RSS Feed

RSS Feed by Calculated Risk on 9/27/2005 11:08:00 PM

Tuesday, September 27, 2005

Jobs: Georgia On My Mind

Georgia has an unemployment problem. The Atlantic Journal Constitution reported on a job fair today:

By noon Tuesday, signs of a troubled Georgia job market swollen with storm evacuees were unmistakable inside the massive Georgia World Congress Center.

At a job fair designed to help victims of Hurricane Katrina, organizers had to block the doors to newcomers after the event reached its limit of 15,000 job-seekers. It was still three hours before registration was expected to end.

The crowd was so big at the United Way Job Fair Tuesday that the 180,000 square feet at the Georgia World Congress Center couldn't hold everyone, so some job seekers were turned away. The limit was 15,000, and most of those, say employers and job seekers, were from Georgia.

Yet the majority of those who made it inside the center, and those who were stuck outside, were not storm evacuees. They were Georgia's jobless — a telling indicator of the state's serious problem with unemployment.

"A Category 5 economic storm is brewing in Georgia, and that's not hyperbole," said Michael Thurmond, commissioner of the Georgia Department of Labor. "The job fair today presents additional evidence as to how difficult the job market is in this state."

Click on graph for larger image.

The job picture is concerning in Georgia. The unemployment rate is rising and has reached the highest level since the recession of the early '90s.

Part of the problem is that Georgia's housing market has underperformed during the housing boom. According to the OFHEO House Price Index, Georgia's housing has only appreciated 12.4% since the end of 2002. This compares to the national average of 26.1%.

So Georgia probably hasn't seen the same housing related employment boom as much of the nation. This is a chicken and the egg problem. Housing might be weak because of relatively weak employment; employment might be weak because of relatively weak housing.

Perhaps partly because of the weak labor market, and as buyers stretch to afford a home, Georgia leads the nation in IO mortgages:

Georgia has become the national leader in an increasingly popular but controversial type of mortgage that lets borrowers postpone payments on the loan principal for years.So it isn't surprising that with a relatively weak labor market, a high concentration of creative loans and minimal house price appreciation:

More than half of mortgages last year in Georgia were interest-only, compared with fewer than one-third nationwide ...

"Georgia ranked fourth in the nation in the number of properties in foreclosure".But what comes first? Weak employment or weak housing? And as the housing market slows, will Georgia's problem become a national problem?

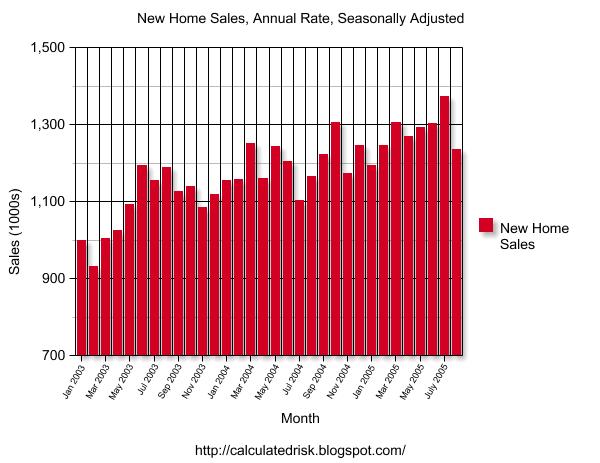

August New Home Sales: 1.237 Million

by Calculated Risk on 9/27/2005 01:49:00 AM

According to a Census Bureau report, New Home Sales in August were at a seasonally adjusted annual rate of 1.237 million vs. market expectations of 1.345 million. July sales were revised down to 1.373 million from 1.41 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in August 2005 were at a seasonally adjusted annual rate of 1,237,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

The Not Seasonally Adjusted monthly rate was 106,000 New Homes sold, down from a revised 118,000 in July.

The median sales price of new houses sold in August 2005 was $220,300; the average sales price was $283,400.

Both the average and median sales price rebounded.

The seasonally adjusted estimate of new houses for sale at the end of August was 479,000. This represents a supply of 4.7 months at the current sales rate.

The seasonally adjusted supply of New Homes was 4.7 months, a significant increase from recent months.

With the usually caveat that one month does not make a trend, this report shows a significant downturn in the New Home Sales market. Sales were off. Inventories were up. Revisions were negative.

This may be the beginning of the end for this housing cycle.

Monday, September 26, 2005

WSJ: Greenspan Warns of Reliance on Housing Loans

by Calculated Risk on 9/26/2005 09:51:00 PM

Greg Ip writes at the WSJ:

]"Federal Reserve Chairman Alan Greenspan, drawing on new research he has personally supervised, said American consumers have become enormously dependent on borrowing against their homes to fuel their spending, and that a rise in mortgage rates could trigger a spending pullback.

Mr. Greenspan's new data show that borrowing against home values added a stunning $600 billion to consumers' spending power last year, equivalent to 7% of personal disposable income -- compared with 3% in 2000 and 1% in 1994.

...

That reversal need not be "disruptive," Mr. Greenspan said. Indeed, he suggested that such a reversal would bring about a needed rise in U.S. saving and a narrower trade deficit. But he also sounded new warnings about speculation in the housing market, focusing on rising sales of second homes, though also playing down the threat of overleveraged homebuyers.

Mr. Greenspan's remarks were among his most extensive to date on the scope and risks of the rise in housing prices and mortgage debt in the past decade, developments to which his own policies have contributed. The remarks suggest that while in the near term higher energy prices may be the greatest threat to consumers, in the longer term Mr. Greenspan sees a cooling housing market as potentially more significant.

Last year's estimate of the value of "home equity extraction," as Mr. Greenspan calls it, was double the value of President Bush's tax cuts, as estimated by Brookings Institution scholar Peter Orszag. It's unclear how much of that home-financed borrowing was spent on goods and services, but Mr. Greenspan suggested it was about half.

...

Mr. Greenspan also repeated his warnings on the increased popularity of some exotic mortgages, which expose the borrower to a greater risk of rising rates or declining home prices.

...

Mr. Greenspan believes this home-equity extraction has been a powerful channel of support to the economy in recent years. Indeed, he believes it's how the Fed's low interest rates propped up the economy after the stock bubble burst in 2001. While the Fed has raised short-term interest rates since last summer, long-term mortgage rates, which are set by bond investors, have stayed surprisingly low. Thus, home-equity extraction has fueled consumer spending longer than Mr. Greenspan thought likely ...

Greenspan on Housing

by Calculated Risk on 9/26/2005 04:26:00 PM

Bloomberg reports: Greenspan Says Speculation Having 'Greater Role' in Home Prices

Sales of vacation houses, or homes that aren't always occupied by owners, are "arguably at historically unprecedented levels," Greenspan said in the text of his remarks to the American Bankers Association annual convention in Palm Desert, California. "This suggests that speculative activity may have had a greater role in generating the recent price increases than it customarily has had in the past."MarketWatch adds: Greenspan weighs in on home prices, Drops may not be fatal, even as housing fuels spending

A new study, co-authored by Greenspan, has found that about four-fifths of the rise in home-mortgage debt has been due to homeowners taking some cash out of the rise in their property's value.Here is the Greenspan study (PDF): Estimates of Home Mortgage Originations, Repayments, and Debt on One-to-Four-Family Residences

"It is difficult to dismiss the conclusion that a significant amount of consumption is driven by capital gains on some combination of both stocks and residences," Greenspan said.

As a result, consumer spending would decline if mortgage rates rise and home turnover and opportunities for mortgage refinancing cash-outs decline, he added.

There also would be some positive developments, as the personal savings rate would likely rise, and the trade deficit would narrow given the likely drop in imports of consumer goods.

"How significant and disruptive such adjustments turn out to be is an open question," Greenspan said.

A few comments: 80% of the increase in mortgage debt "has been due to homeowners taking some cash out". That is a huge amount. If cash refis were cut in half for the last year, GDP would have been flat and if there were no cash out refis, GDP would have declined 3.1%. (Update: assuming cash out goes to consumption) And that is just the direct impact and does not include any secondary effects of layoffs in the housing and retail industries.

I do agree with Greenspan's comment: it is difficult to predict how disruptive the coming adjustment will be, but a recession is likely.

Existing Homes: Sales Strong, Inventories Rise

by Calculated Risk on 9/26/2005 10:44:00 AM

CBS reports: Existing Home Sales Hit 2nd Highest Level

The National Association of Realtors reported Monday that sales of existing homes rose 2 percent in August to a seasonally adjusted annual rate of 7.29 million units, a sales pace that was exceeded only by an all-time high of 7.35 million units in June.Inventories increased from 2,759,000 in July to 2,856,000 in August. This is about what I expected. Existing Home Sales are a trailing indicator and are mostly sales in June and July. Tomorrow's New Home Sales is more interesting and might show the first signs of a slowing housing market.

...

The strong demand pushed prices up to a record level of $220,000 last month, a gain of 15.8 percent from August 2004. That was the biggest 12-month increase since a 17.2 percent increase in July 1979.

...

While the Realtors predicted that Hurricane Katrina, which came ashore in New Orleans in late August, would impact sales in September, they said the impact in August appeared to be minimal.

This and that ...

by Calculated Risk on 9/26/2005 12:03:00 AM

My most recent post is up on Angry Bear: Housing: Buy or Rent?

The inherent problem with the buy vs. rent calculation is estimating the future value of the house. As long as prices are going to continue to appreciate, it doesn't matter what you pay for the house. But when appreciation stops; price matters!

A couple of posts I recommend:

Dr. Duy's Fed Watch: Dejá Not A great series on trying to read the FED's mind.

"I continue to think that Greenspan & Co. are sending increasingly not-so-subtle messages that the days of low interest rates and easy policy are at their end. This is a message for Congress and the Administration, not just the financial markets. Indeed, something unexpected may be happening – a concerted effort to end any sense of a Greenspan-put in the markets or the economy as a whole. It will undoubtedly be interesting to watch this chapter in Fed history play out."Responding to supply shocks Dr. Hamilton cautions about future FED Funds increases, at least until the full impact of Katrina can be assessed.

UPDATE: Two more on the FED:

Macroblog: Funds Rate Probabilities: Keep On Truckin' *AT Least One More Time)

And Dr. Polley asks some questions: Differing opinions on the Fed

I'll throw out these questions to the blogosphere: What are the dangers of a pause in the rate hikes? What are the chances that the market would misinterpret it and see it as a signal that the Fed is done raising rates or that they see recession on the horizon? If you were on the FOMC, what would you do between now and the end of the year to minimize that risk? Do you think that these risks would cause the Fed not to want to pause at all, but treat "measured pace" as meaning 25 b.p. per meeting until they feel they're at the neutral funds rate? Would that be good policy?Best to all.

Saturday, September 24, 2005

Rita: Oil Refinery Impact

by Calculated Risk on 9/24/2005 02:31:00 PM

UPDATE: Status added to some refineries (see list).

The AP reports: Feds Optimistic That Houston Refineries OK

Federal officials were "cautiously optimistic" Saturday that one of the largest concentrations of Texas refineries near Houston escaped serious damage as Hurricane Rita veered farther to the east.As mentioned in the article, the biggest concern is for the refineries in the Port Arthur-Beaumont and Lake Charles areas. These include:

But the Energy Department said it was too soon to assess the impact of the storm on a cluster of refineries in the Port Arthur-Beaumont area that caught the direct impact of the hurricane as it came ashore.

Based on computer modeling and initial reports, department spokesman Craig Stevens said, "We're cautiously optimistic about (the Houston) ... region" and "that the petroleum supply will be OK."

"But we really need to look at the Port Arthur region and other areas directly impacted. ... It may still be two or three days before we get a sense of the actual picture," he said.

| CRUDE OIL | |||

| THROUGHPUT | |||

| COMPANY | LOCATION | CAPACITY (B/D) | STATUS |

| FAR EASTERN TEXAS | 1,013,500 (Total) | ||

| ExxonMobil | Beaumont, Tex. | 348,500 | |

| Valero | Port Arthur, Tex. | 250,000 | 4 feet water, 2 to 4 weeks |

| Motiva | Port Arthur, Tex. | 235,000 | flooded with 4-5 feet water, no date |

| Total | Port Arthur, Tex. | 180,000 | |

| WESTERN LOUISIANA | 593,300 (Total) | ||

| Citgo | Lake Charles, La. | 324,300 | minor damage reported |

| ConocoPhillips | Westlake, La. | 239,000 | |

| Calcasieu | Lake Charles, La. | 30,000 |

Four refineries remain shut down from Katrina: three in New Orleans and the Chevron refinery in Pascagolua, Mississsippi.

Four refineries (ChevronTexaco, located in Pascagoula, MS; ConocoPhillips, located in Belle Chasse, LA; ExxonMobil, located in Chalmette, LA; and Murphy Oil, located in Meraux, LA) remain shut down, and expectations are that these refineries, which represent about 5 percent of total U.S. refining capacity, could be shut down for an extended period.For production, the Minerals Mining Service reports that 100% of GOM oil production is shut-in:

Today’s shut-in oil production is 1,500,898 BOPD. This shut-in oil production is equivalent to 100% of the daily oil production in the GOM, which is currently approximately 1.5 million BOPD.The immediate concern is the loss of refining capacity. For the short term, the loss of oil production is not critical (see Dr. Hamilton's Economic effects of Rita)

Today’s shut-in gas production is 7.488 BCFPD. This shut-in gas production is equivalent to 74.88% of the daily gas production in the GOM, which is currently approximately 10 BCFPD.

Friday, September 23, 2005

NYTimes: Is It Better to Buy or Rent?

by Calculated Risk on 9/23/2005 07:44:00 PM

The NYTimes has an article comparing buying and renting in New York and San Francisco: Is It Better to Buy or Rent?

"... renting might deserve another look right now. After five years in which rents have barely budged while house prices in New York, Washington, Los Angeles and elsewhere have doubled, renting has become a surprisingly smart option for many people who never would have considered it before.Check the graphics on the left of the article. The New York house, selling for

...

Add it all up - which The New York Times did, in an analysis of the major costs and benefits of owning and renting, including tax breaks - and owning a home today is more expensive than renting in much of the Northeast, Florida and California. Only if prices rise well above their already lofty levels will home ownership turn out to be the good deal that it is widely assumed to be."

The analysis was very generous to buyers. They assume the homebuyers receive the entire benefit of the interest and property tax deduction. The article correctly points out this may not be true:

"Don't be buying a house because you think you're saving on the taxes," said Frank Borges LLosa, owner of FranklyRealty.com, a brokerage in Arlington, Va. "You'll save even more by not buying and renting."The article also points out some of the extra benefits of ownership, like stability and being able to choose the "color of their living room walls", but there advantages to renting too - like being able to move easier.

Mr. LLosa added: "I'm not saying not to buy. I'm saying don't buy just for the tax reasons."

Many homeowners also do not receive the full deductions from home ownership. In the Northeast and California, homeowners now have so many deductions that some must pay the alternative minimum tax. This tax effectively wipes out part of their property-tax deduction, further cutting into the benefits of home ownership.

Other homeowners do not itemize their deductions or, if they do so, end up with total deductions only a little larger than the standard deduction that the government offers to all taxpayers, even renters.

"A lot of people hugely overvalue the mortgage deduction," said Dean Baker, co-director of the Center for Economic and Policy Research, a liberal group in Washington, "because they compare it to no deduction instead of comparing it to the standard deduction."

If I was moving to a new bubble area, I would definitely rent.

Housing: Mortgage Applications Still Steady

by Calculated Risk on 9/23/2005 01:00:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Applications Steady During Holiday Shortened Week

The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending September 16. The Market Composite Index — a measure of mortgage loan application volume – was 772.2, an increase of 1.5 percent on a seasonally adjusted basis from 760.6 one week earlier. On an unadjusted basis, the Index increased 11.9 percent compared with the previous week and was up 12.0 percent compared with the same week one year earlier.What I found puzzling is that refinance activity is still strong, even though rates have been flat or rising for some time:

The refinance share of mortgage activity increased to 45.6 percent of total applications from 42.9 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 29.8 percent of total applications from 28.2 percent the previous week.It appears homeowners are still pulling equity out of their houses. Also, given the narrow spread between products, I'm surprised at the volume of ARMs.

Thursday, September 22, 2005

UK Chief Scientist: This IS Global Warming

by Calculated Risk on 9/22/2005 10:59:00 PM

The Independent reports: This IS global warming, says environmental chief

Super-powerful hurricanes now hitting the United States are the "smoking gun" of global warming, one of Britain's leading scientists believes.There is no question that warmer waters lead to more intense hurricanes. From NOAA: Global Warming and Hurricanes

The growing violence of storms such as Katrina, which wrecked New Orleans, and Rita, now threatening Texas, is very probably caused by climate change, said Sir John Lawton, chairman of the Royal Commission on Environmental Pollution. Hurricanes were getting more intense, just as computer models predicted they would, because of the rising temperature of the sea, he said. "The increased intensity of these kinds of extreme storms is very likely to be due to global warming."

"...we cannot say at present whether more or fewer hurricane will occur in the future with global warming, the hurricanes that do occur near the end of the 21st century are expected to be stronger and have significantly more intense rainfall than under present day climate conditions."And there is no question that waters are getting warmer; a fact that is not in dispute. The only question has been if man is contributing to the warming trend. And the overwhelming scientific evidence is that man's activities are a major factor in the warming trend. From the American Association of the Advancement of Science annual meeting: Scientists on AAAS Panel Warn That Ocean Warming Is Having Dramatic Impact

Strong new evidence shows that ocean temperatures are rising because of human activity, and the impact on people and ecosystems worldwide could be severe, scientists on a AAAS panel warned Thursday.The FT also quoted the AAAS report: "‘Global warming real’ say new studies"

The evidence-based on computer models and observations in the field-is so strong that it should put to an end any debate about whether human-caused global warming is a real phenomenon, said Tim Barnett, a research marine physicist in the Climate Research Division at Scripps Institution of Oceanography at the University of California-San Diego.

"The temperature-driven impact that these models predict over the next 30-40 years is severe, not only for the Western United States, but for China and Peru," Barnett said.

"Other parts of the world will face similar problems," he added in an unpublished paper released to reporters. The climate models "suggest that these scenarios have a high enough probability of actually happening that they need to be taken seriously by decision makers...if it is not already too late."

They found that the "warming signals" in the oceans could only have been produced by the build-up of man-made carbon dioxide in the atmosphere. Non-human factors would have produced quite different effects.And on the "debate", Sir John Lawton commented:

Tim Barnett, the Scripps project leader, said previous attempts to show that human activities caused global warming had looked for evidence in the atmosphere. "But the atmosphere is the worst place to look for a global warming signal," he said. "Ninety per cent of the energy from global warming has gone into the oceans and the oceans show its fingerprint much better than the atmosphere."

"There are a group of people in various parts of the world ... who simply don't want to accept human activities can change climate and are changing the climate."The scientific debate is over. It is time for action.

"I'd liken them to the people who denied that smoking causes lung cancer."