RSS Feed

RSS Feed by Calculated Risk on 2/01/2021 10:38:00 AM

Monday, February 01, 2021

Construction Spending Increased 1.0% in December; 4.7% Annual Increase

From the Census Bureau reported that overall construction spending increased:

Construction spending during December 2020 was estimated at a seasonally adjusted annual rate of $1,490.4 billion, 1.0 percent above the revised November estimate of $1,475.6 billion. The December figure is 5.7 percent above the December 2019 estimate of $1,410.3 billion.Both private and public spending increased:

The value of construction in 2020 was $1,429.7 billion, 4.7 percent above the $1,365.1 billion spent in 2019.

emphasis added

Spending on private construction was at a seasonally adjusted annual rate of $1,137.6 billion, 1.2 percent above the revised November estimate of $1,124.4 billion. ...

In December, the estimated seasonally adjusted annual rate of public construction spending was $352.8 billion, 0.5 percent above the revised November estimate of $351.1 billion.

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Residential spending is 2% above the bubble peak (in nominal terms - not adjusted for inflation).

Non-residential spending is 8% above the previous peak in January 2008 (nominal dollars), but has been weak recently.

Public construction spending is 8% above the previous peak in March 2009, and 35% above the austerity low in February 2014.

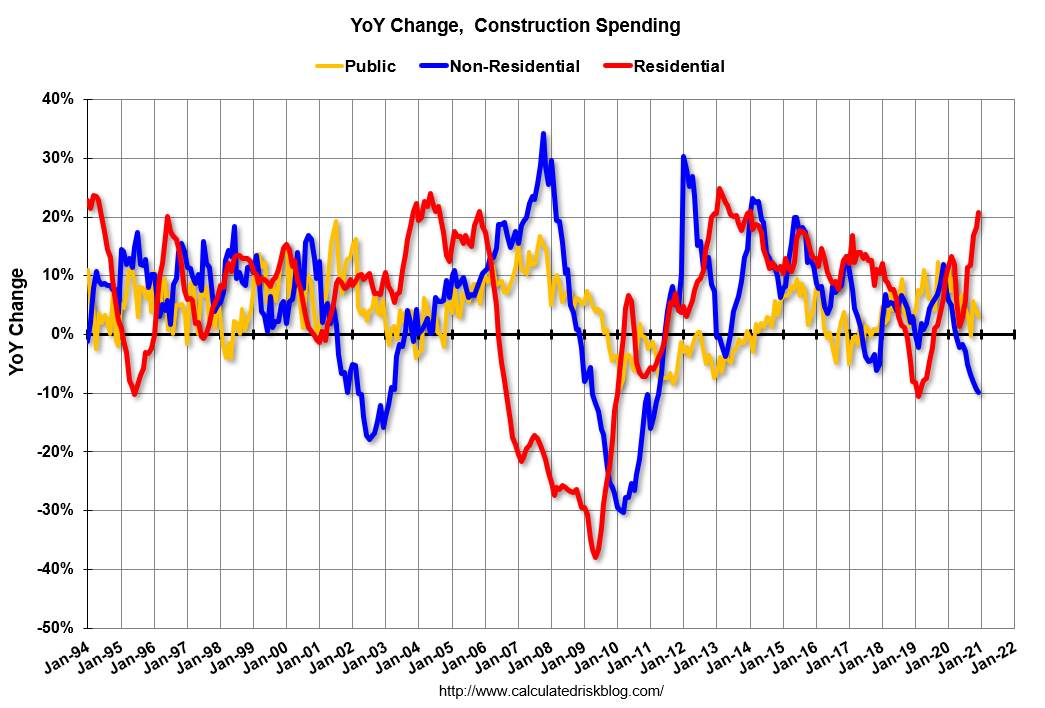

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is up 20.7%. Non-residential spending is down 9.8% year-over-year. Public spending is up 3.0% year-over-year.

Construction was considered an essential service in most areas and did not decline sharply like many other sectors, but it seems likely that non-residential, and public spending (depending on disaster relief), will be under pressure. For example, lodging is down 25% YoY, multi-retail down 21% YoY, and office down 3% YoY.

This was slightly above consensus expectations of a 0.9% increase in spending, and construction spending for the previous two months was revised up. A strong report.