RSS Feed

RSS Feed by Calculated Risk on 5/11/2006 04:07:00 PM

Thursday, May 11, 2006

Shiller: Real Estate could lead World into Recession

From the GlobeandMail.com: Shiller sees U.S. rally cutting out, Feels housing slowdown could be trigger

Stock markets are still expensive, and investors could be in for an unpleasant surprise once corporate profits begin to weaken, says the Yale University economist who predicted the crash of 2000-2002.

...

Mr. Shiller said the Standard & Poor's 500-stock index is still valued at about 27 times earnings -- far below the bubble-era peak of 46 but still well above the long-term average of about 15. Those numbers are based not on last year's earnings but on a 10-year average of profits.

"I think we could have a number of disappointing years," the economist said in an interview yesterday with The Globe and Mail. "We see earnings growing rapidly, but I feel skeptical about [the sustainability of] that."

...

The trigger for a profit slowdown, he suggests, could be a fall in consumer confidence and U.S. housing prices, the signs of which are beginning to appear in places such as San Francisco, Boston and Miami. Mr. Shiller updated Irrational Exuberance last year and devoted a large chunk of it to his view of speculative bubbles in real estate.

"It looks like we're at the peak" in U.S. housing, he said. "But I can't claim victory yet.

"The equity bust of 2000 produced a mild recession, and was rather short-lived. It's very hard to predict . . . [but] if the real estate market does tank, it will cause a worldwide recession." Falling real estate values "will probably be spread over many countries."

Wednesday, May 10, 2006

Fannie CEO Frets about ARMs

by Calculated Risk on 5/10/2006 05:08:00 PM

From Reuters: Fannie CEO frets about adjustable mortgages

Fannie Mae's chief executive said on Wednesday the U.S. housing market will face significant resetting of adjustable rate mortgages over the next two years and he worries about this sparking foreclosures in some locations.

...

"If jobs are pretty stable, if home prices have come up underneath the mortgages to support them and if there's not any incidence of appraisal fraud, it could be just fine," [Daniel Mudd, president and chief executive officer] said. "If in certain geographies, some of those factors are different -- there's some appraisal fraud, or there's an economic downturn or home prices have declined -- it could be a very different scenario.

"In that case, what you'd worry about, really on a neighborhood-by-neighborhood basis, is you have a foreclosure here and you have a foreclosure there and soon you've got four foreclosures on the market and you've got plywood on the windows and that could have a very deleterious effect," on the market, Mudd said.

REAL Fed Funds Rate

by Calculated Risk on 5/10/2006 03:24:00 PM

UPDATE: Professor Thoma parses the FOMC statement: The FOMC Raises Target Rate to 5%

Using the Dallas Fed's trimmed-mean PCE inflation rate (6 month average, annualized) and the effective nominal Fed Funds rate, the Real Fed Funds Rate is now around 2.5% (assuming current inflation at the same level as March).

Click on graph for larger image.

This graphs shows the REAL Fed Funds rate for the last 20 years. The median is 2.9%; still higher than the current rate. Of course inflation could dip with all the rate hikes already in the pipeline and the REAL rate would increase even if the FED pauses.

But right now inflation, using the trimmed-mean PCE method, is still too high. The FED is probably comfortable with measured inflation in the 1% to 2% range.

The wildcard remains the housing market. If housing slows too quickly (see previous post with 20% drop in the MBA Purchase Index from last year) then the economy might slow quicker than expected and the FED will have overshot.

If inflation remains at this level, or continues to increase, then the FED will have to continue hiking rates.

The June meeting should be interesting.

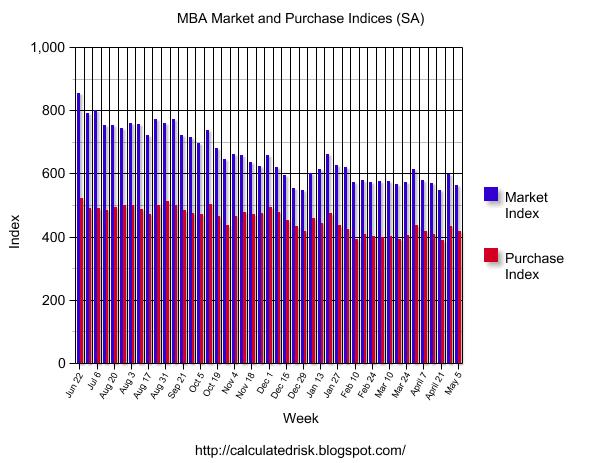

MBA: Mortgage Application Volume Down

by Calculated Risk on 5/10/2006 10:01:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Down

Click on graph for larger image.

The Market Composite Index, a measure of mortgage loan application volume, was 562.1, a decrease of 5.8 percent on a seasonally adjusted basis from 596.8 one week earlier. On an unadjusted basis, the Index decreased 5.2 percent compared with the previous week and was down 27.1 percent compared with the same week one year earlier.Mortgage rates were mixed:

The seasonally-adjusted Purchase Index decreased by 3.9 percent to 416.5 from 433.3 the previous week whereas the Refinance Index decreased by 8.8 percent to 1427.4 from 1565.6 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages increased to 6.61 percent from 6.57 percent ...Change in mortgage applications from one year ago (from Dow Jones):

The average contract interest rate for one-year ARMs decreased to 6.04 percent from 6.08 percent ...

| Total | -27.1% |

| Purchase | -20.7% |

| Refi | -36.9% |

| Fixed-Rate | -19.4% |

| ARM | -41.0% |

Purchase activity is off 20.7% from the comparable week last year.

Tuesday, May 09, 2006

California Real Estate Agent Boom Continues

by Calculated Risk on 5/09/2006 10:06:00 PM

Housing may be slowing, but ...

Click on graph for larger image.

This graph shows the number of licensed Brokers and salespeople in California for each March.

The California Department of Real Estate reports the total number of agents in California is now 490,861, up 0.9% from last month, and up 10% from last March. The number of licensed salespeople has risen 80% since March 2000. The number of Brokers has increased almost 26%.

... the pace of new licensees has not slowed.

The GOP sends me an Email

by Calculated Risk on 5/09/2006 08:31:00 PM

I've made an effort to limit the number of political posts on this blog. This will be an exception ...

As an introduction, I'm a lifelong Republican and former youth delegate to the RNC (when I was in college). The GOP sent me an email today and I've posted excerpts on Angry Bear: The GOP Talking Point.

I'm ready for a change.

Now back to economics ...

Citigroup Remains Bullish

by Calculated Risk on 5/09/2006 02:15:00 PM

I've just read the Citigroup May 9th Consumer Update. To say Citigroup remains bullish on the US economy (and homebuilders too) is an understatement.

I must be missing the fun with the "recreational debt creation", but lets check a few numbers. Real residential construction grew 5.8% over the last year, from $584.1 Billion in Q1 2005 (annualized) to $618.2 Billion in Q1 2006 (in 2000 dollars). GDP grew 3.5% over the same period ($10.999 Trillion to $11,381.40 Trillion in 2000 dollars).

If residential construction had been flat, GDP would have been around 3.1%. So Citigroup's number is technically correct (less than 0.5 percentage points of GDP growth came from growth in residential construction), but that is still a substantial contribution to GDP growth.

And what if residential construction falls 10% this year (a common estimate)? All else being equal that would put real GDP growth at around 2.6%. And that is excluding any impact from the loss of the "wealth effect" and the loss of housing related employment.

It is true that personal interest income has been rising almost as fast as mortgage interest payments. The general idea is simple: as strapped homeowners reduce their personal consumption expenditures, other consumers will take up the slack with their additional interest income.

However, it seems likely that consumers receiving substantial interest income tend to save more - and as interest rates rise, the savings rate will increase - so its not a one for one substitution for consumption. Besides, the primary concern for housing is the marginal homeowner with an ARM. As rates rise, these homeowners might be forced to sell, increasing the supply of houses for sale and eventually putting pressure on prices - and reversing the wealth effect.

There is much more in the Citigroup report, but suffice to say Citigroup didn't convince me. I remain concerned about the impact of the housing slowdown on the general economy.

Monday, May 08, 2006

FOMC Rate Hike Odds

by Calculated Risk on 5/08/2006 10:48:00 PM

Every week Dr. Altig calculates the market expectations of future federal funds rate hikes based on the options on federal funds futures. This weeks post is especially interesting. Expectations are for another 25 bps this Wednesday and then for a pause, at least through the August meeting.

Click on graph for larger image.

This graph shows the daily odds of various Fed Funds rates after the August 8th meeting.

An extended pause is somewhat surprising since most of the recent economic data has been fairly positive. Even the data for the housing market hasn't been terrible - and the housing slowdown hasn't impacted employment significantly yet.

Inflation also appears to be moving higher - as an example the Dallas Fed's trimmed mean PCE inflation rate was an annualized 3.7% in March and 2.4% over the last 6 months - above the high end of the Fed's informal target of 2.0%.

For the FED to pause, they must expect housing will weaken further in the near future. There were a couple of commentaries today suggesting that the housing slowdown is spreading: see Dimartino: Bubble's bursting on all fronts and Housing slowdown appears to be spreading nationwide. Further evidence of a housing slowdown was provided after market hours by Dominion Homes, when they reported a Q1 loss:

Douglas Borror, chief executive officer of the company, said, "Based on the level of sales we are currently experiencing, we do not expect that 2006 will be a profitable year."I think there might be another rate hike in June unless inflationary pressures ease.

Harper's: The New Road to Serfdom

by Calculated Risk on 5/08/2006 11:39:00 AM

Here is the cover from this month's Harper's Magazine:

THE NEW ROAD TO SERFDOM

An Illustrated Guide to the Coming Real Estate Collapse

UPDATE: Professor Thoma posted a cartoon from the China Daily last week that is very similar to the Harper's Magazine cover.

Saturday, May 06, 2006

Buffett: Real estate slowdown ahead

by Calculated Risk on 5/06/2006 09:19:00 PM

CNNMoney reports: Buffett: Real estate slowdown ahead

On the real estate bubble

Buffett: "What we see in our residential brokerage business [HomeServices of America, the nation's second-largest realtor] is a slowdown everyplace, most dramatically in the formerly hottest markets. ... The day traders of the Internet moved into trading condos, and that kind a speculation can produce a market that can move in a big way. You can get real discontinuities. We've had a real bubble to some degree. I would be surprised if there aren't some significant downward adjustments, especially in the higher end of the housing market."

On mortgage financing

Munger: "There is a lot of ridiculous credit being extended in the U.S. housing sector."

Buffett: "Dumb lending always has its consequences. It's like a disease that doesn't manifest itself for a few weeks, like an epidemic that doesn't show up until it's too late to stop it Any developer will build anything he can borrow against. If you look at the 10Ks that are getting filed [by banks] and compare them just against last year's 10Ks, and look at their balances of 'interest accrued but not paid,' you'll see some very interesting statistics [implying that many homeowners are no longer able to service their current debt]."

{kind=link}