practices, by providing the funds to refinance the loans?

- Is there really no money at all left to be wrung out of the subprime lenders, such that we're now ready to talk about the taxpayers stepping in? How could that be?

- Is Schumer's "hundreds of millions or more" a question of capital to make refinance loans with? A subsidy on the interest rate of such loans? A cash transfer to the original lender in the form of debt forgiveness on the loan being refinanced? Additional credit enhancement (i.e., a subsidy of insurance premiums) to make the refinanced loans investment quality? An additional guarantee to the refinancing lender? Is there, in other words, any potential return to the taxpayers? Do I get a lien? Am I now a bondholder? Or am I, the taxpayer, just covering the losses?

Wednesday, April 11, 2007

Moody's: Commercial-Mortgage Risk Forcing Change

by Calculated Risk on 4/11/2007 05:17:00 PM

From Bloomberg: Commercial-Mortgage Risk Forcing Change, Moody's Says (hat tip Brian)

Moody's Investors Service ... will require more protection for investors in securities backed by mortgages on apartment buildings, offices and other commercial properties because of "a continued slide" in lending standards.Clearly the incipient credit crunch has moved beyond subprime.

emphasis added

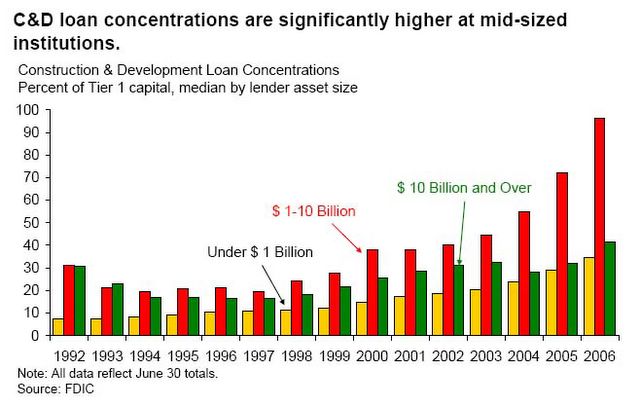

From this previous post: Commercial Bank Exposure to Real Estate: We know, from the FDIC Semiannual Report that the concentration of CRE and C&D loans has increased:

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loanThe housing crisis is now front page news, but there is little discussion about U.S. bank exposure to CRE loans. If a CRE slump follows the residential real estate bust (the typical historical pattern), then the mid-sized institutions might have a serious problem.

concentrations, especially at institutions with total assets between $1 billion and $10 billion.

The Impact of MEW on PCE

by Calculated Risk on 4/11/2007 01:51:00 PM

Barry Ritholtz of The Big Picture and Don Luskin are debating the economic outlook at the USNews.com.

Round 1 is here: The Bullish versus Bearish Economic View

Round 2 can be found here: Don’t Worry–Be Happy vs Worry a Lot–Housing Will Hurt the Economy

Note: I no longer use the second chart presented by Barry - it is correct, but it is easy to misinterpret. See my notes here to apparently get even more confused!

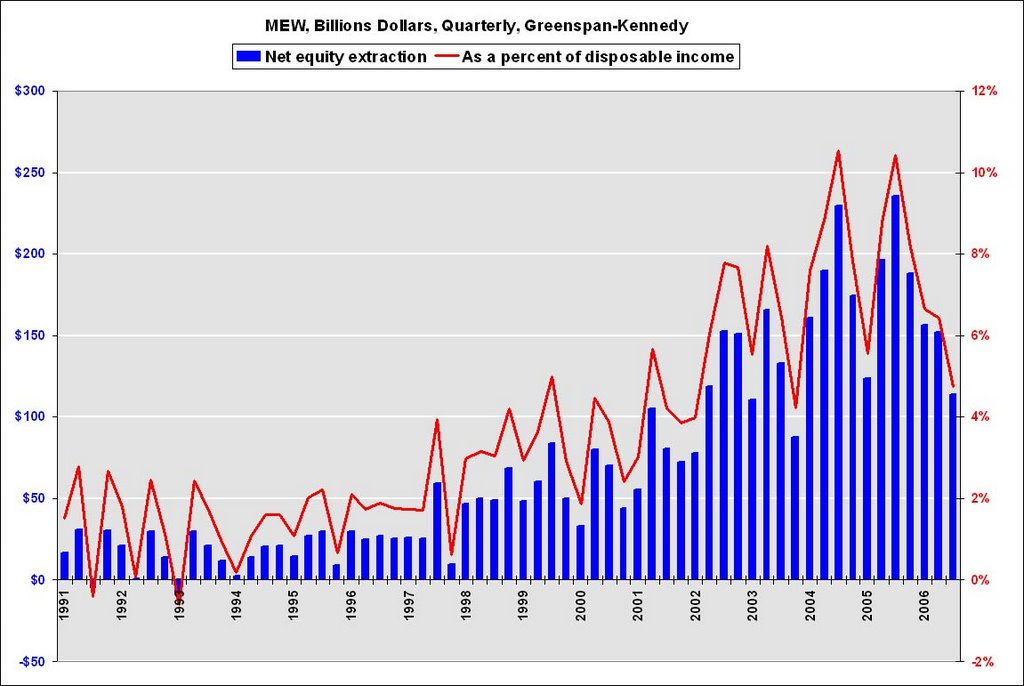

I'd usually stay out of this debate, but since both Barry (with credit - thank you!) and Don (without crediting me) are using my graph, I thought I'd offer some comments. Click on graph for larger image.

Click on graph for larger image.

This graph shows the Greenspan-Kennedy MEW (Mortgage Equity Withdrawal) calculations (through Q3 2006), both in billions of dollars quarterly (not annual rate), and as a percent of personal disposable income. Note: Q4 2006 has not been released by the Fed yet.

Mr. Luskin took my chart and added the Year-over-year change in PCE and suggests there is no correlation. Here is a better comparison. This is of the trailing four quarters of MEW as a percent of PCE vs. the annual change in nominal PCE.

Here is a better comparison. This is of the trailing four quarters of MEW as a percent of PCE vs. the annual change in nominal PCE.

Some observers might think this chart is sort of a Rorschach inkblot test. They would suggest observers see what they want to see.

In fact the correlation is low over this period, around 0.07. But that is the point that Barry is making. In the earlier periods, MEW wasn't important for PCE growth, but in recent years MEW probably was a very important component of PCE.

I think most economists agree that declining MEW in 2007 will negatively impact consumption. The current debate is on the size of the impact. Greenspan has argued that about 50% of MEW flows to consumption. This may be too high or too low - the percentage is difficult to estimate because other factors also impact consumption.

Round 3 should be available shortly.

WSJ: Realtors Predict Annual Price Drop

by Calculated Risk on 4/11/2007 10:59:00 AM

From the WSJ: Realtors Predict Annual Price Drop, Lower Forecasts for Home Sales

A real-estate trade group lowered its forecasts for U.S. home sales this year, while projecting what would be the first annual decline in the median national existing home price since it began keeping records in the late 1960s.My projections are for existing home sales to fall to 5.6 to 5.8 million units and prices to fall from 1% to 3% nationwide (as measured by OFHEO).

In its latest forecast for the real-estate market, the National Association of Realtors projected that existing home sales will fall 2.2% this year to 6.34 million, compared with its previous forecast of a 0.9% decline. The NAR said new home sales are likely to fall 14.2% to 904,000, compared with the prior forecast of a 10.4% drop.

...

The national median existing home price will likely slip 0.7% to $220,300 in 2007, following a 1% gain last year ...