RSS Feed

RSS Feed by Calculated Risk on 8/16/2005 02:41:00 PM

Tuesday, August 16, 2005

Housing, Housing, Housing

For those that need more housing stories, I recommend the following sites:

UPDATE: Also REOWire Stories and commentary. "insight for the default servicing industry"

Patrick's Housing Crash Blog (story links)

Housebubble.com (story links)

Ben Jones' The Housing Bubble 2 (Commentary)

Prof. Pigginton's Econo-Almanac Based in San Diego.

And writing of San Diego, here are two articles on San Diego housing:

As housing slowdown takes hold in San Diego, experts differ on depth

Home inventory soars as buyers take their time

Housing: Record Prices, Growing Caution

by Calculated Risk on 8/16/2005 12:20:00 AM

Amid stories of record home prices are signs of caution. Like these comments:

"Up until two weeks ago, the overwhelming number of professional articles and opinions rendered was that there is no housing bubble. Now more and more people are starting to refute the evidence that there isn't a bubble," DeSalvo [commercial broker with Premier Properties] said. "That is not to say that the market is going to crash but that it is going to slow down."And from National Association of Realtors spokesman Walter Molony:

"The immediate danger in that is with rising interest rates, mortgage rates are going to pick up and it is going to create a different kind of real estate environment," he said. "Those that got the adjustable mortgages and the interest-only mortgages will be the first ones to tumble when that happens."

DeSalvo said another danger is that people getting high-risk loans now are going to try to sell as soon as the market starts to level off to get their money out.

"Everybody was doing it in the stock market, now everyone is doing it in real estate," DeSalvo said. "If they are lucky they will get away with their skin."

Perhaps the most interesting aspect of the current market is the high amount of residential speculation, he said. People are getting equity lines on their existing homes because of the appreciation and investing it in another house or property.And from Economy.com's Analyst Gus Faucher:

"The immediate danger in that is with rising interest rates, mortgage rates are going to pick up and it is going to create a different kind of real estate environment," he said. "Those that got the adjustable mortgages and the interest-only mortgages will be the first ones to tumble when that happens."

Real estate has traditionally been a long-term investment market and it should remain that way, Molony said. Instead, real estate has become the new stock market — the place for everyone to look to make a quick buck, even if that means taking out a high-risk loan, he said.

"That is very risky behavior. You cannot count on an abnormal market indefinitely," Molony said. "People are getting excited about buying homes in a hot market and there are loan officers out there who do not have a historical perspective and have never experienced a market with increasing rates and declining rates."

"We're worried about a bubble in the housing market," said Economy.com's Faucher. But he does not envision the sort of splat that flattened stocks after the dotcom collapse.And finally from Edward Edward Leamer of UCLA's Anderson Forecast:

"We expect that (increases in) house prices could slow or even turn negative on the coasts because those have seen the biggest run," he said.

He thinks that correction is coming and that it will be a doozy. "The situation gets worse and worse," he said, referring to "the elevation of prices beyond their fundamental values."

Leamer said eight of the last 10 housing corrections since World War II have precipitated recessions, the two exceptions being in the early 1950s and early 1960s, when spending on wars in Korea and Vietnam sustained growth.

Monday, August 15, 2005

Port of Long Beach: July Import Traffic Off Slightly

by Calculated Risk on 8/15/2005 09:53:00 PM

Import traffic at the Port of Long Beach fell 2% compared to June, just below the highs of last fall's heavy shipping season. The Port of Los Angeles will report in the next couple of days.

For Long Beach, the number of loaded inbound containers for July was 289 thousand, down 2% from June and up 2.7% from July 2004. Outbound traffic was up 4% at 107 thousand containers rebounding to the levels of May.

The quantity of containers says nothing about the content value, but provides a rough guide on imports from China and the rest of Asia. With these numbers, I expect imports from China to be off slightly for July, and exports to China to be up.

NOTE: The OffPeak initiative (adds late night hours to port operations) started on July 23rd to handle the expected heavier late summer / fall imports.

FED Senior VP: Fed May Need to Raise Rates to Stop `Bubbles'

by Calculated Risk on 8/15/2005 06:01:00 PM

Earlier I posted excerpts from an economic letter by the Federal Reserve's Glenn D. Rudebusch, Senior Vice President and Associate Director of Research: Monetary Policy and Asset Price Bubbles.

Dr. Thoma directs us to some additional comments by Rudebusch. Also see Professor Thoma's related comments on interest rates and balancing the economy: The Insurance Value of Increasing the Federal Funds Rate.

No more Free Money? OC Home Prices Dip

by Calculated Risk on 8/15/2005 04:28:00 PM

Back in March I wrote (in jest) that they were giving away free money in The OC (Orange County, CA). At that time the median home price in OC was $555,000.

Over the next few months median home prices rose to $603K. That was a total of $48K in FREE MONEY (not really free of course) since local RE Broker Gary Watts' prediction of $70,000 in gains this year for the median home.

Now the OC Register is reporting a slight dip in home prices to $601,000 for July. Still $46K in 6 months is well on its way to Mr. Watts' $70K annual appreciation prediction.

Fleckenstein: Top in Place for Housing Market

by Calculated Risk on 8/15/2005 12:42:00 PM

Bill Fleckenstein writes the Contrarian Chronicles for MSN Money. This week he touches on housing:

'To get a feeling for the budding inventory problem in many previously hot markets, let's look at a less-hot market (via the following vignette from a reader of this column): A publicly held home-building company (which shall remain nameless) in Columbus, Ohio, has been buying back homes from financially distressed owners and reselling them, at reduced prices, only to folks who are approved for conventional mortgages. As the reader says: "The inventory of homes is growing -- including one cul-de-sac where a staggering 13 of 20 homes, all less than three years old, are already up for sale."'And on subprime mortgages:

'... a contact in the subprime-lending arena (lenders who specialize in making loans to borrowers with less-than-stellar credit records) suggests to me that it's becoming increasingly difficult for originators of subprime mortgages to sell them at a profit. Unless all of these are booked on the originator's own balance sheet, we'll start to see credit being cut off to the more marginal real-estate speculators -- the driving force, at the margin, behind the real-estate market.'Fleck concludes:

'...the macro winds have shifted, I believe, and none of those shifts has occurred in a way that is bullish for U.S. assets. Bottom line: It's my opinion that a top is being formed (or is already in place), both in the housing market and the stock market. That spells trouble for an economy built on the unsustainable strategy of trying to speculate our way to prosperity.'Fleck has been very bearish for a number of years. He was early (but correct) on the NASDAQ. And he has also been early on housing.

The housing market was very strong in the 2nd quarter. However it does appear that inventories are building and, as Fleck suggests, a top may be close.

CNN: Home prices post record gains

by Calculated Risk on 8/15/2005 12:38:00 PM

CNN reports:

Single-home price growth over the 12 months ending June 30 was the strongest in history, according to the National Association of Realtors.See the article for a list of the top 10 markets. Durham, North Carolina is #9?

In its quarterly survey, NAR found that U.S. home prices rose at an annual rate of 13.6 percent, to a median price of $208,300.

Of the 149 metro areas surveyed, 67 showed gains of more than 10 percent.

David Lereah, NAR's chief economist, called the increases unprecedented. "When you look at appreciation of home prices relative to the overall rate of inflation, these are the strongest increases on record," he said.

Oil, Trade and Housing

by Calculated Risk on 8/15/2005 12:49:00 AM

My most recent post is up on Angry Bear: Oil Prices Revisited.

It looks like oil imports will add about $1.2 Billion to the July trade deficit.

It is possible that higher oil prices are leading to lower interest rates! As Dr. Setser noted:

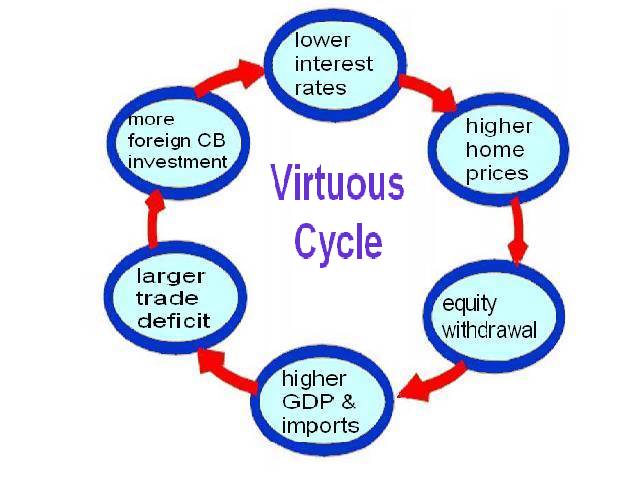

"High oil prices = oil windfall = global savings glut = low long-term rates ... and the low-long term rates help even as high oil prices hurt."And finally, back in March, I speculated that there was a relationship between housing and the trade deficit. In fact, it was possible that a virtuous cycle had developed that might become vicious when housing slows down.

UPDATE: Here are the graphics from the Virtuous-Vicious post.

Click on diagram for larger image.

The following diagram depicts the possible unwinding of the current cycle.

Check out the post for a discussion of how this could work (and some numbers).

It all ties together (hopefully). I'm focused mostly on housing because I think housing is the linchpin for the US economy.

Best to all.

Sunday, August 14, 2005

The "Rising tide of abandoned residential properties"

by Calculated Risk on 8/14/2005 12:17:00 AM

Real estate investors are just walking away from residential property and lenders are getting stuck. Some lenders do not want to take title to the worthless property and the city has started a campaign called the "shaming sign" - placing signs on abandoned property with the names of the lenders' executives. This has induced some lenders to take title and either fix up or demolish the abandoned homes.

This is a story from the Great Depression ... except it is happening right now in Dayton, Ohio.

... others have fallen victim to a conspiracy of carelessness and greed by lenders and their clients, many of them investors. When loans go bad, both duck for cover, their abandoned properties becoming a cancer on neighborhoods.With lax lending restrictions it is no surprise that areas with little or no appreciation are seeing rising foreclosures. I wonder if the "investors" were able to borrow against the home before just walking away from the loan.

This reality has led to a new strategy — the "shaming sign." Those who cut out on neighborhoods are held up to richly deserved embarrassment.

A major bank recently took charge of one of its neglected foreclosure properties; a bank official didn't like seeing his name on a sign.

Another big bank has been bobbing and weaving to avoid responsibility. Unable to sell a foreclosed property, it won't take title itself. Instead, it filed suit against its customer, leaving the property to languish and the city holding the bag.

Another property, though, on Helena Street could have a happy ending. A representative for the owner says the owner will tear the building down and deed the property to an adjacent community garden.

That action hasn't happened yet, but should it comes to pass, it will demonstrate the power and potential of the city's attack on abandoned properties.

Saturday, August 13, 2005

Trade Deficit Projection: June Review

by Calculated Risk on 8/13/2005 10:11:00 PM

Three months ago I started to build a simple model to project the trade deficit. I didn't make as much progress as I had hoped, but the first two components (oil and China) performed reasonably well for two months... but I underestimated China for June.

Here are my projections for June. My model projected a deficit of $17.0 Billion Seasonally Adjusted in energy related petroleum product imports. The actual number was $17.77 Billion (see Exhibit 9). This is an error of 4.3%.

For the trade balance with China, my model projected a deficit of $16.3B NSA (SA is not available). The actual number (see Exhibit 14) was $17.6B or an error of 7.3%.

Here are each of the components and how the model performed:

| ITEM | Projection | Actual | Error |

| US Exports to China (NSA) | $3.2B | $3.4 | 6% |

| US Imports from China (NSA) | $19.5B | $20.99B | 7% |

| US Trade Deficit: China (NSA) | $16.3B | $17.6B | 7% |

| Oil: Imports SA | $19.3B | $19.9B | 3% |

| Oil: Exports SA | $2.3B | $2.14B | 7% |

| OIL Balance SA | $17.0B | $17.77B | 4% |

Some internal data:

| ITEM | Projection | Actual | Error |

| Oil: Contract Price BBL | $45.11 | $44.40 | 1.6% |

| Oil: BBLs Crude | 328.0 | 328.3M | 0% |

| Oil: Price Other BBL | $51.88 | $51.58 | <1% |

| Oil: BBLs Other | 90M | 103.7M | 13% |

| Oil: Oil Imports NSA | $19.5B | $19.9B | 2% |

I really missed on China. I wondered about the surge in imports at LA and attributed them to Japan (imports in Japan were up $1.26B). Overall, my guess of $57.7B was on the high end of estimates, and I still underestimated the deficit for June!