RSS Feed

RSS Feed by Calculated Risk on 8/31/2005 06:12:00 PM

Wednesday, August 31, 2005

Recession Coming?

Even before the devastation of hurricane Katrina, the US economy was apparently headed for a significant slowdown and possible recession. According to a survey of CFOs completed on August 28th (before Katrina): Housing, Fuel Are Top CFO Concerns

In the four years of the survey, this is the first time that CFOs with growing pessimism outnumbered CFOs with growing optimism. Indeed, the level of optimism is down sharply from last quarter's 40 percent and is strikingly lower than last year's 72 percent.Emphasis added. And the most recent numbers have not looked good:

"This is the greatest increase in pessimism that we have seen," says Don Durfee, research editor of CFO magazine. "We’ve found that this optimism index predicts future economic growth quite well. In a situation like this, where the growth in pessimism outweighs the growth in optimism, we expect to see a slowdown in economic growth."

Macroblog: Not The Most Bullish Day For Economic News

The Big Picture: PMI, GDP stink up the joint

And here is how Briefing.com described the Chicago PMI report (with chart):

- An unbelievable plunge to 49.2 in August Chicago PMI index (-14.3 pts).

Key Factors - Record sized plunge leaves index in a contractionary sub 50 level -- the first since April '03 after reaching a 17 yr high in March.

- New orders (30% weight) plunged an astounding 23 points to 46.5 -- presumably off the highs in oil prices.

- Production fell to 56.2 from a nose bleed 70.5 in July as it followed orders.

- Employment fell in line to 51.7, March stood at a high 66.

- Prices paid rose to just 62.9 and doesn't reflect the pricing fear we are assuming caused the orders plunge.

So Katrina impacted an already fragile US economy. Dr. Hamilton notes this while discussing the energy related economic impact of Katrina: Day 2:

... this event did not arrive out of the blue. Instead, it came in an environment in which there was already considerable anxiety about gas prices and sound basis for worrying about a possible recession even if Katrina had done no harm.And Kash makes a similar observation - "I’ve been a bit worried about which way animal spirits were heading in the US" before Katrina struck - he writes on Katrina and Psychology over on Angry Bear:

Could this be enough to tip the whole economic cart over? I'm not certain that it will. But it would seem foolish to deny the very real possibility that it could.

Now add Katrina. ... I think that the current situation contains the seeds for such a shift in sentiment. My personal odds for a recession in 2006 have just gone up, thanks to Katrina.UPDATE: Dr. Polley adds: Katrina and the probability of recession

"I am reluctant to speculate too much too soon about a recession. It's just too early. But all in all, the economics corner of the blogosphere has been (as evidenced by the links here) very reasoned in its assessment of the situation. My take is closest to Hamilton's. It would indeed be foolish to underestimate the possibility that this could be the straw that breaks the camel's back.OTOH, the Ten Year bond has rallied and the yield has dropped from 4.4% to just under 4.1% over the last few weeks. This will probably lead to lower mortgage rates and could possibly boost equity extraction and support the housing market. Tomorrow the OFHEO House Price Index will be released and I believe it will show stunning widespread gains in house prices and that might help with confidence. But I think the housing boom is almost over, even with slightly lower mortgage rates.

...

Of course, that doesn't mean a recession is inevitable. ... I think it is safe to say, however, that this is a very critical moment for the economy. It could swing either way. If we pass this hurdle, I think it bodes well for the future of the recovery."

Flooding as seen from Space

by Calculated Risk on 8/31/2005 03:37:00 PM

After and before photos of the New Orleans area:

Click on photo from larger image.

August 30, 2005.

Photo from NASA Earth Observatory.

August 27, 2005.

Relief and General Information

by Calculated Risk on 8/31/2005 10:44:00 AM

From The Big Picture: Katrina/New Orleans Disaster Relief Aid

From Movie Guy in comments: Many information links (scroll down - 3 different posts)

Bartlett: Housing Balloon or Bubble?

by Calculated Risk on 8/31/2005 01:11:00 AM

Bruce Barlett writes in the Washington Times:

Over the weekend, Federal Reserve Chairman Alan Greenspan warned housing boom speculators should be very careful. What goes up fast can come down just as fast.Bartlett then reviews many of the riskier loans available these days. He concludes:

A key underpinning of the housing price surge is the lenders' belief risks have fallen. They therefore became more willing to lend on terms they would not have extended in the past. This made available mortgages to previously unqualified borrowers and bigger mortgages to those with good credit.

Though he is no alarmist, Mr. Greenspan warned Friday that if lenders should perceive greater risk, rates could rise and borrowing qualifications tighten quickly. "Newly abundant liquidity can readily disappear," he noted.I suggest reading the entire commentary.

Access to mortgages will become much more limited, people will have less money to pay for housing, and this must bring prices down. A mild downturn could thereby become a collapse, with consequences throughout the economy.

Tuesday, August 30, 2005

Damage: "Swimming in Crude, No Gasoline"

by Calculated Risk on 8/30/2005 07:49:00 PM

CBS MarketWatch exaggerates - a little:

"Americans could be swimming in crude, but wouldn't have a drop of gasoline to run their cars."UPDATE: Series of Port Fourchon photos

Wholesale prices of gasoline are already over $3.00 per gallon on the Gulf Coast:

Wholesale gasoline prices on the Gulf Coast broke $3 a gallon on Tuesday -- far higher than prices at most U.S. pumps -- as major refineries remained shut after Hurricane Katrina, trading sources said.There have been some relatively positive damage reports (also CBSMarketWatch):

This could spell a huge spike in retail prices for drivers throughout the United States in the coming days and in particular those in the Southeast, where prices are typically the lowest in the country.

...

"Retail prices are going to vary among regions but for all practical purposes $3 is a floor," said private oil analyst Jim Ritterbusch.

The spike could spread across other regions of the United States due to the shutdown of two fuel pipelines from the Gulf Coast to the Northeast, including the massive Colonial Pipeline.

"This tightness of supply in the Gulf Coast is going to spread," said Ritterbusch, of Galena, Illinois. He said the shutdown of a major fuel pipeline from the Gulf Coast to the Northeast could push prices up in other regions.

"This thing has tentacles that are going to stretch all over the place," Ritterbusch said.

The vital Louisiana Offshore Oil Port, the only U.S. port that can handle supertankers, apparently escaped major damage, the manager of the port told Dow Jones NewsWires.Also: BP says US Gulf oil rigs intact after Hurricane Katrina. But its the refineries that are critical in the short term. Of the 9 major refineries in the area, only Exxon Mobil's Baton Rouge facility is operational. And, as reported earlier, Valero expect to be out of operation for 1 to 2 weeks. Damage reports are expected tomorrow for some of the other refineries.

The major onshore port at Port Fourchon, also escaped major damage, according to Dow Jones NewsWires. The port is the base for oil service operations for oil rigs in the Gulf.

However, the channel leading to the port may have suffered severe silting from the storm surge. Dredging the channel could take weeks or longer. There could be a "very large impact to the energy supply," if the port can't reopen, port manager Ted Falgout told CNBC.

The Henry Hub, the junction of several pipelines in central Louisiana that serves as the pricing point for natural gas, reopened Monday afternoon. The condition of pipelines leading to the Henry Hub from the coast is not known.

The Economist: Katrina Could Tip US / World into Recession

by Calculated Risk on 8/30/2005 04:04:00 PM

The Economist ponders the impact of Katrina: The damage that Katrina could still wreak:

Besides its devastating cost in lives, Katrina could push the American economy—maybe even the world economy—into recession ...

Nor will the effects of Hurricane Katrina be limited to the Gulf Coast and the offices of a few agitated insurers. Analysts are busy rewriting their forecasts of America’s fourth-quarter GDP growth to take into account the expected economic repercussions of the devastation. The affected area’s ports move a large fraction of the nation’s imports—including critical oil and gas supplies—as well as roughly half its exports of agricultural commodities like corn and soyabeans. ...

Chief among the worries is the oil industry. The Gulf of Mexico provides about a tenth of all the crude oil consumed in America; and almost half of the petrol produced in the country comes from refineries in the states along the gulf's shores. Oil companies are busy assessing how much damage was done to drilling rigs, refineries and port facilities ... This is bad news considering that refineries have been running flat out in recent months to keep up with high demand. ... while much of the recent oil-price increase was demand-driven, and thus expected to have relatively benign economic effects, any outages owing to Katrina could cause a supply shock—meaning the kind of sudden, negative effects that battered the world economy in the 1970s.

As a rule of thumb, every $10 sustained increase in the price of a barrel of oil is estimated to result in a loss of something like half a percentage point of GDP. ... Some economists are worried that if there are extensive shutdowns of oil and gas production, this could push the economy to the brink of recession.

That is bad news abroad ... particularly ... Asia ... are already dangerously dependent on robust American demand for their exports. Those countries are also being hit by higher oil prices. Indonesia’s central bank was forced to tighten the money supply sharply on Tuesday ... While rich countries are much less dependent on oil than they used to be, thanks to increases in fuel efficiency and a shift from manufacturing to services, middle-income countries are still big energy guzzlers: India and South Korea use more oil per dollar of GDP today than they did in the 1970s.

Europe’s recovery could also be choked off in its infancy by the steady upward march of prices for petrol and heating oil. That would weaken another of Asian exporters’ main markets and leave the global economy little refuge if American demand were to stutter. If Katrina has damaged America’s capacity to pump and refine oil, forcing Americans to shop abroad for more fuel to feed their gluttonous appetites, it could be a long cold winter for everyone.

Monday, August 29, 2005

Katrina: Refinery Map

by Calculated Risk on 8/29/2005 11:46:00 PM

UPDATE3: Chevron says won't know full storm damage until Wednesday SAN FRANCISCO (AFX) --

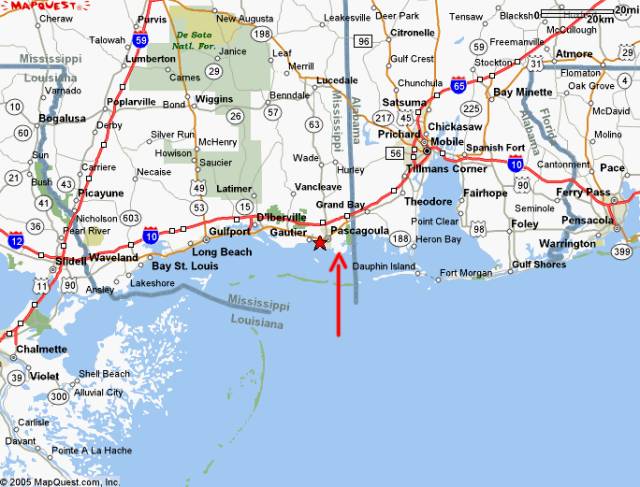

Chevron Corp. said Tuesday it will not know the extent of hurricane damage to its Gulf of Mexico oil and gas facilities until Wednesday. A Houston-based spokesman for the nation's second-biggest oil company said their aircraft were currently making initial damage assessments of offshore rigs and onshore facilities, including the 325,000 barrel-per-day Pascagoula refinery in Mississippi, which the company evacuated ahead of Katrina. Pascagoula is one of the biggest refineries along the Gulf Coast. Chevron evacuated 2,100 offshore employees and contract workers and shut its New Orleans office ahead of the hurricane. The company declined to say how much oil and gas output was shut by the stormUpdate: Here is a much better map. Thanks to Dr. Hamilton. (My Original Map removed)

Click on graph for larger image.

This map shows the location (arrow) of Chevron's Pascagoula facility. This is not on the Louisiana only map linked above.

UPDATE: "Exxon Mobil Refining & Supply Co.'s Baton Rouge, La. refinery - had not been affected by the storm or had resumed normal operations by late Monday."

| Number | Facility | Production 1000s bbl/day |

| 1 | Valero's St. Charles | 260 |

| 2 | Exxon Mobil Corp.'s Baton Rouge | 494 |

| 3 | Motiva's Convent | 255 |

| 3 | Motiva's Norco | 242 |

| 3 | Marathon's Garyville | 245 |

| 4 | ConocoPhillips' Belle Chasse | 247 |

| 4 | Murphy Oil Corp.'s Meraux | 125 |

| 4 | Chalmette Refining | 187 |

| 5 | Chevron's Pascagoula | 325 |

SOURCE.

Valero is the only facility to report:

Valero sees re-opening refinery in Louisiana in 1-2 weeks (VLO) By Carla Mozee

SAN FRANCISCO (MarketWatch) -- Valero Energy Corp. (VLO) said Monday evening that it expects to re-open its St. Charles refinery in Louisiana in one to two weeks. The company said that the refinery is now without power and that it may take two to three days for it to return. It also said that there is 3 feet of flood water in two units and that it may have to repair pumps, electric motors and electrical switchgear. Valero also sees minor damage to its cooling towers. The company said that no major damage is apparent and there's no evidence of spills or leaks.

Katrina: Oil and Gas

by Calculated Risk on 8/29/2005 06:57:00 PM

Luckily hurricane Katrina weakened before it came onshore and the "worst case" scenario was avoided, however there still appears to be severe damage and widespread devastation. My thoughts are with the victims of this massive storm.

Early estimates are that Katrina will be one of the most expensive hurricanes to ever hit the US. Although the damage is major, the economic impact on the United States will be from any significant damage to the oil infrastructure on the Gulf Coast. It will take some time to assess the damage to refineries, and oil and gas production facilities. We are starting to see stories like this:

Valero sees re-opening refinery in Louisiana in 1-2 weeks (VLO) By Carla MozeeAnd some good news on Natural Gas: Henry Hub reopens for delivery

SAN FRANCISCO (MarketWatch) -- Valero Energy Corp. (VLO) said Monday evening that it expects to re-open its St. Charles refinery in Louisiana in one to two weeks. The company said that the refinery is now without power and that it may take two to three days for it to return. It also said that there is 3 feet of flood water in two units and that it may have to repair pumps, electric motors and electrical switchgear. Valero also sees minor damage to its cooling towers. The company said that no major damage is apparent and there's no evidence of spills or leaks.

A potential crisis in the natural-gas markets was apparently averted Monday after the company operating the Henry Hub gas gathering facility said it avoided major damage from Hurricane Katrina and reopened the site for delivery and receipt.But a couple of cautionary comments from this story:

"After Ivan hit, the initial word was that it wasn't that bad." [said Bob Slaughter, president of the National Petrochemical and Refiners Association].

"Our goal is to get back up as soon as possible, but do it safely. It took almost a year to get back up to full production after Hurricane Ivan," [said Tony Lentini, spokesman for Apache Corp].Oil, natural gas and gasoline futures all soared as Katrina appeared to be the storm of the century, and settled back when the damage was less severe than initially feared. Still, from Friday's closing prices, oil is up 2%, gasoline 8% and Natural Gas 18%. On Friday, I pointed out that oil inventories were solid (see Dr. Hamilton's Supply factors in the 2005 oil price surge), but gasoline stocks were tight.

Click on graph for larger image.

This graph is from the DOE.

We will not know the extent of the damage to refineries for several days, but the US can expect a price spike at the pumps on top of already record gasoline prices. One prediction:

"One analyst said pump prices nationwide would likely average more than $2.75 a gallon by week's end — up from $2.61 a gallon last week"

Meanwhile crude stocks are robust and well above the average range. Plus the White House has suggested that oil could be released from the Strategic Petroleum Reserve if needed.

Meanwhile crude stocks are robust and well above the average range. Plus the White House has suggested that oil could be released from the Strategic Petroleum Reserve if needed.It is difficult to make any predictions, especially with stories of oil rigs adrift. But with above average oil stocks, it appears there will be no short term crude oil supply issues.

Gasoline is a different story. And there might be concerns about adequate heating oil supplies too.

Krugman: Greenspan and the Bubble

by Calculated Risk on 8/29/2005 01:54:00 AM

Dr. Krugman writes in the NY Times about Greenspan and the Bubble:

At the conference, Mr. Greenspan didn't say in plain English that house prices are way out of line .... What he did say ... that "history has not dealt kindly with the aftermath of protracted periods of low-risk premiums." I believe that translates as "Beware the bursting bubble."Then Dr. Krugman asks the question we've all been asking: How bad will it be?

But as recently as last October Mr. Greenspan dismissed talk of a housing bubble: "While local economies may experience significant speculative price imbalances, a national severe price distortion seems most unlikely."

Wait, it gets worse. These days Mr. Greenspan expresses concern about the financial risks created by "the prevalence of interest-only loans and the introduction of more-exotic forms of adjustable-rate mortgages." But last year he encouraged families to take on those very risks ...

The U.S. economy is currently suffering from twin imbalances. ... domestic spending is swollen by the housing bubble, which has led both to a huge surge in construction and to high consumer spending, as people extract equity from their homes. On the other side, we have a huge trade deficit ...

One way or another, the economy will eventually eliminate both imbalances. But if the process doesn't go smoothly - if, in particular, the housing bubble bursts before the trade deficit shrinks - we're going to have an economic slowdown, and possibly a recession. ...

A housing slowdown will lead to the loss of many jobs in construction and service industries but won't have much direct effect on the trade deficit. So those jobs won't be replaced by new jobs elsewhere until and unless something else, like a plunge in the value of the dollar, makes U.S. goods more competitive on world markets, leading to higher exports and lower imports.

So there's a rough ride ahead for the U.S. economy ....

Angry Bear: Housing and Recession

by Calculated Risk on 8/29/2005 12:14:00 AM

My most recent post is up on Angry Bear: Housing and Recession

Every time I sat down at my computer today, I found myself checking on hurricane Katrina. I am in shock. The residents of New Orleans are in my thoughts tonight. A couple of days ago I thought this storm might impact the already tight gasoline supplies, but I didn't think it would become a potentially catastrophic storm.

Hopefully the storm will weaken before landfall.

Best to all.

Sunday, August 28, 2005

Borrowing and Bankruptcy

by Calculated Risk on 8/28/2005 09:22:00 AM

The LA Times has two related articles this morning on borrowing and bankruptcy. From "Equity Is Altering Spending Habits and View of Debt":

People are cashing out so quickly that the term "homeowner" may soon be inaccurate. Fifty years ago, Americans owned, on average, three-quarters of their house and the lender owned the rest. These days, it's approaching an even split.This is behavior is being encouraged by industry "experts":

This spend-now-rather-than-save-for-later phenomenon has produced undeniable benefits. Experts attribute much of the nation's economic growth to cash-out refinancings, home equity loans and other methods of tapping rising home values.

"If you paid your mortgage off, it means you probably did not manage your funds efficiently over the years," said David Lereah, chief economist of the National Association of Realtors and author of "Are You Missing the Real Estate Boom?" "It's as if you had 500,000 dollar bills stuffed in your mattress."The entire article is fascinating, but this anecdote shows poor financial planning:

He called it "very unsophisticated."

Anthony Hsieh, chief executive of LendingTree Loans, an Internet-based mortgage company, used a more disparaging term. "If you own your own home free and clear, people will often refer to you as a fool. All that money sitting there, doing nothing."

The financial services industry is doing all it can to avoid letting consumers be foolish. Ditech.com touts home loans as a way to pay off credit cards, and Morgan Stanley says they're a good way to fund education expenses. Wells Fargo suggests taking a chunk out of your house to finance "a dream wedding."

He bought his condo in expensive Marin County, north of San Francisco, for $510,000 in April 2004. The bank offered to finance the whole thing, but he decided to be a little conservative and put 5% down.Although money is fungible, paying for short term assets with long term debt is poor financial planning. Imagine going to a fast food restaurant and buying a hamburger on your credit card. Then you borrow money against your house to pay off your credit card debt. Now you are financing lunch for 30 years!

By January, the condo was worth $555,000, and Levy refinanced. He took out $25,000 in cash, less than the bank offered to give him. The money paid off what he describes as "really ugly" credit card debt.

The interest rate on the credit card had been more than double the rate on his mortgage, so he saved about $600 a month. Furthermore, his mortgage interest is tax-deductible; his credit card interest was not.

"It used to be that all debt was created equal and all debt was evil," Levy said. "But the tax breaks alone make a pretty compelling case to use home equity to finance just about everything."

The other article in the LA Times, "A fresh calamity?", fits nicely with the first.

Under the new bankruptcy regulations, homeowners will no longer necessarily be able to hand the keys to the bank and move on. Lenders will, in many cases, have the option of coming after them for virtually everything else they've got -- income, money in bank accounts and other assets.For homeowners that are heavily in debt, and have refinanced or used a HELOC (Home Equity Line of Credit), this might be their future.

Homeowners who have refinanced may have unwittingly put themselves at the greatest risk. State regulations will still offer financial protections for buyers who have their original mortgages.

"There is no doubt this law will make it harder for some people to walk away," said Gary Painter, a professor at the USC School of Policy, Planning and Development. "It definitely could hurt homeowners."

I wonder who is going to look "foolish" and "unsophisticated" in the coming years.

Saturday, August 27, 2005

Greenspan: Closing Remarks

by Calculated Risk on 8/27/2005 06:38:00 PM

From FED Chairman Alan Greenspan's closing remarks at Jackson Hole, Wyoming:

"... the housing boom will inevitably simmer down. As part of that process, house turnover will decline from currently historic levels, while home price increases will slow and prices could even decrease. As a consequence, home equity extraction will ease and with it some of the strength in personal consumption expenditures. The estimates of how much differ widely."Emphasis added. I believe prices will decrease. And the following, on the relationship between home equity extraction and the currenct account (mostly trade) deficit, is important in how the imbalances will unwind:

"The surprisingly high correlation between increases in home equity extraction and the current account deficit suggests that an end to the housing boom could induce a significant rise in the personal saving rate, a decline in imports, and a corresponding improvement in the current account deficit."And part of Greenspan's conclusion is a little scary:

"Surely difficult challenges lie ahead for the Fed, some undoubtedly of our own making, and others that will be thrust on us by market or other forces."

Gasoline: Demand Strong, Inventories Drop

by Calculated Risk on 8/27/2005 12:03:00 AM

Gasoline stocks have continued to drop and are now near the bottom of the normal range.

Click on graph for larger image.

This graph is from the DOE.

It is possible that we might see a regional spike in gasoline prices unrelated to the price of oil. With possible major hurricane Katrina bearing down on the gulf coast, a drop in the already tight supply might occur.

The National Hurricane Center provides frequent updates on tropical storms. Although the exact location of landfall and intensity are difficult to predict, it appears Katrina will pass over extremely warm waters and make landfall in the Gulf Coast late Monday. This could disrupt several refineries including the 300,000 barrel-a-day Chevron Pascagoula, Mississippi facility.

Meanwhile demand for gasoline has remained strong.

This graph shows the Year over Year % increase in demand for:

1) Year to date.

2) Last 8 weeks compared to similar period last year.

3) Last 4 weeks compared to similar period last year.

(SOURCE: DOE)

Year to date demand for gasoline remains strong. For the shorter periods there is some normal variability, but there is no clear evidence of weakening demand for either period: the last 8 weeks and the last 4 weeks compared to 2004.

This is an update to an earlier post that discusses how the US economy has become more dependent on oil for transportation purposes as opposed to other uses of petroleum.

Friday, August 26, 2005

Dr. Leamer: Housing Has Peaked, Recession in '06

by Calculated Risk on 8/26/2005 05:20:00 PM

From an interview with FoxNews, Dr. Leamer Director of UCLA Anderson Forecast:

... the housing market appears to have peaked "in California and elsewhere. It will take more than a year for this weakness to turn into job losses and to affect the economy in general.Dr. Leamer believes the housing slow down will lead to a recession and will be felt everywhere:

And contrary to what a lot of so-called "experts" are predicting, Leamer, believes the pain will be felt on a national level, not just locally. As an economist he’s much more concerned about the broader implications of a slowdown in the housing market than about the price bubbles some areas are experiencing.And its not just housing - Dr. Leamer is concerned about the auto industry too:

"We’ve had ten economic downturns since World War II and eight of them started in the housing sector. It’s the first component of gross domestic product that starts to weaken," says Leamer. He keeps a close eye on what consumers spend on housing because it has a ripple effect, pointing out that a decline will lead to layoffs in construction, banking, and the real estate industry, to name just a few areas.

Leamer lays the blame squarely on the Federal Reserve for leaving interest rates too low for too long. Now, he says, we’re not only heading for trouble in the housing sector, but in the auto industry — another market that got drunk on historically low rates.Leamer's advice:

Low borrowing costs accelerated future sales by enticing consumers to trade up to bigger homes and new vehicles sooner than they might have done otherwise. ... As a result, car dealers lose the sale they would have gotten two years from now.

As rates creep higher, consumers happily driving their new cars or living in their larger homes have no motivation to purchase additional ones. Since consumer spending drives two-thirds of our economy, when consumers close their wallets, the impact is far-reaching.

While the real estate bubble itself may be all about "location, location, location," in Leamer’s view the coming housing slowdown will have national implications, although areas that have benefited most from the housing boom are likely to be hit hardest. For example, Southern California, where Leamer lives. He says the strong housing market "created a lot of jobs — in construction, in banking, in real estate. If that disappears, a basic driver for the local economy disappears." ...

If you’ve been shopping for a home, Leamer says you "need to recognize the risk and do some hard-nosed thinking" ... he suggests you add up all the monthly costs and benefits (such as tax deductions) of owning versus renting. If buying still makes sense, his advice is: "Think long term — seven to 10 years. Avoid adjustable rate mortgages. Lock in a low, fixed interest rate." ... "If you’re not sure you’re going to be living in the home in two to three years, don’t buy it."

Dr. Duy: More Rate Hikes

by Calculated Risk on 8/26/2005 03:33:00 PM

Dr. Duy discusses a wide variety of topics in today's Fed Watch. Dr. Duy thinks it is very likely that the FED Funds rate will reach 4.25% by the December FOMC meeting:

"... I see the calendar as supportive of another 75bp this year - which will come close to cutting the yield curve to zero unless long term rates start to move - and I see no indications from Fed officials to tell me that this story is wildly wrong."And Duy cautions that the markets may not be prepared:

"... one has to wonder if financial market participants are not entirely convinced that the Fed will continue to raise rates and narrow the spread, or, if the Fed did so to the detriment of the economy, it would quickly reverse course to support financial markets - the "Greenspan put." To me, the latter is not a given this time, especially in an environment of rising energy prices."Duy concludes:

"... regardless of the possibility of a recession in 2006, I still see the Fed as laying the groundwork for continued monetary tightening, even as they see the possibility that financial markets are not entirely prepared for that outcome."As usual, a very insightful look at the Fed's World View.

Dr. Duy's post: Fed Watch: Forecast Calls For More Rate Hikes

Greenspan on the Asset Economy

by Calculated Risk on 8/26/2005 11:02:00 AM

Greenspan spoke this morning at Jackson Hole, Wyoming. This weekend will see many stories on Chairman Greenspan, but here are a few relevant comments (My emphasis added):

The structure of our economy will doubtless change in the years ahead. In particular, our analysis of economic developments almost surely will need to deal in greater detail with balance sheet considerations than was the case in the earlier decades of the postwar period. The determination of global economic activity in recent years has been influenced importantly by capital gains on various types of assets, and the liabilities that finance them. Our forecasts and hence policy are becoming increasingly driven by asset price changes.

The steep rise in the ratio of household net worth to disposable income in the mid-1990s, after a half-century of stability, is a case in point. Although the ratio fell with the collapse of equity prices in 2000, it has rebounded noticeably over the past couple of years, reflecting the rise in the prices of equities and houses.

Whether the currently elevated level of the wealth-to-income ratio will be sustained in the longer run remains to be seen. But arguably, the growing stability of the world economy over the past decade may have encouraged investors to accept increasingly lower levels of compensation for risk. They are exhibiting a seeming willingness to project stability and commit over an ever more extended time horizon.

The lowered risk premiums--the apparent consequence of a long period of economic stability--coupled with greater productivity growth have propelled asset prices higher. The rising prices of stocks, bonds and, more recently, of homes, have engendered a large increase in the market value of claims which, when converted to cash, are a source of purchasing power. Financial intermediaries, of course, routinely convert capital gains in stocks, bonds, and homes into cash for businesses and households to facilitate purchase transactions. The conversions have been markedly facilitated by the financial innovation that has greatly reduced the cost of such transactions.

Thus, this vast increase in the market value of asset claims is in part the indirect result of investors accepting lower compensation for risk. Such an increase in market value is too often viewed by market participants as structural and permanent. To some extent, those higher values may be reflecting the increased flexibility and resilience of our economy. But what they perceive as newly abundant liquidity can readily disappear. Any onset of increased investor caution elevates risk premiums and, as a consequence, lowers asset values and promotes the liquidation of the debt that supported higher prices. This is the reason that history has not dealt kindly with the aftermath of protracted periods of low risk premiums.

Bill Maher: "But don't let me burst your bubble"

by Calculated Risk on 8/26/2005 01:03:00 AM

Bill Maher writes in the LA Times: But don't let me burst your bubble

You don't have to remember history, but you do have to remember Thursday. The bursting of the Nasdaq bubble was only five years ago. People lost a trillion dollars. And here we are today with real estate prices across the country that could aptly be compared to Courtney Love: irrationally high and about to collapse.Enjoy!

I don't want to say there's a housing bubble, but I had a refrigerator delivered this morning and a homeless guy offered me $3 million for the box. Not to burst your bubble, but all bubbles do burst. And we learned this recently. It's not just that grandma was alive the last time it happened. You were alive. Eminem was on the radio. Just like now because, again, it wasn't that long ago.

Thursday, August 25, 2005

Floyd Norris: "The real key to a housing bubble"

by Calculated Risk on 8/25/2005 06:52:00 PM

Floyd Norris, chief financial correspondent of The New York Times, has an interesting take on the housing market:

If housing prices fall, will mortgages cushion the downfall, or make it worse? Put another way, will more overstretched homeowners be forced to sell?Mr. Norris reviews previous housing slowdowns and contrasts housing, bought with mortgages, to stock, bought on margin. I recommend reading his comments.

At issue is whether financial innovations that have made it easier for Americans to buy homes have also made the system less stable and more vulnerable to shocks that could drive many of them from their homes, having lost all they invested in them.

The interesting and somewhat novel observation is that Mr. Norris believes we can tell, when housing starts to slow down, if it is an ordinary housing slowdown or a possible disaster by whether or not transaction volumes decline significantly for existing home sales.

But if and when a fall comes, watch the volume of home sales, particularly of existing homes. Back in 1978, almost four million sales of such homes were counted by the National Association of Realtors. By 1982, amid recession and rising interest rates, the figure was under two million.I've been expecting volumes to drop significantly (what Mr. Norris suggests is normal). Of course the "limited damage" would be a slow down in GDP growth or a mild recession.

...

If [then number of transactions] falls rapidly, that will be an indication that not much has changed, and the damage is likely to be limited.

But if sales volume stays high, that could indicate that the mortgage innovations are hurting. Then we could see rising numbers of foreclosures as homeowners discover they cannot sell their homes for what they owe but also cannot pay their suddenly higher monthly mortgage bills.

If volumes stay high while prices drop, Mr. Norris argues we are in for tough times.

Krugman: Housing Bubble will Burst

by Calculated Risk on 8/25/2005 02:46:00 PM

Reuters quotes Dr. Krugman:

"I'll give you a forecast which might very well be wrong, but I think it will burst in the spring of next year," he said at a derivatives conference in Brazil's winter resort of Campos do Jordao.I think it will be sooner rather than later.

"I would be surprised if it doesn't burst in the next three years," he added.

Krugman said skyrocketing U.S. housing prices were supported by large -- and somewhat "odd" -- capital inflows from emerging market countries, such as China, which has accumulated huge holdings of U.S. Treasury debt, helping keep long-term interest rates abnormally low.

"Americans pay for their houses with money they borrowed from the Chinese," he said.

...

An expected decline in U.S. housing investment would be part of an economic adjustment process which could include the weakening of the dollar, higher U.S. exports and the reduction of current account deficits in the world's largest economy, Krugman said.

"This is how we would like to see it happening -- smoothly -- but there are many moving parts and they're unlikely to move at the same time," he said. "So it's not going to happen unpainfully."

Wednesday, August 24, 2005

Housing Thoughts ...

by Calculated Risk on 8/24/2005 11:25:00 PM

Dr. Duy adds some interesting thoughts today: Another Look at Housing.

Like many others, Dr. Setser, Gen'l Glut, Paul Volcker to name a few, Dr. Duy expresses some concerns:

I was unsettled by the combination of weak durable goods numbers, strong housing numbers, and this morning’s Wall Street Journal piece regarding global capital flows into the US housing market. Like many, I see the need for an eventual rebalancing – a shifting away from consumption and housing and toward investment – of growth in the years ahead.Dr. Duy than adds some excellent analysis and graphs. I believe the graph showing the relationship between the CA (Current Account, mostly trade deficit) and housing starts is very interesting. Dr. Duy concludes:

All in all, it suggests to me that international factors – specifically, the willingness of foreign investors to place their capital into the US – have a significant place in explaining the consumption binge/CA deficit/low interest rate issue.The entire post is well worth reading.

...

Of course, the international angle only increases the difficulty of the Fed’s job – the willingness of foreign capital to flow into the US could mean the Fed will end up strangling the non-housing sectors of the economy to keep overall inflation expectations in line.

And on today's numbers, I plotted the New Home Sales for July for the last 30 years (annual rate, seasonally adjusted).

Click on graph for larger image.

The vertical lines indicate the start of a recession.

With the increasing Existing Homes inventory and this very strong New Home Sales report for July, more and more I think this looks like a blow off top for housing. I probably could have written that last year too, but I didn't see the widespread speculation (especially speculation with riskier financing).

I believe there is a relationship between housing, trade and interest rates, and when that starts to unwind, we may see a vicious cycle on the downside.

Tuesday, August 23, 2005

July New Home Sales: 1.41 Million

by Calculated Risk on 8/23/2005 08:10:00 PM

According to a Census Bureau report, New Home Sales in July were at a seasonally adjusted annual rate of 1.41 million vs. market expectations of 1.35 million. June sales were revised down to 1.324 million from 1.374 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in July 2005 were at a seasonally adjusted annual rate of 1,410,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

The Not Seasonally Adjusted monthly rate was 120,000 New Homes sold, up from a revised 117,000 in June.

The median sales price of new houses sold in July 2005 was $203,800; the average sales price was $275,000.

The average sales price rebounded slightly and the median price is the lowest since 2003.

The seasonally adjusted estimate of new houses for sale at the end of July was 460,000. This represents a supply of 4.0 months at the current sales rate.

The seasonally adjusted supply of New Homes was 4.0 months, about normal for the last few years.

July was a record for sales, but recently the trend has been for downward revisions and July will probably be revised down. Even though inventories are at a record high, with the strong sales, the months of inventory is normal for the last few years.

Median prices continue to fall and are now at 2003 levels.

Shiller Defines a Bubble and Probable Ending

by Calculated Risk on 8/23/2005 07:41:00 PM

Here are some excerpts from a FoxNews interview with Yale Economist Robert Shiller said:

Shiller admits he doesn’t have a short, simple definition and then goes on to say that defining a bubble "is similar to the way psychiatrists define a mental illness, that is, it involves a list of symptoms."And Shiller expects the end to be ugly:

Indeed, to hear Shiller describe a financial bubble it sounds like a disease. "It’s a social contagion," he says, "An epidemic whose mode of transmission is word of mouth. It’s emotional. People keep hearing about price increases. There’s a tinge of envy about other people who have done well, which brings more and more people into the market. This, in turn, pushes prices up." In other words, it's a self-fulfilling prophecy.

... the most important issue is not whether or when the bubble will burst, but what the "end" will it look like. Shiller confesses he has no idea. He says a lot depends on the other factors or "symptoms" in the mix.

In the extreme scenario, buyers start to default on adjustable-rate mortgages and trigger a financial crisis in the banking sector. Real estate prices nosedive as properties are abandoned. If this is compounded by significantly higher oil prices, "it could change the psychology," says Shiller. "Consumer confidence plummets and people pull back on spending." This causes a downward economic spiral and leads to recession.

In the "soft landing" version, real estate prices simply remain flat for years, much as they did after the boom in the 1970s, until they’re back in line with inflation. "This is what people are counting on happening," says Shiller. He considers this outcome unlikely "because the signs of a bubble are stronger."

Though he admits there are so many variables it’s impossible to forecast it precisely, Shiller says he senses that the housing bubble is "more likely to turn out badly."

July Housing Inventories

by Calculated Risk on 8/23/2005 11:13:00 AM

The National Association of Realtors reports that existing home inventories rose to 2.751 in July from 2.653 million in June. Since sales remained strong (7.16 million units vs. 7.33 million annual rate for June), the months of supply only increased to 4.6 months from 4.3 months in June.

Both numbers were better than I expect (sales were higher, inventory lower). They indicate a return to a more "normal" market and not the end of the housing boom - yet.

Year over year (July '04 to July '05) this is a 12.6% inventory increase.

Update: From Bloomberg:

"We are starting to see more houses coming into the market," and that is a sign of a turn, Harris said. "First you see inventories rising, then you see a flattening of prices and then you start to see people have difficulty selling houses because buyers have more options and they get more demanding."

A total of 2.75 million homes were for sale last month, the most since May 1988.

Bruce Bartlett: Bubble fever

by Calculated Risk on 8/23/2005 01:48:00 AM

Bruce Bartlett, in an article for Townhall.com discusses "Bubble fever". Although Barlett does not take a position, he writes:

Today, many of the same economists who correctly predicted the bursting of the stock market bubble, such as Yale University's Robert Shiller, are saying that the housing market is in a bubble. If it should collapse as the stock market did, the impact could be even more painful. Consider this evidence.

-- Homeowners are much more leveraged than they used to be. According to the Federal Reserve, Americans' home equity has fallen to 56.3 percent of their real estate, from 75 percent a generation ago. Another Federal Reserve study found that 16 percent of the money taken out was simply consumed.

-- According to Freddie Mac, people are taking more and more money out of their homes. Cash-out refinancings have risen to 18.1 percent of all refinancings, from 7.2 percent in 2003. In the last four years, homeowners have taken $559 billion in equity out of their homes.

-- More and more homeowners are buying and refinancing with unconventional loans, such as adjustable-rate and interest-only mortgages, rather than traditional fixed mortgages. Such loans have lower initial payments, but will rise automatically when interest rates rise. The Federal Reserve says that 47 percent of all residential mortgages by dollar volume are now non-traditional.

-- A new study by National City Bank found 53 cities in which home prices were in bubble territory -- defined as 30 percent above where they should be based on local income growth, population density and other factors. Santa Barbara, Calif., ranked as the city with the most overpriced real estate -- 69 percent above fundamental value. Based on the ratio of rent to home prices, prices nationally are now almost 40 percent above where they should be.

-- A new study by the Public Policy Institute of California found growing numbers of homeowners paying as much as 50 percent of their income for housing, including mortgage, taxes, insurance and utilities. In California, 15.4 percent of homeowners fall into this category -- including 20 percent of recent homebuyers -- and 10.6 percent nationally. Almost 40 percent of Californians pay at least 30 percent of their income for housing, with 29 percent doing so nationally. According to Fannie Mae, 28 percent is the most one ought to pay.

According to the National Association of Realtors, 23 percent of homes last year were sold as investments, and another 13 percent were vacation homes. With rapid appreciation being a prime motive for both, any falloff in housing prices could cause many of these properties to be dumped on the market quickly, potentially turning a housing downturn into a crash.

Study: Foreclosures Costly to City

by Calculated Risk on 8/23/2005 12:32:00 AM

The Denver Business Journal reports on a new study by University of Colorado-Denver graduate student Christi Icenogle showing that foreclosed properties are costly to a city. After reviewing the direct costs to the city, the article points out that the combination of "loose" financing and slow appreciation has apparently led to higher foreclosure rates in Denver:

Foreclosure rates have been increasing in Denver, [Zachary Urban, Brothers Redevelopment Inc., a housing counseling nonprofit] said, partly because of adjustable rate mortgages with increasing payments over time, and partly because of job losses. He foresees foreclosures continuing to rise as interest-only loans come home to roost.When housing slows, this could become a widespread problem.

Phil Heter, broker/owner of Arvada-based Heter & Co., said he's also been seeing foreclosures increasing, and thinks it's because of loose qualifications on home financing.

"Most of it is 100 percent financing," said Heter, whose Web site is REODenver.com. With no money down and low appreciation, the owners may have little, no, or negative equity in the house and "have a tendency to walk," he said.

In metro Denver, looking at basic homes for first-time homeowners, Heter estimated appreciation was 1 percent last year, and "that's being generous."

Lower appreciation tends to make foreclosure rates higher because the lack of increase in value makes it tougher to sell the home for more than the amount owed.

A related problem for local governments, discussed at the The Housing Bubble, is that revenues have been increasing rapidly for cities in boom areas. But the local governments are, in the opinion of Scott Ellis, Brevard County, Florida Clerk of Courts:

"... dangerously sinking much of the newfound windfall into recurring expenses, mainly raises and additional employees. When the real estate bubble pops, the tax rolls will march backwards ... there will be weeping and gnashing of teeth by the time next tax year rolls around."When housing slows, it appears costs will be rising and revenues falling for cities and local governments.

Monday, August 22, 2005

Reuters: 40 Year Mortgage "Risky"

by Calculated Risk on 8/22/2005 04:18:00 PM

Reuters reports: Stretching mortgage to 40 years can be risky

"This (40-year) loan product screams of a budget-constrained consumer desperate to get into a home," says Gary Schatsky, a fee-only financial adviser/attorney. "This trend is disturbing to me, especially since it feeds into the growing obsession by consumers to get credit.I think a 40 year fixed rate loan is better than an option ARM. But I do agree that they are symptomatic of desperate "budget-constrained consumer[s]" trying to buy a home.

"They need to think through this mortgage's implications because in many cases, it will become their children's mortgage," says Schatsky, who is based in New York.

... Bankrate.com, notes that interest rates on 40-year mortgages are generally 0.25 to 0.50 percentage point higher than on traditional fixed 30-year loans. That difference negates some of the benefits of the lower monthly payment.Here is an example: A $300K 30 year loan with an average Freddie Mac interest rate of 5.8% has payments of $1,760.26 per month.

For the same amount financed for 40 years with a 0.375% higher rate, the payment is $1,687.38. A buyer has to be desperate to pay the higher interest rate for that small reduction in monthly payments.

"This all stems from affordability and borrowers stretching themselves beyond their reach to get into a home they can't afford," says Economy.com's Chen. "What's next, a 50-year loan?"

Recent anecdotal evidence indicates that home price increases are beginning to decelerate, a sign the housing sector is starting to cool.

"When housing cools, so will these loans," Schatsky says. "If a consumer has to take out this loan to qualify for a home, their goal of homeownership needs to be seriously re-evaluated."

Merrill Lynch: Housing Prices Poised to Decline

by Calculated Risk on 8/22/2005 11:43:00 AM

Reuters reports:

Prices in the hot U.S. housing market are poised to decline as demand dries up due to the inability of first-time buyers to afford a home, a Merrill Lynch analyst said in a research report on Monday.

"The housing market has become so stretched that the affordability ratio for first-time buyers, the folks who drive the incremental demand in the real estate sector, has deteriorated to levels last seen in the third quarter of 1989," wrote David Rosenberg.

The price of an average starter home in the United States has climbed 14 percent over the past year, while the average income for the first-time buyer family has risen just 4 percent, Rosenberg said, calling that an "unprecedented gap."

In the third quarter of 1989, bids evaporated and new home sales dropped 20 percent the following year in response to lofty prices that first-time buyers could not afford, the analyst said.

The inventory of unsold new homes rose to a 8.4 months' supply from 7.1 months' and that inventory buildup led to a 5.8 percent drop in the median price of a new home, he said.

Sunday, August 21, 2005

Sign, Sign, Everywhere a Sign

by Calculated Risk on 8/21/2005 09:06:00 PM

My most recent post is up on Angry Bear: Signs of the Times.

"Sign, sign, everywhere a sign

Blockin' out the scenery, breakin' my mind"

Signs, Five Man Electrical Band

Click on photo for larger image.

Orange County, CA Aug 21, 2005

This photo shows four houses in a row for sale. Two spec houses are being built, the one on the left nearing completion, has a "For Sale by Owner" sign.

For the 3rd and 4th houses, I've blown up the offering signs (upper right corner). The 3rd house is an older home with a For Sale / For lease sign. The last home is a newer resale with a small sign reading "New Listing".

Although three or four listings in a row is rare, a house for sale on every block is common. And when I drove around my neighborhood this morning, there was an open house sign on almost every corner. This may just be a temporary surge in inventories, but it feels like a sea change.

Saturday, August 20, 2005

Housing Bagholders: "Wall St. Waits to See What Will Be Repaid"

by Calculated Risk on 8/20/2005 10:53:00 PM

The Los Angeles Times reports: Wall St. Waits to See What Will Be Repaid

The financial services industry has made it possible for millions of Americans to stop thinking, "I can't afford that."Food for thought (or concern). If investors pull back, yields will rise and a housing decline will be a self-fulfilling prophecy. But where will those investors move their money? Ten year treasuries yielding 4.2%?

Now, Wall Street is beginning to wonder how many people really couldn't afford what they bought in recent years on incredibly cheap credit.

One-percent mortgage loans, zero-percent car loans, home-equity loans for more than what your property is worth — all of this has been the cushy financial reality for U.S. consumers in this decade. No house, car or vacation has been out of reach, thanks to a network of eager lenders and the global army of investors who've supplied them with capital at rock-bottom rates.

In the midst of any wild party, however, some people do things they later come to regret. And while talk of a housing bubble has been incessant over the last year, only now are the money handlers on Wall Street beginning to worry about payback — that is, how much of the credit extended in this borrowing extravaganza won't be paid back.

...

Home mortgage and equity line-of-credit debt has swelled from $4.8 trillion at the end of 2000 to nearly $8 trillion now. And behind every borrower there's a lender.

Which raises the question: How fast will investors in financial company stocks and in mortgage-backed bonds rush to sell, if they begin to sense that a wave of loan defaults is inevitable?

Richard X. Bove, a veteran banking industry analyst at the firm of Punk, Ziegel & Co. in New York, last week sent clients a research report with a chilling title: "This Powder Keg is Going to Blow."

...

The biggest threat of upheaval is in the mortgage-backed securities market itself.

That market, worth nearly $4 trillion, has provided much of the capital for the housing boom. Instead of holding on to the loans they make, many lenders package them and sell them to investors worldwide via mortgage-backed bonds. The bond owners get the loan interest and principal passed through to them.

The genius of the mortgage-backed securities market is how it has been sliced and diced by investment bankers. There's a piece of a mortgage to match every investor's need — long-term and short-term paper, high yield and lower yield, insured and uninsured.

But the increasing complexity of the securities also raises the risk that some investors will feel they can't be sure exactly what they're holding, particularly in the case of bonds backed by the new wave of adjustable-rate mortgage loans. If investors begin to worry that they won't be repaid, their rush for the exits could be thunderous.

"Securitization shifts risks from banks to other investors, but this does not necessarily mean less systemic risk [to the economy and markets] because we don't know how these relatively new market participants will react in a declining market," Joseph Abate, a senior economist at brokerage Lehman Bros., said in a report to clients Friday.

Friday, August 19, 2005

NAR Cautions Buyers on Specialty Loans

by Calculated Risk on 8/19/2005 03:18:00 PM

The National Association or Realtors (NAR) cautioned homebuyers on certain loans today:

Homebuyers may not realize that monthly payments on some types of specialty mortgages can increase by as much as 50 percent or more when the introductory period ends.I suppose late is better than never. Just yesterday I posted excerpts from: Home buyers get comfy with debt. I suspect some of those buyers are going to wish they had been "cautioned".

...

"Consumers are susceptible to loans with monthly payments that can spike dramatically, or that actually increase the amount they owe on their home." NAR President Al Mansell of Salt Lake City.

...

"We’re warning homebuyers to approach these new mortgages carefully," says Mike Calhoun, general counsel for the Center for Responsible Lending. "They should be cautious about accepting a mortgage they can’t afford. These mortgages can be devastating for families who are stretching their budget to buy a home."

"Consumers particularly need to understand the risks inherent in specialty mortgages when financing a home purchase," says David Lereah, NAR’s chief economist.

Housing: "'For Sale' Signs Mushroom"

by Calculated Risk on 8/19/2005 12:32:00 PM

The Sacramento Bee reports: Region's home sales signal softer market.

Jim Eggleston, owner of Sacramento's biggest residential "For Sale" sign installer, predicts this will be his busiest week in 21 years in business. He's had to hire an extra worker and buy a new delivery truck since his crew planted a one-day record of 225 signs on Monday.In my neighborhood, I see the same phenomenon. And the Desert Sun (Palm Springs, CA) reports:

"There are whole lot of houses going up for sale," says Eggleston, who promises next-day installation when a real estate broker orders a new sign. "The number of 'For Sale' signs we're removing keeps going down relative to the number we're putting up."

Price rises come as local sales counts have recently been falling, and the inventory of unsold resale homes is up dramatically from a year ago.Next week nationwide existing home inventories for July will be reported. Should be interesting.

According to DataQuick, the total 1,259 new-construction and resale homes sold in July was down 12.1 percent from a year ago.

And unsold resale inventory is currently at around 3,452 properties, according to Greg Berkemer, executive vice president of the California Desert Association of Realtors. That figure is up 63 percent from a year ago and is more than twice the 1,400 seen in April 2004.

Thursday, August 18, 2005

Oil's Impact on the Economy

by Calculated Risk on 8/18/2005 08:16:00 PM

Several blogs are commenting on oil's potential impact on the economy. First a quote:

"People are able to pull money out of their homes and put it into their gas tanks," said Mark Zandi, chief economist at Economy.com. "So the overall effects on consumer spending have been small."Mortgage extraction to purchase consumables is probably not a viable long term strategy. Dr. Roubini comments:

Until now consumers have reacted to the oil shock as if it was a temporary shock: when a shock to real income is temporary it is optimal to maintain the consumption level and reduce savings in face of reduced real income. But if the shock is persistent or permanent the rational response to the reduced income should a reduction in consumption equivalent to the permanent reduction of income with little effect on savings. U.S. consumers have reacted so far to the oil shock as if it was temporary and they have further reduced their savings rate down to zero; but two years of large and protracted increases in oil prices suggest that part of the shock is permanent. With already stretched and slow-growing incomes, U.S. consumer have dipped into their rising housing wealth and borrowed more and more against it, in part to finance the real income shock from higher oil prices.Professor Hamilton expresses concern that consumer psychology might be changing:

In my opinion, the reason that the oil price increases of the last two years have not caused a recession yet is that they have built up gradually, and resulted not from a drop in supply but instead from strong global demand. Faced with a gradual price increase and rising incomes, most people have been able to adapt to the higher prices and make adjustments in an orderly way that does not cause serious economic dislocations.Barry Ritholtz, who is already predicting a recession in 2006, also comments on consumer psychology:

On the other hand, just within the last couple of weeks, I've been hearing a lot more expressions of anxiety and concern-- the sort of psychological factors that produce abrupt spending changes.

While Oil may be a much smaller percentage of GDP today than it was in the 1970s, the relative financial conditions of indebted consumers may also be that much less able to absorb an extended shock than it was then.And as usual, I provide a few graphs over on Angry Bear. Dr. Roubini concludes:

...

Record high gasoline prices, that fall back a little but stay inflated; Add a housing boom that doesn't crash, but merely fizzles. The ongoing refinacing machine which drove so much consumer spending decellerates rapidly. Add to it a War which the majority of the country now believes turns out to be "Not worth it" and a significant percent (though not quite a majority) beleives we were led into under "false premises." Lastly, the myriad stimulus from the government -- tax cuts, ultra low interest rates, deficit spending, increased money supply, military expenditures -- all begin to fade.

What might all this a recipe for?

Is there a risk of an outright recession? Probably not as consumption is still firm and labor market conditions are modestly improving. But a significant U.S. growth slowdown by year end to a level below the 3.5% U.S. potential growth rate cannot be excluded: growth slumping towards the 2.0-2.5% range by early 2006 cannot be ruled out if oil prices remain at current level. And the expectation that the Fed may ease in face of such economic slowdown may prove incorrect: with a housing bubble and a large current account deficit and a core inflation rate that may be creeping soon above 2% the Fed may not be able to afford to ease if the economy slows down. In 2003 when the concerns were about deflation, the Fed reacted to the pre-Iraqi war oil spike and economic slowdown by reducing the Fed Fund rate to 1%. Today, with inflationary pressures modestly creeping up the Fed would face a much tougher dilemma if the latest oil shock turns to be, as likely, stagflationary.I have a similar view (from my AB post): My view (not Angry Bear) is a combination of a housing slowdown and high energy prices will probably lead to an economic slowdown next year, and possibly a recession.

So, if oil prices remain at the current levels or increase further there is not yet the risk of an outright recession but certainly a high probability of a significant economic slowdown by year end and into 2006.

EDAB/UCLA July Report

by Calculated Risk on 8/18/2005 02:11:00 PM

Economic Development Alliance for Business (EDAB) presents a monthly economic report for the East Bay (Northern California). Christopher Thornberg, Senior Economist for UCLA Anderson Forecast is the author. A few excerpts:

(Hat tip to Brian Smits who sent me this report)

"... unfortunately there is a big problem brewing out there that is unlikely to go away quietly: the massive run-up in real estate prices across the state. Housing prices have continued to grow at a truly spectacular rate across the state and again in the Bay Area. Rampant speculation continues to fuel the fire as investors have seemingly already forgotten the lessons learned so hard in the last major asset bubble that ended not even five years ago. While there are those who try and rationalize the rapid increase in prices, we see no justification for these increases—the fundamentals that drive the price of a housing asset have been pointing to a cool market, not a hot one. Rental growth remains weak, mortgage rates have been rising slowly, and contrary to common belief the pace of home building in the area is completely in line with the growth of the workforce—the so-called housing shortage does not exist. Yes, inventory levels are low but this is due to frantic behavior of buyers."But Thornberg believes the economic problems are a year away:

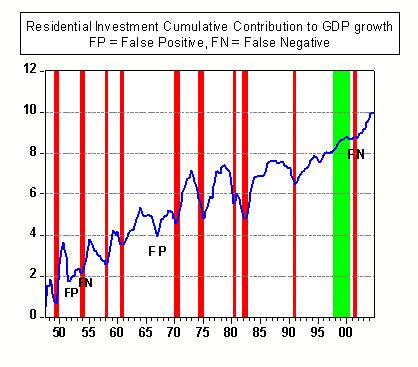

"There are some preliminary data that show what may be the beginning of the cooling of the market. But a major slowdown is at least a year away, if not more. Expect the recovery to continue well into 2006 and job growth in the East Bay to pick up speed during these 12 months. The end of 2006 or early 2007 will be the beginning of trouble, however."Thornberg presents the following graph showing that housing slowdowns have preceded eight of the 10 recessions since WWII.

Click on graph for larger image.

New Home Sales is one of my favorite leading indicators. Here are a couple of posts: New Home Sales as Leading Indicator and Update: New Home Sales as Leading Indicator.

I'm looking for a drop in housing transaction as an indicator of an economic slowdown and possible recession in '06. Thornberg also thinks its too early to predict a recession and compares the late '80s slump (leading to the early '90s recession) to today.

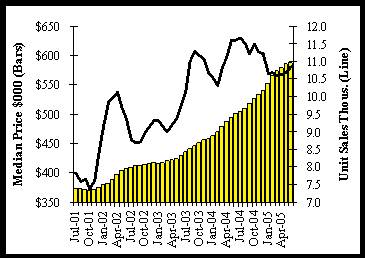

"The ... chart shows unit sales and median prices at the end of the late eighties run-up in prices. Market activity peaked in the end of 1988, and price appreciation began to slow within 6 months, and stopped within 18. So keep an eye on market activity, since this will be the first sign of impending problems. More recently unit sales have begun to fall, and you can see some slowdown in price appreciation. This may not be completely convincing evidence since you can see a similar slowdown in 2002 that quickly reversed itself. Of course this time prices are higher and more out of whack relative to income, and interest rates are rising rather than falling. This makes it considerably more likely to be the beginning of the end."

"... as of now the bubble continues to expand. And while there are certainly signs that we are past the peak in this state, activity remains at a historically high pace. There is almost no chance of a major economic slowdown in the next 12 months for the nation ..."There is much more in the report.

Homeowners Debt: "45% of Income not Uncommon"

by Calculated Risk on 8/18/2005 11:24:00 AM

The Mercury News reports: Home buyers get comfy with debt.

One out of five recent buyers have committed more than half their total earnings to homeownership, according to a new study. Slightly over half of home buyers in the past two years spend more than 30 percent of their total income on housing, exceeding a level recommended by the U.S. Department of Housing and Urban Development.If I remember correctly, the limits for borrowers with perfect credit were approximately 33% of income for housing and 40% of income for total debt not long ago. Now one in five of recent buyers are over 50% just for housing. That seems like extremely loose lending practices.

Because the study was based on data from 2003 and 2004, the situation now can only be worse because home prices have continued to rise dramatically since then.

The Public Policy Institute of California, in a study released today, reports that Californians are strategizing and willing to be house poor as never before.Here is the PPIC report: California's Newest Homeowners: Affording the Unaffordable

...

They've been helped by low interest rates and lenient lenders. But more than anything, their success in buying homes results from being inventive and ready to spend an awful lot of their earnings on owning a home.

Port of Los Angeles: Imports Up 5% over June

by Calculated Risk on 8/18/2005 12:46:00 AM

The Port of Los Angeles released their July statistics today. Inbound (loaded containers) was 352 thousand compared to 334 thousand in June - an increase of 5%.

Outbound volume was 97.5 thousand loaded containers vs. 96.6 thousand for June. This is an 1% increase from June.

Port of Long Beach traffic indicated a slight decline in imports for July. Looking at both numbers, I expect imports from China to be flat or off slightly from June to July.

NOTE: The OffPeak initiative (adds late night hours to port operations) started on July 23rd to handle the expected heavier late summer / fall imports.

Wednesday, August 17, 2005

Freddie Mac: Cash-Out Volume Prime Conventional Loans

by Calculated Risk on 8/17/2005 11:26:00 PM

Here is a table of the cash out volumes (according to Freddie Mac) since 1993 (note numbers don't exactly match earlier post - these are the revised numbers):

| YEAR | Equity Extraction | Equity Extraction |

| Billions ($) | Plus 2nd/Heloc $B | |

| 1993 | $19.9 | $39.3 |

| 1994 | $13.8 | $29.2 |

| 1995 | $11.2 | $21.7 |

| 1996 | $17.4 | $34.5 |

| 1997 | $21.4 | $39.1 |

| 1998 | $39.9 | $72.4 |

| 1999 | $37.0 | $71.1 |

| 2000 | $26.2 | $60.4 |

| 2001 | $82.9 | $135.5 |

| 2002 | $111.1 | $170.5 |

| 2003 | $146.9 | $224.4 |

| 2004 | $139.6 | $182.0 |

| 2005(est) | $161.7 | $200.0 |

| 2006(forecast) | $68.7 | $93.6 |

Freddie Mac reports that equity extraction was $102 Billion for the first 6 months of 2005 (they estimate $161.7B for the year).

Some of the surge in the late '90s was attributed at the time to borrowing to invest in the NASDAQ stock bubble. People were concerned by the large jump in equity extraction, especially in '98 and '99. Seems inconsequential now.

The projected drop off next year (of $100 Billion) is approximately 0.8% of GDP (GDP will be over $12 Trillion in '06).

DiMartino:Housing froth still bubbling

by Calculated Risk on 8/17/2005 09:47:00 PM

Danielle DiMartino surveys this week's housing stories for the Dallas Morning News: First the National Association of Home Builders survey:

The housing market index of the National Association of Home Builders declined three points to 67 in August.On the FED and lending standards:

...

"This relationship suggests to us that the purchases of new homes could turn soft in the near term," Northern Trust economist Asha Bangalore wrote recently.

... the Federal Reserve's latest Senior Loan Officer Opinion Survey, it was apparent that, as the Bank Credit Analyst put it, "The Fed speaks but banks don't hear it."And on the Housing ATM:

A quick history lesson: In the past, bankers tightened up lending standards to match the degree of Fed tightening.

"This makes sense, because rising rates boost the odds of loan defaults," the BCA noted. "This time, banks are ignoring the Fed. The new survey shows an increasing willingness to make consumer loans."

...fresh news out of mortgage giant Freddie Mac on Americans' insatiable appetite for cash to fuel their runaway spending habits.... Thanks more to increasing home values than interest rates, in the first half of this year, cash-out refinancings have totaled a record $102 billion.And from Freddie Mac:

Total equity cashed out in the second quarter is estimated at $59 billion, up from the revised cash-out estimate for the first quarter of 2005 of $43 billion.Home Equity Extraction:

... homeowners extracted $140 billion in home equity through first lien refinances in 2004."

2001: $83 Billion

2002: $96 Billion

2003: $139 Billion

2004: $140 Billion

2005: $102 Billion (first 6 months)

From former Fed chief Paul Volcker (quotes and video link - worth a repeat):

"Altogether, the circumstances seem as dangerous and intractable as I can remember."

"Boomers are spending like there is no tomorrow."

"Homeownership has become a vehicle for borrowing and leveraging as much as a source of financial security."

More on Labor Slack

by Calculated Risk on 8/17/2005 03:07:00 PM

Responding to an earlier post, Ken Melvin directs us to some comments in an article in the SF Gate: Want a Wal-Mart job? Join the crowd 11,000 apply for 400 openings at retailer's new Oakland store.

"It's not about Wal-Mart -- it's about the rest of the labor market," [Stephen Levy, an economist for the Center for Continuing Study of the California Economy] said. "If the rest of the labor market was strong, you wouldn't have 11, 000 people applying for 400 jobs."That sure sounds like slack in the labor market.

During the dot-com boom, Levy said, businesses like Starbucks bumped up wages to recruit employees in the middle of a hot job market. But now the situation has reversed, and more people are willing to take whatever they can get.

On the same topic, MaxSpeak has another post today: Measured for Slack. This was a follow-up to the WSJ Econoblog yesterday with Dr. Altig of Macroblog discussing the labor market with MaxSpeak's Max Sawicky and Tom Walker. If you haven't already, check out the WSJ Econoblog: Debating Job-Market 'Slack'.

WSJ: Three on Housing

by Calculated Risk on 8/17/2005 11:32:00 AM

The WSJ covers housing today:

How Will Home Boom End? Even If Prices Don't Collapse, Some Owners Will Feel Pain; Big Mortgages, Little Equity

Near nation's capital, a hot market cools

The Energy in Real Estate, By John Makin, Wall Street Journal Editorial Excerpts can be found at EconomistView. (Thanks to Dr. Thoma)

Dr. Leamer: "Smells" like Housing Turning Point

by Calculated Risk on 8/17/2005 12:00:00 AM

Dr. Leamer, economist and UCLA Anderson Forecast Director, said today:

"It's going to take several more months of information before we know whether this month was the turning point, but it sure smells like it,"I agree. I'd like to see an increase in inventories, a drop in sales and the flattening of prices over several months before I call the top - but it sure "smells like it" right now.

Leamer said he suspects the affordability crunch is putting the brakes on San Diego's market, where the annual price appreciation has tumbled from the 30 percent range last year to 5 percent this year.Columnist Bonnie Erge expressed my view succinctly in Waiting for the Bubble to Burst:

"Rising interest rates are making it just a little less affordable for certain home buyers, and when you pull out that fraction of buyers in a fragile market, that might be enough to turn the thing around," Leamer said

It's bubble-bursting time, if you ask me.

Tuesday, August 16, 2005

Job Growth: Bush's 2nd Term

by Calculated Risk on 8/16/2005 10:25:00 PM

The online world receives another treat today as Dr. Altig of Macroblog discusses the labor market with MaxSpeak's Max Sawicky and Tom Walker. Check out the WSJ Econoblog: Debating Job-Market 'Slack'.

I'd like to make my own small mundane contribution. In January I cut Mr. Bush some slack with regards to job creation during his first term. Bush's first term, with a net loss of 759K private sector jobs (a gain of 119K total jobs), has to be considered disappointing. However there were some reasons for the poor net job creation, the most compelling being that the economy was clearly overheated when Bush took office.

Looking forward there are no clear reasons why the US economy shouldn't see more normal job growth during Bush's 2nd term. With the economy adding 1.7 million working age people per year (according to the Census Bureau), the US economy should expect a minimum of 6.8 million net jobs created during Bush's 2nd term.

On the upside, the participation rate could increase and the economy could add close to 10 million net jobs. This is a realistic upside; the economy added 10.8 million jobs in Reagan's 2nd term and over 10 million jobs during each of Clinton's terms in office. The economy is larger today, so as a percentage gain, 10 million jobs would be less than for the Reagan or Clinton presidencies.

So for Bush's 2nd term, anything less than 6.8 Million net jobs will have to be considered poor. And anything above 10 million net jobs as excellent. Of course, in additional to the number of jobs, the quality of the jobs and real wage increases are also important measures.

For the quantity of jobs, the following graph provides a measurement tool for job growth during Bush's 2nd term.

Click on graph for larger image.

The blue line is for 10 million jobs created during Bush's 2nd term; the purple line for 6.8 million jobs. The insert shows net job creation for the first 6 months of the 2nd term - currently just below the blue line.

I will update the graph each month.

Housing, Housing, Housing

by Calculated Risk on 8/16/2005 02:41:00 PM

For those that need more housing stories, I recommend the following sites:

UPDATE: Also REOWire Stories and commentary. "insight for the default servicing industry"

Patrick's Housing Crash Blog (story links)

Housebubble.com (story links)

Ben Jones' The Housing Bubble 2 (Commentary)

Prof. Pigginton's Econo-Almanac Based in San Diego.

And writing of San Diego, here are two articles on San Diego housing:

As housing slowdown takes hold in San Diego, experts differ on depth